BMYMP - Viatris: It Is Always Cheap Yet It Is Always Declining

2023-11-21 13:48:38 ET

Summary

- VTRS reported Q3-2023 earnings in line with estimates, with total sales down 3.3%.

- Adjusted EBITDA fell again, and new product launches are not delivering the same margins as the old business.

- We look at the progress made since its listing and tell you why the stock always appears cheap but never delivers.

On our last coverage of Viatris Inc. (VTRS) we pointed out that those that sell volatility will be victorious over the buy and hope (we beg your pardon, hold) crowd. We gave this yet another neutral rating. Specifically, we said:

So, this morning's excitement aside, we would maintain our previous long-term view of the business. That view is that this is a melting ice cube. Those bullish should consider using covered calls or cash secured puts to sell volatility on this stock. We think those investors could make some longer-term returns. The buy and hold crowd will not.

Source: That Free Cash Flow Is Not As Attractive As It Sounds

That has been a good call as the stock remains unable to find traction.

Seeking Alpha

We examine the recently released Q3-2023 results and tell you why VTRS gave the bulls a modicum of hope.

Q3-2023

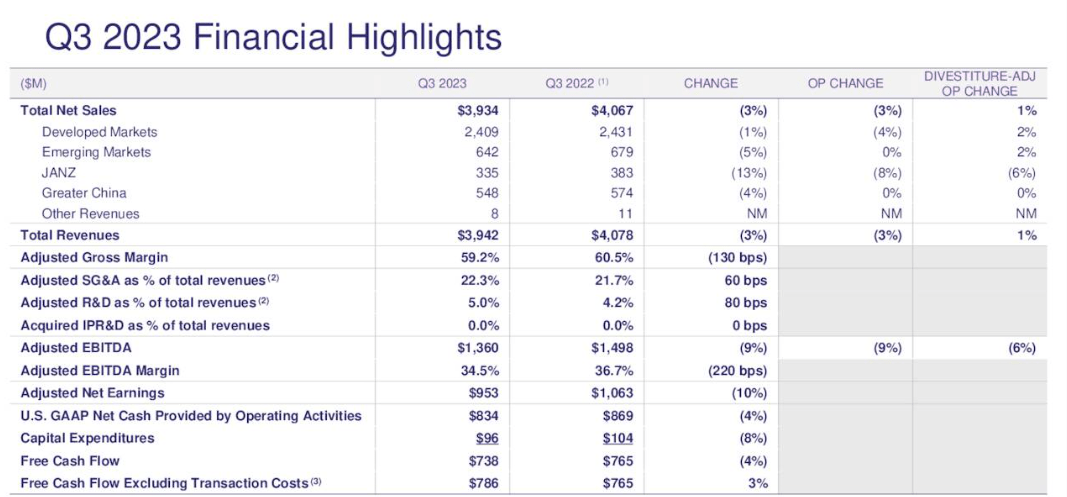

VTRS reported Q3-2023 earnings that were in line with analyst estimates. Total sales were down 3.3% over 2022 but if you excluded the divested business and adjusted for the impact of Forex, VTRS actually had increased sales. Now that may sound like we are bending over backwards to find positive news, but that is how VTRS itself presents it. The "divestiture adjusted operational revenue growth" on the slide below refers to exactly that.

{kind=link}

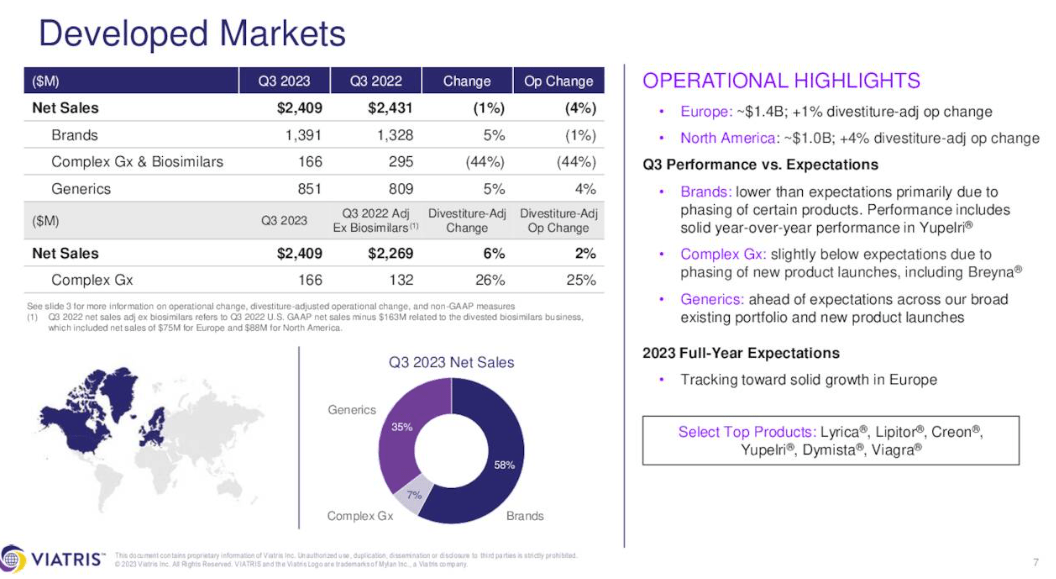

Developed markets were the strongest segment with the adjusted sales actually up 2%.

{kind=link}

Emerging markets and China were weak, with even adjusted sales showing declines. JANZ (Japan, Australia, New Zealand) was the weakest with a 6% adjusted sales decline.

VTRS Q3-2023 Presentation

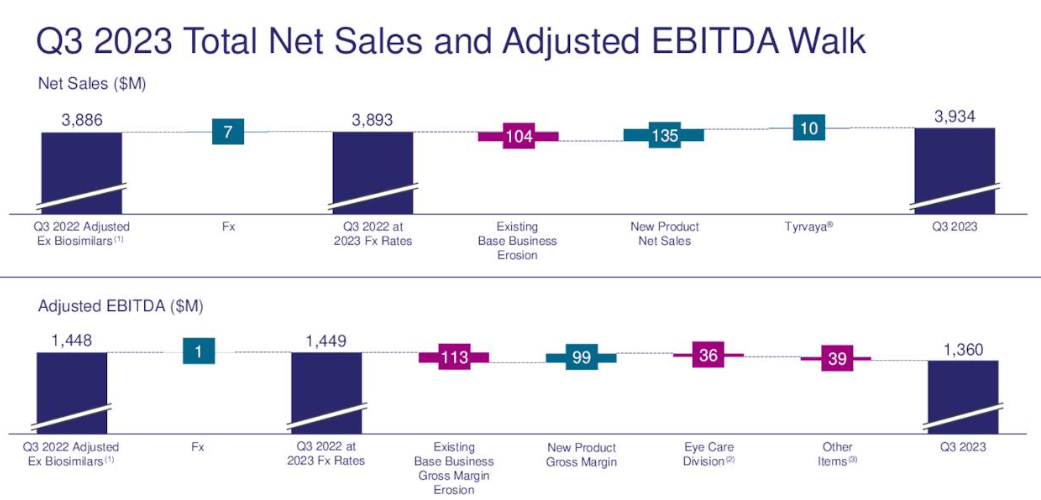

As it usually happens with VTRS, the adjusted EBITDA fell once again.

{kind=link}

The company's new product launches are not delivering the same kind of margins as the old business and you can see the erosion in the slide above (negative $113 million vs positive $99 million). The good part for VTRS was that none of this was unexpected and overall the adjusted gross margin has held up far better than what many bears had probably expected.

{kind=link}

Outlook

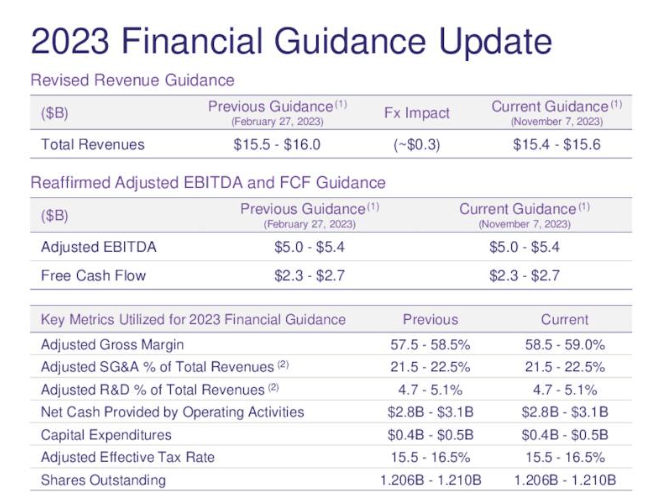

The company had a strong quarter of product launches but had to lower sales guidance for the year to $15.4-$15.6 billion, thanks to a soaring US dollar.

{kind=link}

This is probably the biggest negative to come out of the report. It may seem like a small 2% drop but you have to keep in mind that the company has already reported three whole quarters worth of results. So this is all a Q4-2023 drop. Now the US dollar did soar in Q3-2023. We are showing the performance from July 31, 2023, to date below. VTRS conference call was on November 7, 2023.

The US dollar has pulled back since then and VTRS could deliver a positive surprise when the full-year tally is done.

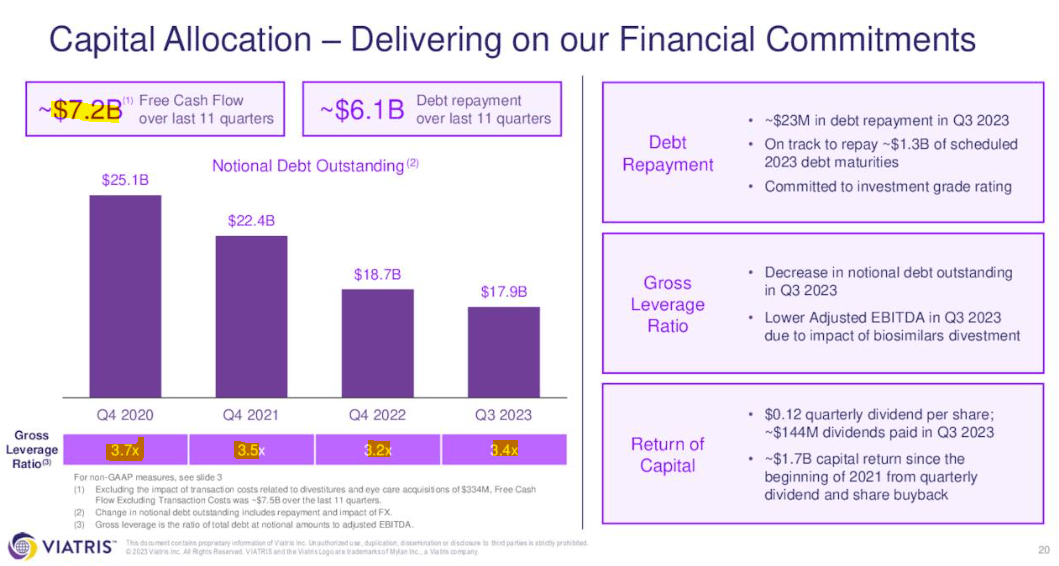

The bigger story is how VTRS is balancing the debt paydown while aiming to reward shareholders. The primary commitment has been, rightfully, the debt paydown. $6.1 billion of the $7.2 billion of free cash flow has gone in that direction.

{kind=link}

Despite that massive cash stream going towards debt, the debt to adjusted EBITDA number is still struggling to make it to 3.0X. That is the problem with sales and adjusted EBITDA erosion. If VTRS could have made the same paydown, while keeping adjusted EBITDA flat since their listing, the leverage would be close to 2.62X. Investors can see this for themselves by applying the 2020 adjusted EBITDA to the current debt of $17.9 billion.

VTRS Q3-2023 Presentation

As we move into 2024, analysts will have to once again extrapolate the base business erosion and see if the company can actually make real progress. So far the answer has been a "Nein". Earnings estimates for 2024 have dropped from $3.15 at the beginning of 2023, to $2.79. The latest drop came right after the Q3-2023 results.

2025 estimates have followed a similar trajectory.

While not an exact match, VTRS' performance in 2023 has matched the two-year forward EPS expectation.

This should not shock anyone as earnings estimates, or rather changes in earnings estimates, are the biggest driver of stock performance.

Verdict

We first wrote about VTRS more than 30 months back.

{kind=link}

The stock was the ultimate value trap in our opinion and we had little faith in management to execute. That has played out so far with the only real winners being those that used the high implied volatilities to repeatedly sell covered calls. They probably made up the 22.16% loss and far more. Yes, we get the cheap aspect and the 3X earnings multiple. What bulls need to get is that there is still $18 billion of debt ahead of the equity and the capacity to service that has only marginally improved since VTRS listed.

Those getting excited about the capital return program should know that the share counts are barely budging here.

That is because stock-based compensation is offsetting a good deal of the benefit.

VTRS Q3-2023 10-Q

As we hit the low $9's, we can argue that there is some value here. You can run some discounted cash flow analysis with some modestly high rates and come out with the idea that the NPV is positive. Normally, at these levels, we might have even nudged a buy rating. The problem here is that while VTRS has held up a bit, the rest of the healthcare sector has gotten decimated. We show Bristol-Myers Squibb Company ( BMY ) and Organon & Company ( OGN ) as two examples in a sector filled with red.

You can find further value in the sector with healthcare closed end funds trading at a discount to the reduced NAV . So you have to be a true believer here to buy this and we cannot say that we are that excited. VTRS only looks cheap if you disregard the debt. Adjusted for it, we would rather own a BMY at 7.0X EV to EBITDA today than VTRS at 5.5X.

We rate the stock a hold/neutral and once again remind investors that those option premiums are your best friend.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Viatris: It Is Always Cheap, Yet It Is Always Declining