VHT - VHT: Current Valuation Not Justified Due To Declining Long-Term Earnings Growth Forecast

2023-11-02 10:15:33 ET

Summary

- VHT offers better downside protection than the broader market but its long-term earnings growth is in a declining trend.

- VHT's valuation is not attractive relative to the S&P 500 index.

- Valuation compression is likely in an upcoming economic recession.

Introduction

We wrote an article on Vanguard Health Care ETF ( VHT ) back in July 2020. At that time, we held the view that VHT is a good long-term holding for investors with a long-term investment horizon that seeks dividend growth (click here ). It has been over 3 years now since that article was written. Therefore, we think it is time to re-visit VHT and provide our insights and recommendations.

ETF Overview

VHT owns a portfolio of large-cap healthcare stocks in the United States. It has an expense ratio of 0.1%, which is cheap compared to other similar health care funds. The fund has better downside protection than the broader market, namely the S&P 500 index. However, its long-term earnings growth outlook has diminished significantly in the past two decades. Its current long-term earnings growth outlook now significantly trailed the S&P 500 index's growth forecast. While VHT's valuation has stayed quite flat since 2014, this valuation is not justified given its declining long-term growth forecast trend. Hence, we think investors with a long-term investment horizon are better off investing in other sectors.

YCharts

Fund Analysis

VHT is now testing the trough reached in June 2022

The past two years were quite challenging for the equity market in general. VHT is not without exception. The S&P 500 index has declined by about 12.5% since reaching the peak in late 2021. Similarly, VHT declined quite a bit as well. It registered a loss of 15.6% in the past year. Unlike the S&P 500 index that had a rollercoaster ride which declined sharply in 2022 and rebounded strongly in H1 2023 before resuming its declined in Q3 2023, VHT was in a slow decline for most of the past 2 years. However, the decline appears to be accelerating lately as VHT's fund price is now testing the trough reached in June 2022.

YCharts

VHT has comparable performance to the S&P 500

VHT has performed quite well in the past. In fact, it has delivered a total return of 483% since its inception in 2004. It has also delivered strong returns in the past 10 years. As can be seen from the chart below, the fund has generated a total return of 168.7% in the past 10 years. In contrast, S&P 500 index has delivered a total return of 183.9%. As the chart below shows, VHT's total return closely tracks the S&P 500 index for the most of the time in the past 10 years. Therefore, its long-term return appears to be comparable to the S&P 500 index, at least from a historical perspective.

YCharts

Portfolio Composition

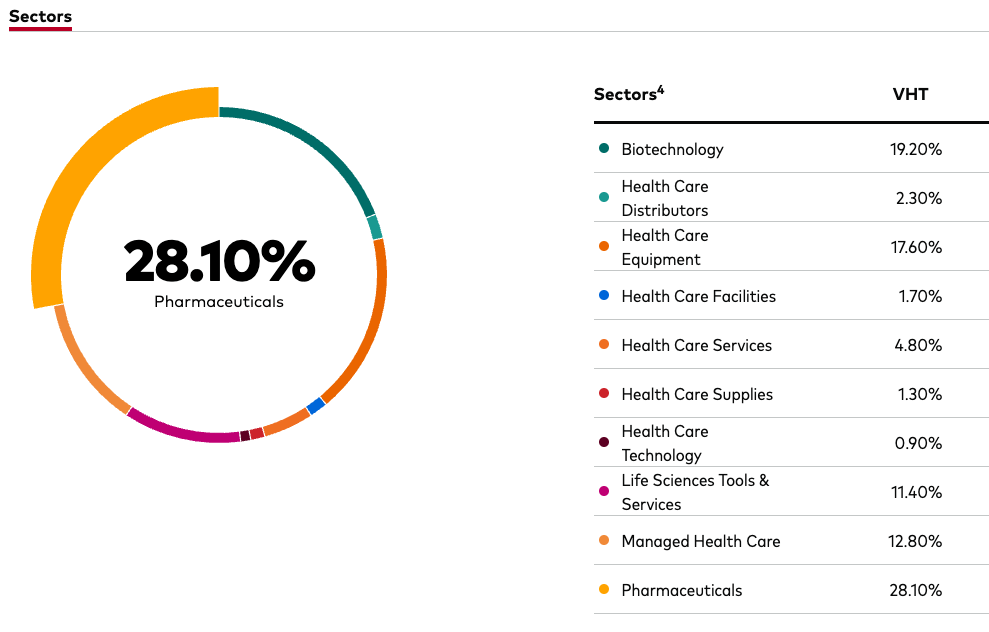

Let us take a look at VHT's portfolio. The largest two subsectors in VHT's portfolio belongs to Pharmaceuticals and biotechnology, which represents about 28.1% and 19.2% of the entire portfolio respectively. According to Straits Research , a research firm which analyzes and project growths of different industries, the global biotechnology & pharmaceutical services market size is projected to grow at a compound annual growth rate of 5.45% from 2022 to 2030. VHT's third largest subsector belongs to health care equipment sector. This sector is also expected to grow at an annual rate of 5.5% between 2022 and 2030 according to Precedence Research , a Canada based firm that offers strategic market insights. These mid-single digit growth rates are not high, but are still quite good compared to other defensive sectors. For example, utilities sector typically have low single digit growth rate. Therefore, VHT should have a long runway of growth.

{kind=link}

But, long-term forecast earnings growth rate appears to be declining

While stocks in VHT's portfolio should benefit from an ageing population and growth in healthcare demand in the future, its earnings growth forecast has been weakening. Here, we will look at the average earnings forecast of stocks in the healthcare sector in the S&P 500 index. Since VHT's portfolio consists of large-cap stocks, we believe we can gain insights by examining the healthcare sector in the S&P 500 index.

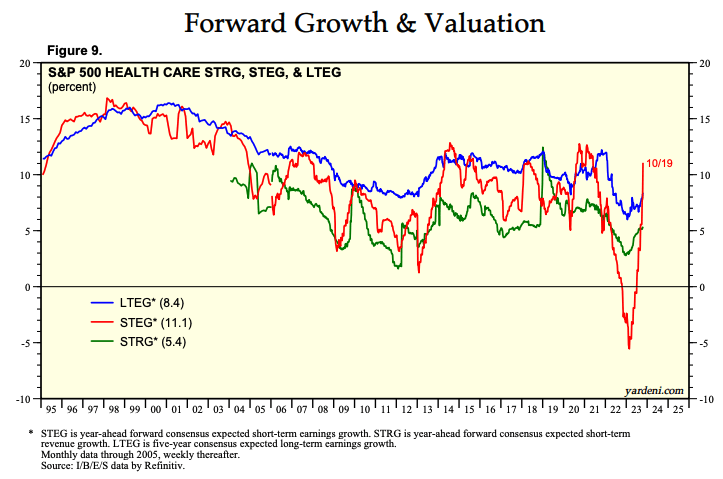

As can be seen from the chart below, long-term earnings growth forecast has been in a declining trend in the past two decades. Specifically, the long-term earnings growth rate has declined from the peak of above 15% in 2000/2001 to only 8.4% today. This is a warning sign. We do not know exactly what caused this decline as it requires detail analysis of the entire industry. We can only guess that it was likely due to government regulations, and funding constraints on public health care industry. For example, the use of generic drugs can result in profit margin decline in many pharmaceutical companies.

{kind=link}

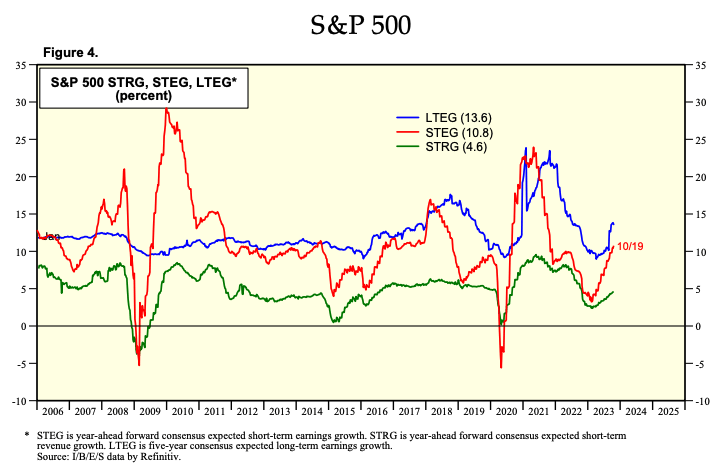

Now, let us compare healthcare sector's earnings growth with S&P 500 index's long-term earnings growth outlook. As can be seen from the chart below, the S&P 500 index's long-term earnings growth rate stayed relatively within the range of 10%~15% since 2006. Its current long-term earnings growth rate of 13.6% is also significantly higher than the healthcare sector's 8.4% mentioned in the previous paragraph. Based on this trend, we think it is very likely that VHT's performance will lag the S&P 500 index in the next 5~10 years.

{kind=link}

Looking forward, we believe healthcare industry will eventually experience margin expansion and better earnings growth rate due to technology advancement. Technology has the potential to transform the health care industry. New technology advancements can significantly reduce the heavy reliance on healthcare workers in health care services. The use of artificial intelligence can also speed up the process of new drug developments, and help quickly analyze medical images. This will likely happen in the years to come. Therefore, we should eventually see higher earnings growth in the health care industry from the current level.

Valuation compression likely in upcoming recession

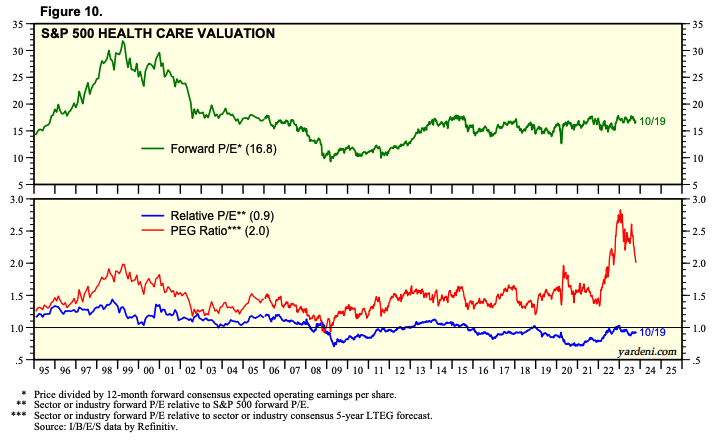

Although we think VHT's margin should eventually improve in the future, its fund price will likely face some pressures in the near-term. Let us now evaluate VHT's valuation. We will again use the S&P 500 healthcare sector as a reference. As can be seen from the chart below, the average forward P/E ratio of healthcare stocks in the S&P 500 index is about 16.8x. Since 2014, the average forward P/E ratio has stayed relative flat and typically between 15x and 17x. Therefore, healthcare sector's valuation appears reasonable. However, the average forward P/E ratio of the S&P 500 index is currently about 18.1x. Given that healthcare sector's long-term earnings growth forecast now significantly trailed the S&P 500 index's growth forecast, it is difficult to justify VHT's high valuation. In addition, we have also noticed that in between 2008 and 2014 (the years during and immediately after the Great Recession), the valuation was much lower in the range of 10x and 13x. Therefore, valuation compression will likely happen in the upcoming economic recession.

{kind=link}

VHT has better downside protection than the broader market, but still significant downside risk

Although VHT may see valuation compression in an economic recession, it offers better downside protection than the broader market. This is not hard to explain as people still need to access healthcare services and products even during economic recessions. Therefore, revenues and earnings of stocks in VHT's portfolio are less impacted in an economic recession than many other stocks. As can be seen from the chart below, VHT's fund price declined by about 40% during the Great Recession in 2008/2009. In contrast, the S&P 500 index declined over 55%. During the outbreak of COVID-19 in 2020, VHT only declined by about 22% whereas the S&P 500 index declined by about 34%.

YCharts

Investor Takeaway

While VHT may provide better downside protection in an economic recession, its long-term earnings growth forecast has been in a declining trend and is inferior than the S&P 500 index. Given that its valuation is also not cheap relative the S&P 500 index, we think the risk and reward profile of owning VHT in the long-term is not attractive. Hence, we think investors with a long-term investment horizon should seek other alternatives.

Additional Disclosure : This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

For further details see:

VHT: Current Valuation Not Justified Due To Declining Long-Term Earnings Growth Forecast