SMAWF - VGK: Downside Risks More Pronounced

Summary

- The EU economy has weathered the economic divorce with Russia better than expected, at least on the surface. It took over 800 billion euros in spending to mask the scale of damage.

- The money was needed to cushion the blow from the need to bid up the price of LNG to the point needed for companies to be willing to break contracts and divert shipments.

- Such a high rate of mitigation spending is unsustainable, while there are no alternative solutions on the table. The EU economy will de-industrialize in line with energy supply realities.

- The Vanguard FTSE Europe ETF has had a decent run in the past few months, largely thanks to the EU economy holding up better than feared.

- The markets seem to be mistaking expensive, unsustainable efforts to mask the economic damage for actual resilience. The ETF's only long-term strong point at this time is the broad global exposure of many companies that make up the fund.

Investment thesis: Defying many fears, the EU economy weathered the energy crisis of the past year and a half rather well, at least on the surface. Thanks to a mild winter, efforts to cut demand, as well as an aggressive program to outbid the world for LNG supplies, the EU did not run out of natural gas. In fact, supplies in storage are higher than average for this time of year. The Vanguard FTSE Europe ETF (VGK) has done better than expected in the past few months, thanks to the seemingly positive, or better-than-expected economic developments. The fact that it took over 800 billion euros in mitigation spending since March of 2022, or about $80 billion per month on average in national and EU-wide initiatives to paper over what is otherwise arguably permanent economic damage in the EU, as a result of its energy crisis, which is still ongoing needs to be factored in. In particular, we have to be conscious of the unsustainable nature of so much extra spending on mitigation efforts. At some point, it will have to stop, making the long-term prospects of Europe-dependent investment assets rather bleak going forward.

The VGK ETF offers broad exposure to European companies. Its weakness within the current global context is its exposure to the EU economy, while its strength is the global reach of many of the companies represented in the fund.

The VGK fund currently has 1349 stocks represented as holdings, with a median market cap of the companies of over $46 billion. It is currently trading at a P/E ratio of over 12. The fund's expense ratio is .11%.

{kind=link}

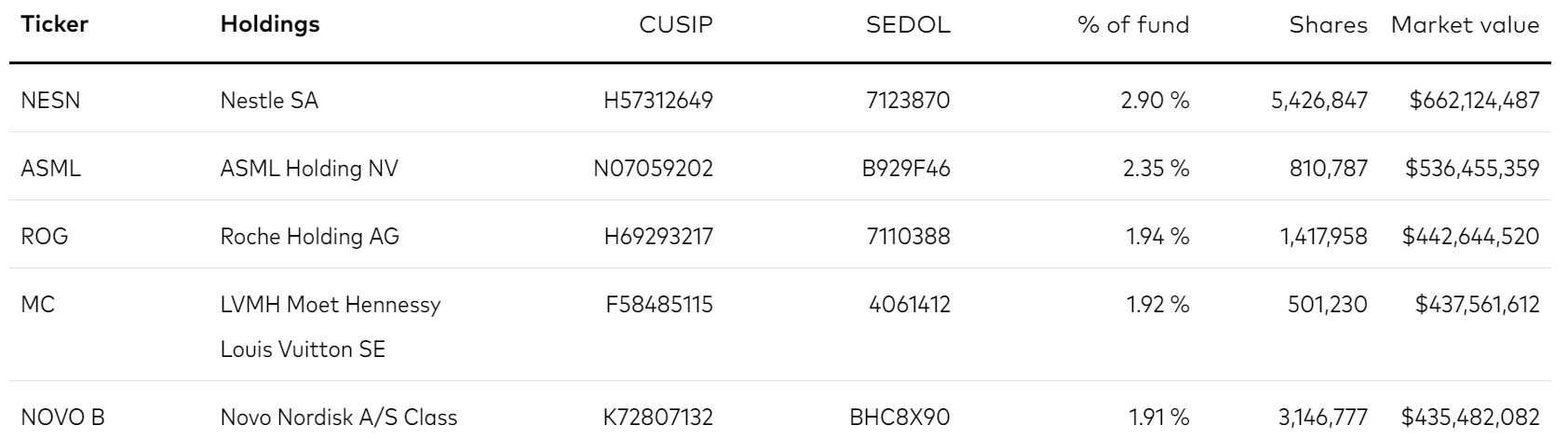

Looking at the top five holdings of this ETF, we see a common denominator, namely companies that do significant business, whether it is sales, operations, or both, outside of Europe. ASML ( ASML ) for instance sells most of its lithography machines to Asian and American customers such as TSMC ( TSM ), Intel ( INTC ), and Samsung ( OTCPK:SSNLF ). Nestle SA ( OTCPK:NSRGY ) has operations and sells its products all over the world. The same goes for many of the companies on the fund's list of top holdings. In many ways, this fund is at least as much dependent on the outlook for the global economy as it is on the European economy.

At the same time, we should not overlook the fund's deep operational as well as sales revenue roots in Europe. In other words, the exposure to the ailing EU economy is still significant enough to consider this mostly a bet on the EU economy. We should also keep in mind that as the geopolitical situation around the world continues to worsen, it is increasingly likely that the EU will be dragged into an economic confrontation with China, by the US. The latest ratcheting up of tensions is by no means encouraging in this regard. Many of the companies represented in this fund, such as Siemens (SIEGY) have extensive business ties with China.

Europe's energy crisis is far from over, with long-term prospects bleak.

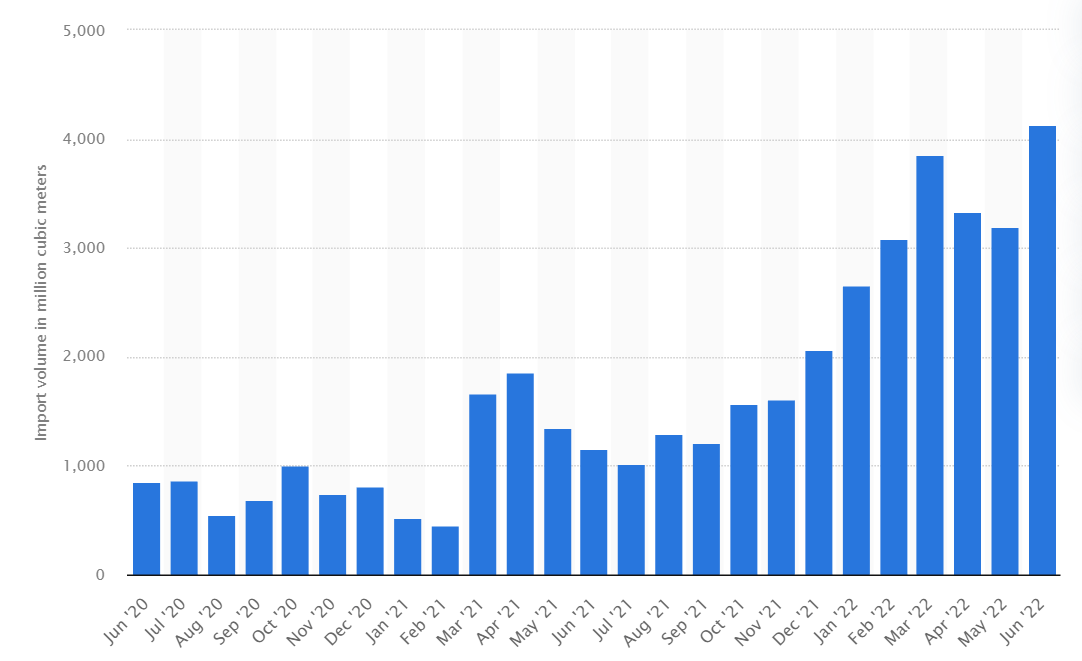

A combination of massive volumes of mostly US LNG, a very mild winter, and some severe cuts in demand helped the EU get through the past year, with very little reliance on Russian natural gas, which in 2021 made up about 40% of the EU's supplies.

EU monthly imports of US LNG (Statista)

{kind=link}

Growing imports of mostly US LNG are by no means enough to cover EU natural gas demand measured at 2021 levels. It has been reported in the past few months that demand is down by about a quarter compared with the previous years. The least economically damaging path to cutting demand has been to ask households to consume less, which they managed to do in large part thanks to milder winter weather this past winter, but also because many EU households were not able to financially keep up with rising utility bills.

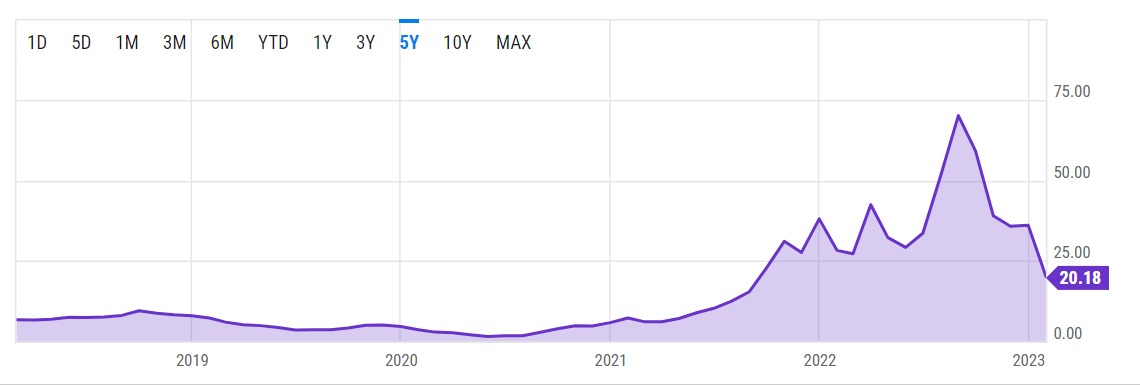

By far the greatest factor that helped the EU get through the past winter has been its willingness to bid up the price of gas as high as it needed to be to outbid other potential buyers of LNG, including those who had long-term contracts, yet they lost out, with LNG suppliers willing to pay the penalty stipulated in the contract for not delivering to the long-term buyer, in favor of diverting deliveries to Europe.

EU natural gas import price per million BTUs. (Y Charts)

{kind=link}

As we can see, while prices also increased in the US, Europeans have been paying significantly higher prices for their natural gas imports, which was the only way to attract sufficient volumes needed to build a comfortable reserve cushion. In order to sustain these exorbitant import costs, the EU injected massive volumes of subsidies, aid, and bailouts into the economy, to the tune of $800 billion , when including the UK & Norway. It is very important to understand the fact that the EU managed to outbid developing nations such as India, Pakistan & Bangladesh for those LNG supplies by using its mature economy advantage, in other words, a high GDP per capita and a high capacity to borrow money on the cheap comparatively speaking.

The EU and the UK will not be able to keep this up forever. Furthermore, the weather might not collaborate going forward, thus they may need to poach even more LNG volumes from others in the coming months and years. Another important factor this year might be the resurgence of China's economic activities after it finally gave up on its zero COVID policy. The February PMI numbers for China are confirming a sharp rebound, meaning that it will require more energy, thus it is unlikely to re-sell much if any LNG to Europe, as it did last year.

It should also be noted that American long-term geopolitical strategic thinking may also get in the way of seeing the continued reallocation of its LNG to Europe for the long term. Just a bit over a decade ago, GDP size by continents , had Europe in the first place, followed by North America and Asia in the third spot. Within this short span of time, Asia moved into first place and Europe into third. Not only that but the Asian economy is nearly double the size of Europe's currently, and it is set to become larger than that of Europe & North America combined by the end of this decade if current trends continue. For the US, having most of its LNG stuck, headed to Europe, instead of the Asian market is an opportunity lost to establish itself as an important player in Asian geopolitics going forward. I expect that within about a year or so, US LNG flows will be increasingly diverted to Asia, leaving Europe literally in the cold.

Investment implications:

On the surface, it may make sense to invest in this fund. With a P/E ratio of just over 12, it is cheaper than US indexes. The S&P currently trades at around 21. EU GDP numbers also came in decent for 2022, despite all the challenges. Europe did spend about the equivalent of 5% of GDP on mitigation efforts, without which things would look much uglier. It is not sustainable to continue doing this for much longer. Every month that an average of about $80 billion is spent across the EU on keeping industries and consumers afloat, is a month closer to the point where the markets or politics will force some governments to abandon this support. It will probably start with some of the financially weaker states, like Italy.

Below the surface, we see an energy supply situation that continues to be untenable as a result of the economic divorce from Russia. The true magnitude of the impact on the EU economy has been temporarily masked by the massive spending that national governments engaged in. Even so, EU steel production is now lower than it was in 2020, as the COVID lockdowns were shutting everything down. The only time in the past 25 years that production was lower than the recent monthly lows we saw was immediately after the financial crisis of 2008. EU Ammonia fertilizer production is down a staggering 70%. Vegetable shortages and price spikes are popping up all over Europe. These are just a few examples of severe problems under the surface, as factors such as reduced greenhouse farm output are starting to bite, while most other industries that are very energy intensive or need natural gas as a feedstock are grinding to a halt.

At some point, Europe's ability to sustain upwards of $100 billion/month on energy crisis mitigating efforts will diminish. It could happen this month, or it could happen a year from now, but it will. At the same time, American resolve to sacrifice its increasingly globally strategic LNG exports in a region that is increasingly irrelevant from a global geostrategic and economic point of view will diminish as well.

The weather will not always play in Europe's favor either. We should keep in mind that Europe's energy crisis actually started in 2021, with a significant shortfall in wind energy putting increased pressure on its natural gas supplies, as it needed to plug the gap left by renewables. Finally, we should not expect European households to agree to a severe reduction in their comfort levels in their homes by being obliged to reduce the temperature in the winter, whether it is because they cannot afford the cost of heating or due to other considerations.

The long-term prospects of the European business sector look increasingly bleak in their home base. There are still many companies on the list within the VGK fund that have significant global exposure, thus it can be argued that they may be able to make up for any shortfalls within their home markets abroad. Even that potential advantage may cease for companies like ASML, and Siemens, as the global supply chains are increasingly disrupted by geopolitics, and the technological edge over rising competitors in the developing world such as Chinese or Indian companies is quickly melting away.

Overall, the long-term upside for this fund is very limited, even though some metrics such as the P/E ratio that is roughly half of the valuation levels we see with US indices, which may suggest that this is a good value investment. The downside risks are arguably more pronounced, with the negative factors I cited in the article far outweighing any hypothetical factors that could provide for a bullish case.

For further details see:

VGK: Downside Risks More Pronounced