NVSEF - Vertex Pharmaceuticals Looks Expensive Though It Isn't

2023-11-16 23:16:56 ET

Summary

- Vertex Pharmaceuticals Incorporated is a global $90-billion market-cap biotechnology company specializing in developing transformative medicines.

- Despite the close-to-zero growth in EPS, the Company maintained a strong financial position, ending the quarter with $13.63 billion in cash and investments, and continued to allocate cash to share repurchases.

- 2024 should provide VRTX with a wealth of new catalysts for operational growth, which should lead to a further increase in sales and operating profits.

- We need to look at FCF yield and margins first. With these things, VRTX is getting better and better every year despite its rising market capitalization.

- Without giving a specific price target, I am taking the risk and giving the stock a Buy rating today.

The Company

Vertex Pharmaceuticals Incorporated ( VRTX ) is a global $90-billion market cap biotechnology company specializing in developing transformative medicines. They focus on treating serious diseases, with a primary emphasis on cystic fibrosis ((CF)). The company has 4 approved medicines for CF and is actively working on additional treatments for CF, as well as other conditions like sickle cell disease, beta thalassemia, and pain disorders. They have a triple combination regimen, TRIKAFTA/KAFTRIO, widely used for CF treatment. Vertex is also exploring mRNA and genetic therapies for CF patients without benefit from current treatments. The firm reports for 1 business segment - pharmaceuticals.

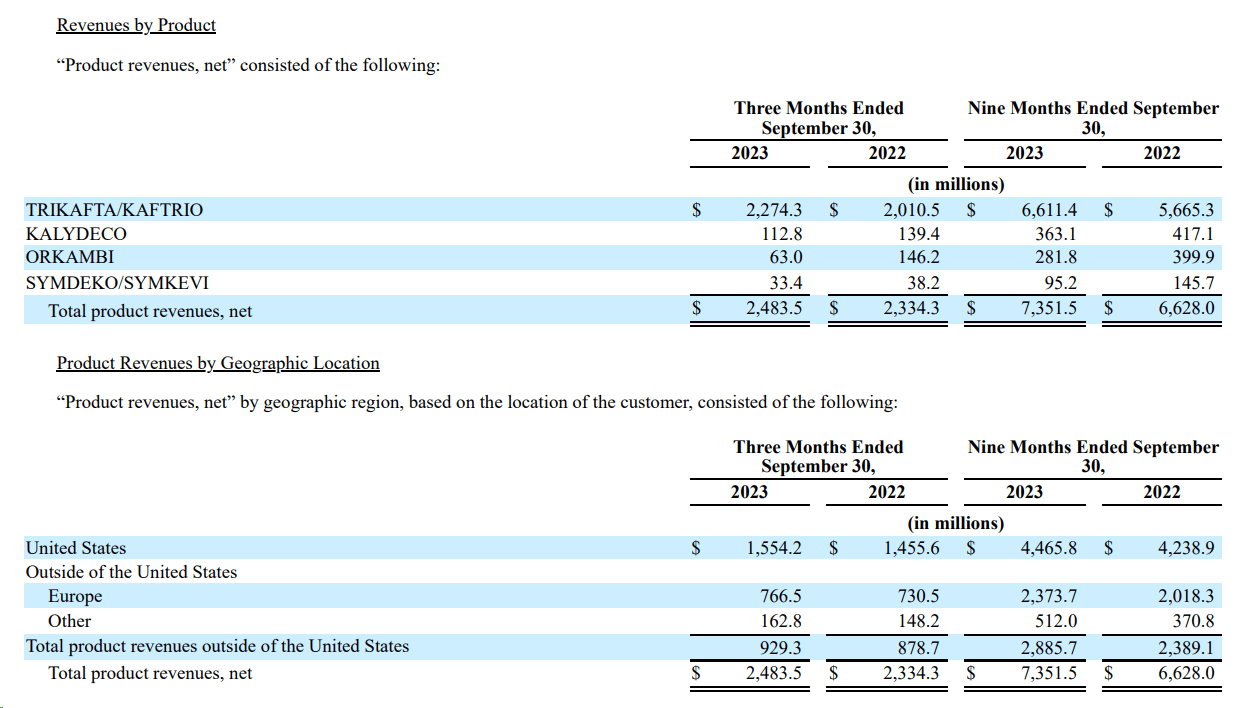

In Q3 FY2023 , Vertex showcased robust financial performance, reporting a 6% YoY increase in revenue to $2.48 billion. This growth was chiefly attributed to a 7% YoY expansion in U.S. revenue, driven by the recent FDA approval of TRIKAFTA for patients aged 2-5. Internationally, revenue experienced a 6% YoY boost, reflecting the sustained strong adoption of TRIKAFTA/KAFTRIO in markets with recent reimbursement achievements and expanded label coverage for younger age groups. Despite a $150 basis point headwind from changes in foreign currency, the YTD revenue reached $7.35 billion, marking an 11% growth over the corresponding period in the prior year.

{kind=link}

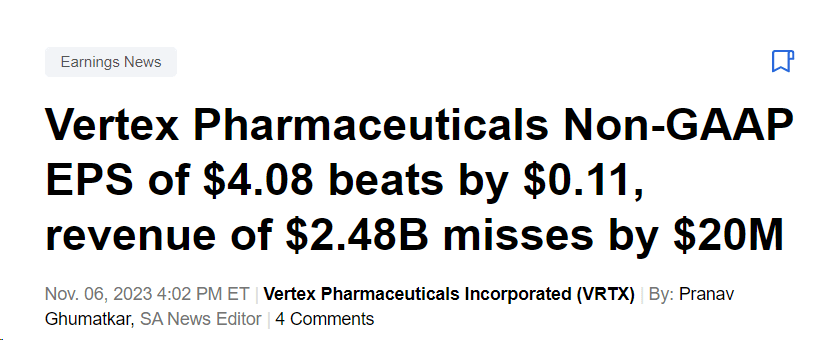

During Q3 FY2023, Vertex reported total operating expenses of $993 million, a notable increase from $758 million in the same period of 2022. This rise was in line with expectations, driven by continued investments in research and development (R&D). Key areas of increased investment included clinical studies for VX-548 in acute pain, the vanzacaftor triple in CF, and initiatives related to type 1 diabetes. The non-GAAP operating income for Q3 2023 was $1.17 billion, reflecting a 2% growth in non-GAAP EPS, which stood at $4.08, beating the consensus by $0.11 (~3%).

Seeking Alpha, post-earnings reaction

{kind=link}

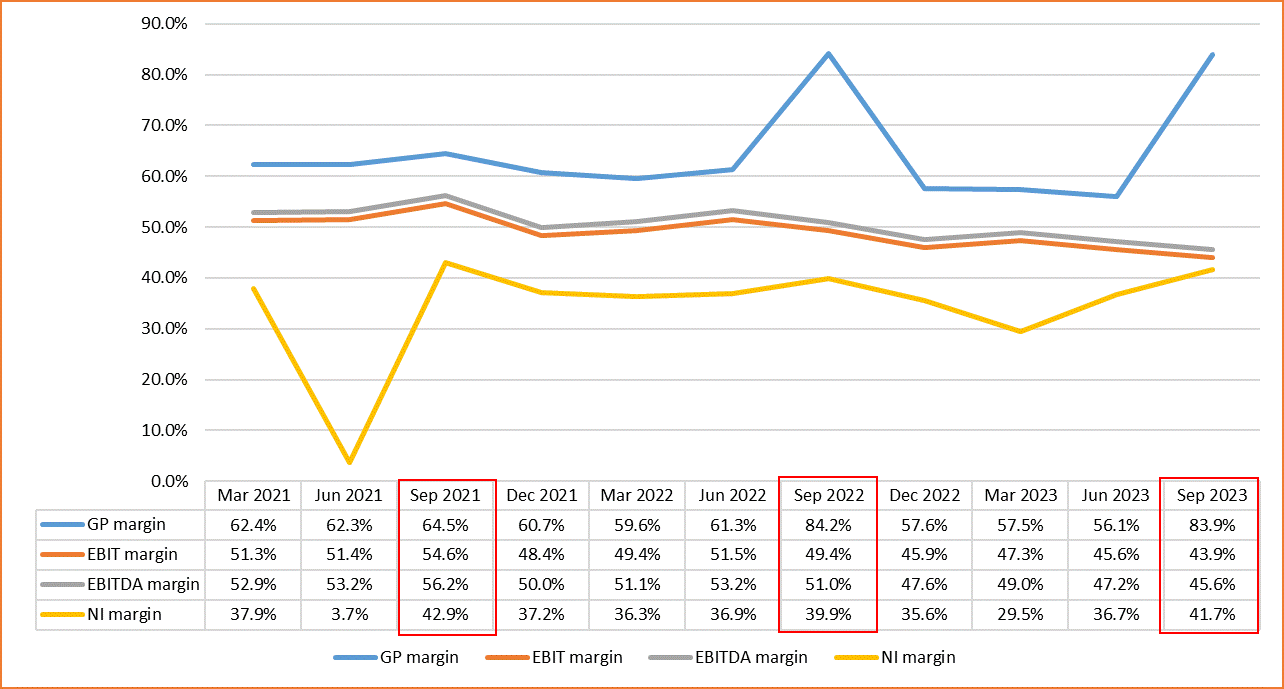

As far as the dynamics of the company's margins are concerned, we see an improvement in net profit compared to the previous year, but a slight dip in gross profit and EBITDA:

{kind=link}

Despite the close-to-zero growth in EPS, Vertex maintained a strong financial position, ending the quarter with $13.63 billion in cash and investments, and continued to allocate cash to share repurchases, spending ~$285 million to repurchase ~900,000 shares YTD, the CFO commented during the earnings call . As of September 30, 2023, it had $2.72 billion remaining on its repurchase authorization.

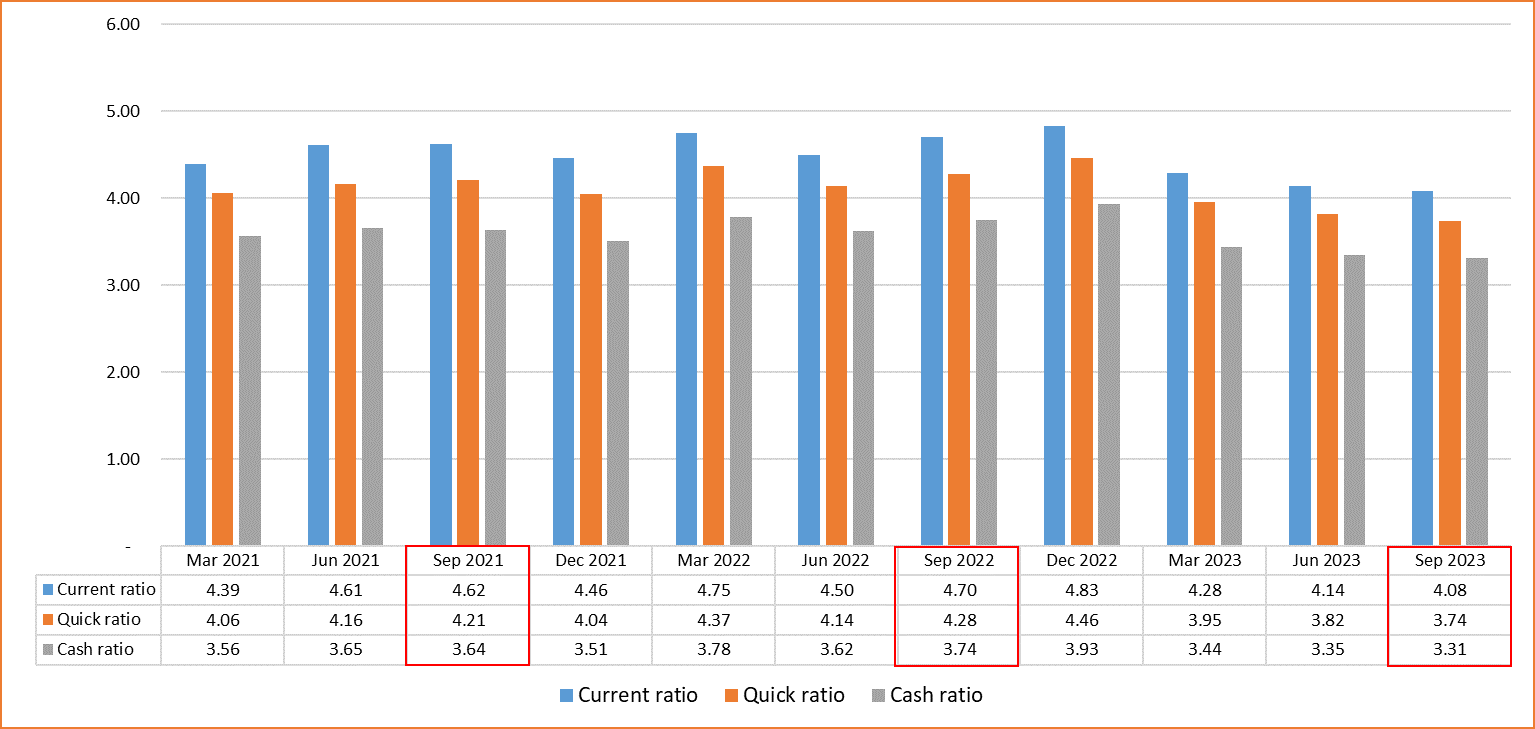

In terms of liquidity, I do not see any serious problems: In general, VRTX keeps its current, quick, and cash ratios well above 1 from quarter to quarter:

{kind=link}

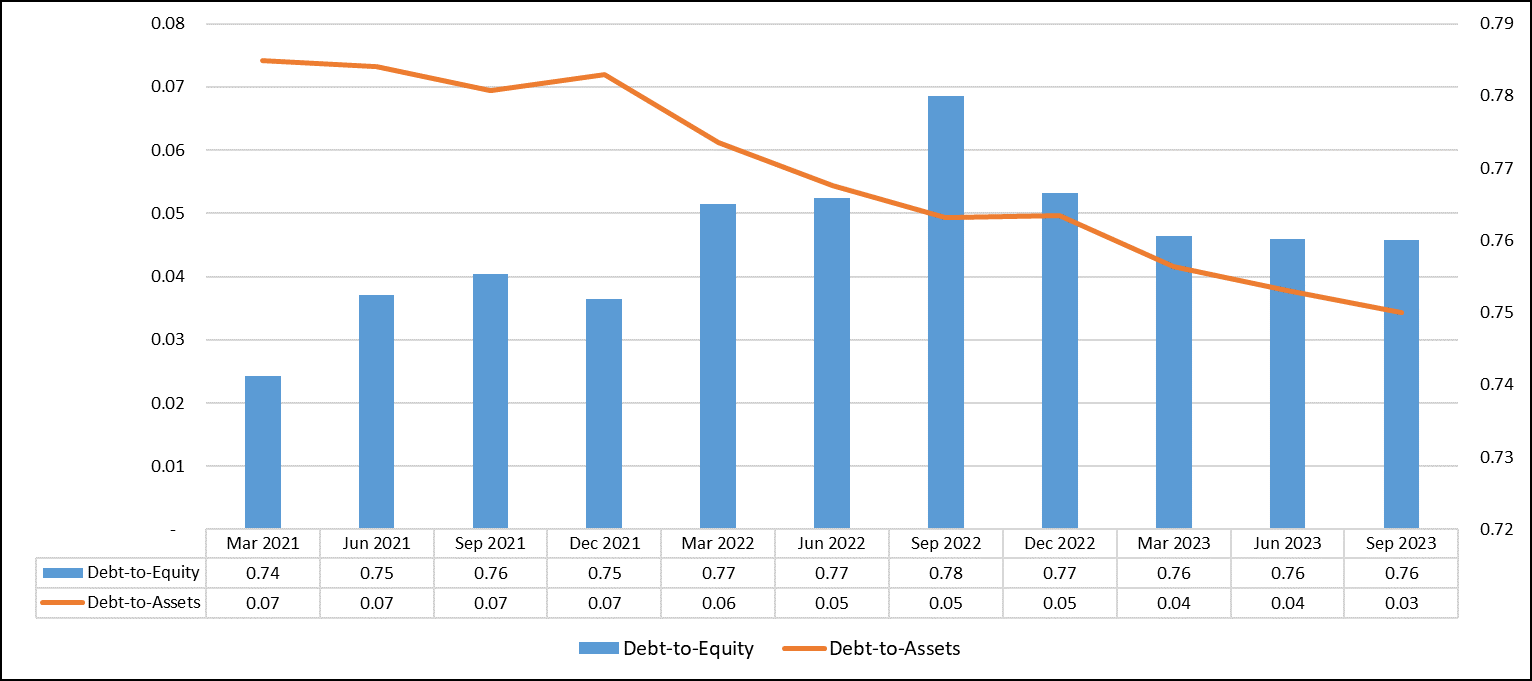

Total debt was $745 million in Q3, down from $900 million at the end of FY2022, and accounted for 4% of total capital - down from 6% and below the peer average of 16%, according to Argus Research [proprietary source]. It is worth noting that VRTX's leverage ratios continue to fall, indicating a gradual improvement in the company's already strong balance sheet:

{kind=link}

In discussing new launches (earnings calls and conferences ), Vertex Pharmaceuticals anticipates FY2024 as a foundational year for exa-cel, emphasizing transformative patient outcomes. VX-548 is positioned as an innovative option for the estimated 80 million U.S. patients with acute pain, with a focus on leveraging a specialty sales force for hospital-driven sales. The company sees a commercial opportunity in peripheral neuropathic pain ((PNP)), aiming to address the needs of approximately 10 million annual PNP patients with its specialty model. The neuropathic pain market as a whole is expected to reach a value of $4.9 billion by 2030, with a CAGR of ~4.72%, according to a report by Market Research Future . So I expect Vertex to be well positioned to capture much of this growth.

VRTX emphasizes VX-548's role in providing effective pain relief without the addiction potential of opioids, aligning with broader community interests and policy changes. The company notes positive market trends away from previous opioid restrictions. While leveraging existing capabilities, Vertex acknowledges the need for adaptation to a hospital institution-driven sales approach and has brought in new capabilities through its pain business unit to effectively navigate this market segment.

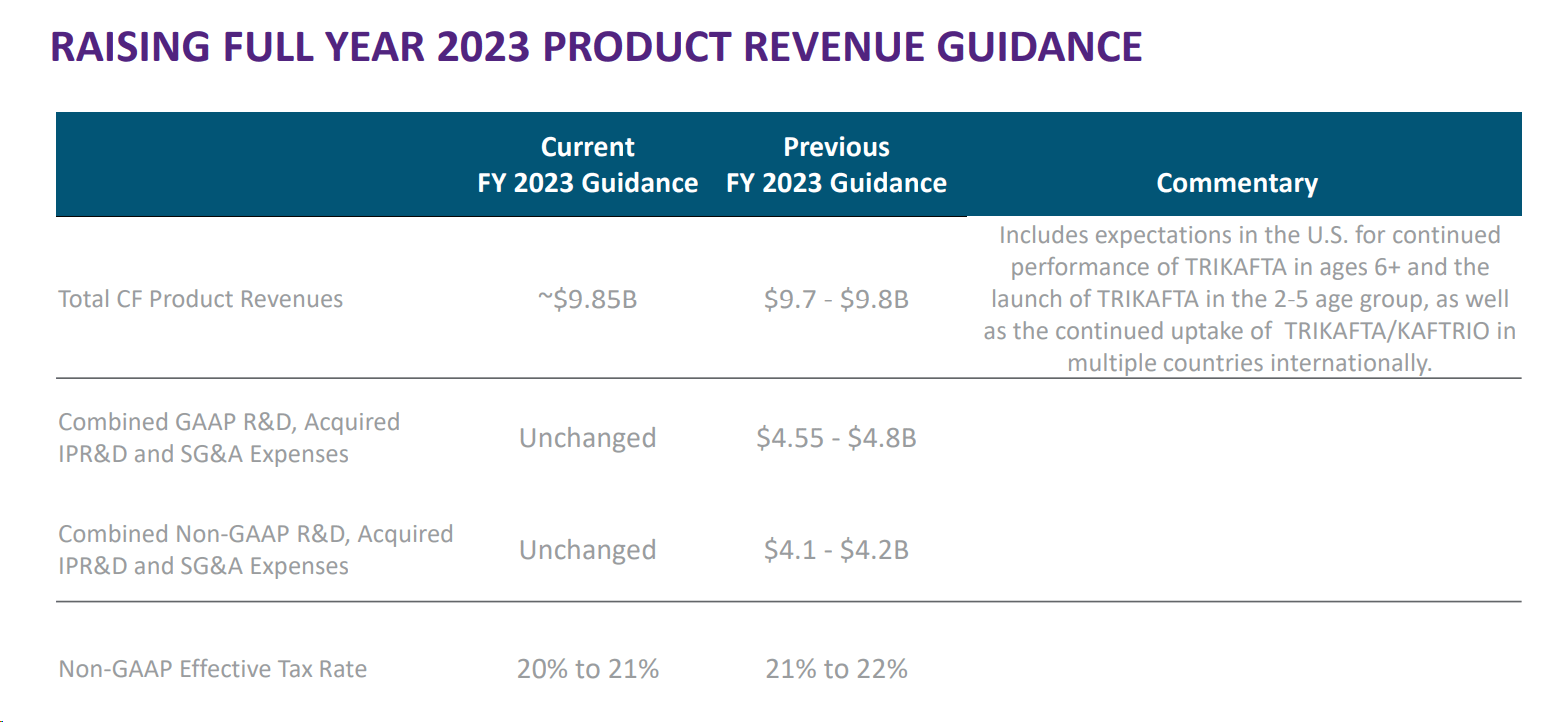

So looking ahead, the firm's management was quite optimistic about its 2023 outlook, raising its FY2023 revenue guidance to ~$9.85 billion, maintaining its expense guidance while lowering the projected non-GAAP effective tax rate by 100 basis points to a range of 20-21%.

{kind=link}

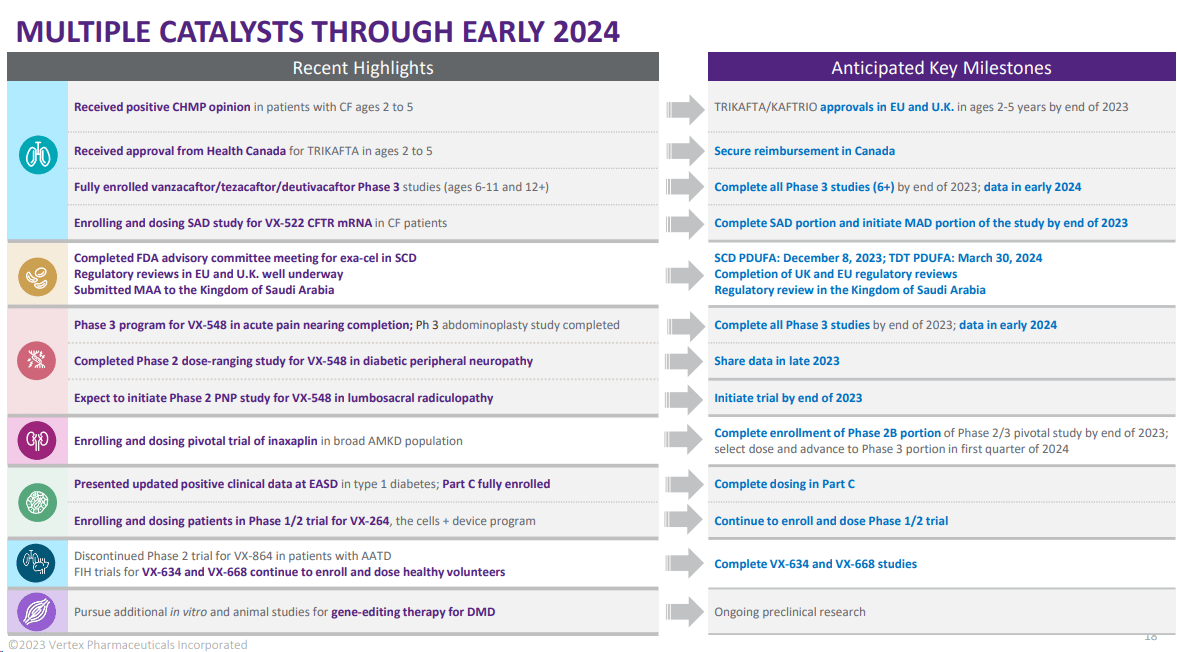

Vertex highlighted its unwavering focus on advancing programs, including multiple mid and late-stage clinical development initiatives, and emphasized ongoing investments internally and externally. As the company looks towards FY2024, it anticipates achieving further important milestones across various disease areas, solidifying its position as a leader in biopharmaceutical innovation.

2024 should provide VRTX with a wealth of new catalysts for operational growth, which should lead to a further increase in sales and operating profit against the backdrop of the existing solid financial position.

{kind=link}

But what about VRTX stock's valuation?

The Valuation

At first glance, VRTX appears to be highly overvalued, as the GAAP P/E ratio for the next year is ~23x , while the EV/EBITDA ratio is ~16.4x (35% higher than the sector 's median figure). Even in comparison with AbbVie ( ABBV ) or Novartis ( NVS ), such indicators do not appear normal:

However, we are dealing with a biopharmaceutical company where we have to consider its market positioning. Vertex is one of the largest companies of its kind, and if expectations for 2024 are met, the currently high multiples could maintain their premium thanks to operational growth (in which case the stock should continue to rise).

VRTX continues to increase its FCF yield over the long term, despite all the share price increases fueled by share buybacks (which makes the lack of dividends completely uncritical to growth). With the current FCF yield, buying VRTX today is cheaper than it was in 2018, for example, when the stock cost around $150-160.

Yes, this 4.6% yield is lower than what ABBV or NVS can show, but if you look at the projections for the growth of the companies' businesses, VRTX is expected to grow faster, justifying the existing premium.

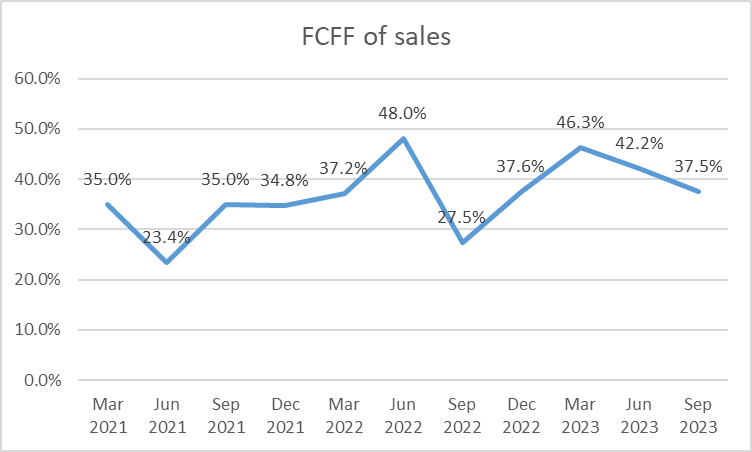

The company has averaged 37% of its revenue in FCFF over the last 12 quarters - that's a lot. I expect VRTX to have a FCFF margin of 40% in FY2024.

{kind=link}

With projected sales of $10.56 billion, that's $4.224 billion in FCFF for next year. With a market capitalization of ~$90 billion, that's a yield of ~4.7%, which is roughly in line with the current figure. So VRTX should have new opportunities for an even more massive buyback due to a higher FCFF - that's a pretty strong bullish catalyst for next year in my opinion.

The Bottom Line

Of course, investing in Vertex Pharmaceuticals stock comes with its share of risks despite its successful track record. The unpredictable nature of drug development and regulatory processes poses uncertainties. VRTX faces stiff competition, notably from AbbVie, which could impact its market standing. The company's heavy reliance on a few drugs makes it vulnerable to shifts in market dynamics or generic competition. Intellectual property challenges, potential financial strains from high debt, and the need for additional capital further compound the risks. Macro factors like economic downturns and regulatory changes also pose potential threats.

Despite all the risk factors, however, I don't think VRTX is rising in price without reason. Yes, its key valuation multiples look pretty expensive. However, investors buy such stocks primarily for growth, not value. Since VRTX doesn't pay dividends, it returns capital to investors by buying its shares back from the market, so we need to look at FCF yield and margins first. With these things, VRTX is getting better and better every year despite its rising market capitalization. The company is betting on next year, and if its upcoming products achieve the expected market success, I expect VRTX to trade much higher than it does today. Without giving a specific price target, I am taking the risk and giving the stock a Buy rating today.

Thank you for reading!

For further details see:

Vertex Pharmaceuticals Looks Expensive, Though It Isn't