GE - VGI Partners 2023 Semi-Annual Investor Letter

2023-08-09 11:30:00 ET

Summary

- VGI Partners Global Investments Limited is an Australia-based investment company. The Company’s Investment Strategy is to create a concentrated Portfolio, predominantly comprised of Long and Short Positions in global listed securities, actively managed with a focus on capital preservation.

- VGI Partners Global Investments Limited generated a net return of 19.7% in the first half of 2023.

- The portfolio has evolved over the past year, with new positions contributing positively to returns.

- The investment philosophy and approach of the strategy remain unchanged, seeking to provide access to under-appreciated, high-quality businesses.

"I am personally skeptical of some of the hype that has gone into artificial intelligence. I think old-fashioned intelligence works pretty well."

- CHARLIE MUNGER, 2023 BERKSHIRE HATHAWAY MEETING, MAY 2023

Dear Fellow Investors,

For the six months ended 30 June 2023 (1HCY23), VGI Partners Global Investments Limited (ASX:VG1) generated a net return of 19.7% [1] at an average net exposure of 72%.

Global equity indices have rebounded since the beginning of 2023, with the MSCI World Index rising +14% to 30 June 2023, the S&P 500 rising +16% over the period and the technology-focused NASDAQ Composite increasing +32%. The period was defined by the narrow leadership from the technology sector, with the top 7 contributors of the S&P500 driving just over 50% of the index return YTD to June. Whilst equity market indices are approaching valuation levels in aggregate that are beginning to appear stretched, this has largely been driven by such excessive outperformance from larger-cap technology companies and we are continuing to find a number of situations across a variety of sectors and markets where there remain attractive opportunities in which to deploy our capital.

As regular readers of our updates would be aware, the portfolio has seen some evolution over the previous 12 months, and we are pleased that a number of new positions have contributed positively to returns over the period. Additionally, some existing holdings have been reduced as share prices approach our assessment of fair value, while the short portfolio has also undertaken some repositioning. We discuss a number of these portfolio movements later in this letter.

Importantly, the investment philosophy and approach of the strategy remains unchanged: VG1 seeks to provide investors with access to a concentrated portfolio of under-appreciated, high-quality businesses, with the ambition to grow our capital at 10-15% per annum over the longer term. We look to achieve this through utilising VGI's deeply fundamental investment approach and a longer-term investment horizon as we seek to uncover opportunities where high-quality businesses have been fundamentally mispriced, or misunderstood, providing us with the ability to generate favorable risk-adjusted returns on our capital.

Performance Summary

We have been pleased with the performance of the portfolio in 1HCY23 and feel it continues to remain well positioned for future positive risk-adjusted returns. The market has provided us with an important lesson in the value of patience, with a number of key positive contributors through the first half coming from positions that had been performance detractors through CY2022.

While underperformance through the short term was undoubtedly painful for investors and managers alike, we undertook a process of reunderwriting our investment theses on a number of these positions through late 2022 in response to weaker share price moves and have been pleased that investors have been able to benefit from the recovery in share prices in the positions in which we retained our conviction (and, in some cases, where we used weaker share prices moves to add exposure as valuations became more attractive).

The largest contributors to performance through the period have included ecommerce tech behemoth Amazon, audio streaming subscription service Spotify and experience management company Qualtrics. Most recently, we have seen an additional number of positions rally back closer to fair value, and we have taken the opportunity to trim some positions and/or exited others.

While we had some successes with single-stock shorts, the greatest detractors to VG1's returns have been more thematic-based basket shorts within the semiconductors and homebuilding space. Having seen our thesis be disproved, we have now covered these positions.

Our proprietary screens, which focus on identifying accounting red flags, have also displayed greater efficacy over the year, identifying a number of situations where weak cash conversion or evidence of poor capital allocation have provided opportunities on the short side. With markets back at higher levels we continue to see this proprietary tool as a key to unearthing short opportunities.

Finally, in terms of FX, VG1 remains fully hedged to Australia Dollars (AUD). As we take an active view on the currency, we may move back to an unhedged or partially hedged position, but only when we believe there is a clear mispricing based on our fundamental analysis. Currently, we remain positive on the AUD because of the favourable position Australia finds itself in: endowed with plenty of commodities at a time when demand for these is growing rapidly given the global undersupply and underinvestment in commodity production experienced in recent years.

Market Observations

As stated in our recent webinar update, we want to remind investors that our process seeks to observe rather than predict - the economic environment and we do not make investments decisions based on the ability to predict the future state of macroeconomic variables. That doesn't mean, however, that we are not aware of the range of likely future scenarios; we construct the portfolio and size our positions to seek to protect capital in a range of economic outcomes. Quality companies, where we focus the bulk of our research efforts, are characteristically able to thrive in most economic environments, however we are often queried on our current thoughts on broader markets and have thus summarised our current reading of the economic environment below.

Importantly, these observations largely come as a by-product of the deep fundamental research approach undertaken at VGI, with the team typically listening and participating in over 250 earnings calls per annum, which provide a wide range of insights on industry sectors and the broader economic climate. Since the beginning of 2023, much of the investment community's energy has been focused on trying to predict the timing and severity of a US recession and, while we have no crystal ball in this regard, it may be helpful to share some of the recent insights we have gleaned from earnings reports in this context.

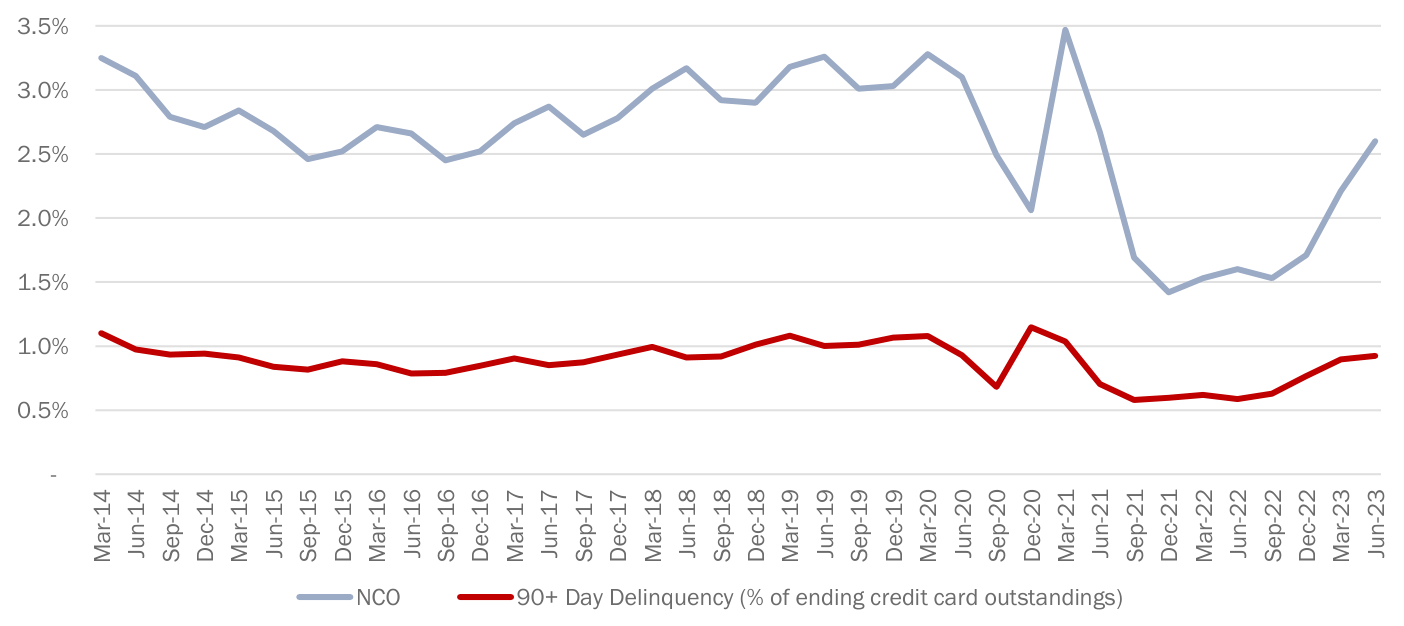

Major bank earnings reports and consumer credit metrics obtained within them are helpful to contextualise where consumer health is relative to expectations. It is clear that credit quality is normalising in the US, with credit card Net Charge Offs (NCOs) at both Bank of America and JP Morgan increasing, but still sitting well below a mid-cycle credit environment:

Bank of America Credit Card NCOs and 90+ Day Delinquency - Quarterly

{kind=link}

Coupled with a still high (but slowly declining) deposit base per account holder, it is clear that consumer health has yet to suffer greatly. Comments from the major bank CFOs and CEOs have confirmed this:

"So it gets back to this idea that the consumer is still in a pretty healthy place. You can see that in the unemployment statistics and you can see it in the way that they're just continuing to spend a little bit more money year-over-year. So I feel like we've been pretty consistent. The consumer's pretty resilient. That remains the case." - Alistair Borthwick, CFO - Bank of America Corporation, July 2023

"The consumer's in good shape - spending down their excess cash. That's all tailwinds. Even if we go into a recession they're going in with rather good conditions, low borrowings and good house price value still." - Jamie Dimon, CEO - JP Morgan Chase, July 2023

Supply chain bottlenecks and labour availability have noticeably improved over the last 6 months. General Mills (manufacturer of grocery items such as cereal, snacks and cooking ingredients) noted in their June conference call that "on-shelf availability is back above 90%", which is around pre-Covid levels, echoing comments from Walmart one month earlier who noted that they were, "much more confident in the supply chain now vs 6 months ago". The CEO of Lockheed Martin (a manufacturer of defence systems in the US) also noted in July that, "over the past six months, our labour availability has improved significantly".

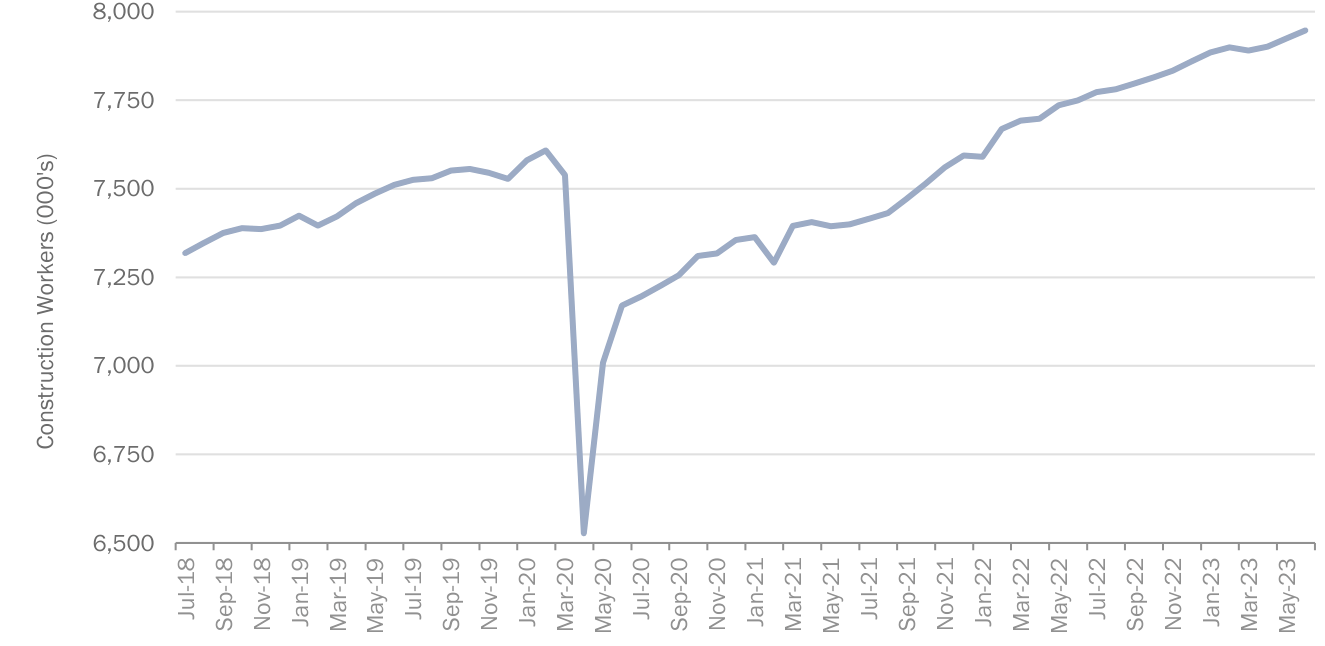

Many consider employment a leading indicator of recessions, with particular focus on the construction sector, however the US labour market appears incredibly strong. Whilst commentators have expected to see a flattening or even decline in construction industry employment in 2023, the sector has added 88k jobs since the beginning of the year and the quarterly total unemployment rate sits at lows of 3.5% - a level not seen since the late 1960s.

US Non-Farm Payrolls - Construction Industry Employment

{kind=link}

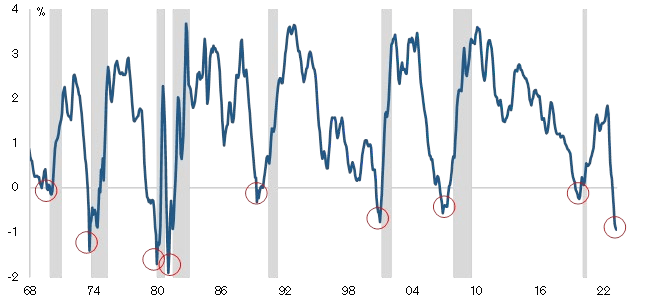

But it is always fine until it isn't. Yield curve inversion 2 has been a strong predictor of future recessions in the past, although the lag from the date of first inversion to recession has varied.

Yield Curve (3 month - 10 Year)

{kind=link}

The US yield curve first inverted in this cycle in October of 2022. Now 9 months on from this we are certainly in the 5 to 17-month window during which historical precedent predicts a recession would begin.

Yield Curve (3 month - 10 Year): Historical Behaviour Around Recessions (months)

With the impending resumption of student loan payments in the US (due to Covid-19 payment relief ceasing) we see a number of businesses with exposure to socio-economic cohorts that may struggle in the coming 12 months. However, relative to expectations at the beginning of 2023, the US economy has held up much better than expected, with robust consumer spending and employment. We have been thoughtful in regards to our US economic exposure and have had a number of short positions in place to offset our exposures on the long side.

Whilst our short positions in US housing, consumer discretionary and technology have ultimately been a drag this year, they did position us for a different set of circumstances and provided protection on the downside. With markets again buoyant we are starting to see opportunities on the short side become increasingly attractive.

Portfolio Thoughts & Positioning

As a reminder, VGI Partners seeks to build a concentrated portfolio for VG1 of under-appreciated, highquality businesses that operate within (or we believe will soon operate within) attractive industry structures. These positions are offset by short positions in companies perceived to be encountering structural or cyclical headwinds, business model weakness and/or accounting irregularities.

The table below provides a snapshot of the top 10 long holdings in VG1's portfolio as at 30 June 2023, and represents a collection of what we believe to be high-quality, attractively-priced, global businesses with significant potential to meaningfully grow their earnings over many years ahead. Consistent with our concentrated approach, the top 10 long positions account for 70% of our total invested capital.

| Top 10 Long Investments as at 30 June 2023 | % of Portfolio |

|---|---|

| CME Group Inc. ( CME ) | |

| 9% | |

| Amazon ( AMZN ) | |

| 9% | |

| GE Healthcare ( GEHC ) | |

| 9% | |

| Deutsche Börse AG | |

| 8% | |

| London Stock Exchange Group ( LDNXF ) | |

| 7% | |

| Rheinmetall AG ( RNMBF ) | |

| 7% | |

| Schlumberger ( SLB ) | |

| 6% | |

| Pinterest ( PINS ) | |

| 5% | |

| The Walt Disney Co. ( DIS ) | |

| 5% | |

| DSM-Firmenich ( KDSKF ) | |

| 5% | |

| Source: VGI Partners analysis. | |

The team retains a high level of conviction in our core portfolio holdings. Over the last six months we have made some changes to long-held investments as we have seen more attractive risk-adjusted opportunities arise . As at 30 June 2023, we see in the long portfolio, conservatively, about 25% potential upside to our estimate of fair value for the underlying stocks.

Regular readers of our monthly reports will recognise a number of our existing longer-term positions in the above, in addition to more recent changes to the overall portfolio composition. As a consequence of updated information and adjustments to our assessment of risk-reward, previously larger positions in multinational payments business Mastercard, German ERP software provider SAP and Swiss headquartered luxury watch and jewellery retailer Cie Financière Richemont have been exited, while VG1 has reduced slightly positions in Amazon and CME Group. New positions that have been added over the last six months include GE Healthcare, which we discuss later in this letter, London Stock Exchange Group, Rheinmetall and Disney.

Below we provide a brief update on some of our key holdings.

CME (~9% weighting as at 30 June 2023)

CME operates futures and derivatives exchanges, including the Chicago Mercantile Exchange, the New York Mercantile Exchange, the Chicago Board of Trade, and the Dow Jones Index Services. On top of this, CME also owns other key assets related to foreign exchange trading & infrastructure and a strategic shareholding in Standard & Poor's (S&P) Index business.

The key driver of trading activity for CME is in its interest rate derivatives products, where it has an effective monopoly in the exchange trading of interest rate derivatives in the United States, through its benchmark products across the entirety of the interest rate curve. Demand for interest rate derivatives is driven by volatility in interest rate markets, whose effect is compounded by the number of bonds held by those looking to manage interest rate risk and, by extension, market liquidity.

The below chart of average daily volumes of interest rate derivatives and US Federal debt held by the public illustrates the extremely strong relationship between the size of the US Treasury market and volumes growth, although there are deviations around this primarily around Fed intervention (for example, at the start of the pandemic, volumes were suppressed by an enormous amount of Quantitative Easing (QE) and effectively zero interest rates which reduced the demand for hedging products). We expect the growth in the size of the US Treasury market, particularly in relation to privately held US treasuries as the Fed undergoes a balance sheet unwind, to remain a powerful underpinning of CME's interest rate derivatives business.

Size of the US Federal Debt Held by the Public vs Average Daily Volume of CME Interest Rate Contracts

{kind=link}

CME's 1H23 results have been pleasing, with revenue growth of over 8% translating to EPS growth of 22%. CME has benefited from increased transaction and clearing fees because of pricing (Revenue Per Contract) and mix shifting towards higher revenue contracts. Similar to other exchange assets, CME has seen a significant increase in net interest income (NII), a result of underlying collateral balances earning a higher rate of interest as rates have increased sharply over the last 18 months.

Current conditions are highly favourable for CME's interest rate derivatives business, other derivatives complexes and net interest margin and we see substantial upside risk to consensus earnings and free cashflow estimates. We believe that CME's assets are critical pieces of market infrastructure and will be recognised as such in the future.

Amazon (~9% weighting as at 30 June 2023)

We continue to see upside to Amazon's two core businesses - Amazon Web Services (AWS) and retail/ecommerce. Whilst Microsoft and ChatGPT have captured the imagination of investors looking for AI exposure, the AI business at AWS is extremely well positioned to increase sales through its combination of software infrastructure products, proprietary training and inference chips (an alternative to NVIDIA). AWS is also developing large language models which are only beginning to be appreciated by the investment community.

In addition, we see significant room for Amazon's retail business to surprise to the upside through margin expansion. After a period of massive capacity expansion and transport infrastructure investment, Amazon has rationalised its North American retail footprint and we believe it will reap the margin benefit of this over the coming years.

GE Healthcare (~9% weighting as at 30 June 2023)

GE Healthcare ( GEHC ) is a global medical technology leader in the Imaging, Ultrasound and Patient Monitoring space. Having initiated a position shortly after it was spun out of parent company GE in late 2022, the stock has become one of our core holdings. We will discuss the investment thesis and upside potential in greater detail later in this letter.

Deutsche Börse AG (~8% weighting as at 30 June 2023)

Deutsche Börse (DB1) is a well-diversified exchange group whose activities touch on most aspects of European capital markets, offering a blend of transactional and non-transactional revenue exposure. It provides trading, clearing, pre/post-trading and data & analytic services in four key operating segments: Trading & Clearing, Fund Services, Security Services and Data & Analytics.

We consider that DB1 is an underappreciated portfolio of dominant businesses, with management deploying the benefits of current cyclical strength into long term structural growth opportunities. Since 2021, net interest income ( NII ) has been the key cyclical tailwind for this business, generating high drop- through earnings from collateral balances - the market ascribes a low multiple to these earnings due to their sensitivity to interest rates movements. However, using the cash generated from this and other cyclical tailwinds over the past several years, DB1 has committed to driving structural growth. This strategy has recently manifested itself through the acquisition of SimCorp - a Danish listed company providing mission-critical software solutions to asset managers with over 60% recurring revenues.

DB1's 1H23 results have shown ongoing progress towards its recognition as a diversified financial technology provider, with revenue growth of 18% translating to EPS growth of 20%. Highlights included 16% revenue growth in fund services, 7% growth in data and analytics and the earlier mentioned growth in NII. We believe that over time the quality of the existing businesses, synergy realisation and ultimately greater earnings stability will be better appreciated by the market and reflected in the stock's rating. DB1 trades at a significant discount to the rest of the Exchange sector with the lowest PEG ratio of the major developed market exchanges.

London Stock Exchange Group (~7% weighting as at 30 June 2023)

The London Stock Exchange Group (LSEG) has transformed from a traditional exchange into a Data and Analytics group. Today it only generates 3% of revenue from its legacy cash equities exchange. In doing so, it has transitioned into a business with an attractive recurring revenue profile and an opportunity to cross-sell data and analytics services on the back of its large acquisition of Refinitiv in 2021. Since then, LSEG has invested behind Refinitiv which has led to revenue growth acceleration.

We think LSEG is now at an inflection point not only to continue improving revenue growth, but also to benefit from margin improvement after a heavy investment period that has seen LSEG incur additional spending from the integration of the Refinitiv assets, as well as a large partnership with Microsoft. We expect LSEG to elaborate further on this strategy at its investor day later in 2023 and to introduce new medium-term financial targets.

We find the valuation highly compelling for this quality of asset. LSEG is trading at a discount to nearly all of its Data & Analytics peers, despite a more attractive growth profile over the next three years in our view. In addition, the original Refinitiv vendors have been selling down their large stake which has been steadily reducing the valuation overhang - as this continues, we think this will continue to close the valuation gap with peers.

It is worth highlighting that while three of our top five positions are financial exchanges (CME, DB1 and LSEG), we don't consider LSEG a direct peer, viewing it primarily as a Data & Analytics business, more akin to businesses such as S&P Global (less the credit ratings business), MSCI (with a lower exposure to indices) and Bloomberg. Moreover, as we mentioned earlier, we have slightly reduced our combined positions in CME and DB1. More broadly, we are finding attractive opportunities in the UK market as valuation levels look more compelling than many other global developed markets.

DSM-Firmenich (~5% weighting as at 30 June 2023)

DSM-Firmenich is also a recent addition to the portfolio, having grown from a smaller position earlier in the year. DSM-Firmenich is the combination of publicly traded DSM and the privately held Firmenich. The resulting company makes up one of the four major players in the concentrated Flavours & Fragrances industry and the transaction marks the completion of a major portfolio transformation at DSM over the last few decades. DSM has repositioned itself from a commodity chemicals supplier to a high value-add Flavours & Fragrances solutions provider. We believe the stock has been overlooked by the investment community given the historical business profile but expect material upside to be realised over the coming years as the earnings quality of the merged business, improving margin profile and resulting high ROIC are better appreciated.

Stock in Focus - GE Healthcare

One of our recent new investments is GE HealthCare (GEHC), which was spun out from General Electric ( GE ) in late 2022. Currently it is our third largest position due to a combination of strong performance and growing the weight (we initiated a position when the company was spun off).

GEHC is a leader in Imaging and Ultrasound machines, which includes PET and CT scans, MRI, X-Ray and ultrasounds - these account for nearly three quarters of revenues. GEHC is a global business with revenues well spread between the US, Europe, China and emerging markets. The business model is both predictable and resilient in our view:

- Predictable because 50% of revenues are recurring in nature, coming from servicing the machines, selling spare parts and consumables - giving the business attractive razor & razorblade economics.

- Resilient because Imaging is a mission-critical category for GEHC's customers - it is the most important revenue driving category for hospitals and one that is prioritised irrespective of the economic environment.

We like the Imaging industry because it is effectively a three-player market between GEHC, Siemens Healthineers and Phillips, and the industry has continued to consolidate over the last 10 years. Scale gives the large players the ability to reinvest in R&D and to entrench their position through close relationships with hospitals.

Our GEHC investment thesis is based on an under-appreciated margin opportunity as a newly independent company. We often see this with spin-off situations:

- A hidden asset with a renewed focus on capturing market share;

- A bloated cost structure that can be better optimised; and

- A newly independent and aligned management team.

All of these are in place at GEHC. For a long time, the company has been run within the larger GE conglomerate and milked for its cashflows, with GE's investment priority being its Aerospace business (prior to COVID, we were investors in GE so have followed the company closely for a long time). However now as a newly independent entity, GEHC can focus on its core business with a fully independent and aligned management team that we expect will act with more urgency.

The margin opportunity stands out when comparing GEHC to its closest peer Siemens Healthineers, whose Imaging business generates operating margins in the low 20s percentage compared to GEHC in the mid-teens. Our diligence suggests that there are no structural reasons for this margin differential - therefore we think GEHC will close the margin gap over time by addressing the low-hanging fruit in the cost base while also launching new, higher-margin products (resulting from the recent step up in R&D spend). We believe market expectations for GEHC's margins are too low and therefore see meaningful room to surprise to the upside - leading to high-teens earnings growth over the next few years.

Imaging Operating Margin Differential (GE HealthCare vs Siemens Healthineers)

{kind=link}

Another important tailwind for margins we expect will be the growing penetration of digital tools in Imaging, which GE has been investing behind. GEHC's large global install base of >4m machines gives them a strong advantage in terms of data collection, even more so today when data is extremely valuable and can be overlayed with software applications.

We have already started to see strong demand from hospitals for these software applications because they can meaningfully reduce costs - for example by allowing doctors to read and analyse imaging scans in much shorter time windows, addressing both staffing issues and costs. The adoption of digital services will support growth, better service attach rates and ultimately improve margins - and importantly we do not think we have to underwrite this to get upside to the current valuation.

We view GEHC's valuation as compelling at current levels, particularly with the meaningful improvement in free cashflow ((FCF)) generation we expect over the next 3 years. On current metrics, which we think still only reflect a depressed earnings base, the stock is trading at a discount to most medtech peers despite having a more attractive growth profile. On a more normalised basis, the stock is on a FCF yield of over 6%, which we think is very appealing. Being a newly independent company, there is still some scepticism with regards to management execution but we think the market will start to become more comfortable as the company starts to deliver on its margin opportunity.

As a closing comment, the medtech industry is one we like and one where we have had some successful investments in recent years (Intuitive Surgical and Olympus). We expect to continue looking for opportunities in the sector.

In Closing

We have been pleased with the performance delivered for the 1HCY23, albeit we recognise this performance sits in the context of a weaker period of overall returns in recent years. We appreciate our investors' patience and support through this period. We have been very pleased with the continued benefits accruing from the recent merger of the VGI Partners business with Regal and feel this is becoming increasingly tangible for investors via improved returns. We remain very optimistic around the current shape of the portfolio and opportunities for the strategy and look forward to continuing to keep investors updated with our progress.

We have always viewed the opportunity to manage our investors' capital as a privilege, and we thank investors for their continued support and encouragement.

Yours faithfully,

VGI Partners

Footnotes1 Past performance is not a reliable indicator of future performance. 2 Yield curve inversion refers to a period where long-term interest rates are less than short-term interest rates. DisclaimerThis newsletter is provided by Regal Partners Marketing Services Pty Ltd (ACN 637 448 072) (Regal Partners Marketing), a corporate authorised representative of Attunga Capital Pty Ltd (ABN 96 117 683 093) (AFSL 297385) (Attunga). Regal Partners Marketing and Attunga are businesses of Regal Partners Limited (ABN 33 129 188 450) (together, referred to as Regal Partners). The Regal Partners Marketing Financial Services Guide can be found on the Regal Partners Limited website or is available on request. VGI Partners, is a business of Regal Partners Limited, which is the investment manager of VGI Partners Global Investments Limited (VG1). The information in this document (Information) has been prepared for general information purposes only and without taking into account any recipient's investment objectives, financial situation or particular circumstances (including financial and taxation position). The Information does not (and does not intend to) contain a recommendation or statement of opinion intended to be investment advice or to influence a decision to deal with any financial product nor does it constitute an offer, solicitation or commitment by VG1 or Regal Partners. It is the sole responsibility of the recipient to consider the risks connected with any investment strategy contained in the Information. None of VG1, Regal Partners, their related bodies corporate nor any of their respective directors, employees, officers or agents accept any liability for any loss or damage arising directly or indirectly from the use of all or any part of the Information. Neither VG1 nor Regal Partners represents or warrants that the Information in this document is accurate, complete or up to date and accepts no liability if it is not. Past performance The historical financial information and performance figures given in this document are given for illustrative purposes only and should not be relied upon as (and are not) an indication of VG1 or Regal Partners' views on the future performance of VG1 or other Funds or strategies managed by Regal Partners or its related bodies corporate. You should note that past performance of VG1 or Funds or strategies managed by Regal Partners or its related bodies corporate cannot be relied upon as an indicator of (and provide no guidance as to) future performance. Forward-looking statements This document contains certain "forward-looking statements" that are based on management's beliefs, assumptions and expectations and on information currently available to management. Forward-looking statements can generally be identified by the use of forward-looking words such as, "expect", "anticipate", "likely", "intend", "should", "could", "may", "predict", "plan", "propose", "will", "believe", "forecast", "estimate", "target" "outlook", "guidance" and other similar expressions. Indications of, and guidance or outlook on, future earnings or financial performance are also forward-looking statements. You are cautioned not to place undue reliance on forward-looking statements. Any such statements, opinions and estimates in this document speak only as of the date of this document and are based on assumptions and contingencies and are subject to change without notice, as are statements about market and industry trends, projections, guidance and estimates. Forward-looking statements are provided as a general guide only. The forward-looking statements contained in this document are not indications, guarantees or predictions of future performance and involve known and unknown risks and uncertainties and other factors, many of which are beyond the control of VG1 or Regal Partners, and may involve significant elements of subjective judgement and assumptions as to future events which may or may not be correct. There can be no assurance that actual outcomes will not differ materially from these forward-looking statements. No representation, warranty or assurance (express or implied) is given or made in relation to any forward-looking statement by any person (including VG1, Regal Partners, their related bodies corporate or any of their respective directors, officers, employees, agents or advisers). In particular, no representation, warranty or assurance (express or implied) is given that the occurrence of the events expressed or implied in any forward-looking statements in this document will actually occur. Except as required by law or regulation, VG1 and Regal Partners disclaim any obligation or undertaking to update forward-looking statements in this document to reflect any changes in expectations in relation to any forward-looking statement or change in events, circumstances or conditions on which any statement is based. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

VGI Partners 2023 Semi-Annual Investor Letter