VET - Vermilion Energy: Strong 2022 Results And An Attractive Valuation

2023-03-09 08:23:08 ET

Summary

- Vermilion reported a strong 2022 with C$1.6B in fund flows and C$1.1B in free cash flow.

- 2023 cash flows look to decline due to the weaker energy prices and to rebound later in 2024, even though conservative price assumptions are used for 2024.

- Vermilion will be focused on debt repayments for much of 2023, while the company is also doing some buybacks, and has a small quarterly dividend.

Investment Thesis

I wrote a detailed article on Vermilion Energy (VET) a few months ago, which is worth the read. This is my take on the 2022 results and what to expect over the near term.

{kind=link}

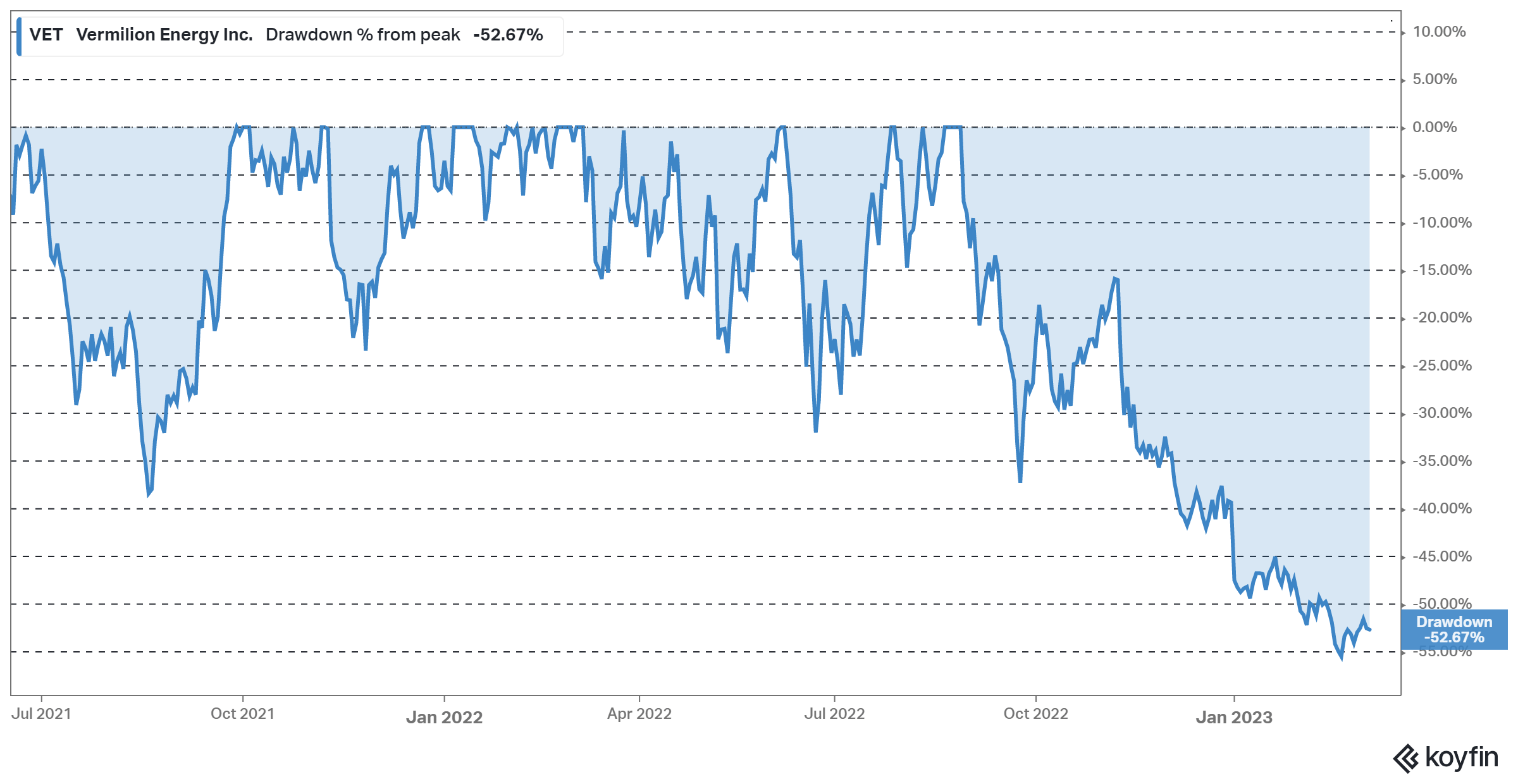

Vermilion has seen the share price decline by more than 50% from the peak in 2022, part of the decline makes sense due to lower oil & natural gas prices together with the windfall profit taxes in Europe, which came into effect for 2022-2023 in the end of last year.

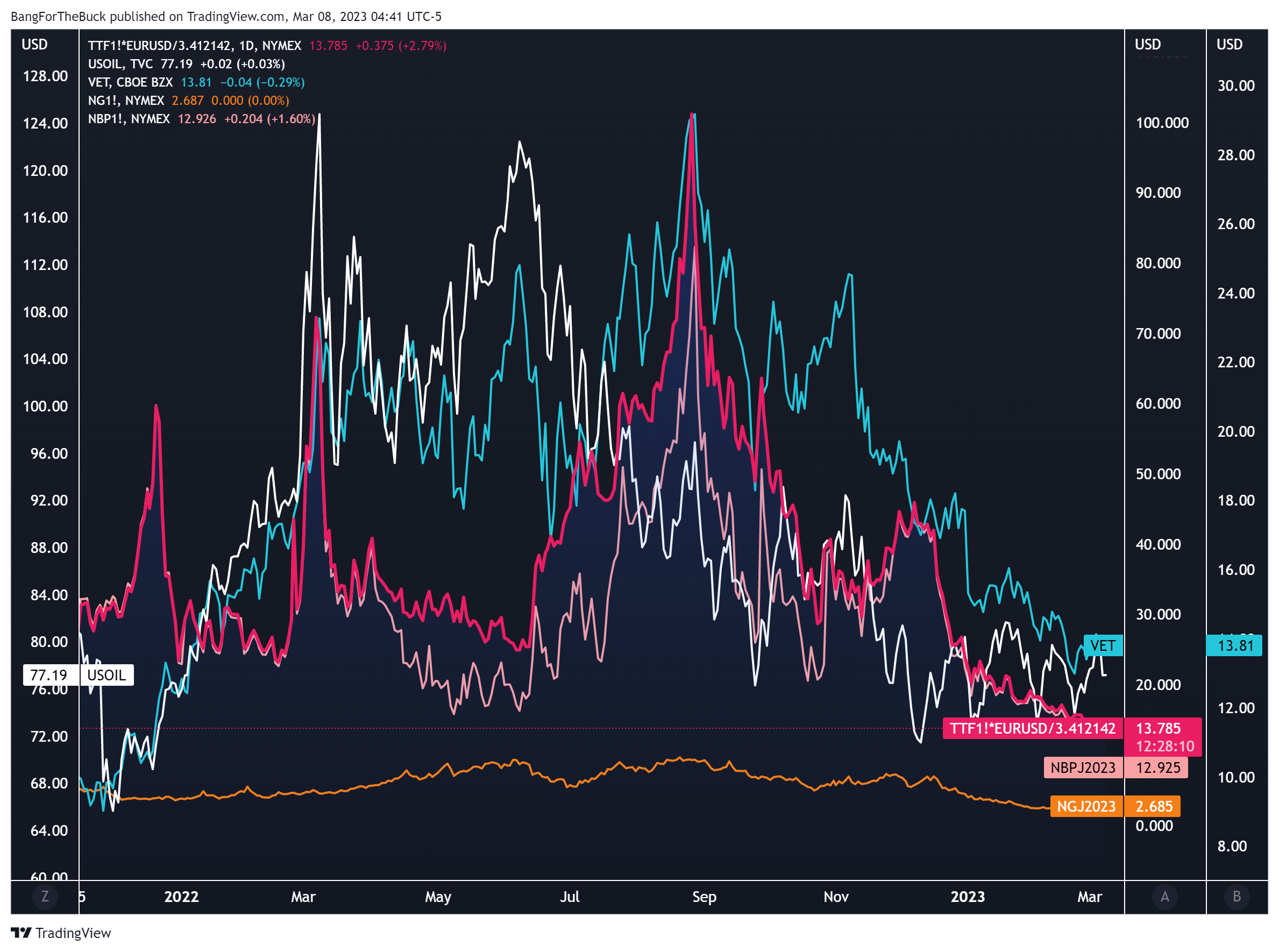

However, the market is in my view still underappreciating how profitable the European natural gas market is for Vermilion, even with the windfall taxes, where prices are still above the peak levels we saw in the U.S. during last year. That is illustrated by the two red series in the chart below compared to the orange series for U.S. natural gas prices. A substantial part of Vermilion's revenues is also derived from crude oil, which has seen less of a decline compared to natural gas.

Figure 2 - Source: TradingView

{kind=link}

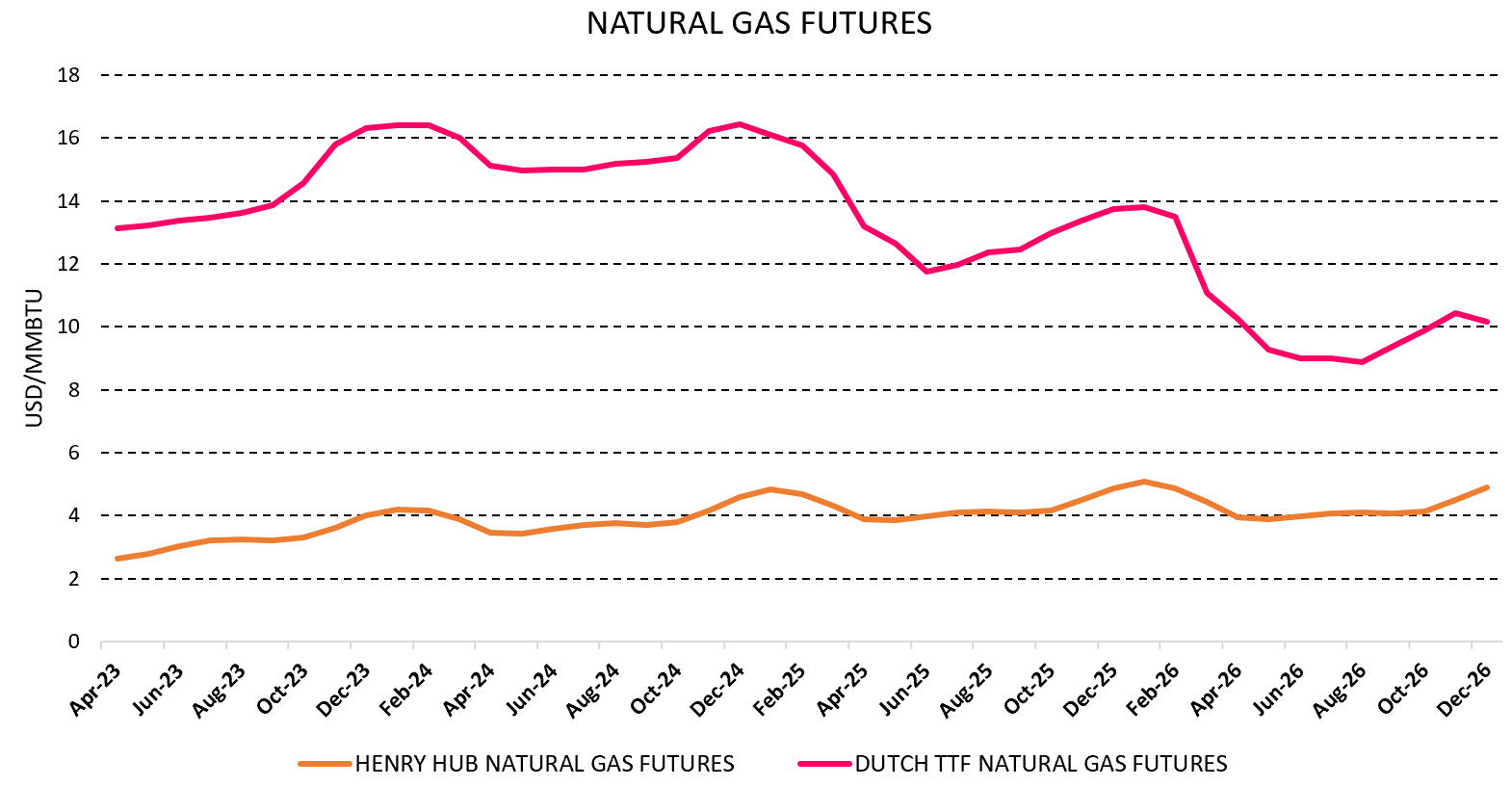

In the chart below, we can also see the massive difference in futures prices between the U.S. and European natural gas markets, represented by the Dutch TTF here.

{kind=link}

2022 Results & Guidance

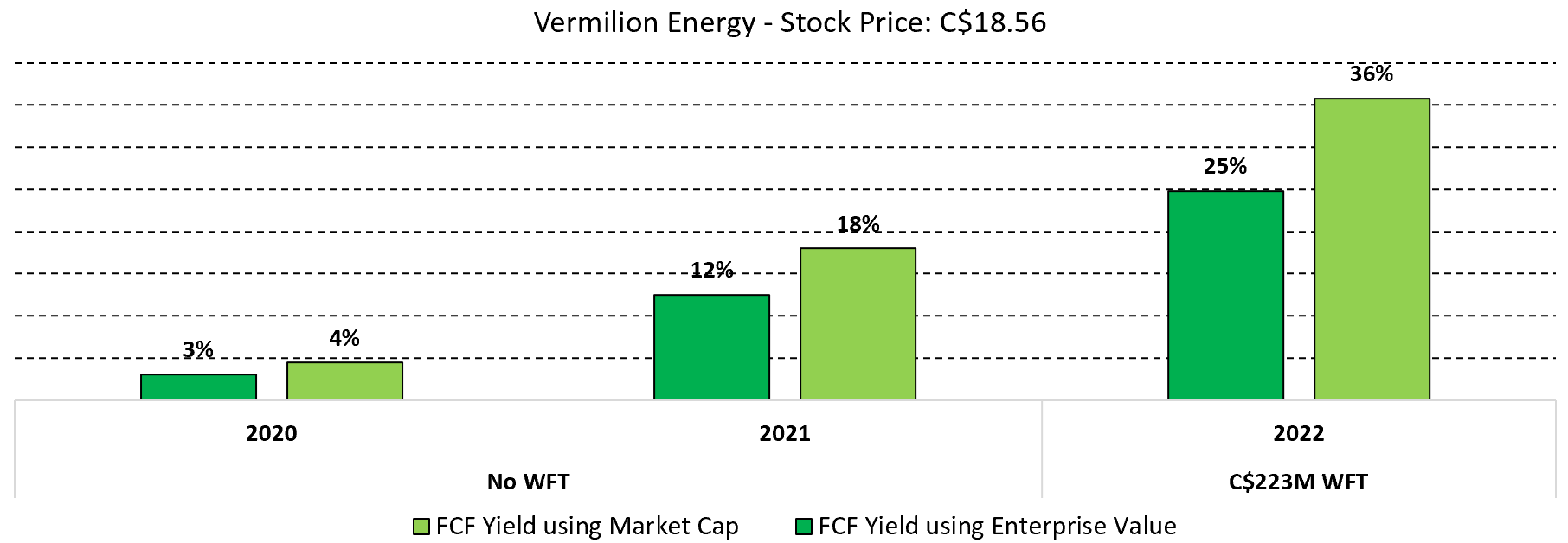

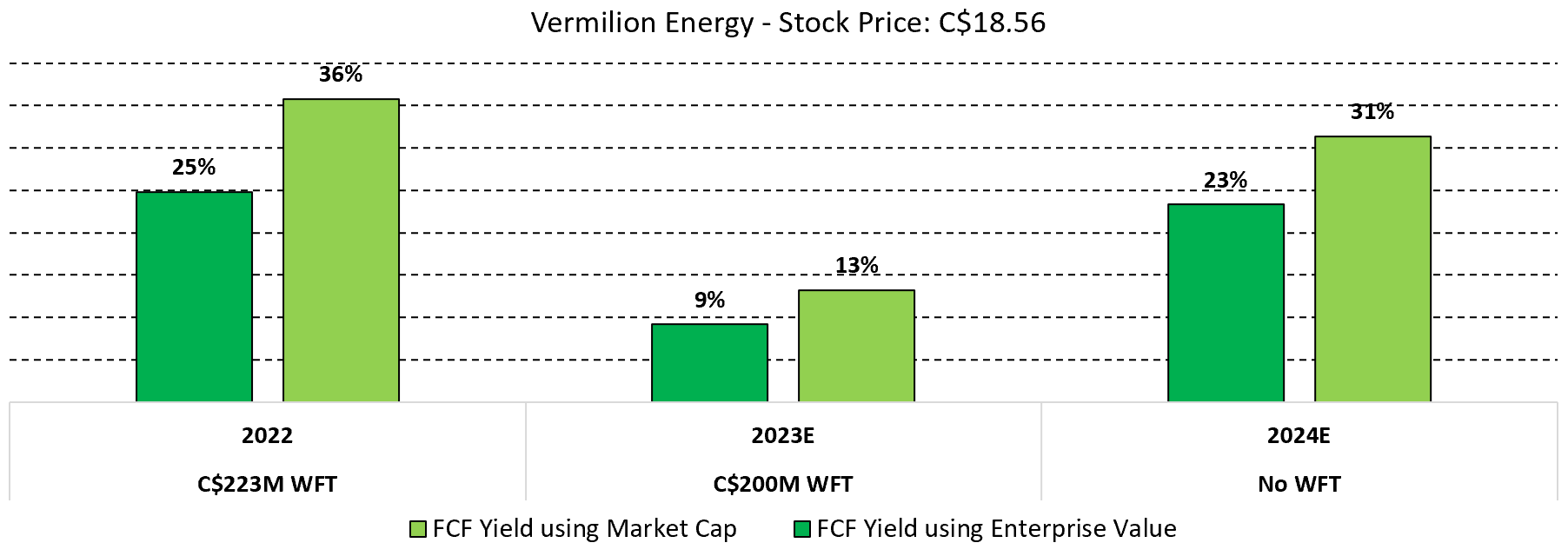

Vermilion reported a record C$1.6B in fund flows from operations ("FFO") during 2022 and C$1.1B in free cash flow ("FCF"). Net Earnings were C$1.3B, which comes to C$8.03 per share. This is a strong result given that the company has a C$3B market cap and an enterprise value of C$4.4B, using the latest stock price and financials. This translates to a 25-36% FCF yield for 2022, depending on if we use the market cap or enterprise value that incorporates the net debt.

Figure 4 - Source: Annual Reports

{kind=link}

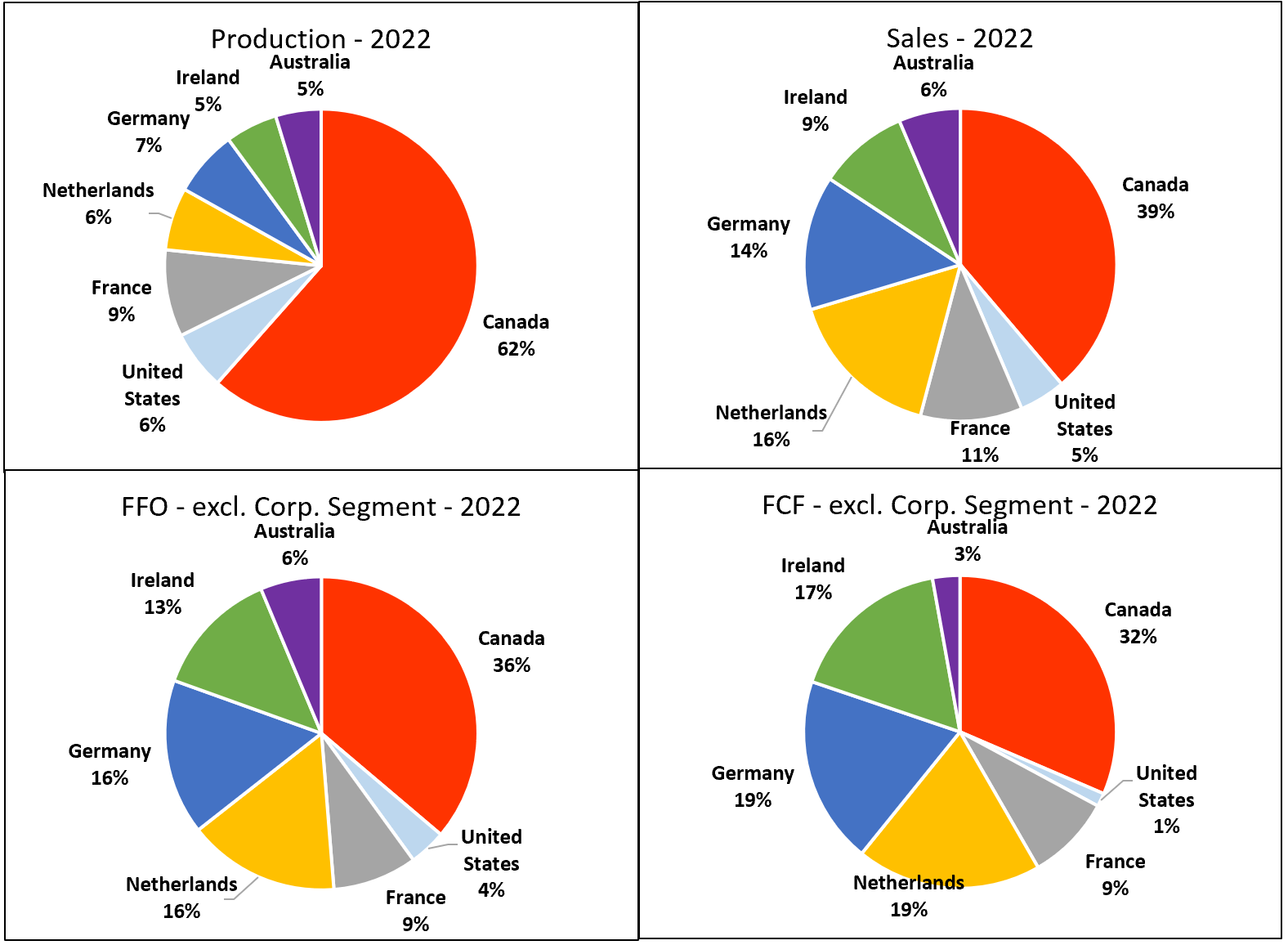

The below figure illustrates that while the majority of 2022 production came from Canada, European natural gas as represented by Ireland, Germany, and the Netherlands is a large percentage of fund flows and free cash flow. Note that these charts do not include the C$223M in windfall profit tax during 2022, which the company reported under the corporate segment.

Figure 5 - Source: 2022 Annual Report

{kind=link}

The company did in the 2022 report confirm that the Corrib acquisition is set to close in the end of March this year, with a cash payment of C$200M. While the very high temporary windfall profit taxes in Ireland have no doubt decreased the attractiveness of that acquisition, the payback period is still roughly just a year. Vermilion also announced the divestments of about 5,500 boe/d of non-core light oil assets in southeast Saskatchewan for C$225M, set to close in Q1-23, which will ultimately be used to reduce the net debt.

Due to the planned divestments and some maintenance work in Australia during Q1-23, the company has revised the 2023 production guidance down to 84,000 boe/d, while CAPEX is still estimated to C$570M.

Valuation & Conclusion

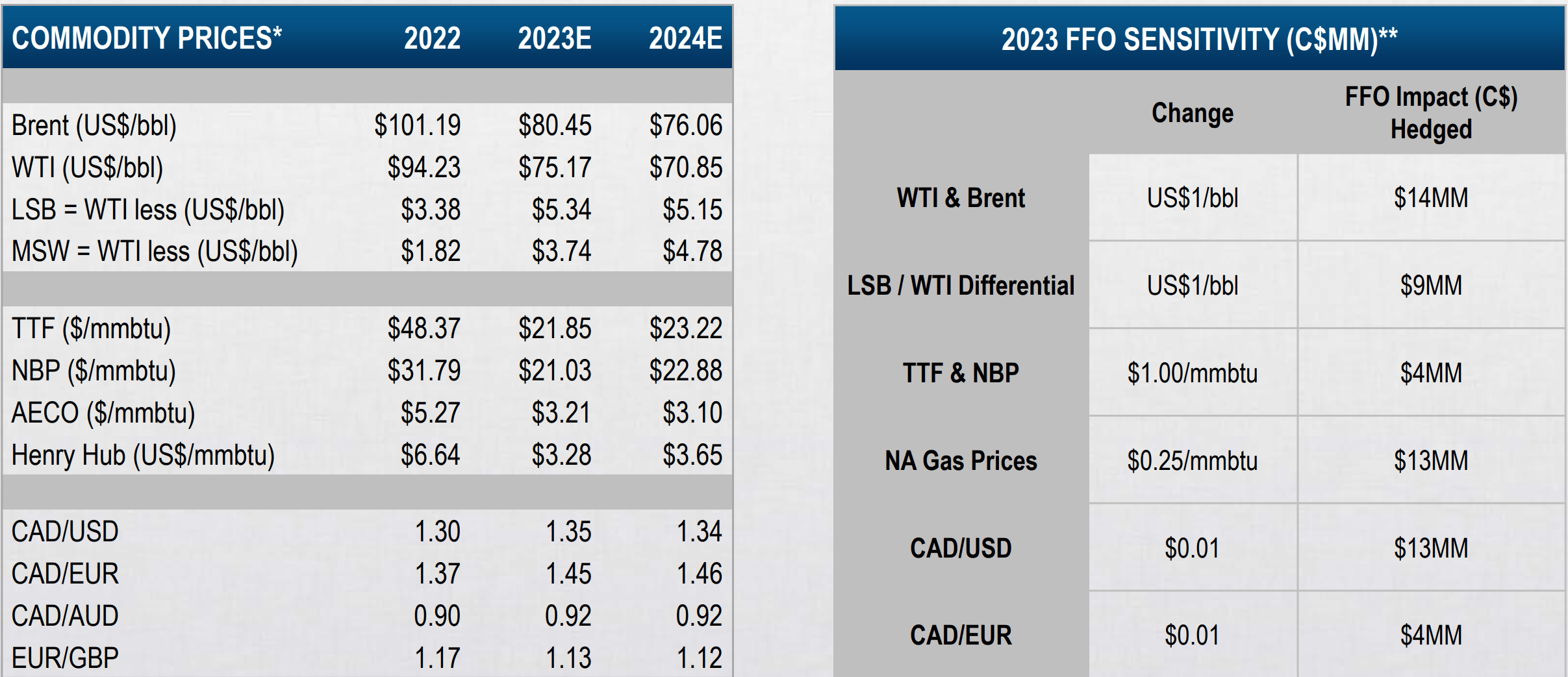

Figure 6 - Source: Vermilion March 2023 Presentation

{kind=link}

Based on the latest price assumptions, which can be seen in the figure above, and figure 7 in the company's latest slide deck . The company looks to be estimating fund flows to somewhere just shy of C$1B in 2023 and just north of C$1.5B for 2024.

I have assumed 2024 CAPEX will be the same as 2023 CAPEX, which would roughly give us C$400M in FCF for 2023 and C$950M in 2024. Vermilion has estimated the windfall profit tax in 2023 to C$200M. I have also assumed the net debt will decrease by C$300M in 2023. These assumptions would give us the following FCF yields.

Figure 7 - Source: My Estimates Derived of Vermilion's figures

{kind=link}

We can see that 2023 looks to be a softer year for Vermilion, while 2024 looks better. The 2024 numbers are of course somewhat dependent on the removal of the windfall profit taxes, where the probability of that happening is difficult to determine. I do however think the probability is quite good that energy prices turn out to be significantly better for 2023-2024 than the assumptions used in figure 6 above.

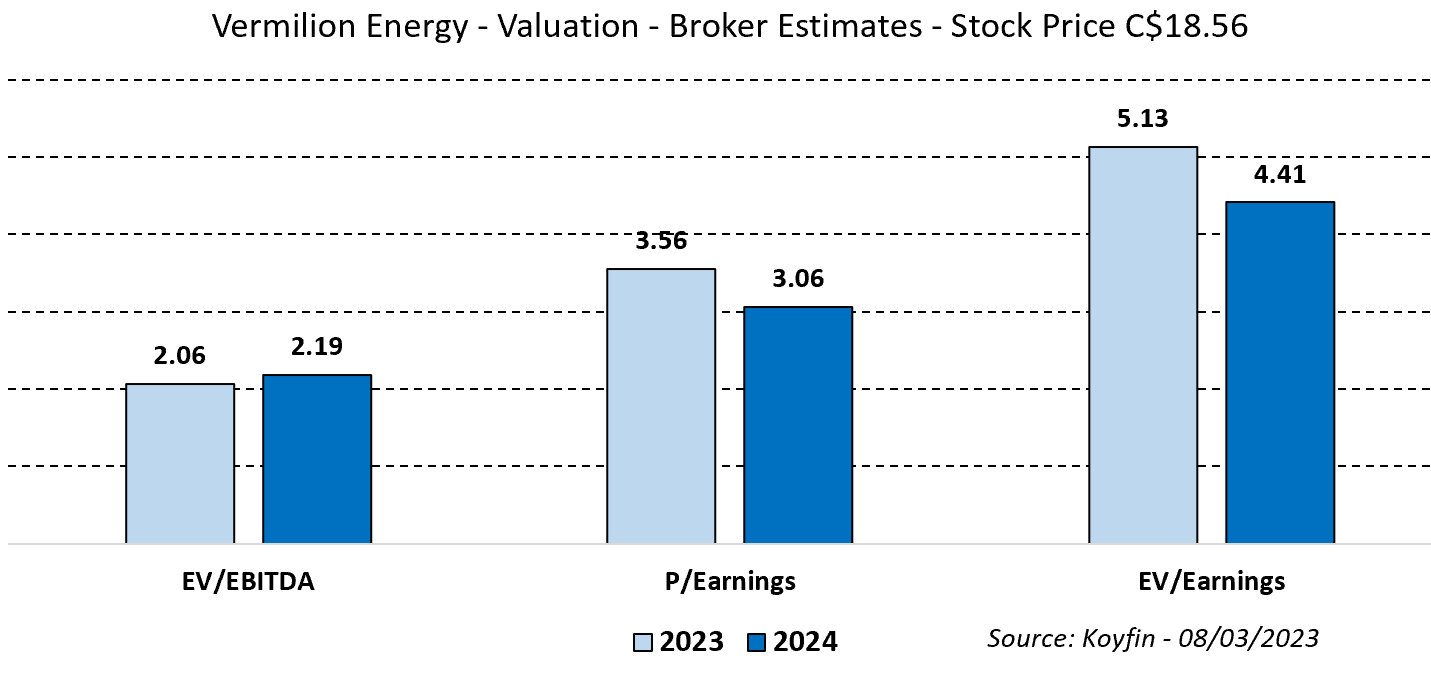

The brokers covering the stock also have the company trading with a very attractive valuation multiple for the next couple of years, even if the 2023 estimates probably need to be revised somewhat lower.

{kind=link}

I went long Vermilion in December of 2022 and I continue to like the value proposition. Given the somewhat weaker energy prices in the beginning of 2023, we might need to wait until late 2023 or early 2024 to see the stock react to the expected higher shareholder distributions, but the valuation continues to be compelling.

The company is moving in the right direction with divestments of non-core assets, some buybacks, and debt repayment as interest rates have increased. The company has also boosted its reserves in 2022. More patience might be required to realize the potential unless we see a reversal in energy prices relatively soon.

For further details see:

Vermilion Energy: Strong 2022 Results And An Attractive Valuation