VWSYF - Vestas Wind Systems: One Of My Favorite Options A 'Hold'

2023-05-23 23:47:44 ET

Summary

- I've been targeting Vestas wind systems during the past year, not by straight stock buying, but by writing conservatively-priced put options.

- Vestas Wind is a bit of a market leader in, as the name suggests, wind power. In this article, I will introduce you to the company.

- I will start out my coverage on Seeking Alpha with a "HOLD" on this particular company - and here are the reasons for that.

Dear readers/followers,

Ask anyone who knows what Vestas Wind Systems A/S is ( OTCPK:VWDRY ) and they'll likely have some strong opinions about whether you should be investing in the business or not. I am no different. I think Vestas Wind is a superb overall business, but I'm unsure of the near-term future, which makes me unsure of how far the company will fall prior to recovering its momentum. The company also doesn't have the best current fundamentals or track record, further impairing the conservative upside that I see for it.

However, should this company recover and see the profit trends management considers to be likely, your upside could be massive. Let me show you the two ways of viewing Vestas Wind Systems.

Vestas Wind Systems - Reviewing the company

Vestas is older than you think. The company was actually founded back in 1945, and currently operates facilities and manufacturing across the globe, with operations in most continents. It's the largest Wind Turbine company in the world, and a few years ago, it reached a milestone of installing almost 70,000 turbines in total for a capacity of over 100 GW in over 80 countries.

The company's roots go back all the way to 1898 - though at the time it had nothing to do with wind turbines, instead focusing on manufacturing appliances, agricultural equipment, intercoolers, and cranes. It did not enter the wind turbine industry until 1979, and in the beginning, it was a small part of its operation.

In 2003, it merged with NEG Micon, which already at the time resulted in the largest wind power manufacturer in the world. The company has been more volatile than you might expect for a market leader though, and went through multiple periods of losses and recoveries.

Some basic facts to begin with here.

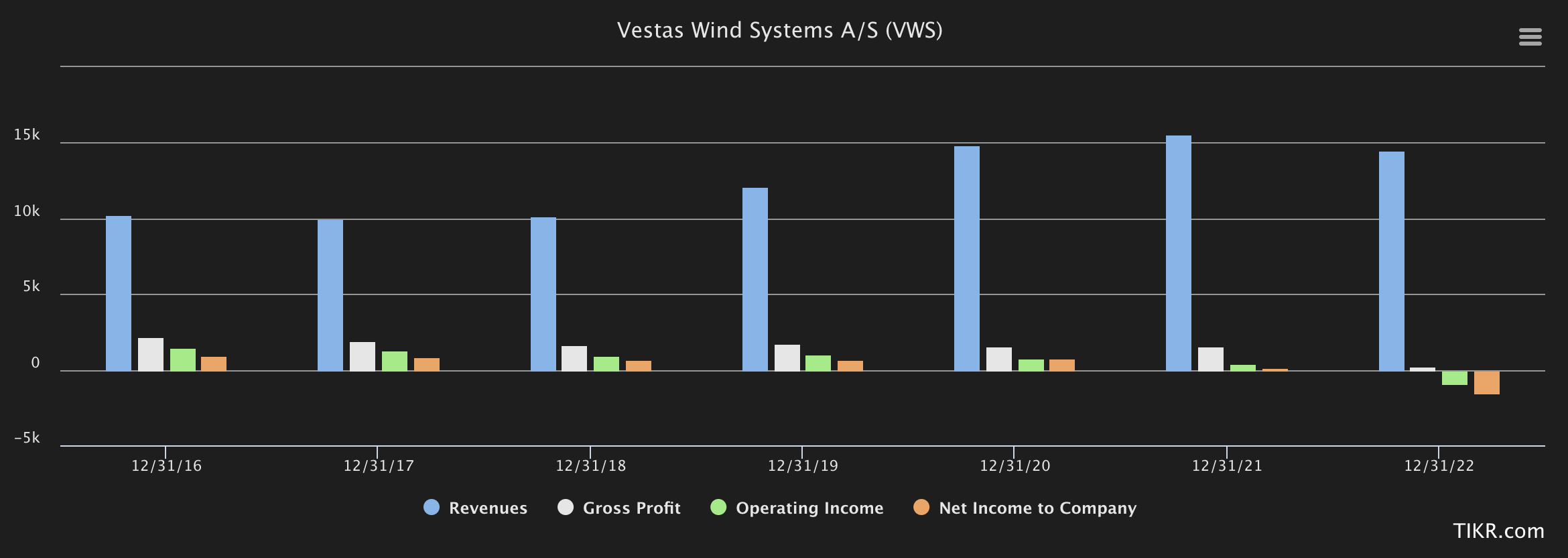

Vestas typically operates a business that generates between €10-€15B worth of revenues which typically comes through COGS to a Gross margin of around 10-18%, through OpEx to an OM of around 8-13% and settles at a net income margin between 5-7%. This is not what has happened in 2021 and 2022 though, which saw the company go through severe declines in profits, if not margins. However, you know what I think about revenues without solid margins - and that's pretty much exactly what Vestas currently has.

{kind=link}

Vestas Margins (TIKR.com/S&P Global)

So why this development? In a word, macroeconomics. Or the pressure, rather from macro. The Ukraine/Russian war has not been kind to the company, and cost inflation and SCM have driven this company's costs up, while driving profits into the ground, rather than as an ESG-driven environment might be expected to, see profits grow.

As of the latest year of 2022, it has resulted in gross margins of 1.92%, with every other profit margin negative. This makes the company one of the least profitable businesses in the entire industrial space, which is not kind. It also means that warning signs are flashing across the spectrum, with OI at a loss, assets growing faster than revenues, a low safety score, and new issuances of debt. It also has a poor record of stock buybacks, and rev/share in decline, and despite this, the price for the stock is relatively high.

Are you starting to see why I am not as positive about the company as some other contributors on Seeking Alpha have been, and why I am not "Pounding the table" on the company here?

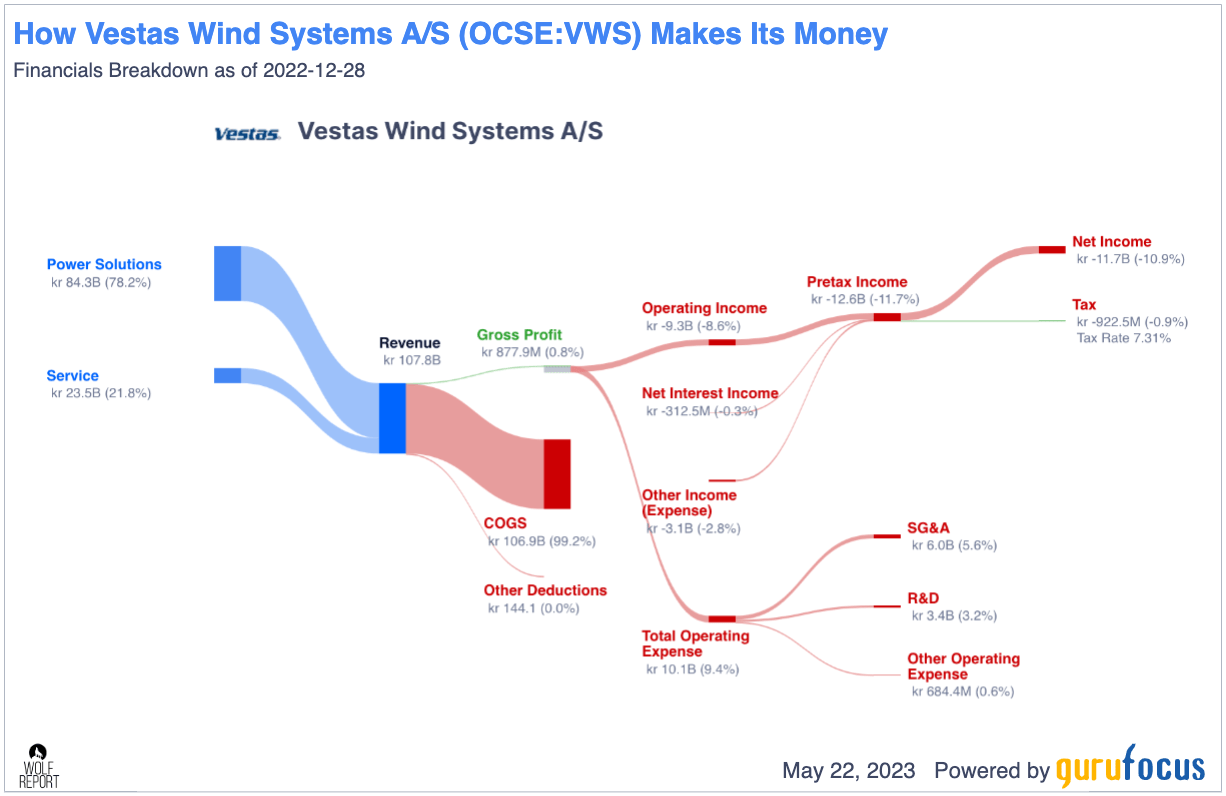

Vestas makes its money from two segments.

- It builds generators

- It services its products.

Pretty simple, right? These come in the form of the Power solutions and the service sector - unfortunately, this is all currently almost in the negative.

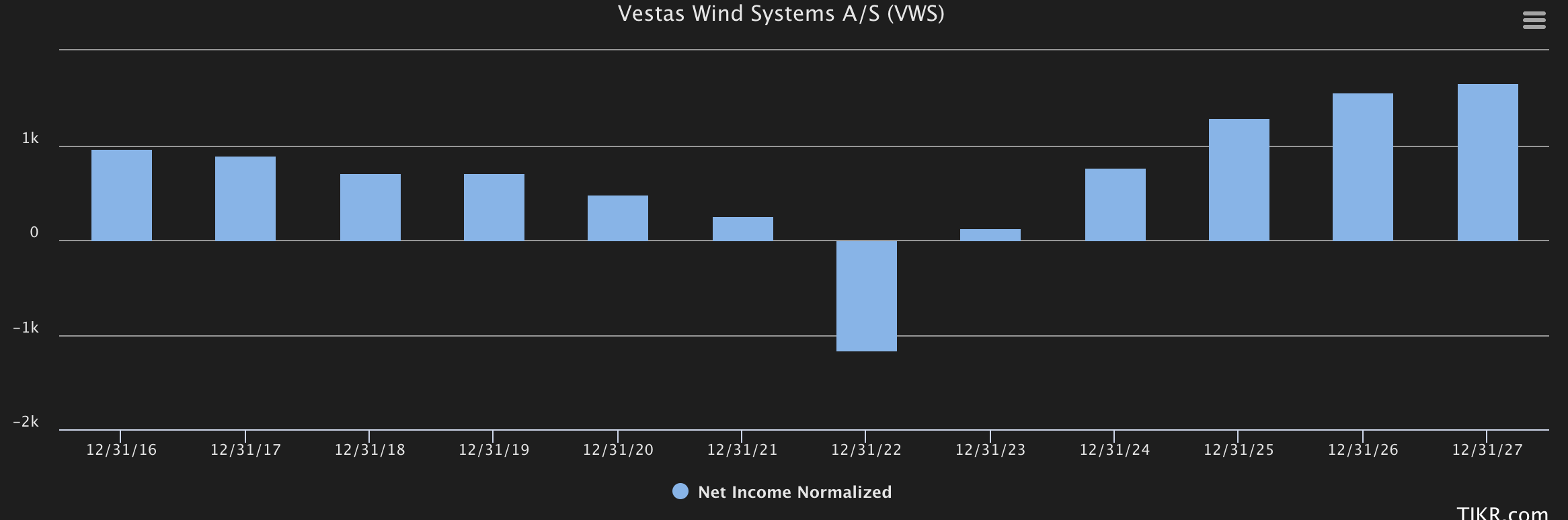

{kind=link}

Vestas revenue/net (GuruFocus)

Not exactly a flattering picture, no matter how "good" the company might be outside of these trends. That's not something you want to see, because what it shows you is a company basically completely unable to make a profit from a 100B DKK revenue. ROIC net of WACC went positive at the highest level back in 2016. Since then it has been on a steady decline. It went negative in -19 and has stayed negative since. The latest number for 2022 comes to a negative ROIC net of WACC of -18%, which is, not mincing words, an abysmal result for a company like this.

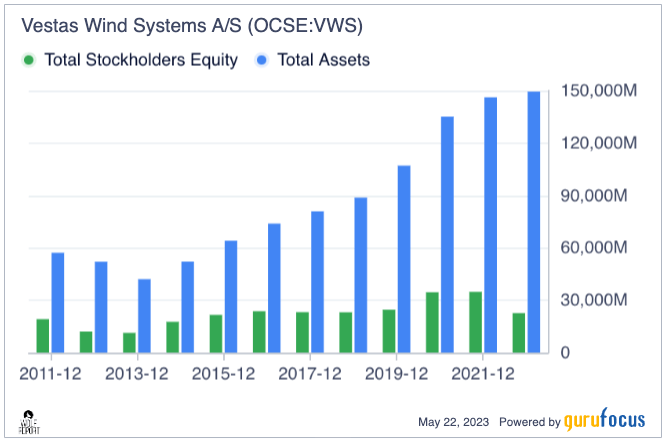

This has in turn taken deep bites out of shareholder equity, where the portion of stockholders' equity is now at the lowest level for many many years, looking at the total % of company assets.

{kind=link}

Vestas SE (GuruFocus)

All of these things are essentially small worrying "blips" on the radar. Same thing with the complete lack of insider activity. Taken at face value on their own, their indicative value is low. Taken together and looked at over time, I see a company in serious decline. My question becomes "When and how does it turn around?"

Because I believe it can - or I would not be writing this article.

Vestas needs to exit Russia. It has operations there. It also needs to fight inflation, and those pressures are becoming increasingly pervasive. Permitting is also harder in this environment, which means that overall, it's not a good set of conditions for any type of project completion. This is, of course, a significant problem for a business like this one.

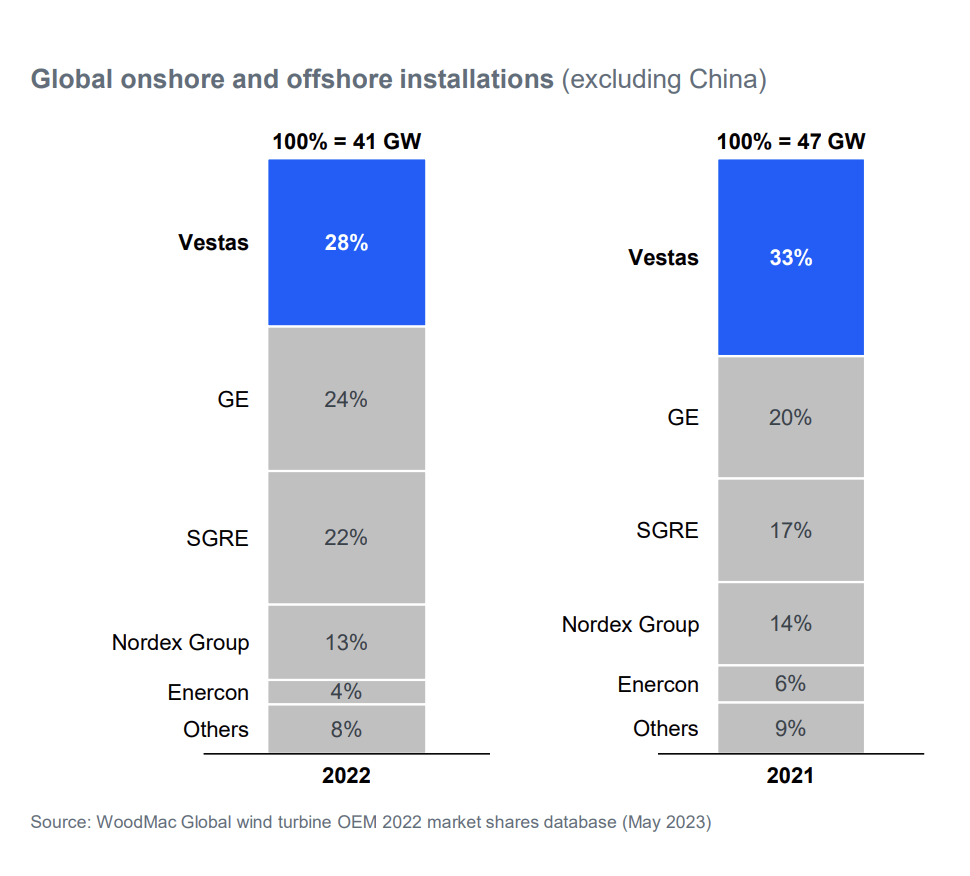

Still, Vestas is still the market leader - even if their market share is actually shrinking at a rather worrying pace when looking at total installations for 2022.

{kind=link}

Vestas IR (Vestas IR)

The service segment is seeing perhaps the lowest amount of pressure, with a well-filled backlog of over €31B, and 147 GW under currently active contracts. Out of those, 136 are onshore, which makes for easier servicing, with an average contract duration of 11 years. However, as long as the company doesn't make money on these things, their contracts and backlogs do not really matter. A business is only a solid business if it manages to squeeze enough net profit from its revenues to not only pay its people but also its shareholders/investors - otherwise, what's the point? There is no value added.

Thankfully, 1Q23 is seeing significant activity in major energy markets across the world. The company has seen an order intake of 50 MW during the quarter, with a total project pipeline of 32 GW. There's nothing wrong with the number of orders the company has. The problem is the details of the contracts, their adjustability for margins, and their issues with legacy projects like many companies currently have, are not widely known.

The positives for the 1Q23 period include a revenue increase of 14% YoY. The company is finally increasing prices, and these price increases are finally finding their way from the top line and downward. This has resulted in GM improvements, but this 755% improvement is from a level of essentially zero, so it really doesn't count. The company went EBIT-positive again, but it really should never have gone negative in the first place - so again, doesn't really count. Net profit is positive, but the point is that it's positive at €16M at a revenue of €2.8B. That corresponds to a quarterly net profit margin of 0.56%, which is still abysmal, and leaves Vestas with a lot to do.

Profitability improvements only make the company more attractive if we can see it returning to a level that makes sense to invest in.

Let's look at current valuations and forecasts.

Vestas Valuation - so-so, I'll stick with my options

I didn't go through much of the minutia of the company here, because frankly, you do not need details here. All you need to know is that the company really, from a fundamental financial perspective, isn't that investable as I see it. Far too often we bog down in minutia as to what the company is expected to do or get caught up in some romantic version of what the company does.

So for the time being, Vestas is a profitability-challenged wind turbine manufacturer and service business. As for analysts, this is what they expect the company to do coming out of 2023.

{kind=link}

TIKR.com Vestas (TIKR.com)

I'm not too keen on this forecast. I consider it much too exuberant, given the massive recovery in 2024E. Either this comes from the company working through non-negotiable legacy contracts which in turn will revert margins, or it's combined with a volume increase based on new orders. I believe it presents a far too oversimplified picture of the post-Ukraine energy sector.

This picture simply does not make sense to me - and it's really hard to convince me that a company with this sort of EPS trend is worth that sort of, or any sort of premium.

{kind=link}

Vestas valuation ( F.A.S.T. Graphs )

I do believe in normalization for Vestas - but I believe the normalization will come far slower, impeding growth in the company. Vestas has been on a mostly negative trajectory since peaking in froth at over 300 DKK, resulting in a negative RoR of 33.35% since 2021. I do not believe the company is done falling.

That is why I have been "bottom fishing". I find the lowest possible workable cash-secured put options, and I sell them at good prices to generate Alpha. Some of my earliest Puts were Vestas at strikes of 150-165 DKK/share, where I would have been fairly content buying the company as a longer-term bet.

Current analyst targets?

As frothy as ever - 22 analysts follow the company. Out of those 22, we have an average PT of 285 DKK from a range of 188 DKK to 455 DKK. The spread here is absolutely insane. Out of those 22, only 7 are at "BUY" despite what is essentially a double-digit upside for the company. The rest of the analysts are very split. Most are at "HOLD", but a fair amount of 6 are either at "SELL" or underperform.

This should add some color to the otherwise mostly bullish picture that's being presented here. I'm bullish at the right price - but I don't see that 188 DKK native target as being conservative enough to give me a good upside when the company is at negative EBIT and net, and I don't see a clear, near-term catalyst for a significant improvement. Note significant. I do believe it will climb, but the upside and bullish thesis is predicated on a significant bounce back. That is not something I currently see - though you're free to argue for it, of course.

I believe the current macro presents a problematic view for a company like Vestas. At best, I believe we'll see recovery slowly or at a slightly increased pace, with positive net earnings trending upward after 2023.

Given the market today, that is not nearly enough to make me positive on the stock.

I begin with a 165 DKK share price target, and call this stock a "HOLD" here.

Here is my current thesis on Vestas.

Thesis

- Vestas Wind is a well-loved Wind Turbine company that has captured the hearts and minds of many ESG investors. I like the company - but only if it can go back to the profitability that we saw years ago. I do not see this easily in the company's near-term future.

- I believe a combination of pricing pressures and at least momentary trend shifts in the energy markets will see Vestas continue to be under pressure from non-trivial inflation and operating pressure, specifically margins. This will prevent the company from rising back up quickly, rather than turning this into a slower process for the time being.

- For that reason, I am now at a "HOLD", and I give the company a 165 DKK price target. That is also, not coincidentally, where I put my CSPs that I use to expose to Vestas.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Not cheap, does not have a high upside on a realistic basis, and the dividend is a bit iffy at this time. I'm not sold on Vestas at this time, and go "HOLD".

For further details see:

Vestas Wind Systems: One Of My Favorite Options, A 'Hold'