VET - Vermilion: The Q1-23 Result Confirms The Attractive Valuation

2023-06-01 17:45:05 ET

Summary

- Q1-23 was a decent quarter for Vermilion, with 82,455 boe/d in production, C$253M in fund flows, and C$98M in free cash flow.

- Vermilion is among the cheaper Canadian oil & natural gas producer, based on forward estimates.

- European windfall profit taxes didn't have as much of an impact as many feared.

A version of this article was published in conjunction with the Q1-23 earnings result in my investing group, Off The Beaten Path.

Investment Thesis

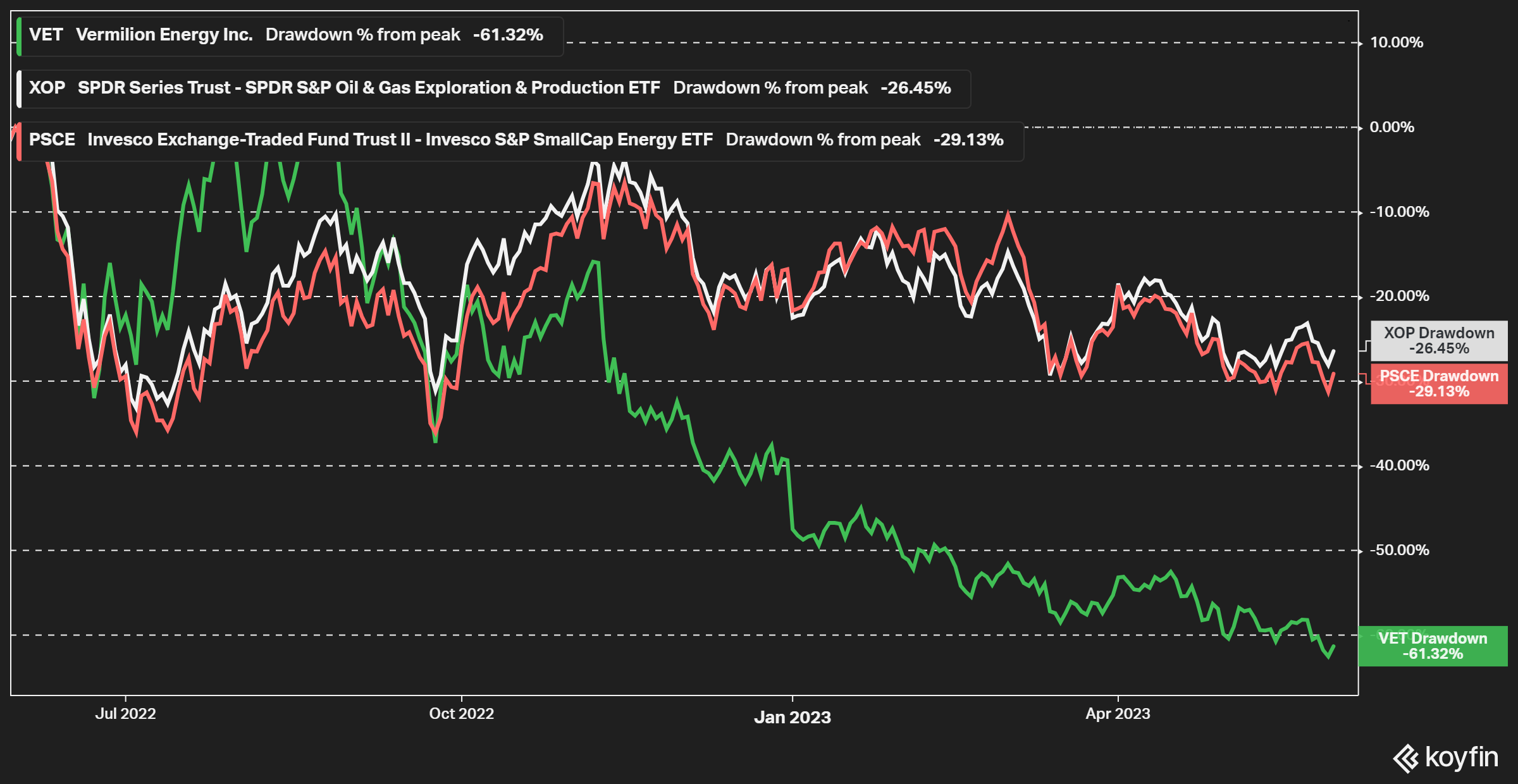

Vermilion Energy ( VET ) has been one of the worst Canadian oil & natural gas producers this year, in terms of performance. The stock is down 36% YTD. That is despite the fact that the stock was already going into the year substantially off the highs from last year. The stock is now down more than 60% from the peak last year, which is substantially more than most peers.

{kind=link}

Figure 1 - Source: Koyfin

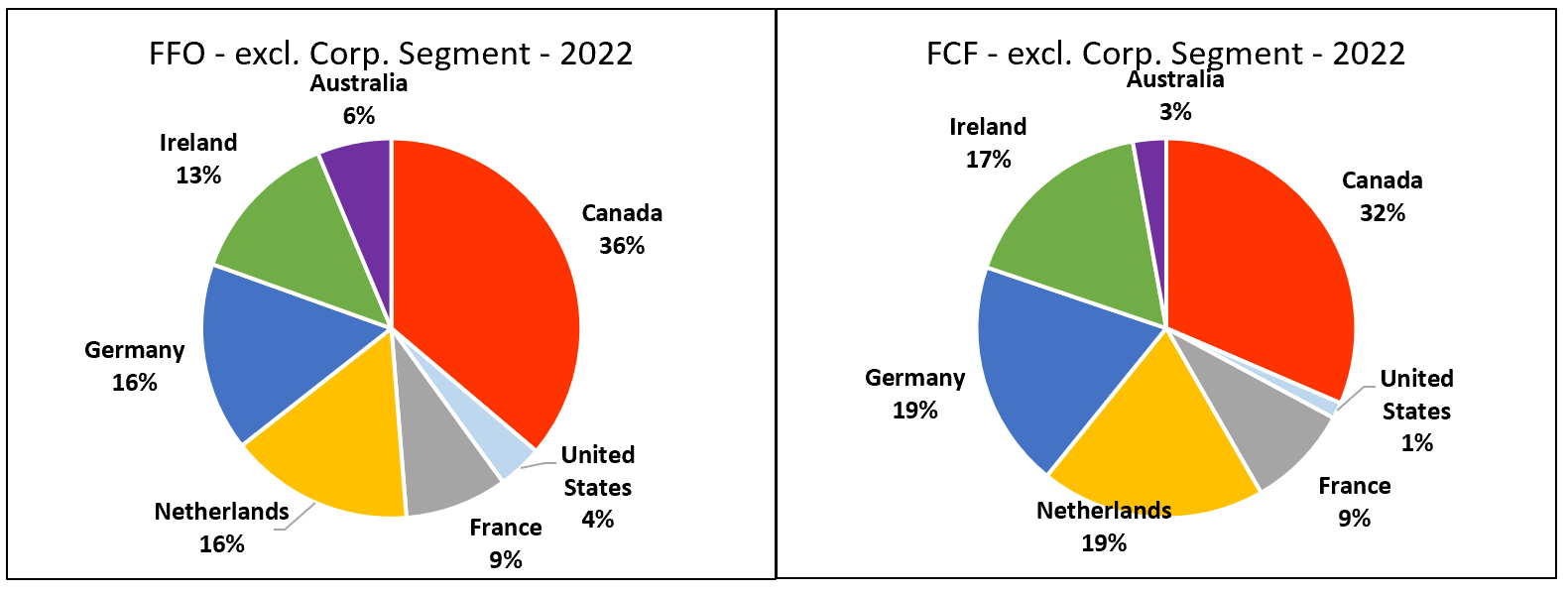

Part of this decline can naturally be explained by the decline in energy prices, European natural gas prices specifically, which have recently been an outsized contributor to fund flows and free cash flow for the company. The European windfall profit tax has no doubt played a part as well, even if I would argue it has probably had a larger impact on the sentiment than the overall profitability of Vermilion.

{kind=link}

Figure 2 - Source: Vermilion Q4-22 Report

{kind=link}

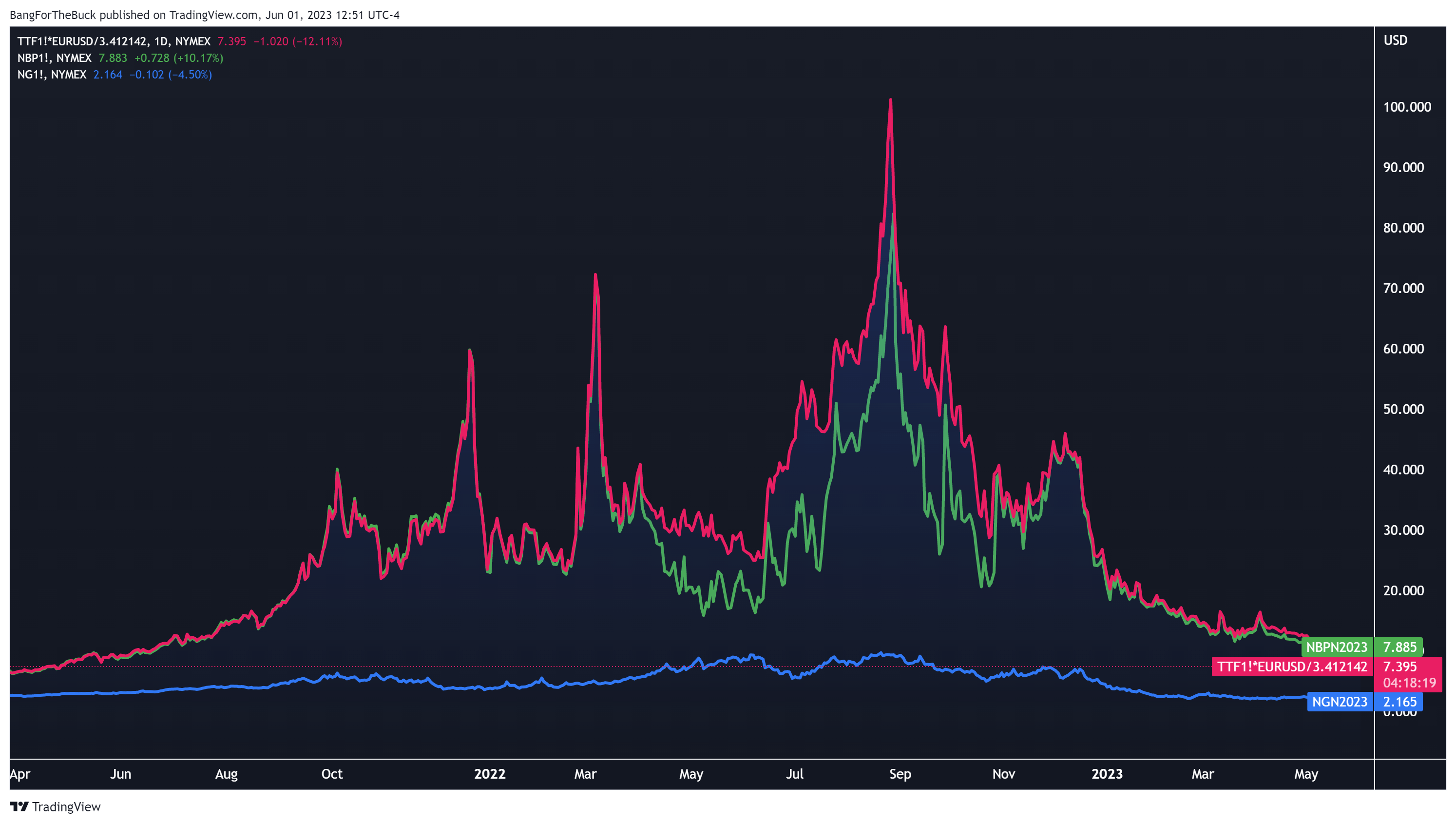

Figure 3 - Source: TradingView - Dutch, UK, & U.S. natural gas prices

I have covered the stock a few times recently on Seeking Alpha, and those articles can be found here . There is no question I was early when I started buying Vermilion in December 2022, but the company is after the substantial decline trading with a very attractive valuation at current energy prices. So, for anyone with more patience, I continue to think Vermilion is a very good investment at this level. My typical investment horizon is 18–36 months, and I have increased my position during the recent weakness.

Q1-23 Results

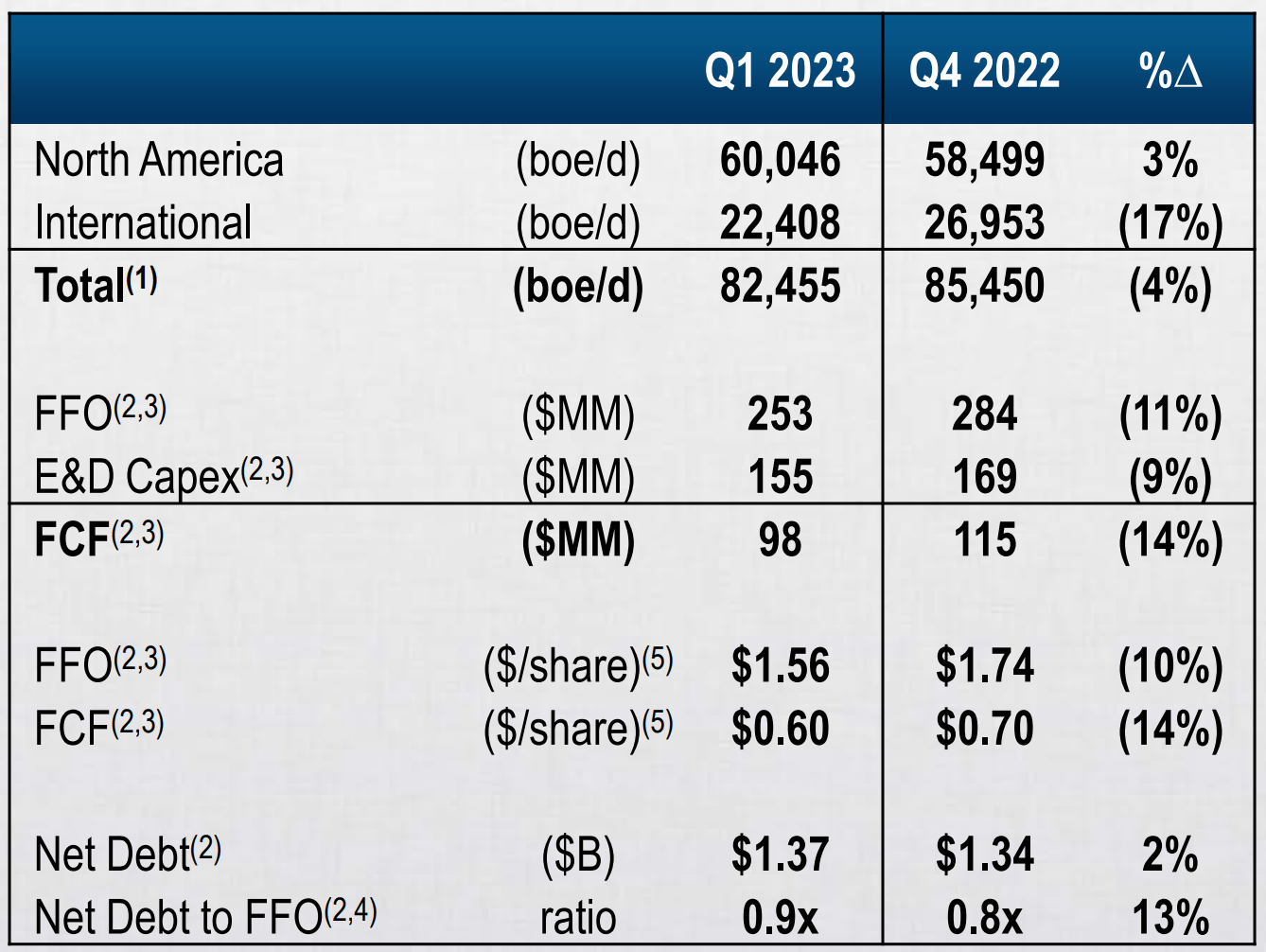

In early May, Vermilion reported its Q1-23 results and hosted a conference call. Production was 82,455 boe/d during the first quarter, which was at the lower end of the latest guidance of 82,000-86,000 boe/d. Earlier this year, the company communicated that the Australian operation was scheduled to be offline in Q1 due to maintenance, but is now expected to be offline for most of Q2 as well.

In Q2, the company has also been affected by the forest fires in Alberta, but has lately started to restart curtailed operations and the annual production guidance of 82,000-86,000 boe/d remains unchanged as of the last update.

{kind=link}

Figure 4 - Source: Vermilion Corporate Presentation

Fund flows in Q1-23 were C$253M and the company reported C$98M in free cash flow for the quarter. The cash flows are down compared to last year, but that should not be a surprise to anyone given the lower energy prices in 2023.

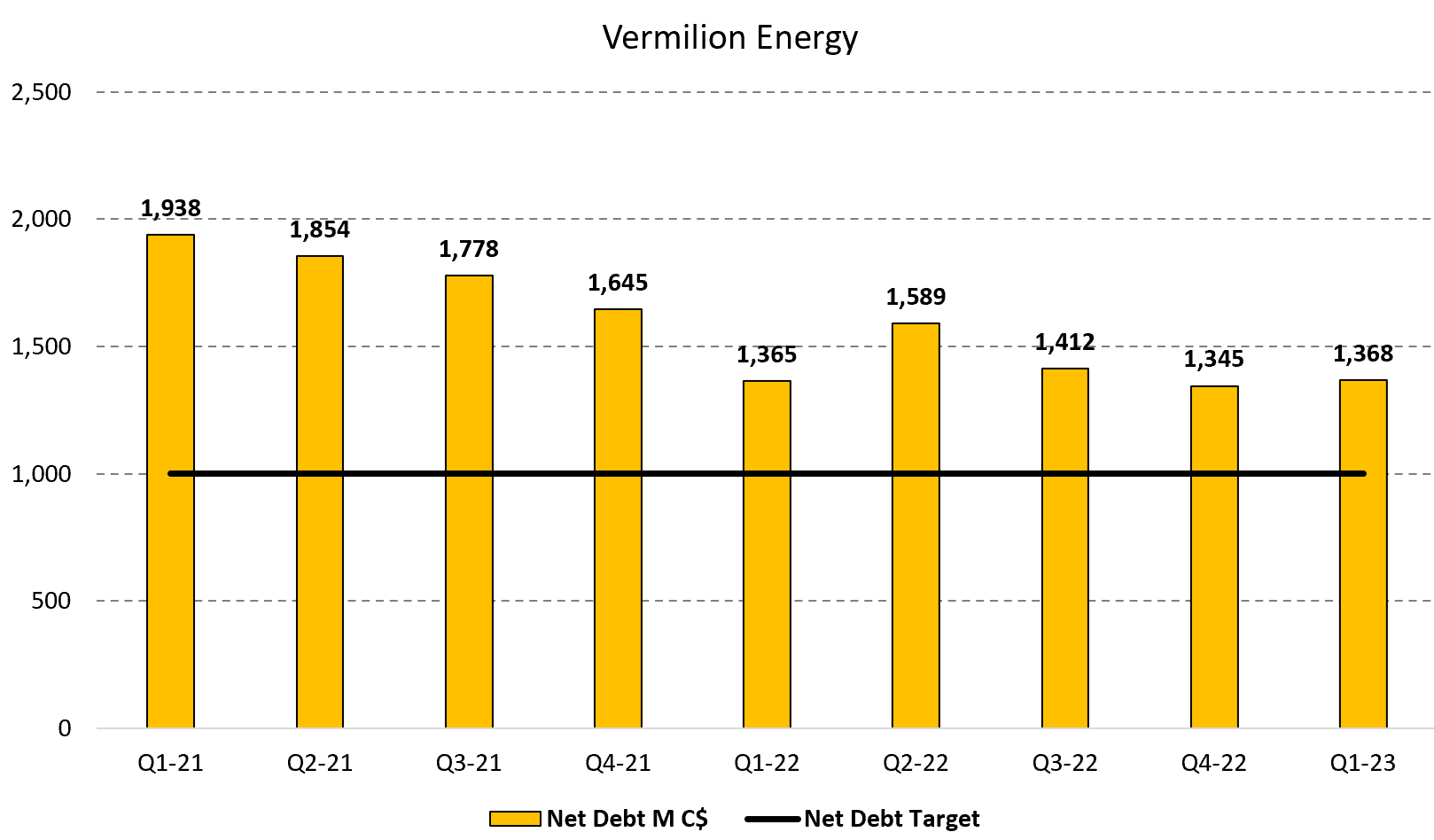

There has been a lot of criticism lately against Vermilion and the lower shareholder distributions, where the current dividend yield is only 2.7%, while the company is focused on deleveraging. Last year, Vermilion was on track to deleverage quicker, which would likely have led to higher shareholder distributions in 2023. However, with the addition of the European windfall profit tax and weaker energy prices, everything was pushed back a few quarters.

I can understand and support the company in its effort to get the leverage ratio down, before more substantial dividends and buybacks, which is why I think patience will be required for anyone investing in Vermilion. The net debt was at C$1,368M at the end of Q1-23 and will hopefully reach or get close to the C$1B net debt target by the end of this year, which should lead to a boost in shareholder distributions in 2024.

{kind=link}

Figure 5 - Source: Vermilion Quarterly Reports

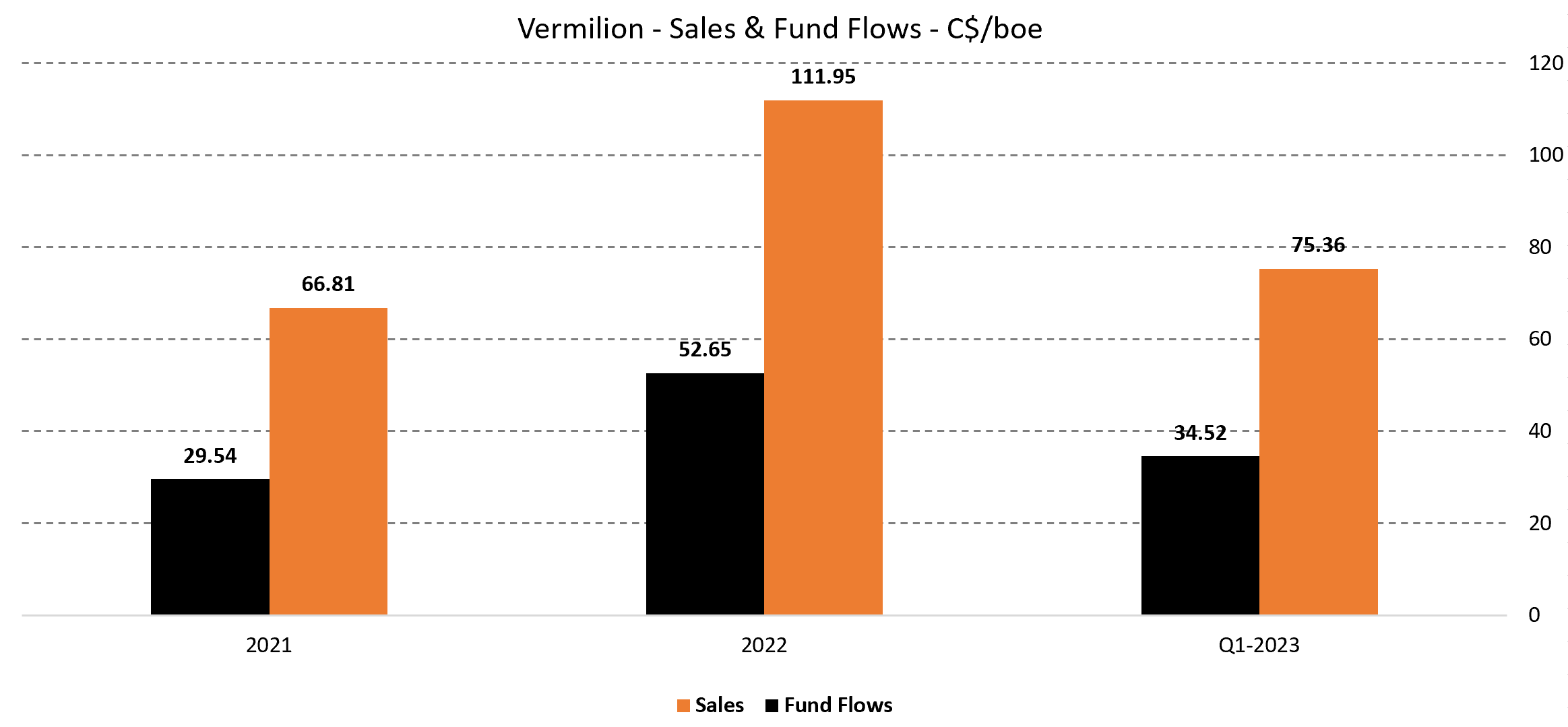

Even though energy prices are down significantly from 2022, Vermilion did still report a sales price of C$75.36/boe and fund flows of C$34.52/boe in Q1-23, which are respectable numbers.

{kind=link}

Figure 6 - Source: Vermilion Quarterly Reports

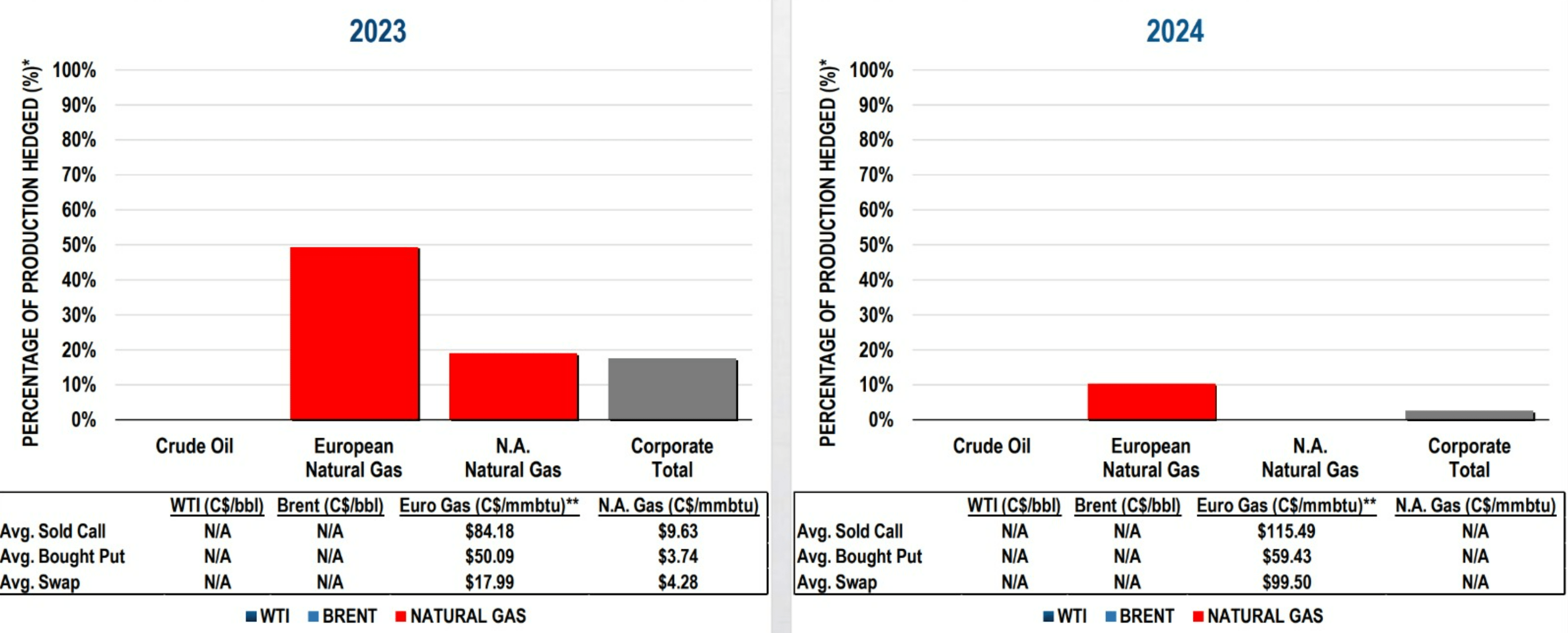

The attractive sales and fund flows are partly because European natural gas prices are still trading with a substantial premium to its North American equivalent, despite being down a lot from the peak levels last year, as illustrated in figure 3 further above. The company also has close to 50% of its the European natural gas production hedged in 2023, at attractive levels.

{kind=link}

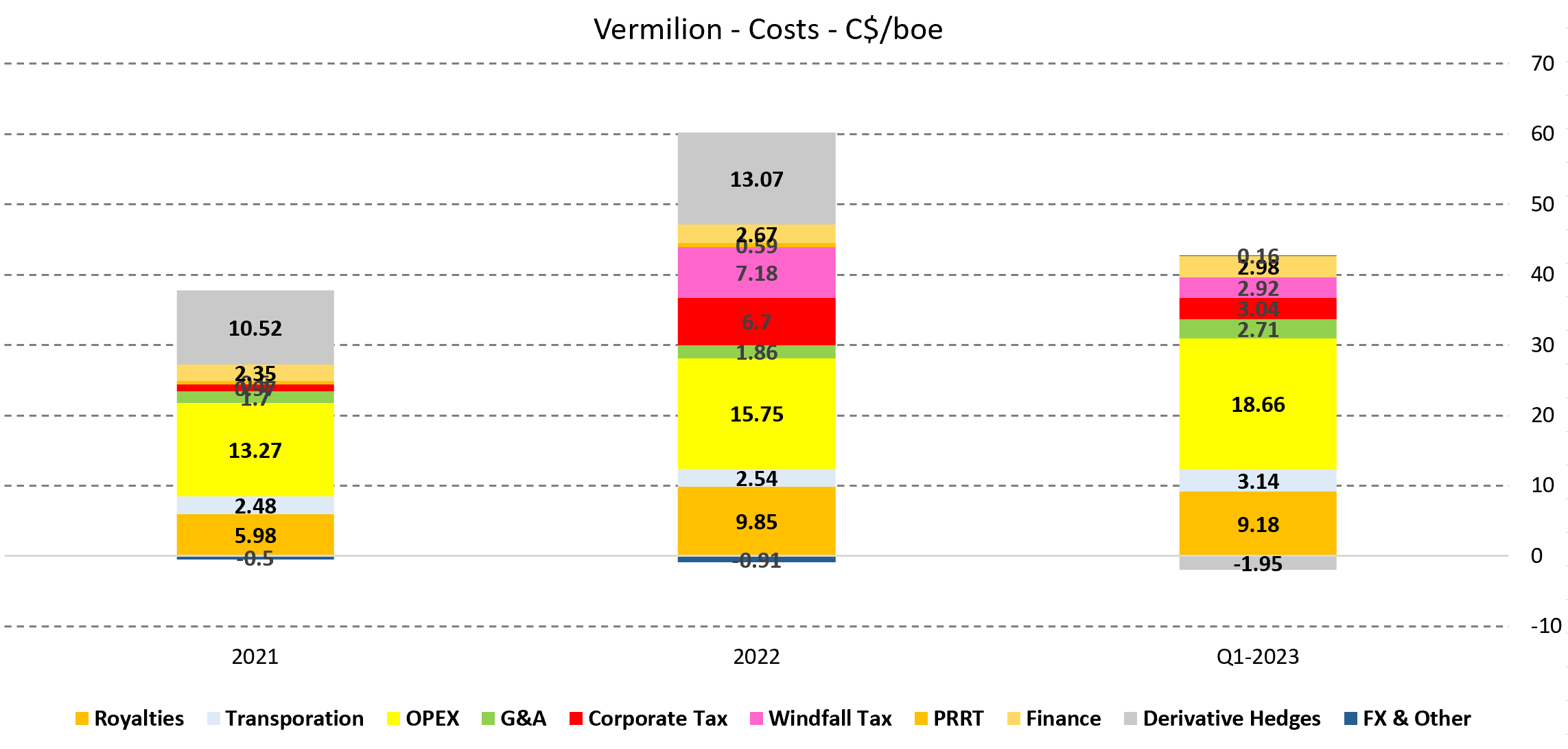

The relatively low costs have also had an impact, even if there were some YoY increases. For example, we can see that the controversial windfall profit tax only accounted for C$2.92/boe in Q1-23, even if we did see royalties increase as well.

{kind=link}

Valuation & Conclusion

Vermilion's stock price has gotten severely punished over the last year, while part of the decline is justifiable due to lower energy prices, the size of the decline has in my view been excessive.

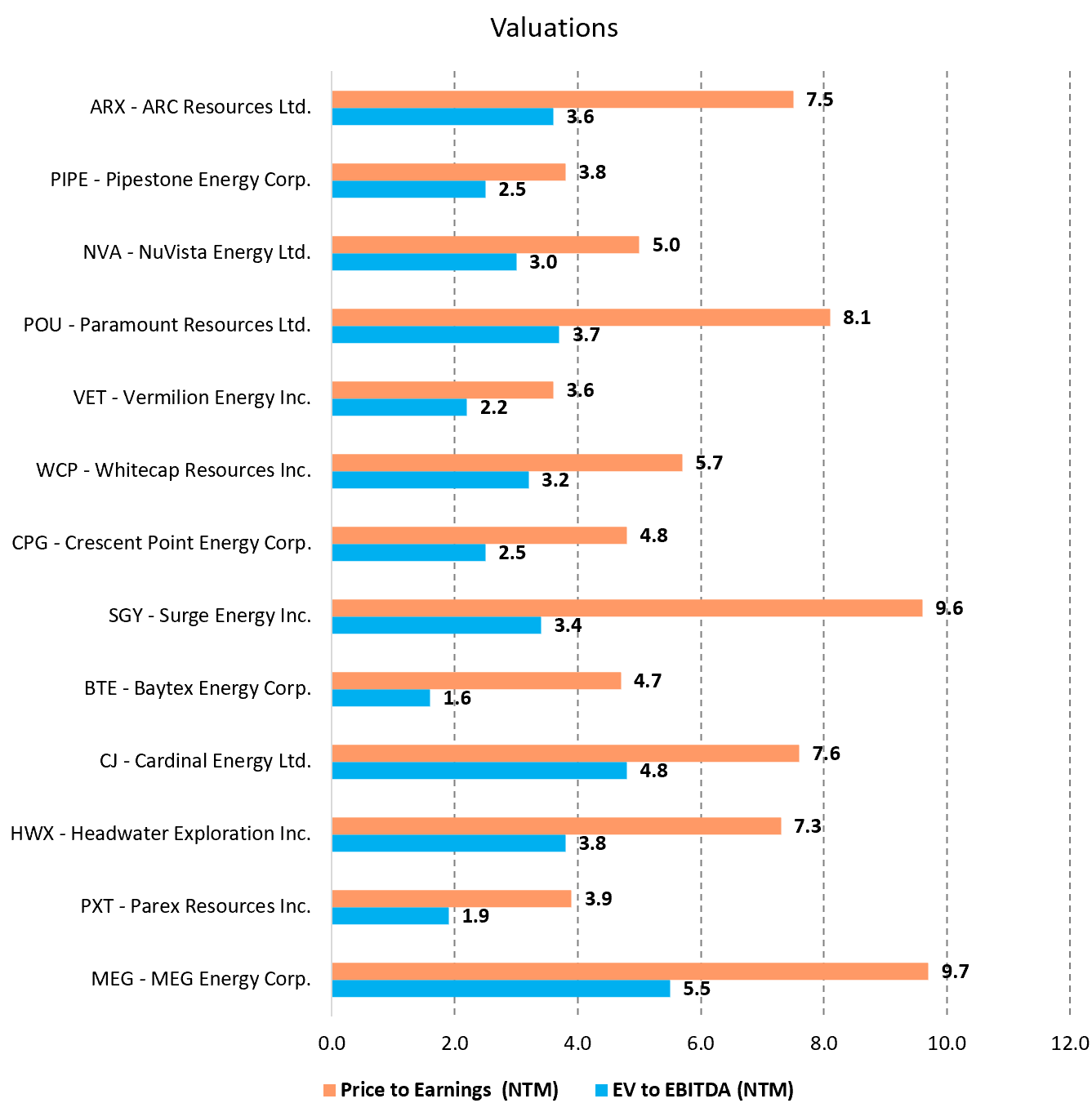

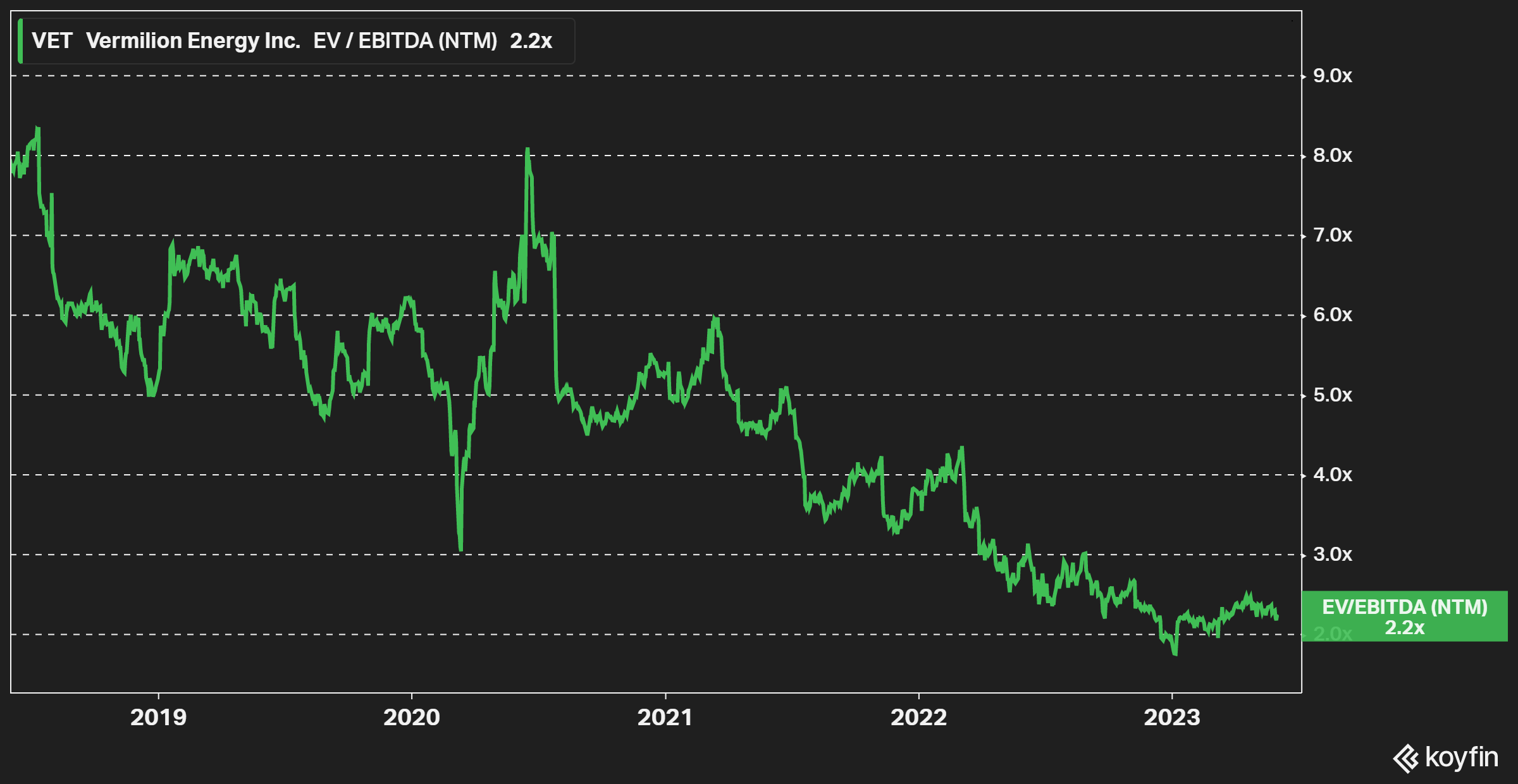

The below figures look at the forward-looking EV/EBITDA and P/E ratios for Vermilion and a few peers. Where we can see that Vermilion is extremely cheap on an absolute basis, relative to peers, and in relation to its own history.

{kind=link}

{kind=link}

It remains to be seen what will happen with the European windfall profit taxes next year. The weaker the energy prices, the higher the likelihood of a rollback. That would naturally improve the profitability for Vermilion in 2024 and beyond. If we get another substantial energy price spike leading up to next winter, the probability is higher that some or all windfall profit taxes remain. While I strongly dislike the idea of punishing one specific industry arbitrarily, Vermilion should be able to thrive regardless of the outcome with the windfall profit taxes in the European Union.

For further details see:

Vermilion: The Q1-23 Result Confirms The Attractive Valuation