VIAV - Viavi Solutions: Revenues May Have Already Bottomed

2023-07-06 05:34:15 ET

Summary

- Viavi, a telecom testing equipment manufacturer, has seen a rise in share prices despite a 21.5% year-on-year decline in sales in its fiscal third quarter for 2023.

- The company's management expects a recovery in its Network and Service Enablement business, which could drive up revenues in the fourth quarter.

- Despite the company's optimistic outlook, the article suggests a hold position on the stock due to potential economic uncertainties.

- The long-term outlook remains positive though due to its products covering both testing needs for fixed line and wireless.

There is a common saying that "the market is forward-looking", signifying that whether it is equities or bonds, the current price reflects what investors expect to happen in the future. Applying this saying to Viavi Solutions ( VIAV ) whose share price is now on an uptrend as shown by the blue chart means that its revenues which currently lag (orange chart) should also follow suit.

Thus, my objective is to assess whether the market is right to think that Viavi's sales have already dipped in its fiscal third quarter for 2023 (FQ3'23) and that from now on they should rise. For this purpose, I will primarily scan its earnings transcripts and finances.

I start by painting a picture of the services offered and how these have been impacted by lower demand.

The Test Equipment Manufacturer's Revenues

As a telecom testing equipment manufacturer, Viavi provides the sort of testers that are used by communications services providers as well as equipment manufacturers to respectively qualify their networks and products. As such, the number of sales that the testing play can drive depends on demand from these companies, and, any pullback is likely to translate into revenue shortfalls.

This is exactly what happened in FQ3'23 (ending in April) when sales of $247.8 million represented a 21.5% year-over-year decline. Still, this figure is $0.8 million above the midpoint of the management guidance which means that while there were expectations of a shortfall, this was less bad than anticipated. The same was the case for the operating profit margin which at 11.4% was 0.4% above the expectation. This was partly due to a restructuring exercise involving the realignment of the business with the growth areas, as well as job cuts. Now, to encourage staff to leave the company will have to compensate them an amount of $10 million to $50 million but in return, this should translate into $25 million of annual cost savings from the second half of this year. This represents about 4% of FY'22 total operating expenses.

Now, progress in managing cost bodes well for profitability but is not sufficient a reason to invest in a company as ultimately it is the topline that drives margins. For this purpose, after the dip in sales, I look at potential recovery.

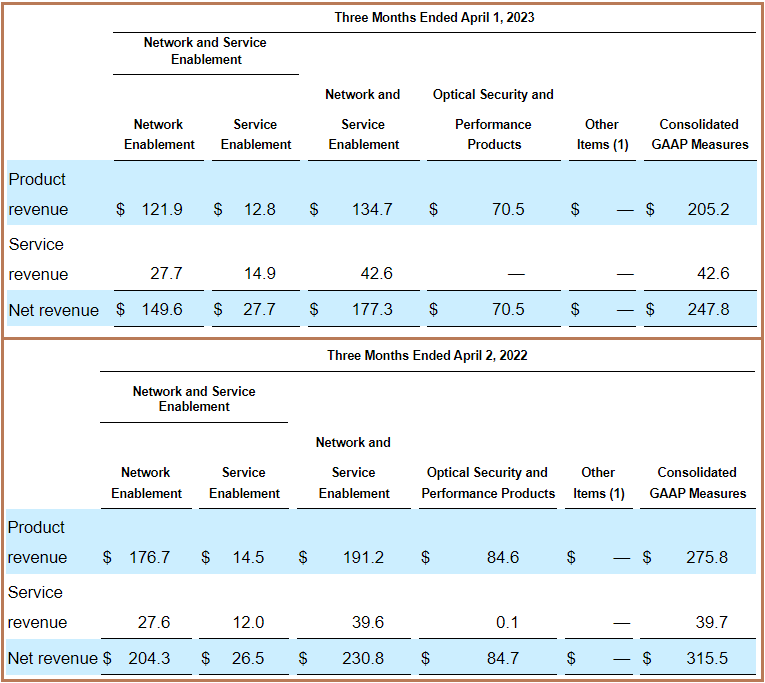

In this respect, the company operates with three segments, NE (Network Enablement), SE (Service Enablement), and Optical Security and Performance Products as illustrated below. The one most impacted by market softness was NE whose sales contracted by double digits figures, from $204.3 million in FQ3'22 to $149.6 million during the latest reported quarter.

Segmental Revenues (seekingalpha.com)

{kind=link}

On the other hand, a lower degree of demand destruction impacted Optical Security and Performance products used in setting up high-speed fiber equipment. Continuing on a positive note, SE grew by 4.5% y-o-y. Furthermore, the management expects its NSE (Network and Service Enablement) business which is the combination of the revenues of NE and SE segments, to have " bottomed out in Q3", which can be interpreted as a sign of recovery.

Now, since the NSE constituted $177.3 million out of the total revenues of $247.8 million for FQ3'23, or 71.5%, any recovery in this business could drive up the topline in FQ4'23, which ends in July.

Assessing the Outlook

In order to verify that this positive outlook is achievable, I have charted the quarterly capital expenditure of the nation's main carriers as charted below. Now, Viavi's customer base spans the world and these companies do not necessarily source test equipment from Viavi, but, the charts still provide a general indication of the spending trend. In this case, since for most of the companies, it is either an upward or horizontal trend as to their capital spending, this shows that they are still investing money in building their networks and are therefore likely to buy testing gear, either from Viavi or its competitors. I have also drawn the chart for Cisco (NASDAQ: CSCO ) which is a network equipment manufacturer.

Looking more specifically at the product application areas, the company testing gears are used both for testing fiber and cable networks, as well as for 5G wireless. Here, in contrast to what is commonly believed, it is not testing demand for the fifth generation wireless which is seeing strength, but rather cable networks from the likes of Comcast (CMCSA) or fiber deployment by Charter Communications ( CHTR ) driven by funding from the FCC's Rural Digital Opportunity Fund.

As for wireless, a contraction in sales for the lab test equipment commonly used for R&D-oriented tasks accounted for most of the revenue slump. On the other hand, demand for testing gear used for field work has been relatively sustained, which is aligned with the fact that mobile network operators are expanding coverage across the U.S.

Therefore, while investments in expanding network coverage continue (above charts), it is more of a mixed picture when it comes to Viavi's products, which may also suggest some competitive pressure.

A History of Beating Estimates but Be Realistic

However, the executives are optimistic that things will improve in Q4 as I mentioned earlier. To support their position, they provide a topline guidance of $242 million to $262 million whose midpoint of $252 million would represent a $4.2 million increase over F Q3'23's sales. Moreover, avionics had been highlighted as being a bright spot with the company having a solid product in the form of the AVX-10K flight line test set which is approved for Boeing ( BA ) aircraft.

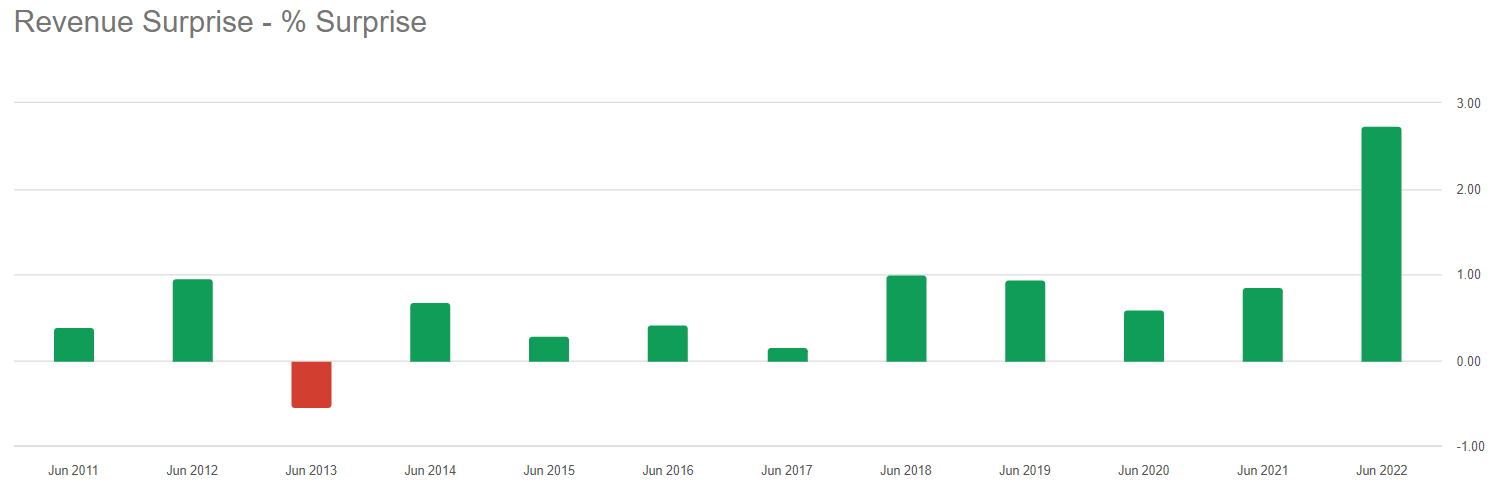

Now, to verify if this guidance could become a reality, I checked the revenue surprise as pictured below, and found that during the last twelve years, the company missed analysts' expectations only once (as illustrated in red), with translates to a success rate of 91.7%. This means that there is a very high probability of the company meeting or even beating analysts' revenue estimates of $252 million (mid-point) for the final quarter. This can in turn result in the annual revenues for the fiscal period ending in June 2023 beating the estimates of $1.12 billion.

{kind=link}

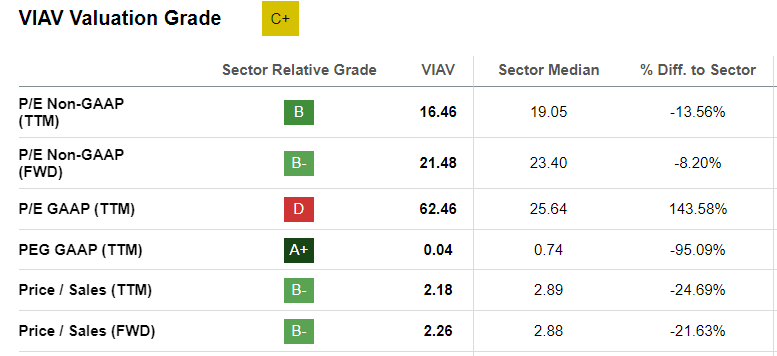

This may be the reason for investors' optimism about the stock since the earnings call on May 2. After the subsequent upside of about 20%, the valuation grade now stands at " C+ " with one of the contributing factors being the trailing GAAP P/E having reached "D" as shown below. This means rich valuations based on earnings due to the company's higher profitability scores.

On the other hand, the trailing Price-to-Sales multiple of 2.18x remains well below the sector median's 2.89x. Thus, the company may be trading at a discount of 24.69%. Adjusting the share price of $11.21 accordingly, I have a target of $13.98, signifying that the upside may be sustained.

Valuations metrics (www.seekingalpha.com)

{kind=link}

However, adopting a dose of realism, things could not work out as expected and the recovery could take longer. Thus, looking at the broader economic picture, there is typically an 18-month lag between the time interest rates were raised at the most aggressive pace around June last year, and the time when the full effects are felt by businesses in general. Thus, despite the U.S. economy proving to be resilient up to now, one cannot exclude a mild recession by the end of this year.

In consequence, with borrowing costs remaining high, businesses could cut capex, albeit temporarily, or even consider cheaper alternative testing equipment in case the economic outlook gets dimmer. To complicate matters, the Fed does not have the luxury to cut rates rapidly as, despite being on a downtrend , inflation still remains higher than its 2% target.

More of a Hold

In conclusion and going against market optimism, I have a hold position on the stock given that we still have to see signs of a recovery in sales. However, I am optimistic for the longer term as Viavi serves two main markets, which are fixed line (cable and fiber) and wireless, where service providers compete with each other. This essentially means that they would have to both expand and improve the quality of their networks in turn implying more purchases of test and quality assurance equipment. Moreover, its balance sheet remains healthy with cash and equivalents of $586.6 million with debt totaling $847.4 million . This is sufficient to redeem about $107 million of convertible notes due next year.

For further details see:

Viavi Solutions: Revenues May Have Already Bottomed