VICR - Vicor: Still Overvalued

Summary

- Vicor stock is down 32% since my Seeking Alpha SELL article back in May of this year.

- However, I wouldn't advise investors to make an attempt to take advantage of the sell-off: the stock appears to have a further and considerable downside.

- I say that because the stock has been unable to buck downward pressure due to a report in March its products were cut out of the Nvidia supply chain.

- Meantime, there are other headwinds, and the most recent earnings report simply does not - in my opinion - justify the current 60x forward multiple.

Back in May I suggested on Seeking Alpha that the stock of leading high-performance power module manufacturer Vicor ( VICR ) was ripe for selling (see Vicor: Whipsawed ). Indeed, the stock has fallen 32% in the 6-months since that piece was published. But before investors are tempted to do some "bottom fishing" here, they may want to wait until the bottom has actually been set - and I don't think that is the case. The company is facing some strong headwinds and - with a forward P/E of 60x - the current valuation level appears to be totally out-of-sync with the company's demonstrated revenue and earnings.

Investment Thesis

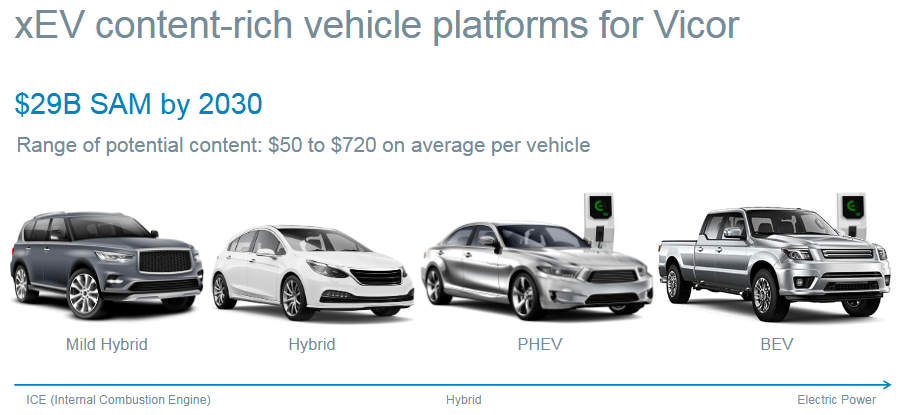

Vicor designs and manufactures proprietary and high-performance modular power solutions. The company's power delivery products provide industry leading high power-density and excellent power-efficiency from source to load. Vicor has customers throughout the technology sector - including high-performance computing ("HPC"), EVs, robotics, satellites, and aerospace & defense. In particular, Vicor believes the global EV market is a huge opportunity, with its potential content per vehicle of up to an estimated $720:

{kind=link}

Headwinds

However, despite the fact that Vicor has proprietary solutions, the market in which it operates is ripe for competition and fairly wide-open. With EV manufacturers striving to bring down the cost of their vehicles, none likely want to get caught designing in a high-margin proprietary solution that cannot be second-sourced. And with the supply-chain challenges recently experienced throughout the technology sector, that same argument likely holds for the other sub-sectors that Vicor operates in as well - like HPC. Indeed, one reason VICR's stock has been so weak this year is likely the report back in March that VICR's products had been designed out of Nvidia's ( NVDA ) next generation of Hopper GPUs while also pointing out that Nvidia was an estimated 55% of Vicor's total revenue. It was an excellent call in my opinion. But to be fair, note that Needham & Company disagreed with that opinion , and defended Vicor:

Based on our conversations with industry participants, we believe NVIDIA has adopted a dual-sourcing strategy with the H100 and expect it to ship a version of the H100 SXM5 card powered by Vicor later this year. We still believe Vicor can meet our revenue forecast based on its strong backlog, but acknowledge the multi-sourcing strategy increases the importance of a successful manufacturing ramp of Vicor's expanded manufacturing facility in Andover.

Needham even reiterated its BUY recommendation and $130 price target. But that didn't work out too well:

Meantime, a company like Wolfspeed ( WOLF ) is killing it with silicon carbide based solutions for the EV market (and other highly power-efficiency conscious applications). In Wolf's Q4, the company grew revenue to $228.5 million ( +56.7% yoy ).

Now let's take a look at Vicor's most recent earnings report.

Earnings

Vicor released its Q2 report in July, and in my opinion it was noticeably weak and a continuation of VICR's previous earnings disappointments - at least compared to my expectations. However, note that the market said Vicor's Q2 was a beat on both the top- and bottom-lines.

Yet from my perspective, quarterly revenue of $102.2 million was up only 7.1% yoy. Not too good for a company sporting a forward multiple of 60x - at least not in the current market environment. In addition, the book-to-bill ratio came in under 1 - another sign of weakness that fails to support such a lofty valuation.

The EV thesis for Vicor does not appear to be working out as the company expected - at least not yet. I say that because Tesla's ( TSLA ) most recent Q3 results were quite strong in my opinion. After all, in Q3 Tesla produced over 365,000 vehicles and delivered over 343,000 vehicles (+54% yoy) . Of course Tesla isn't the only EV maker out there, but if Tesla is any indication of the growth of the overall EV market (and it is ...), and if Vicor was participating in that market to any meaningful extent, why is Vicor's revenue growth so tepid in comparison?

In addition, Vicor's gross margin as a percentage of revenue fell to 45.8% for Q2. That compared to 52.3% for Q2 last year - but did increase from 42.6% in the prior quarter. One of the investment thesis' for Vicor was that the addition supply capacity the company had been adding would raise overall company efficiency and increase gross margin. That certainly hasn't happened yet. Vicor CFO Jim Schmidt gave some color on the margin issue during the Q2 conference call :

Headwinds impacting our gross margin including elevated cost of securing supply and outsourced capacity continued in Q2. In addition, tariffs, continue to be a drag on gross margin at $2.1 million in Q2 and 2.1% of revenue. Our work to reduce tariffs by reducing imports from China continues.

Since the Chinese dramatically increased its belligerence with respect to Taiwan, the Biden administration has cracked-down hard on technology trade with China . Indeed, that Reuter's article just referenced reported that Nvidia - again, one of Vicor's largest customers - had been told by the U.S. government to restrict exports to China for two of its AI computing chips - the latest salvo in the Biden administration's broader effort to hamper China's access to the most sophisticated semiconductors for AI and other potential military applications. That's a headwind for Vicor as compared to last year.

One possible bright-spot is that Vicor's one-year backlog stands at $400 million. However, that is roughly 4x Q2 revenue, which - once again - isn't overly supportive of a 60x forward multiple.

Summary & Conclusion

The bottom line: considering the rather strong headwinds facing Vicor - primarily increased competition (i.e. margin pressure) and the China trade issue - I simply don't see a reason to go long the stock at this time. In fact, in my opinion, the company's most recent financial results don't come close to supporting a 60x forward multiple, and suggest that the multiple could easily drop by half over the next year.

That said, Seeking Alpha paints a somewhat different picture, certainly as far as the SA Authors are concerned - they have a STRONG BUY recommendation:

Seeking Alpha

You can click on the link above to get more detailed information on these ratings and grades. Meantime, as previously indicated you can probably guess that I certainly agree with the "D" rating on valuation. And I question the "A" score for growth given that revenue this year is only expected to be up only ~11%. Yet I have my doubts it will even be that high considering first 6-months revenue was only $190 million (+3.4% over the first 6-months of last year). Time will tell. While I'll give SA a pass on the "C-" for profitability, not sure how they came up with a "C-" rating for momentum considering the stock is down 62% this year, under-performing the S&P500 by a whopping 50%.

VICR is a STRONG SELL and could easily trade-down to the $35 level (it closed Friday at $46 and change. At $35, VICR would still have a forward P/E of ~45x, which is - in my opinion - still extremely generous given VICR's most recent earnings report. I'll end with a 5-year price chart of VICR stock and note that it is now below its pre-pandemic high in early 2020, another sign that momentum is absolutely terrible:

For further details see:

Vicor: Still Overvalued