VRNA - Verona Pharma's Ensifentrine: Potentially A New Era In Respiratory Disease Treatment

2023-11-18 02:54:02 ET

Summary

- Verona Pharma is a biopharmaceutical company focused on developing and commercializing innovative therapies for respiratory diseases.

- Their main candidate drug, ensifentrine, has shown promising results in clinical trials for COPD, cystic fibrosis, and asthma.

- The potential market for ensifentrine is significant, with millions of patients worldwide, and it could capture a significant portion of the COPD treatment market.

- I think that despite its current pre-revenue status, enfinentrine's imminent commercialization in 2H 2024 offsets VRNA's inherent risks and makes VRNA a good "buy" at these levels.

Verona Pharma ( VRNA ) is a biopharmaceutical company based in London with offices in the US. VRNA´s main candidate drug is ensifentrine, a promising treatment for patients suffering from COPD, cystic fibrosis, and asthma. This medicine is a bronchodilator and non-steroidal anti-inflammatory agent that has demonstrated promising results in clinical trials. In over a decade, ensifentrine constitutes the first major advancement in respiratory therapy, making it VRNA’s crown jewel. Ensifentrine has been granted a PDUFA date in June 2024, and VRNA is prepared for commercialization post-FDA approval around 2H 2024. In my view, I think there are inherent risks related to VRNA’s nature as a pre-revenue biopharmaceutical company. However, ensifentrine’s tangible use and market are undeniable valuation drivers that suggest it's a good “buy” at these levels.

Business Overview

Verona Pharma is a biopharmaceutical company headquartered in London, UK, with offices in Raleigh and Savannah in the US. The company aims to improve the health and quality of life of millions affected by chronic respiratory diseases, focusing on developing and commercializing innovative therapies for unmet medical needs to alleviate these illnesses. If successfully developed and approved, VRNA's product candidate, ensifentrine, can be the first therapy for treating respiratory diseases that combines bronchodilator and non-steroidal anti-inflammatory activities in one compound, the first novel treatment for these illnesses in over a decade. This product is an inhaled therapy that opens the patient's airways and reduces the lungs' inflammation to provide relief from conditions such as chronic obstructive pulmonary disease (( COPD )), cystic fibrosis (( CF )), and asthma.

Source: Investor Update Commercial Presentation, October 2023.

Ensifentrine was successfully evaluated in the Phase 3 ENHANCE clinical trials for the maintenance treatment of COPD. Ensifentrine met the primary endpoint in ENHANCE-1 and ENHANCE-2 trials, demonstrating improvements in lung function. VRNA sought approval from the US FDA for ensifentrine, and the FDA assigned a PDUFA date of June 26, 2024. There is optimism concerning the FDA approval because of the positive results of the clinical trials. Moreover, additional analysis of the ENHANCE-1 and 2 data demonstrates reductions in (COPD) exacerbations and potential reduction in healthcare resource utilization.

Additionally, VRNA is expanding to China, collaborating with its development partner, Nuance Pharma. VRNA is also advancing two new clinical programs. The first presents a combination of ensifentrine with glycopyrrolate for (COPD) maintenance treatment, and the second is a trial for non-cystic fibrosis bronchiectasis.

VRNA's Market Context and Dynamics

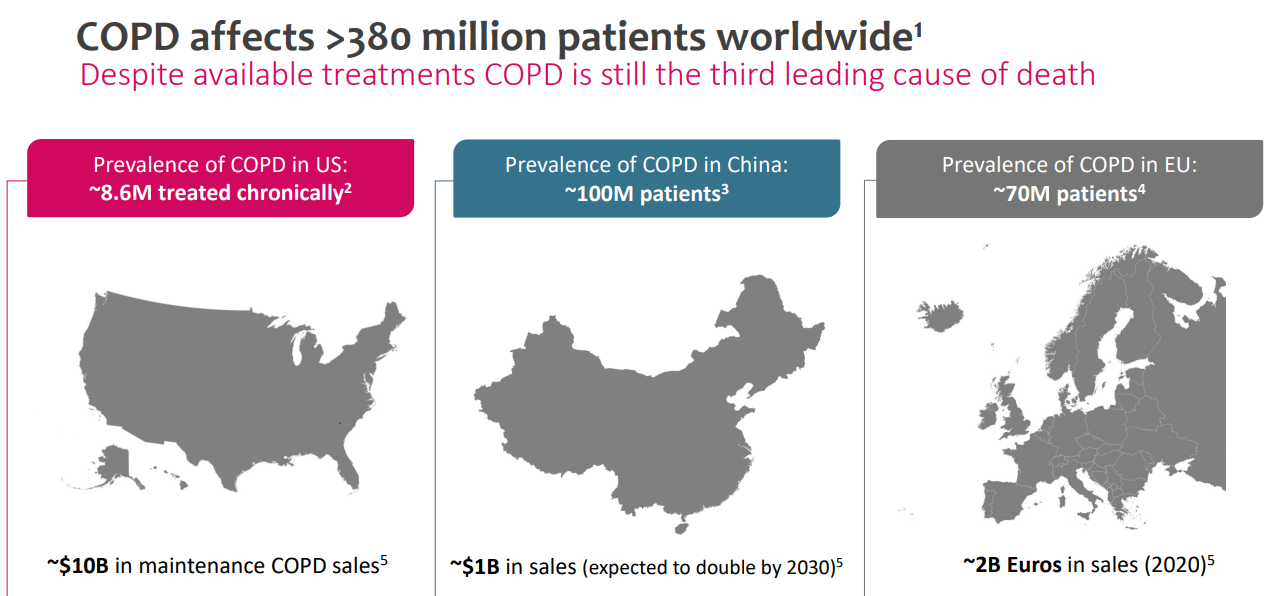

It’s also worth noting that COPD affects more than 380 million patients worldwide, and it is the third leading cause of death worldwide. VRNA's target market would be the population being treated for COPD symptoms in the US, which is estimated to be approximately 8.6 million patients treated chronically, corresponding to approximately $10.0 billion in maintenance treatments for this disease. The prevalence of COPD in the EU is roughly 66 million patients , and most don't even know it. In China, the prevalence is estimated at around 100 million .

COPD Prevalence and Treated US Population. (Source: Investor Update Commercial Presentation, October 2023.)

{kind=link}

Naturally, the potential competitors for ensifentrine in the COPD and asthma treatment markets are GlaxoSmithKline ( GSK ) with its drugs Advair (fluticasone/salmeterol), Anoro (umeclidinium/vilanterol) and Breo (fluticasone furoate/vilanterol); Boehringer Ingelheim with the Spiriva (tiotropium) prescription, AstraZeneca with Symbicort (budesonide/formoterol) for asthma and COPD. Also, Big Pharma companies like Novartis offer drugs like Ultibro Breezhaler (indacaterol/glycopyrronium) for COPD, Pfizer with Spiriva (in collaboration with Boehringer Ingelheim. Teva Pharmaceutical Industries provides a range of inhaler-based treatments for asthma and COPD, including ProAir (albuterol) and Qvar (beclomethasone), Chiesi Farmaceutici, known for their drug Trimbow, a combination inhaler for COPD treatment, and Mylan's Viatris generic versions of popular asthma and COPD medications with a competitive price in the market. Thus, the market is huge, and plenty of competitors exist.

{kind=link}

VRNA's ensifentrine is exciting news for investors. (TradingView.)

However, ensifentrine can be an add-on therapy complementary to the maintenance therapy that the patients are currently receiving. Patients who are in maintenance therapy can use ensifentrine not necessarily to replace the current treatment but in addition to it as an effective supplementary treatment. Approximately 1.8 million patients are currently treated with either LAMA (Long-Acting Muscarinic Antagonist), LABA (Long-Acting Beta-Agonist), or ICS (Inhaled Corticosteroids) therapies. Also, 1.0 million patients receive LABA and LAMA prescriptions, and 1.6 million patients are on a triple therapy of LABA, LAMA, and ICS in the US.

Therefore, ensifentrine could capture a significant portion of the COPD treatment market, appealing to many patients due to unmet medical needs and the hope for new, more efficient therapies. It is worth noticing that ensifentrine is not a typical COPD treatment; it is a novel treatment option for COPD that is neither a LAMA, LABA, nor an ICS medication. It is a first-in-class drug with a unique mechanism of action because it is a dual inhibitor of the enzymes phosphodiesterase 3 (PDE3) and phosphodiesterase 4 (PDE4). This dual inhibition leads to bronchodilator and anti-inflammatory effects.

Source: Investor Update Commercial Presentation, October 2023.

Solid Footing Prior Ensifentrine's Launch

Recently, VRNA reported on November 2, 2023, a solid foundation for ensifentrine commercialization upon FDA approval in the PDUFA date on June 26. They are funded through at least the end of 2025, with their current financial resources of $257.4 million in cash, plus some expected UK tax credits. VRNA also has $130.0 million in potential future draws from a debt facility, which should provide enough funding for the next twelve months. Overall, VRNA's financial performance was better than expected, with a GAAP EPS of -$0.02, which beats by $0.14.

Still, VRNA registered a net loss of $14.7 million, a decrease compared to the same period in 2022. Moreover, R&D costs were significantly lower than in the previous year. For context, for the quarter ending September 2023, VRNA spent about $3.0 million in R&D, compared to the same quarter in 2022, where the figure was $9.8 million. This is a huge drop. Meanwhile, SG&A expenses increased, unlike R&D, mostly due to increased preparations for the potential commercial launch of the ensifentrine??. So, this seems to suggest that VRNA is now gearing up for its commercialization stage, and the financial posturing backs this up. Indeed, their latest quarterly filing says VRNA aims to begin commercialization in 2024, subject to the approval of its NDA (New Drug Application). Moreover, VRNA has key hires ready, and the company has developed relationships with physicians and payers, highlighting their readiness for fast commercialization post-approval??.

Upside Valuation Potential

The valuation equation of VRNA is rather simple, though still somewhat speculative. As you might imagine, the company is still pre-revenue, but ostensibly, it’s on the cusp of starting to be profitable in 2H 2024. However, we must grasp VRNA’s current pricing against its revenue potential to determine if it's a good investment. For this, the company has actually given us some fascinating information in a slide deck for investors.

Source: Investor Update Commercial Presentation, October 2023.

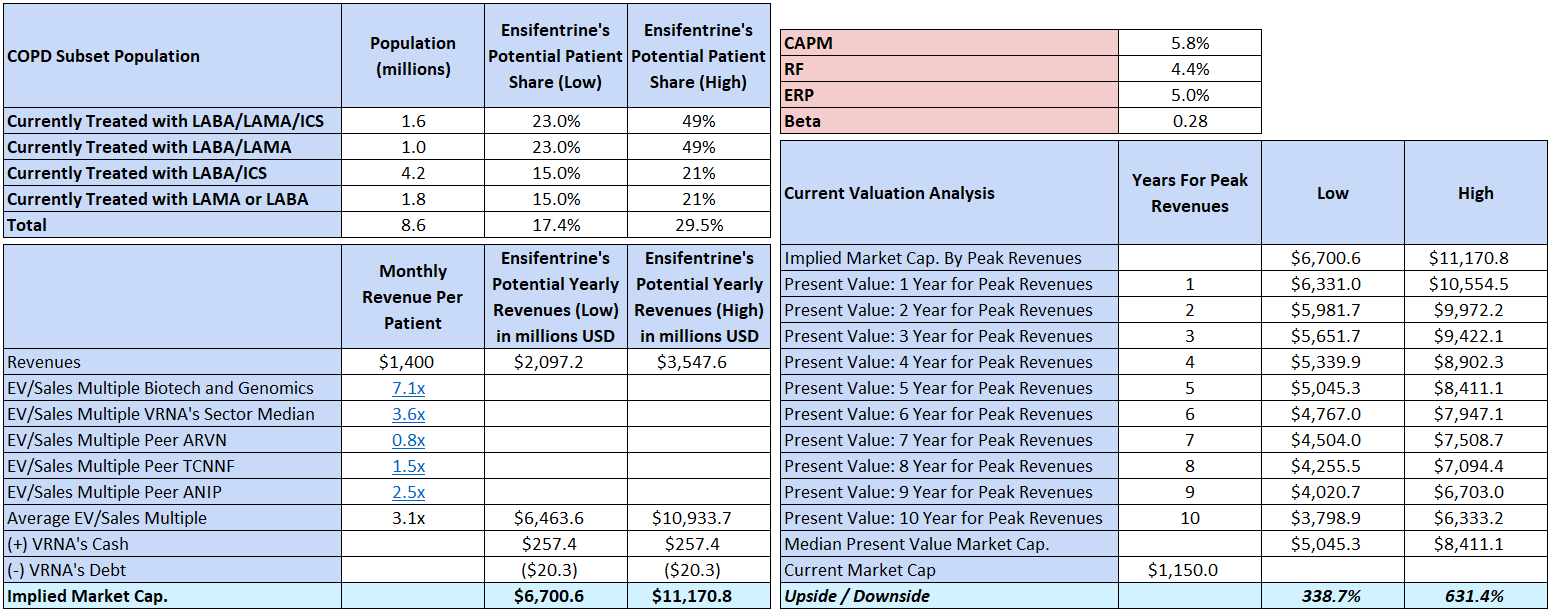

Currently, VRNA’s market is estimated to be approximately 8.6 million patients (US patients being treated), of which 6.0 million were directly targeted in the company’s ENHANCE trials. As you can see in the image above, the company estimates it can eventually reach a 15% to 21% market share within this COPD population subset. Additionally, it’s worth noting that VRNA also thinks that the 1.6 million patients currently treated with LABA/LAMA/ICS and the 1.0 million treated with LABA/LAMA could also use ensifentrine as a complementary treatment. In fact, VRNA estimates that via this approach, they could eventually get a 23% to 49% market share in these two other COPD population subsets.

Source: Investor Update Commercial Presentation, October 2023.

Moreover, the company aims to price ensifentrine at roughly $1,400 per month per patient. As previously noted, this is a long-term treatment, so these will likely be recurrent revenues for many years. However, it’s worth mentioning that the current price tag is slightly above the median price point for the current COPD treatments (see image above). It’s possible that given ensifentrine’s effectiveness and viability as a complementary treatment, coupled with Medicare’s favorable pricing dynamics for customers, the company can grow a niche within the 8.6 million target market.

{kind=link}

Author's elaboration.

Using the company’s estimates, I calculate that VRNA’s peak sales could be roughly $2.1 billion to $3.6 billion annually. However, it’s difficult to anticipate when VRNA will reach such revenues precisely. Moreover, we don’t know the actual margins the company will be able to extract during the commercialization process, nor do we know the required CAPEX for expansion.

Nevertheless, we can bypass those variables using an EV/Sales multiple. Determining the appropriate multiple is a trick, so I’ve compiled a few multiples and then taken their average. I used the biotech and genomics sector multiple, VRNA’s sector , and peer multiples. The results are visible in the table above. After adjusting implied EV estimates for VRNA’s cash and debt , we can get a rough back-of-the-envelope valuation estimate for its market cap. However, depending on how long it takes to reach those peak sales, the discounted present value of that market cap estimate will fluctuate. Using the CAPM as the discount rate, I estimate that the median present value for VRNA should be around $5.0 to $8.4 billion, which is between a 338.7% to a 631.4% upside potential from current levels.

Nevertheless, I don’t want to give a precise price target because that’s beside the point. The key takeaway is that the company appears exceedingly cheap at these levels when juxtaposed to its valuation potential and high likelihood of successful commercialization. Thus, I think VRNA is a clear “buy,” but it’s worth remembering it’s a speculative company, so size your position accordingly.

Risks to the Investment Thesis

Nevertheless, tempering expectations as investors is important. The above isn’t a target price, nor do I think that’s a sensible investment thesis. I think it illustrates the upside potential for the company, assuming everything goes according to plan with no meaningful setbacks, which is rarely the case. In this spirit, I think it’s vital to consider the risks to VRNA’s otherwise promising investment prospects.

At this point, the principal risk for VRNA is not receiving FDA approval on June 26, 2024. If there are delays or negative outcomes from the FDA, it would be detrimental to the company's financial projections. Another risk is that VRNA may need help scaling production to meet market demands; shortages produced for several reasons will impact revenues and market presence. Additionally, VRNA must ensure that ensifentrine's pricing is appropriate to be competitive in the market and that health insurance covers it totally or partially. Lastly, VRNA products are expanding to China, which involves regulatory, cultural, and operational challenges that the company and its partner Nuance Pharma must face successfully.

Conclusion

Overall, the company is an interesting investment in the sector. Its key product, ensifentrine, is promising and versatile from a market penetration perspective. It can be either a standalone treatment or a complement to the current treatment regimens for COPD patients. Moreover, it’s the first meaningful new product developed for this affliction in roughly a decade, meaning its market and patient base will likely be receptive to VRNA’s latest offering. I think the upside is evident and undeniable from a valuation potential analysis. Yet, it’s important to constrain the optimism around this rosy outlook with the inherent risks related to clinical-stage biopharmaceutical companies like VRNA. Most of the uncertainties have indeed been removed given VRNA’s ENHANCE trials, which have brought ensifentrine near the cusp of FDA approval for its NDA. But uncertainties remain until it’s approved, and then even after that, commercialization remains a challenge. This will still require CAPEX to expand production capabilities, distribution networks, and marketing campaigns to introduce this new product to COPD patients. Moreover, ensifentrine’s pricing dynamics are slightly higher than current offerings, so there are no evident pricing advantages. But, taking a step back, I think VRNA offers a promising investment opportunity at its current valuation because the upside potential far outweighs the risks. This is why it is worth rating it a “buy” at this level is worth rating.

For further details see:

Verona Pharma's Ensifentrine: Potentially A New Era In Respiratory Disease Treatment