VET:CC - Vermilion Energy: Don't Let A Warm Winter Cool Your Enthusiasm

2023-04-19 08:20:00 ET

Summary

- The shareholders of Vermilion Energy have endured a large sell-off with their share price now down upwards of 50%+ versus its peak during 2022.

- This resulted from what I feel was a perfect storm of negative sentiment following the windfall tax in Europe and a warmer-than-expected winter that sent natural gas prices crashing.

- Whilst disappointing, neither derails the appeal of their shares that are trading with a double-digit free cash flow yield based upon their middle-of-the-road results from 2021.

- As they repay debt and increase shareholder returns, I expect their ample upside potential will be unlocked in the years ahead.

- Following their large sell-off, I now believe that upgrading my previous buy rating to a strong buy rating is appropriate.

Introduction

When last discussing Vermilion Energy ( VET ) back in late 2022, my previous article suggested that windfall tax or not, investors can still win. Alas, the subsequent months were not easy for shareholders as negative sentiment prevailed to a far greater extent than envisioned at the time with their share price enduring a large sell-off, which was significantly influenced by a warmer-than-expected winter that sent natural gas prices crashing. Whilst a disappointing setback, I feel as though you should not let a warm winter cool your enthusiasm for their shares, given the very desirable value they offer that should be unlocked in time, thereby resulting in a higher share price.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

Author

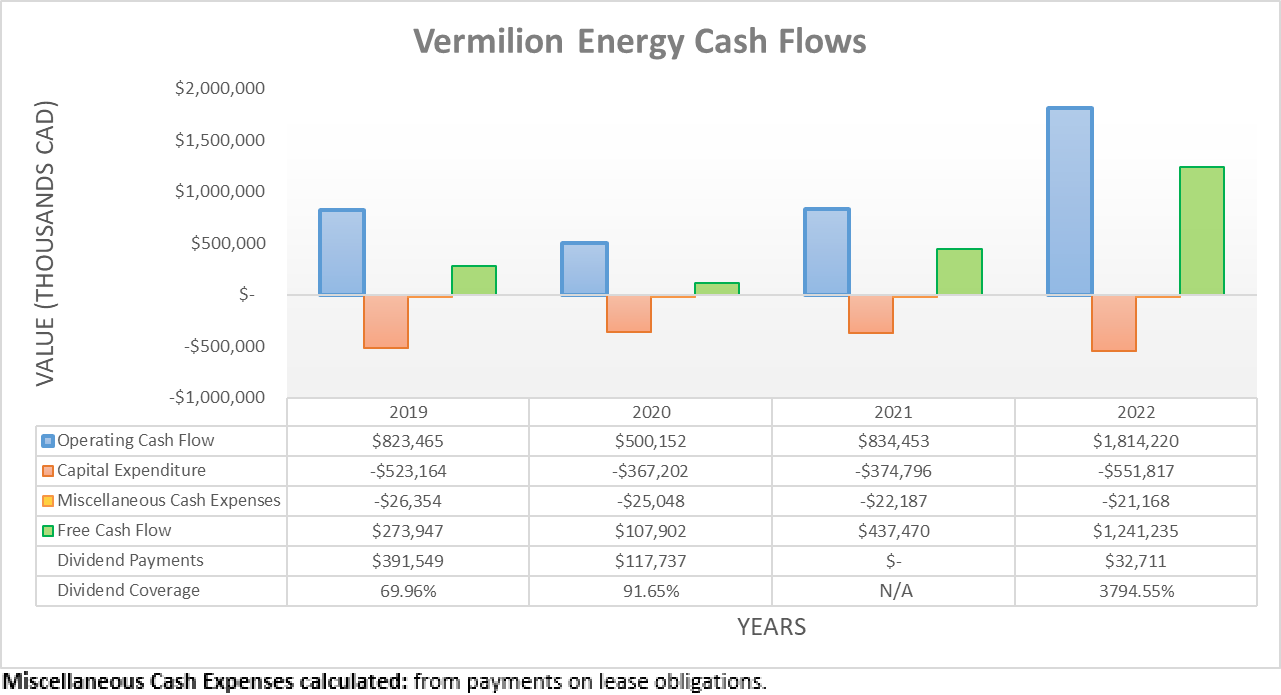

After seeing their operating cash flow climb past the C$1b mark for the first time ever during the first nine months of 2022, it seemingly continued into the fourth quarter with the full year seeing a result of C$1.814b. Despite oil and gas prices easing, this marks a continuation of their previous results during the first nine months that at the time, saw operating cash flow of C$1.319b. Thanks to this massive cash windfall, they were left with free cash flow of C$1.241b for the full year, which helped fund various achievements, most notably repaying debt whilst also restarting shareholder returns as well as also funding their Leucrotta acquisition that was discussed within my earlier article .

{kind=link}

Author

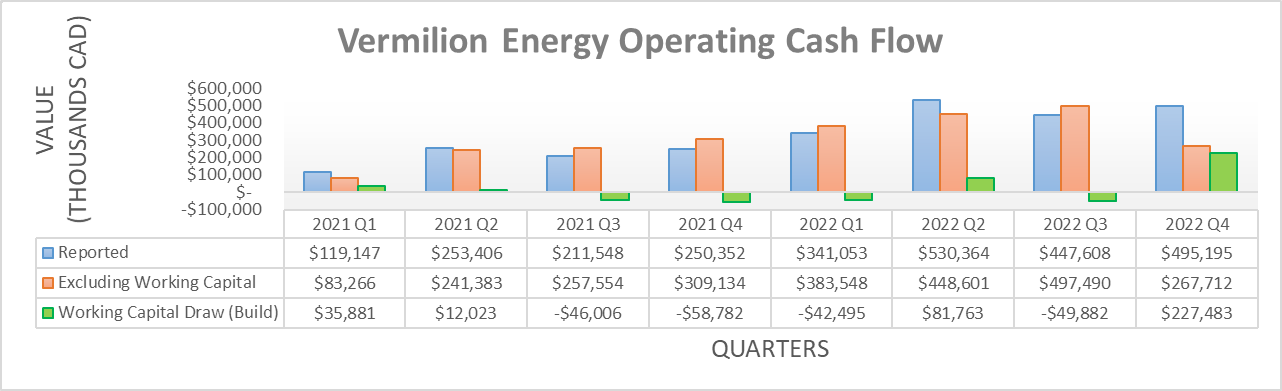

When viewing their operating cash flow on a quarterly basis, it shows the fourth quarter of 2022 provided their second highest ever reported result of C$495.2m that was only surpassed by their previous result of C$530.4m during the second quarter. Although if looking beneath the surface at their underlying result of C$267.7m that excludes working capital movements, it shows the fourth quarter actually saw an abnormally large working capital draw of C$227.5m. Whilst this materially boosted their results, they also had to make their first windfall tax payment in Europe that incurred a cost of C$223m based upon the information on slide three of their fourth quarter of 2022 results presentation . Since this was enacted retrospectively but not paid until the fourth quarter, it also skewed their reported operating cash flow, although in the opposite manner by weighing down the fourth quarter disproportionately.

Whilst the windfall tax is a disappointment for shareholders, it scales with commodity prices and thus as my previous analysis discussed, it does not necessarily derail the appeal of their shares, although it would have created a degree of negative sentiments in the short-term. Nevertheless, 2022 was still an amazing year overall but despite their aforementioned achievements, sadly their share price endured a large sell-off that leaves it down upwards of 50%+ from its peak during 2022. Whilst oil prices have eased in recent months due to economic concerns versus their triple-digit levels during parts of 2022, the biggest culprit is natural gas prices, which form a large portion of their free cash flow even after this downturn.

Vermilion Energy Corporate Presentation April 2023

After seeing natural gas prices surge to never-before-seen levels during 2022 as Russian supply was taken off the market, Europe was fortunate to see a warmer-than-expected winter that helped avert a natural gas crisis via lowering demand for heating . Due to laws of supply and demand, this sent natural gas prices crashing, not just in Europe but also, within the United States that also saw similar weather conditions lowering demand. The market tends to price shares by their fundamentals in the medium to long-term but in the short-term, it is heavily influenced by sentiment. When natural gas prices started crashing, the combination with the windfall tax created what I feel was a perfect storm of negative sentiment that resulted in a large sell-off.

I feel it prudent to remember that when it comes to the weather, it can move both ways and thus whilst the winter of 2022 was warmer-than-expected, the upcoming winter of 2023 could just as easily be colder-than-expected, thereby providing a boost to natural gas demand and hence, prices. Very importantly, the recent crash does not stem from fundamental problems and thus regardless of the prevailing future weather conditions, it does not necessarily hinder the medium to long-term appeal of their shares that in turn, makes the large sell-off an opportune time to assess the value they now offer.

Due to the inherent volatility of oil and gas prices, it complicates this process but my preferred approach utilizes their historical cash flow performance, whilst selecting a basis point that includes a margin of safety. I feel their results during 2021 fit the bill for two reasons, firstly because oil and gas prices were not particularly high nor low on average, thereby making for middle-of-the-road operating conditions. Secondarily, it did not include their Leucrotta acquisition, nor their soon-to-close Corrib acquisition that was discussed within my previously linked articles. When combined, the higher production from these new assets should ensure a margin of safety that accounts for future windfall tax payments, which should only be relatively minor unless there is a repeat of the booming natural gas of 2022.

Looking back at 2021, their free cash flow was C$437.5m that sees a very high free cash flow yield of circa 15% when compared against their current market capitalization of approximately C$3b. Whilst free cash flow yield is not as commonly thought about as dividend yield, it effectively represents the upper limit they can afford to pay via dividends or share buybacks consistently. So, think about it this way, would you say a safe circa 15% dividend yield is very desirable? Or alternatively, what about seeing the company removing more than 10% of their outstanding share count per annum? Regardless of the split between dividend and share buybacks, I certainly would find that very desirable, as I suspect many other investors would too because it offers ample upside potential that could see capital gains on a higher share price. Whilst yes, they are currently only paying out a fraction of this potential, going forwards into 2023 and beyond, it should be unlocked as they continue repaying debt.

{kind=link}

Author

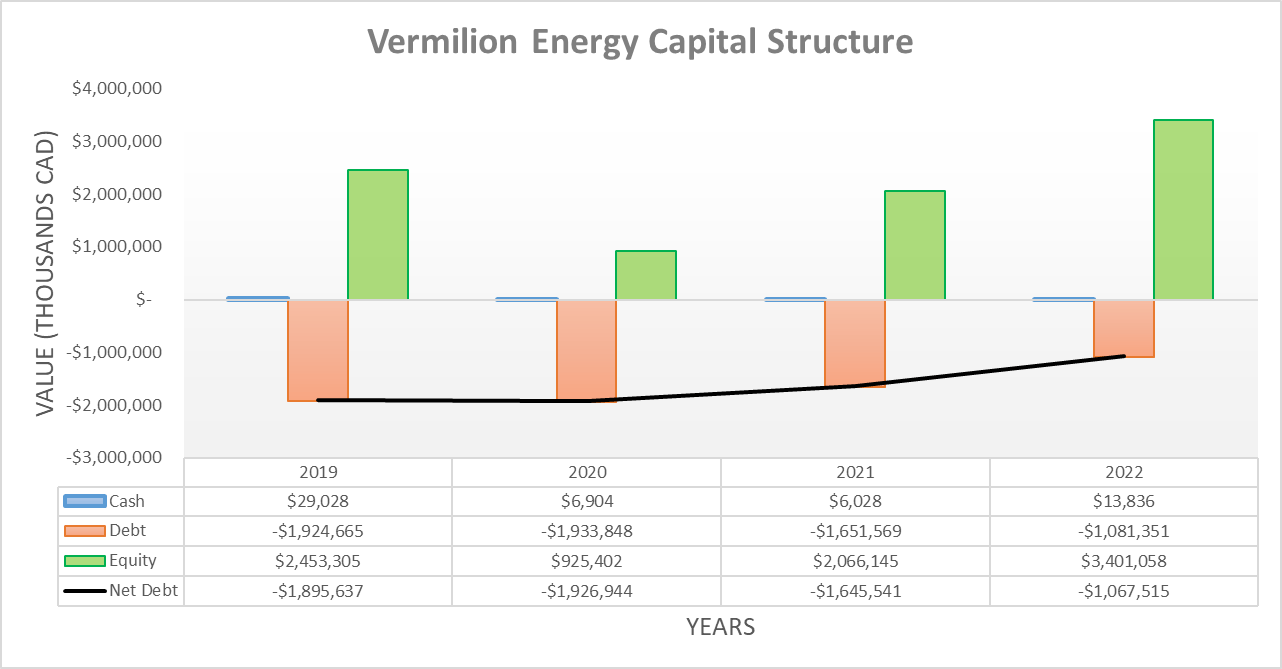

Since conducting the previous analysis, the fourth quarter of 2022 saw their net debt plunge to C$1.068b versus its previous level of C$1.402b following the third quarter, although this was partly a result of their abnormally large working capital draw. Despite having restarted shareholder returns and undertaken their Leucrotta acquisition, they still ended 2022 with net debt down significantly versus its previous level of C$1.645b at the end of 2021. Going forwards into 2023 and 2024, their net debt should continue its downward march with management planning to eventually hit as low as only a mere C$500m.

Vermilion Energy Fourth Quarter Of 2022 Results Presentation

The eagle-eyed reader might notice the above graph states their net debt is noticeably higher than C$1b at circa C$1.3b. Although as their 2022 Annual Report shows, management includes an adjusted working capital component that was responsible for most of this difference, as well as their inclusion of unrealized foreign exchange on swapped USD borrowings that was also partly responsible. Whilst there is nothing wrong with their approach per se, my analysis utilizes the debt and cash as listed on their balance sheet to aid with comparability across the many companies that I cover. Normally these two approaches do not vary materially but given their abnormally large working capital draw during the fourth quarter, this was not the case this time. This should only be a temporary anomaly because going forwards into 2023, the difference should net out as their abnormally large working capital draw reverses into a build.

Far more exciting and important than exactly where their net debt sits at the end of 2023 is their accompanying outlook for shareholder returns, which clearly shows that as net debt comes down, it will see their shareholder returns increase as a percentage of their prevailing free cash flow. Going forwards into 2023, this is expected to reach upwards of 25% and whilst this marks a sizeable increase versus the mere circa 10% during 2022, it is still relatively minor versus the 50%+ possibly coming during 2024 and beyond.

This outlook works in conjunction with their aforementioned double-digit free cash flow yield via translating it into shareholder returns and thus, seeing their ample upside potential unlocked. Since the shareholder returns are more tangible, headline-grabbing and obviously, more appealing, they should boost sentiment surrounding their shares as they increase, especially as the impacts of the windfall tax and the warmer-than-expected winter fall into the rear-view mirror and thus are most likely forgotten as time passes. In turn, this should help their share price rally in the medium to long-term, as their double-digit free cash flow yield clearly indicates there is ample upside potential in the years ahead once this perfect storm of negative sentiment passes.

I would normally now expand into a detailed assessment of their leverage and debt serviceability but in this situation, it does not feel necessary. Apart from the fact management is planning to half their net debt in the coming years, neither of these two considerations have been problematic. To this point, their leverage is clearly very low given their operating cash flow of C$1.814b during 2022 easily surpasses their net debt, regardless if utilizing my approach or that of management. Meanwhile, their accompanying debt serviceability is also perfect given their most recent interest expense of C$82.9m during 2022 sees interest coverage of more than 20 versus their operating cash flow.

{kind=link}

Author

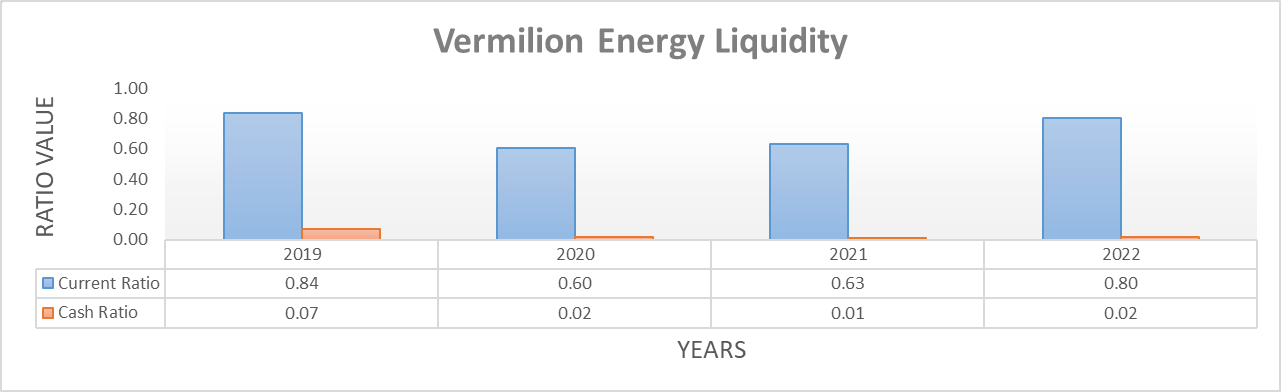

When it comes to their liquidity, it was positive to see their current ratio improve to 0.80 during the fourth quarter of 2022 versus its previous result of 0.61 following the third quarter. Whilst their accompanying cash ratio barely improved to 0.02 versus 0.01 across these same two points in time, it nevertheless still helped better cement their adequate liquidity.

Since management is planning to continue repaying their debt during 2023 and 2024, it means they should be a net contributor to capital markets within the foreseeable future. Apart from removing risks surrounding debt maturities, it also reduces their direct exposure to any future banking crisis as much as possible. Whilst stability seemingly returned to capital markets after Credit Suisse ( CS ) was taken over by UBS ( UBS ), the risk of another more severe banking crisis remains, especially whilst monetary policy is still tight. Even though the emergence of another banking crisis would hurt indirectly via lower oil and gas prices given the economic impact, at least it does not threaten to derail their capital allocation strategy, more so at worse, it would only slow down their progress.

Conclusion

It is not as though we are seeing headlines about natural gas being replaced but rather, its recent downturn is primarily a result of warmer-than-expected weather. In reality, the opposite could have happened, which could eventuate later this year and provide the company with booming operating conditions.

Thankfully, investors do not need to rely upon speculative weather patterns because even based upon their free cash flow during 2021, their shares still trade with a double-digit free cash flow yield that importantly, ensures a margin of safety. As the perfect storm of negative sentiment passes and they increase their shareholder returns in the years ahead, it should unlock the ample upside potential offered by their free cash flow and thus, I believe that upgrading my previous buy rating to a strong buy rating is now appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Vermilion Energy’s Quarterly Reports , all calculated figures were performed by the author.

For further details see:

Vermilion Energy: Don't Let A Warm Winter Cool Your Enthusiasm