VET - Vermilion Energy: Capital Return And Regulatory Headwinds In The Limelight

Summary

- Vermilion Energy has plans in place to return more excess capital to its shareholders in 2H 2022 and 2023 as indicated in its new return of capital framework.

- However, there are concerns about the negative impact of a potential EU windfall tax on VET's future cash flow.

- I assign a Hold investment rating to Vermilion Energy, after considering both the upside relating to increased capital return and the downside associated with a potential windfall tax.

Elevator Pitch

I rate Vermilion Energy's ( VET ) ( VET:CA ) stock as a Hold.

The risk-reward for VET is balanced, pointing to a Neutral or Hold rating for Vermilion Energy. On the positive side of things, Vermilion Energy has firmed up plans for the company's future capital return. On the negative side of things, there are significant regulatory risks with regards to VET's exposure to Europe, as a potential windfall tax might take away a large chunk of the company's FY 2023 cash flow.

Company Description

On its corporate website , VET refers to itself as "an international energy producer" that is "focused on the exploitation of light oil and liquids-rich natural gas conventional resource plays in North America" and "conventional natural gas and oil opportunities in Europe and Australia."

In terms of geographic mix, North American and international markets account for 37% and 63% of Vermilion Energy's pro forma fiscal 2022 Fund Flows from Operations or FFO, respectively as indicated in its October 2022 investor presentation .

With respect to product or commodity mix, VET is expected to earn 49%, 27%, 15%, and 9% of the company's FFO from European gas, oil/condensate/NGL (natural gas liquids), oil (brent), and North American gas, respectively in FY 2022.

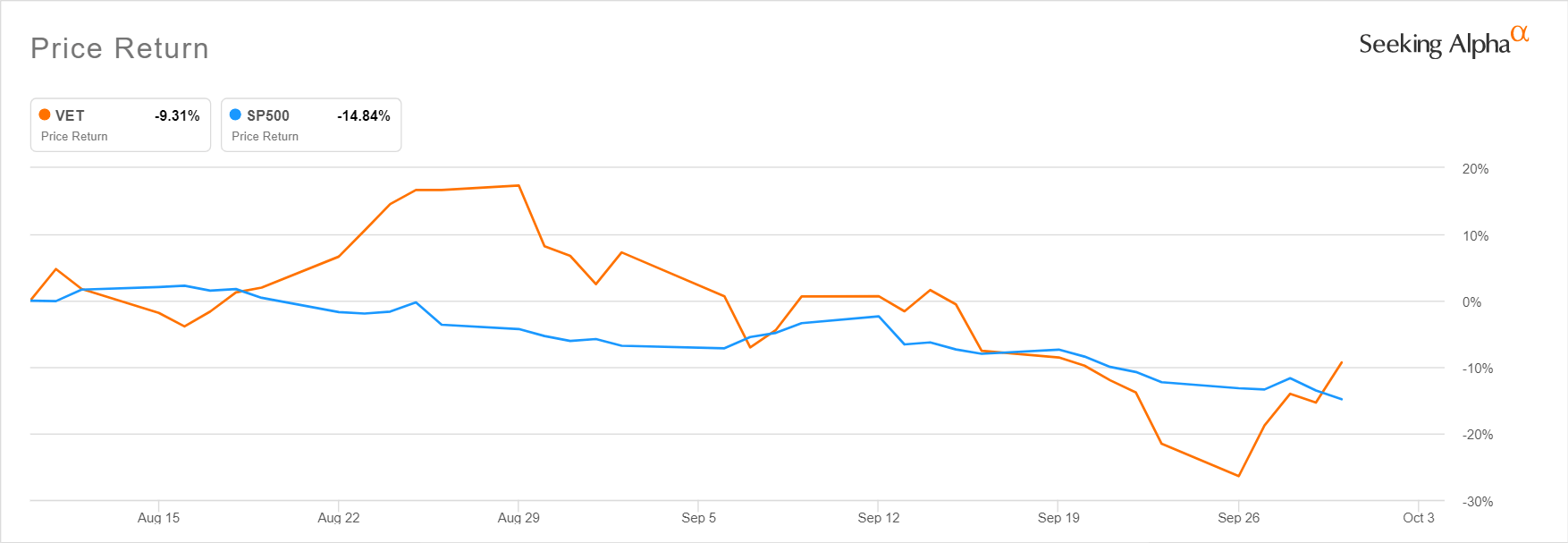

Recent Stock Price Performance For VET

Vermilion Energy's shares have outperformed the broader market in the last two months as indicated in the chart presented below.

Vermilion Energy's Share Price Performance Since Early-to-Mid August 2022

{kind=link}

However, this is really a tale of two halves. VET's stock did better than the S&P 500 between August 10, 2022 and August 31, 2022. But the performance of Vermilion Energy's shares began to track the S&P 500 more closely in early-to-mid September. In late-September, Vermilion Energy's stock actually underperformed the broader market.

In the subsequent two sections of the article, I will explain the factors that led to Vermilion Energy's initial share price performance in August and its subsequent underperformance towards the end of September.

Shareholder Capital Return Plan Announcement

On August 11, 2022, VET issued a press release disclosing its Q2 2022 financial results. But it wasn't Vermilion Energy's most quarterly financial performance that really caught the attention of investors. Instead, it was Vermilion Energy's announcement (revealed in its quarterly earnings media release) that the company will have a "formal return of capital framework" in place that excited the market. This sparked the run-up in VET's share price between mid-August and end-August as highlighted in the prior section.

As part of its new return of capital framework, Vermilion Energy has set a goal of distributing as much as a quarter of the company's free cash flow to shareholders in the second half of 2022. In 2023, VET targets to allocate an even larger proportion, or specifically between half and three-quarters, of its free cash flow to shareholder capital return.

The actual percentage of free cash flow returned to shareholders will be dependent on the progress of Vermilion Energy's deleveraging process. As indicated in the table below, VET could potentially even distribute up to 90% of its free cash flow to shareholders in the future, if and when its net debt and net debt-to-FFO ratio drop to under $500 million and 0.5 times, respectively. As a reference, Vermilion Energy's net debt amounted to $1.6 billion as of June 30, 2022 which translated into a net debt-to-FFO ratio of 1.1 times as revealed in its Q2 2022 results press release.

VET's Proportion Of Free Cash Flow Allocated To Shareholder Capital Return Under Various Financial Leverage Scenarios

VET's October 2022 Investor Presentation

{kind=link}

Notably, Vermilion Energy has already begun the process of rewarding its shareholders with increased capital returns. VET spent $72 million (equivalent to about 2% of its market capitalization) to buy back about 2.3 million of its shares between July 2022 and September 2022. Furthermore, the company raised its quarterly dividend per share by a third to $0.08 for the third quarter of 2022.

The current sell-side's consensus FY 2023 free cash flow forecast for VET is approximately $1.5 billion as per S&P Capital IQ . Assuming that Vermilion Energy allocates half of its free cash flow to shareholder capital return, VET could be potentially trading at a forward FY 2023 shareholder return yield (the sum of dividends and buybacks divided by market capitalization) of as high as 21% based on my estimates. As such, it doesn't come as a surprise that VET's shares performed well in the latter half of August 2022 after the return of capital framework was officially announced.

Regulatory Headwinds In Europe

VET's presence in the European market is a double-edged sword.

On one hand, Vermilion Energy specifically highlighted in its October 2022 investor presentation that it has "meaningful exposure to premium priced European gas." This is expected to be a key driver of the company's earnings and cash flow in the near term, until the energy crisis in Europe eases. As highlighted earlier in this article, European gas is projected to contribute 49% of VET's FY 2022 FFO.

On the other hand, VET faces regulatory headwinds relating to the current European energy crisis. The Guardian reported on September 14, 2022 that "EU (European Union) expects to raise €140bn from windfall tax on energy firms."

The windfall tax might have a substantial effect on the bottom line of oil & gas companies operating in Europe. As an example, TotalEnergies SE (TTE) ( TTFNF ), a French energy company, noted that it "may have to pay more than a billion euros ($1 billion)" windfall tax, according to a September 21, 2022 Bloomberg article which cited comments from TTE's CEO.

Things might not be good for Vermilion Energy as well. A research report (not publicly available) titled "Potential EU Windfall Profits Tax" published by Scotiabank on September 16, 2022 estimated that "a potential windfall tax" could represent as much as "21-26% of (VET's) cash flow" for 2023. In the event of reduced cash flow resulting from a windfall tax, Vermilion Energy's actual dividends and buybacks next year might disappoint the market.

This makes it clear why VET's shares underperformed the S&P 500 since late-September 2022, as investors became increasingly worried about the financial impact of a potential windfall tax.

Closing Thoughts

Vermilion Energy is rated as a Hold. My view of VET's outlook is mixed, taking into account both expectations of higher shareholder capital return and the downside risk relating to a substantial EU windfall tax.

For further details see:

Vermilion Energy: Capital Return And Regulatory Headwinds In The Limelight