EVTL - Vertical Aerospace: 2 Reasons Why This Stock Is A Strong Sell

2023-10-21 01:44:13 ET

Summary

- Vertical Aerospace is a disruptive player in the zero-emission aviation sector, offering electric vertical take-off vehicles for short-distance transport services.

- The company operates in a high-risk, cash-intensive industry that demands substantial investments and has consistently reported losses in recent years.

- The company's financial stability is delicate, with potential delays due to necessary certifications and a concerning balance sheet, making it a risky investment.

Vertical Aerospace (EVTL) is a disruptive player in the zero-emission aviation sector, offering electric vertical take-off vehicles for short-distance transport services. While I greatly admire the company's innovative design and technological advancements, there are several cautionary signs for potential investors to consider before investing in the stock.

Firstly, the industry where the company operates demands substantial investments, and there's a risk these may never yield profitability. Secondly, in the broader context of the macroeconomic environment, the company has consistently reported losses in recent years. With interest rates currently at record highs and investors shifting towards companies viewed as more "stable and secure," Vertical Aerospace may not be the most favorable option at this time.

Moreover, the potential delays associated with the necessary certifications could further jeopardize the company's already delicate financial stability.

1. The high-risk, cash-intensive industry cannot return as much as expected

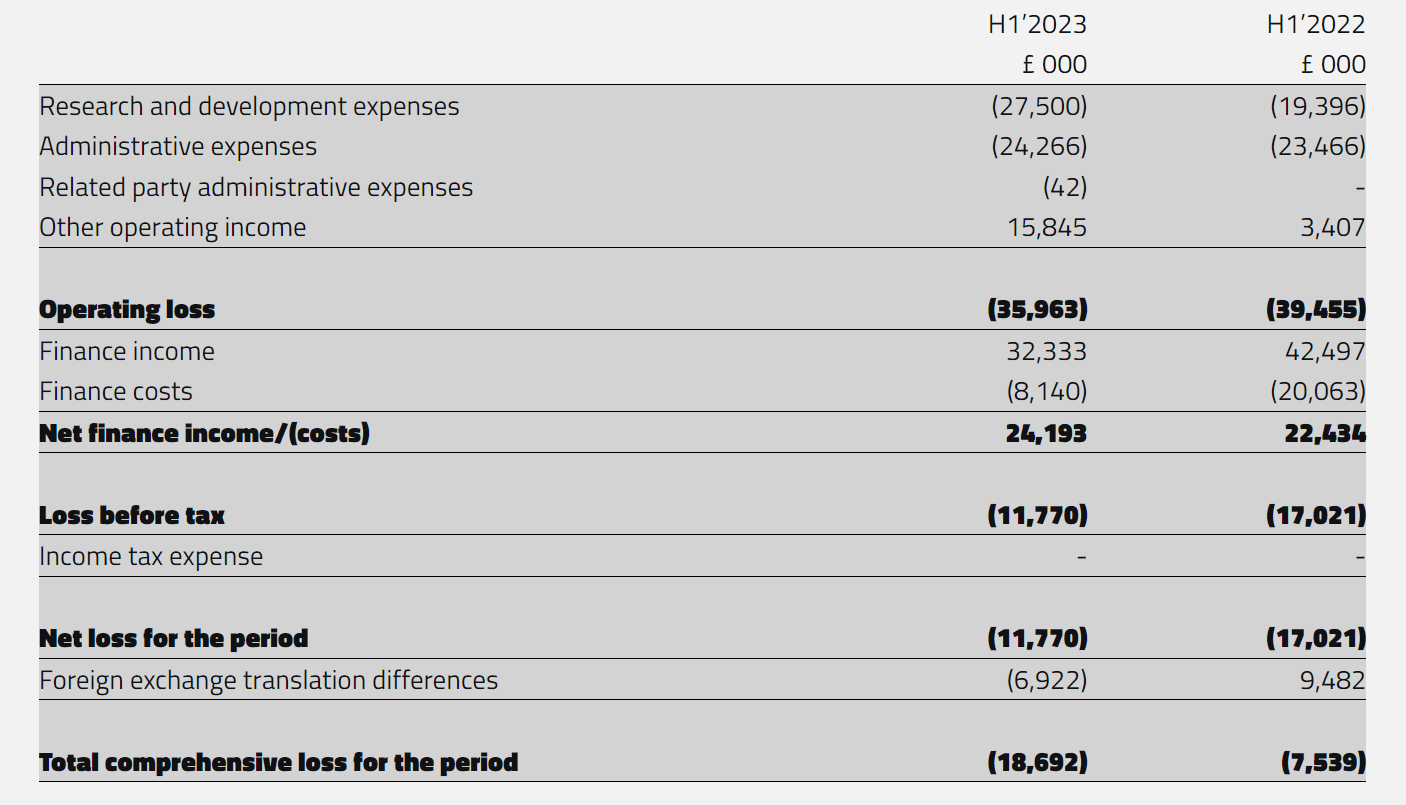

One of the significant issues with the company, in my view, lies within its operational sector. Being a disruptive company, Vertical requires substantial financing and has a high cash burn rate. Over the past few years, cash flow has consistently been negative, and as of 2022, the revenue stands at £0. The company needs to invest heavily in testing and refining its prototypes, however it has not yet reached the stage of production!

Another significant concern regards the required certifications , which have been delayed to 2026, despite earlier expectations for 2024. This means significant spending, which may not necessarily lead to mass production of its vehicles.

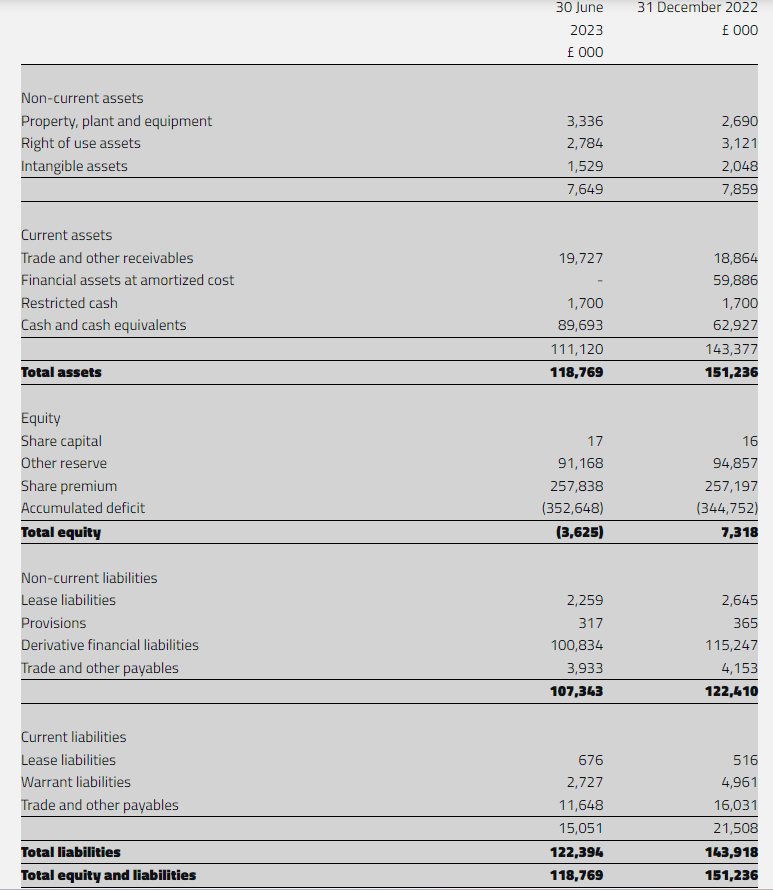

To add to this, the company's balance sheet is cause for serious concern. The current cash reserves amount to £89.69 million ( H1FY23 ), which, according to the latest statements, is sufficient to cover operations until 2024 . However, new capital injections will be necessary. This presents a truly disconcerting situation, one that could deteriorate rapidly in a short span of time, especially considering other metrics: negative equity of £3.62 million and an accumulated deficit of £352.64 million. Given that the company has no revenue, the rate at which it consumes cash is exceptionally high. At the close of the first quarter ( Q1FY23 ), Vertical had £104 million in cash, a decrease of £25 million in just 3 months. Considering that £89 million must also suffice for 2024, the financial situation is very precarious.

Vertical Income Statement (Vertical H1FY23) Vertical Balance Sheet (Vertical H1FY23)

{kind=link}

{kind=link}

Moreover, in my opinion, there's the added concern of risks associated with such a delicate sector. Consider instances of plane or helicopter accidents: aside from rigorous official investigations that often trace the problem back to the production lines, there is usually a significant media component, bringing the incident to public attention. It's easy to understand that if Vertical's aircraft were to enter operation, they would be in full view of the public, and even the slightest error or accident could result in significant setbacks, potentially wiping out years of testing and capital. As evidence of this, in 2022, a plane crash involving Boeing in China (BA) led to a more than 10% loss for the company. For a small, new company like Vertical a similar event could have even more amplified consequences.

Hence, not only does the company require vast investments for its disruptive industry, which have largely depleted its cash reserves and may never yield profitability, but also, if it were to start production and sales, the inherent risks of its sector could potentially lead to adverse outcomes, rendering it a very risky investment.

2. Right now the market does not appreciate companies like Vertical Aerospace

One crucial consideration in my investment approach is to carefully assess the international macroeconomic and geopolitical trends. This provides a clearer perspective on whether an investment holds promise or might yield mediocre returns. A business that looks excellent on paper may not necessarily perform that way in reality. At present, Vertical Aerospace falls into the latter category in my view.

We're facing a range of substantial risks at this moment, primarily from a macroeconomic point of view and, to a significant extent, from a geopolitical one as well. During times of uncertainty, investors tend to gravitate towards assets they perceive as "safer," and Vertical Aerospace isn't seen as one of them.

We can observe how the performance of growth and value companies shifts with changes in macroeconomic cycles. In the current scenario, given the high interest rates, investors are favoring stable companies with robust cash flows, which offer lower volatility. Moreover, the elevated interest rates increase the cost of debt, something Vertical Aerospace heavily relies on for ongoing testing and sustaining operations until the first vehicles are sold and payments from orders start coming in. This puts the company in a precarious situation.

In this complex mix of challenges, Vertical Aerospace operates in an environment where investors are exercising caution, avoiding risky assets. Adding to the difficulty is the limited capacity to issue new debt for financing. It is a difficult situation to manage in the long term, not to mention the risk of having potential problems regarding its cash reserves first.

Bottom line

While I find Vertical Aerospace's products promising in the long run, approaching it as an investment demands careful consideration. It's crucial to scrutinize not only the balance sheet but also the prevailing macroeconomic conditions and the industry landscape, which may conceal various challenges.

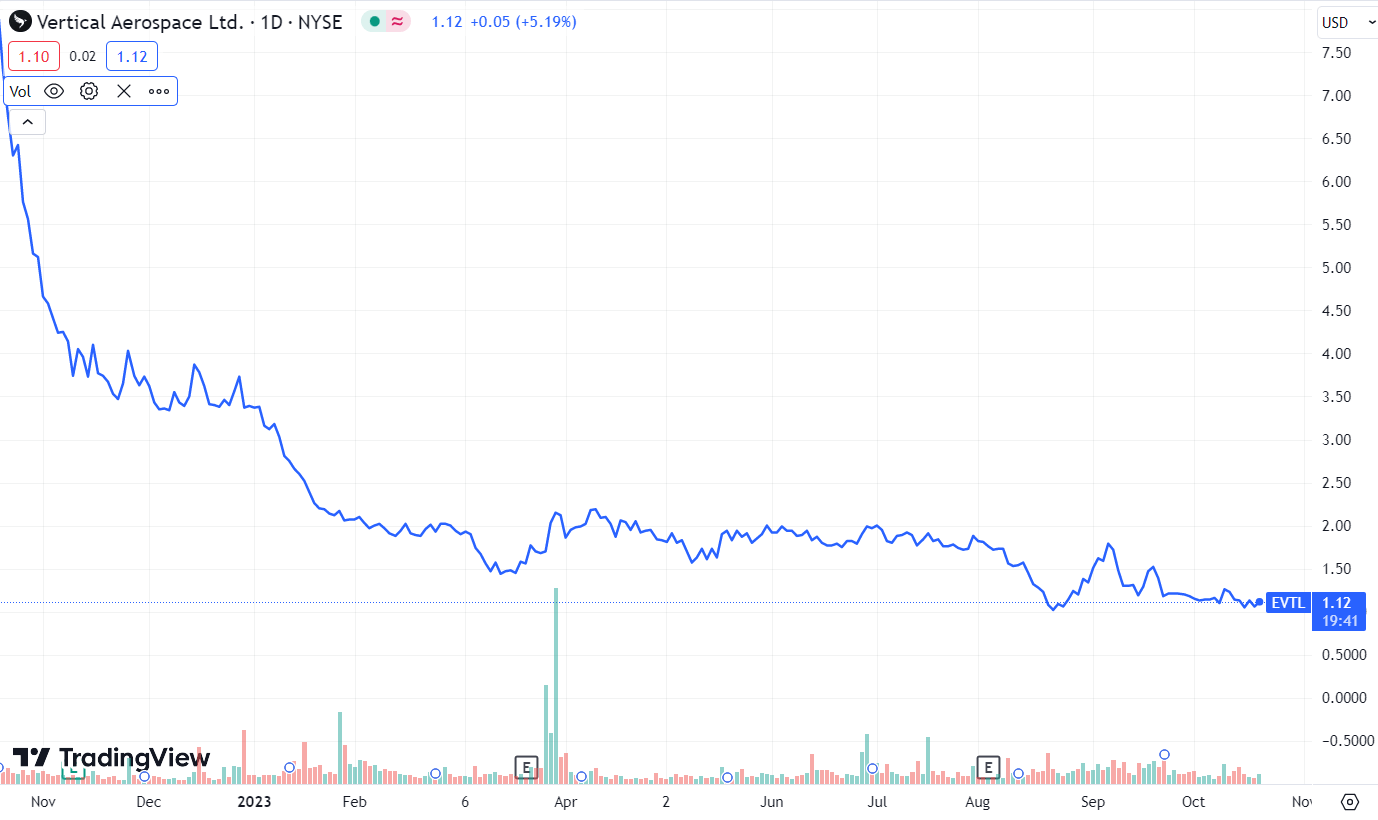

Vertical's stock has been consistently losing momentum since its IPO, and its performance hasn't improved in the past year.

Vertical 1Y Performance (TradingView)

{kind=link}

Given the current challenges and the very negative momentum of the company, I anticipate a continued decline until more reassuring signs surface regarding its cash situation. Hence, my rating for the company is "Strong Sell".

For further details see:

Vertical Aerospace: 2 Reasons Why This Stock Is A Strong Sell