VWSYF - Vestas Wind Systems: Doubt Regarding My 'Hold' But Choice Was Right

2023-08-24 03:55:59 ET

Summary

- Vestas Wind Systems is facing challenges in the wind power industry and its latest annual report shows negative financials and low profit margins.

- The company is struggling with cost increases and unprofitable contracts, leading to a decline in its share price.

- Analysts have mixed opinions on Vestas, with some predicting a recovery in profitability by 2025, while others remain cautious and recommend a hold on the stock.

Dear readers,

Vestas Wind Systems ( OTCPK:VWDRY ) is a company I've been reviewing, and investing into in a variety of ways for a few years at this point. My latest approach for Vestas, which I have used for the last year and more, has been the strategic use of options to guarantee an attractive entry price. Because while this company does come with a non-trivial sort of upside, it also comes with a fair deal of challenges, which I personally consider to be pretty non-trivial.

Still, my last stance for the company was a clear "HOLD". And this proved to be the right choice since then. I say this because the company declined almost 20%

Seeking Alpha Vestas RoR (Seeking Alpha)

So I am overall very pleased that I did not invest in the common. My puts also did not go through - I wrote new ones last week at very impressive overall pricing and premiums, ensuring myself a double-digit annualized RoR unless the company's share price crashes.

Let's see what's causing this recent trend break, and how we can take advantage of the situation to make a good deal of profit.

Vestas - Plenty to like, but plenty of challenges

So, I'm far more positively inclined towards Solar power than I am towards onshore wind power. I see plenty of challenges to this sort of power generation, and this comes both from analyst as well as professional experience because I've in my work sat in councils that have declined companies' applications to put up onshore wind parks within municipal borders.

My stance does of course not make Vestas a bad investment. It's just that I think it's worth a lot less of a premium than other analysts seem to think. This is despite it being a 125-year company, with wind turbine production since the late 70's.

The company's latest annual report is not a pleasant read, nor is the revenue/net picture anything that we want to see, as everything that matters is in the negative, with a gross profit margin of 0.8%, one of the lowest I've ever officially covered outside of tech growth stocks.

{kind=link}

There is, of course, context required here. This is not the typical sort of development for this company, nor should it be expected to stay this way for an extensive period of time.

What you're looking at is inflation- and SCM-related cost increases, driving profits to below zero. Why? Because the company, during a pandemic and ESG-highs promised to deliver plants and turbines for a certain price, contractually agreed at the time, and now essentially having to deliver at a loss because their contracts and agreements did not allow for indexation or price increases in the case of the environment we've been seeing here. Not a unique problem - Alstom ( OTCPK:ALSMY ) which I've reviewed had the same issue.

What was previously an environment where ESG and green was the buzzword of the year, with a premium being applied to anything with a wind turbine or solar cell, we're now in a much more somber environment. It's not just wind turbines or Vestas - in certain places, including Sweden (part of the Scandinavian context here), the government has removed all subsidies relevant for EVs, which has led to a massive crash in the sale of EVs. That's not just relevant by the way for the total number of sales, but also as a part of the total number of sold cars. The estimate for 2023 was 40% EV share, it's been adjusted down to 35%, with less than 90,000 EVs sold during the entire year (Source: Ny Teknik ).

This is somewhat trend-setting for ESG and these sorts of companies overall. Their overall premia are definitely deflating, and this is actually a good thing.

The latest set of Vestas results we have are the 2Q results, presented around 1-2 weeks ago. While the company was able to report an increase in top-line sales with 8%, and a 4% revenue growth - though this was driven primarily by service growth - the troubles for Vestas are far from over.

What Vestas has to do, and indeed what the company is doing, is ensuring that every delivery now comes at a profitable price, even as they execute on its unprofitable backlog. The company is still at a negative margin of EBIT -2% - so it's still pre-tax unprofitable. But it's improving from what you see above.

The company is also very careful in its wording, referring merely to "meeting its 2023 guidance", without clearly and everywhere stating what that guidance is, for the obvious set of reasons that this guidance is not necessarily all that positive.

Here are the company's problems, simply presented.

Vestas IR (Vestas IR)

The company is selling its products at a mEUR/MW price that's lower than they can afford, and while the mix is improving in the power solutions segment, the service segment seems to be what the company is beating the drum for as the major saving grace, due to the contract structure with service contracts being clause for indexation with regards to inflation.

Vestas IR (Vestas IR)

The company still, and easily, takes the position of being one of the most sustainable energy companies in the world - but you probably know my position on things like this. It's a great thing if it can be done easily, or as something profitable for the business, but as an argument for a business that's not profitable overall, it leaves a lot to be desired. Financials and cash are where it's at for me - and Vestas does not necessarily outperform significantly here.

It's also important to see these results on a granular level. Revenue was only up due to the service segment. Power solution segment revenue was down 3%, due to lower APAC activity. The EBIT margin for the segment was -6.9%, which is quite a significant way from even being profitable - but I'm not too worried about this in the long term. The issue here is getting past the backlog of horror projects, in the sense of their unprofitability of them. As long as the company can do this, then this is something I've seen more than once and doesn't cause me not to invest.

Vestas IR (Vestas IR)

In a sense, this is actually the structure Vestas has had for some time. They sell their plants at barely any profit while delivering profit in the service segment. It's not a bad business model as such, provided you can keep the service segment active, and the EBIT margin in service is over 21%, so that's solid.

However, the problem is that this only works if CapEx and OpEx are not eating up the difference. And with SG&A, this has risen almost 100 bps of revenue since 2022. There are a few components to this. Lower overall revenue, higher IT costs, inflation, and other things.

The company also saw a very high level of leverage back in 1Q23, when it reached 5.8x net debt/EBITDA, which is to be compared to below 1x back in mid-2022. It's down to 4.5x at this time, and the company is still BBB-rated, but it's still not a positive thing.

The company's margins for 2023 are expected to remain in the negative range, around -2% EBIT , though service margins are at around 22%. So it's likely to be at least until 2024 until we see improvements here in the company's profitability, which we need to take into consideration when investing in Vestas here.

Let's look at that valuation and see what we should look for if we want a good/market-beating upside here.

Vestas - A lot to like, if you buy at the right price and at the right upside.

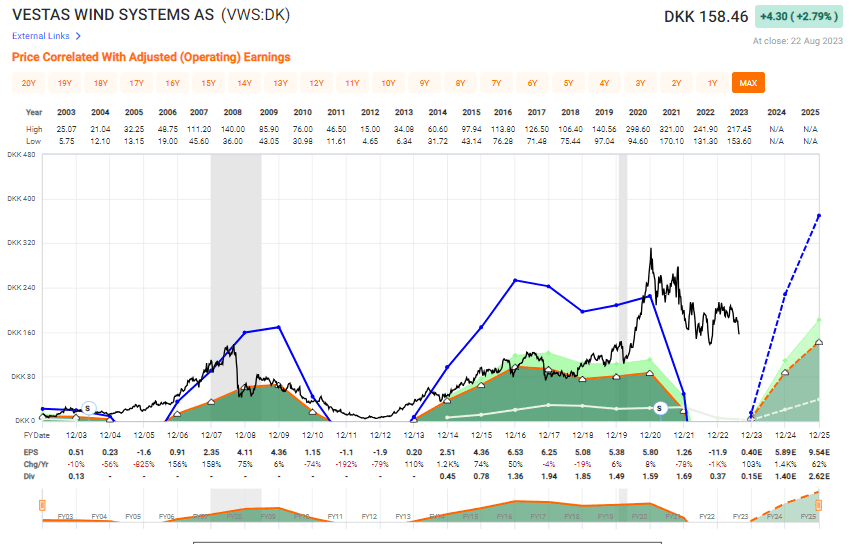

So, any quality company is a "BUY" if the price is low enough. And I do maintain that Vestas is indeed still a quality company. The company trades at native symbol VWS on the Copenhagen stock market. Today, the company is at around 158 DKK per share, which still is a high price - but below my previous PT for the company.

That means that I'm actually delivering an update here, and I'm cutting my price target by 10 DKK to account for the higher recovery period that we're seeing in this quarter. That things are going to be turning around, I don't doubt that for one second.

{kind=link}

The company's valuation here, and the forecasts, are based on Vestas managing positive adjusted EPS in the next year. I'm personally not convinced that the company will actually manage this.

That's why I'm pleased that the company's options premiums have been increasing during the down days for the past few weeks. I've been able to lock in some very impressive annualized rates of return, by committing on a 30-45 day basis to buy the company at valuations I consider attractive for the long term. In the latest set of CSPs, I was able to lock in a strike of 140 DKK , that is well below even my updated PT of 155 DKK, and I made 18% annualized using this option.

If you follow our service, you get those sorts of alerts in real-time on chat - which is really the only way to use those. You need to act more or less on the day because the next day the options premiums might no longer fulfill that 15% annualized minimum.

Remember, that 15%, that's what I want to see no matter what I invest in.

I do believe in normalization for Vestas in terms of its common share - but I believe the normalization will come far slower, impeding growth in the company than most analysts currently seem to believe.

The company has been on a negative trajectory since peaking in froth at over 300 DKK, resulting in a negative RoR of 33.35% since 2021, when it peaked. I do not believe the company is done falling, and I stated this in my last article as well, and it is proven right here.

That's why CSPs were the best option to go here and continue to be going forward.

If you forecast the company as being able to recover to around 9.5 DKK on an adjusted EPS basis by 2025E, which is the current FactSet forecast, then you could make annualized returns of over 31% here, or ROR of almost 92% in total. But these forecasts come with an accuracy rating of less than 10%, so I'd be very careful giving them any sort of faith or trust (Source: FactSet)

S&P Global has a set of targets coming in at around 190 DKK up to 450 DKK. For the one with that 450 DKK PT, my message is "Good luck". 180 is far more logical. My previous target was 165, it's now down to 155 DKK, which means I'm by far the lowest target here among the 23 others that follow the business. However, despite an average PT of 280 DKK from these 23 analysts, only 8 analysts are actually at a "BUY", while 16 are at either "HOLD", "Underperform" or "SELL". This is despite an "official" upside of almost 40% at this time.

I interpret this both as a lack of conviction and a lack of seriousness on the part of the people following this company.

Vestas is, as I see it, going nowhere in profit until at least 2024. For that reason, my strategy continues to be CSPs - and that's how I beat the market when it comes to this business.

Questions?

Let me know!

Thesis

- Vestas Wind is a well-loved Wind Turbine company that has captured the hearts and minds of many ESG investors. I like the company - but only if it can go back to the profitability that we saw years ago. I do not see this easily in the company's near-term future.

- I believe a combination of pricing pressures and at least momentary trend shifts in the energy markets will see Vestas continue to be under pressure from non-trivial inflation and operating pressure, specifically margins. This will prevent the company from rising back up quickly, rather than turning this into a slower process for the time being.

- For that reason, I am still at a "HOLD", and I give the company a 155 DKK price target. My new CSP targets are below 145 SEK/share, and this is where I currently have the contracts I "run".

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Not cheap, does not have a high upside on a realistic basis, and the dividend is a bit iffy at this time. I'm not sold on Vestas at this time, and go "HOLD".

For further details see:

Vestas Wind Systems: Doubt Regarding My 'Hold', But Choice Was Right