VIAV - Viavi's Positioning In 5G: Promising But Stock Is Expensive

2023-10-09 09:49:53 ET

Summary

- Viavi Solutions is a network testing and monitoring company with a diversified portfolio covering three essential business segments.

- VIAV faces competition in various segments but maintains a strong position due to its extensive product range, strategic acquisitions, and focus on innovation, evidenced by its 956 U.S. patents.

- VIAV's financial performance in 2023 showed a decline in product revenues but stability in service revenues.

- VIAV looks slightly overvalued, indicating a potential downside of 20.3% from its current levels. However, its improving business margins and momentum in the 5G sector make it a company to watch.

- While VIAV has strong business fundamentals and is strategically positioned for the 5G transition, concerns about its current valuation lead to a neutral rating for the company.

Viavi Solutions Inc. ( VIAV ) is a promising network testing and monitoring business, boasting a diversified portfolio that covers three essential business segments. In my view, VIAV's strategic initiatives, coupled with its financial trajectory and positioning in the midst of the 5G technological evolution, provide it with a solid foundation for long-term growth. I believe that while VIAV's dedication to innovation and its significant role in the 5G transition are noteworthy, there are valid concerns regarding its current valuation, which might indicate potential risks. Drawing from these observations, I think that a neutral rating for the company seems appropriate when weighing VIAV's promising business prospects against its price.

Business Overview

Viavi Solutions is a network testing and monitoring company offering light management solutions catering to various industries, including telecommunications, government sectors, and consumer electronics. The core revenue streams emanate from three business segments: Network Enablement ('NE'), Service Enablement ('SE'), and Optical Security and Performance Products ('OSP').

The Network Enablement segment fundamentally supports the lifecycle of network operations for notable clients such as AT&T ( T ) and Verizon ( VZ ) by providing essential tools for network design, maintenance, and optimization. In my opinion, the extensive array of products within the NE segment reflects a solid foundation for meeting diverse client needs.

{kind=link}

Moreover, VIAV's strategic focus on acquisitions and restructuring programs to align the business better with market conditions and enhance overall profitability underscores a proactive approach toward capital flexibility and profitability growth. The intellectual property portfolio, boasting 956 U.S. patents as of July 1, 2023, is a testament to VIAV's investment in innovation and a solid groundwork for maintaining a competitive stance in the market (more on its R&D expenses later). I believe this is a judicious strategy in a technology-driven industry where innovation equates to market relevance and long-term sustainability. The strategic acquisitions, I infer, are a thoughtful move to harness synergies and bolster the firm's market position.

Revenue and R&D Dynamics

On the other hand, the Service Enablement segment competes with NetScout Systems, Inc. ( NTCT ), Riverbed Technology, Inc., and Spirent Communications plc ( SPMYY ), enhancing network, service, and application visibility for global Communication Service Providers (CSPs), enterprises, and cloud operators. This is essential in reducing operational expenses and augmenting service reliability , especially during the transition to 5G technology which is a significant market driver.

The Network Enablement segment, despite facing competition from firms like Anritsu Corporation ( AITUF ), EXFO Inc., and Keysight Technologies, Inc. ( KEYS ), fundamentally supports the lifecycle of network operations for notable clients such as AT&T and Verizon by providing essential tools for network design, maintenance, and optimization. With a broad product portfolio, this segment is crucial for Network Equipment Manufacturers (NEMs) in developing next-generation network equipment, showcasing VIAV's holistic engagement in this sector.

The Optical Security and Performance Products segment is at the forefront of venturing into the consumer electronics sector, where it manufactures optical filters for 3D sensing applications , despite facing competition from Anti-Counterfeiting technology providers like Giesecke & Devrient and De La Rue plc ( DELRF ). Furthermore, by diversifying into government and automotive markets, this segment expands VIAV's market footprint and accentuates the company's potential for growth and profitability in a competitive market landscape.

5G Market Outlook from Transparency Market Research

Thus, VIAV's comprehensive approach toward customer engagement, encapsulating project management, installation, and implementation, emphasizes a long-term vision toward building and nurturing customer relationships. This is pivotal in ensuring a steady revenue stream and understanding and responding to evolving market needs. However, as we'll see, it seems the problem lies in VIAV's focus on service revenues and lackluster product revenues.

Declining Product Revenues Are A Concern

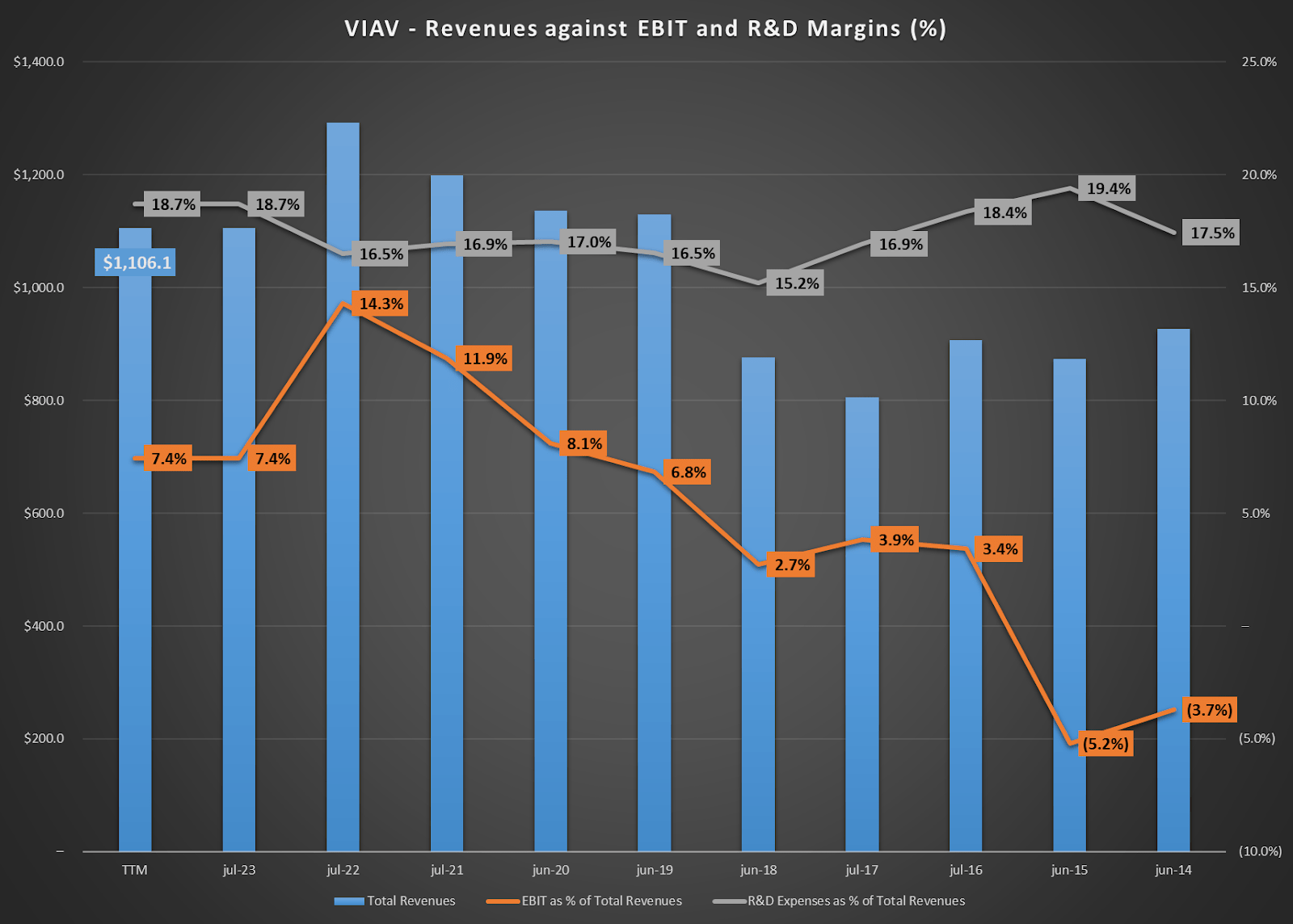

VIAV's 2023 financial performance provides insight into the market's shifting dynamics favoring service revenues. Despite outperforming projections , the 17.6% YoY decrease in product revenues to $936.1 million aligns with broader industry trends. This trend is accentuated by the OSP’s EBIT operating reduction from 40.5% to 36.5%, pointing to possible inefficiencies and a diminished demand for VIAV’s Optical Security and Performance Products. Among VIAV’s segments (NE, SE, and OSP), only SE (mostly service revenues) saw modest growth from 2022 to 2023. This relative stability in the face of a broader revenue decline is a positive sign.

However, it's concerning that service revenues now constitute 9.4% of total revenues, up from 8.0% in 2022. The growth in service revenues from $147.5 million in 2021 to $170.0 million in 2023 might indicate a change in consumer behavior. Yet, considering that a substantial 84.6% of VIAV’s revenues stem from products, I believe the company must re-emphasize its product revenues. While the growth in service revenues is noteworthy, the cornerstone of VIAV's financial health remains its product segment. In fact, VIAV's management compared the current dynamics to a proverbial "Mexican standoff" in the telecom industry. I believe this suggests that they face challenges in product innovation because they're waiting to see how competitors act before acting themselves, which is further evidenced by the decline in product-related revenues. Unfortunately, I think VIAV needs to address this issue quickly before product revenues continue suffering, leading to even worse EBIT margins in the future.

VIAV’s latest 10-K.

Note that SE and Service revenues are not exactly the same. Still, SE is mostly service-related, so I touch on it separately to further emphasize that service revenues are holding up and that the problem lies in VIAV’s product-related revenues.

VIAV’s latest 10-K.

Also, looking at Viavi's allocation of 37.2% of its operating expenses to R&D last year underscores its dedication to innovation despite market adversities and a dip in EBIT margins. I believe this commitment aligns with the fiscal patterns of 2023, where Viavi's focus on nascent technologies, notably 5G, was prominent. Their recent earnings call, highlighting a transition to 800 gig connectivity, strengthens my belief that Viavi isn't merely adapting to industry trends but aspires to lead. This gains significance when considering the decline in the NSE segment's operating profit margins from 15.6% in 2022 to 7.6% in 2023. While it might have been tempting for VIAV to reduce R&D spending to elevate its EBIT margins momentarily, I believe such a move would have jeopardized its long-term market position. Instead, Viavi's emphasis on 5G suggests a strategic intent to penetrate emerging markets and counterbalance such waning demand.

Fiscal 4Q 2023 Earnings Call Supplementary Slides

VIAV’s investment in a new Chandler facility also signifies a commitment to technological and infrastructural growth. Despite the downturn in NSE demand during fiscal 2023, Viavi's forward-thinking approach indicates a business strategy rooted in pioneering products and holistic solutions. This approach is designed to diversify their offerings and insulate the firm from market volatility. Reflecting on these factors, I remain optimistic about Viavi's future trajectory. I anticipate that their sustained R&D and infrastructural investments will bear fruit, potentially enhancing revenues and EBIT margins. In my valuation model, I've estimated a 2% YoY increase in EBIT margins through 2027, a plausible projection given Viavi's strategic endeavors and potential 5G secular tailwinds.

Valuation Analysis

Nevertheless, it's worth noting that VIAV’s R&D expenses have not seen a significant rise when measured as a percentage of total revenues. This suggests that the company is committed to advancing its technology but is also mindful of managing its overall operating expenses. In my opinion, this balanced approach speaks to the company's strategic financial management and its vision for sustainable growth.

With the provided financial background , it's evident that VIAV has maintained a certain level of stability, coupled with moderate growth prospects for the future. I believe the positive trend in EBIT margins indicates potential for slight margin expansion, which aligns with my model assumptions. This is further supported by the company's revenue CAGR of 5.4% since 2017. Such growth is commendable, especially when considering the competitive nature of its sector and the capital-intensive nature of its operations.

Seeking Alpha plus Author's elaboration.

{kind=link}

However, it's important to note that VIAV carries significant debt. While this debt results in a WACC lower than its CAPM, benefiting my valuation model, it also slightly elevates the company's risk profile. I believe this could impact its attractiveness as an M&A candidate, given that its enterprise value surpasses its market cap. I've relied on historical margins for tax, D&A, CAPEX, and NOWC metrics. My valuation model's assumptions are conservative and grounded in reason, ensuring a balanced perspective on the company's future.

Seeking Alpha plus Author's elaboration.

From the valuation model presented, it appears that VIAV might be slightly overvalued, suggesting a potential 20.3% downside from its current levels. In my view, the company's robust business fundamentals somewhat mitigate this valuation concern. While the current valuation doesn't seem to offer a compelling investment opportunity, I believe that VIAV's potentially improving business margins and the ongoing momentum in the 5G sector make it a company to watch in the long term. However, in my opinion, the current price levels do not necessitate immediate action. Hence, I give it a neutral rating.

Conclusion

Viavi Solutions has made a significant mark in the network testing and monitoring sector, positioning itself in line with technological advancements, particularly the 5G transition. In my view, the company's strategic initiatives and consistent focus on innovation highlight its potential for sustained growth in the future. However, the financial data suggests a different narrative. I believe there are concerns regarding its current valuation, especially with indications of a potential 20.3% downside. Given these factors, I think a neutral rating for VIAV is appropriate. While investors should recognize VIAV's commendable strengths, they must also be prudent about the potential valuation risks.

For further details see:

Viavi's Positioning In 5G: Promising, But Stock Is Expensive