VITFF - Victoria Gold: Canadian Mid-Tier Gold Producer

2023-08-04 15:41:27 ET

Summary

- Victoria Gold is a mid-tier gold producer in Canada with a long-life mine that is economic at low gold prices.

- The stock is currently undervalued due to a lack of sentiment in the PM mining sector.

- The company's Eagle mine in the Yukon is in a prime location and has the potential for significant growth and exploration success.

Introduction

Victoria Gold (OTC: VITFF) is a mid-tier gold producer in Canada (Yukon). They are one of the few large open-pit miners with economic costs at low gold prices. They began producing in 2020 and have a long-life mine. The future looks bright for them, and I like their Eagle mine.

What makes this stock interesting is the current lack of sentiment in PM miners. We have endured both a 12-year correction since the 2011 high in gold, and a 3-year correction since the 2020 break-out. Investors are simply tired of waiting for gold to break out. Subsequently, Victoria is currently selling for a FCF (free cash flow) multiple of 5. IMO, it is half off, and should be selling at a 10.

I think investors are ignoring the premiums that will be paid for mines in good locations. And Victoria’s Eagle mine in the Yukon is about as good a location as you can find. It’s in the middle of nowhere, bothering no one. I think investors will gladly pay a 20 multiple once gold reaches $2500, and sentiment improves.

If I’m right, then the leverage is huge if gold prices take off. Not only should their multiple go up by a factor of 4, but they could also increase their valuation based on the FCF, which will expand . For example, I’m projecting their FCF to increase from $85 million to around $300 million at $3,000 gold in a few years. If we value them with a conservative 15 multiple (instead of my expected 20), that is a $4.5B valuation.

That upside is based only on the Eagle mine. However, Victoria has the potential to grow into a very large company if they don’t get acquired. They have a second mine (Raven) in their pipeline and equity ownership in two companies (Banyan and Lahontan) that they could acquire.

Of course, many things can go wrong, and usually do with PM miners. These investments are never slam dunks and go according to plan. I will point out some of the risks of owning Victoria below.

One thing I always like to point out is that investing in PM miners is speculating. We are gambling, since so many things can go wrong. Keep your allocations low and expect to lose money on some of your PM mining stocks. What we are really betting on is PM prices going higher. If gold prices rise, then Victoria Gold will be in a strong position. If gold prices languish, then bad things can happen.

| Stock Name |

| Symbol (US) |

| Type |

| Category |

| Share Price (US) |

| FD Shares |

| FD Mkt Cap (8/3/2023) |

| Victoria Gold |

| Gold |

| Mid-Tier Producer |

| $6.05 |

| 69M |

| $417M |

Company Overview

Victoria Gold is a mid-tier producer in Canada. Their Eagle Gold project began production in 2019. It is a 5 million oz resource (.7 gpt) in the Yukon. It has a 75% recovery rate, so the actual resource is about 3.5 million oz, which is still large. It is a large property (150,000 acres) with a lot of exploration potential. They already have a second discovery at Nugget (124 meters at 3.5 gpt). I expect them to find more gold. Eagle is a large property (175,000 acres) with many drill targets.

The $285 million capex was financed using $200 million of debt and by diluting shares using equity financing. They still have $184 million in debt. They owe $58 million over the next 6 Qtrs. Then another $125 million is due in December 2024. This will likely need to be rolled over into a longer-term loan. Hopefully, they can afford their next 6 quarterly payments using their FCF.

Currently, their FCF is about $20M a Qtr, and their loan debt is about $10M a Qtr. Seems like they should be okay, and won’t need to dilute shares. They will produce around 175K oz in 2023, with an AISC of about $1,200, and a breakeven (FCF) of around $1,450. In 2024, production is forecast to rise to 194K oz. In 2025, they will finally reach 200K, which they should be able to maintain for another ten years with exploration success.

A takeover is possible, although I don't think they would take a lowball offer because insiders own about 25%, and the CEO has a substantial amount of shares. I would think it will take a premium of at least 35%. The likely buyer is Coeur Mining, which owns 10% of the shares. This is the biggest risk IMO. We don’t want them to get taken out with their leverage for higher gold prices.

They will likely have exploration success to expand their resources. They have already found three other nearby discoveries (Olive, Shamrock, and Nugget). I expect them to find more gold and become a 250,000 oz producer at their Eagle mine.

They have another project that is nearby. Raven is already a 1.1M oz deposit (at 1.7 gpt) and is growing in size. They plan to build a separate mill for Raven, so it will require permitting. I don’t expect the first pour at Raven until the end of the decade. We don’t have any guidance yet for a PEA, so it is still very early.

They own 12% of Banyan Gold, which has a 4M oz deposit (at .6 gpt) in the Yukon. This is a similar deposit to the Eagle and would be a perfect acquisition for Victoria. Plus, they own 48% of Lahontan Gold, which has a 1.5 million oz deposit in Nevada. So, they have many possibilities to grow production.

Company Info

Cash : $21 million

Debt: $183 million

Current Gold Resources: 6 million oz.

Current Gold Production: 175K oz.

Current All-in Costs (breakeven): $1,450 per oz.

Current FCF multiple: 5

Estimated Future Gold Reserves: 4 million oz.

Estimated Future Gold Production: 225K oz.

Estimated Future Gold All-in Costs (breakeven): $1,600 per oz.

Estimated Future FCF Multiple: 15

Scorecard (1 to 10)

Properties/Projects: 7.5

Costs/Grade/Economics: 8

People/Management: 7.5

Cash/Debt: 7

Location Risk: 8

Risk-Reward: 7.5

Upside Potential: 8

Production Growth Potential/Exploration: 7.5

Overall Rating: 7.5

Strengths/Positives

Moderate costs (economic at low gold prices).

Excellent location.

Significant upside potential.

Good management team.

Second mine in their pipeline.

Good exploration potential.

Risks/Red Flags

Dependence on higher PM prices (for large returns).

High debt.

Could be acquired.

Long wait for their second mine (Raven).

Speculation stock (high risk).

Estimated Future Valuation ($ 3000 Gold )

Gold production estimate for the long term: 225K oz.

Gold All-In Costs (break-even): $1,600 per oz.

225K oz. x ($3,000 - $1,600) = $315 million annual FCF (free cash flow).

$315 million x 15 (FCF multiplier) = $4.7 billion.

Current FD market cap: $417 million.

Upside potential: 1,000%.

Future Valuation Explained

This is an estimated return and will only occur if all assumptions are correct. A more likely outcome will be something less than this amount, although it is not crazy talk to expect the FCF multiple to reach 20.

My All-In Costs are the expected costs that will generate FCF.

I used a future FCF multiplier of 15, which I think is conservative for my expectations. I expect them to receive a 20 multiple.

I used a future PM price of $3,000 gold because I am a long-term investor who plans to wait for higher gold prices. I expect to see this level reached within 3-5 years.

A $3,000 gold price may seem like a pie-in-the-sky fantasy, but gold traded at $700 in 2008 and then went up 170% to $1900 in 2011, over a 4-year period. Expecting gold to rise 50% from $2,000 to $3,000 is not a stretch. Below is the monthly gold chart.

{kind=link}

Gold Monthly Chart (Trading View)

Also, the only reason to own gold mining stocks, IMO, is if you are concerned about the state of the US economy and debt bubble that seems to be at a breaking point. The US has been living off debt since the early 1980s, and this can only continue for so long. At some point, our national debt ($32T and growing rapidly), corporate debt ($24T), and household debt ($1T in credit card debt) will become an issue, and gold will benefit from that outcome. At least, that’s my thesis.

Some investors think that debt is not a problem because the US economy is strong. If you believe that, then PM miners are probably not where you want to invest. My concern with debt is the reason I use $3,000 gold as my target.

Balance Sheet/Share Diluti on

They currently have a weak balance sheet with $21 million in cash and only $183 million in long-term debt. They owe $58 million over the next 6 Qtrs (about $10 million each Qtr). Then another $125 million is due in December 2024. This $125 million will likely need to be rolled over into a longer-term loan. I don’t think that will be an issue with their strong FCF. Loans are rolled over all the time. Hopefully, they can afford their next 6 quarterly payments using their FCF, and won’t need to dilute shares.

Note that once they clean up their balance sheet and get rid of their debt, the potential for a high FCF multiple increases substantially. Why? Because investors are drawn to companies with clean balance sheets and high FCF. That combination works amazingly well.

Risk/Reward

As I mentioned at the beginning, investing in PM miners is speculating . Why? Because one of your assumptions is bound to get flipped. The biggest risk is that PM prices won't rise, or inflation will cause costs to rise significantly, reducing expected margins. Many things can go wrong.

One thing that could go wrong is our expectation of margins. I'm expecting large margins as gold prices rise, which will drive up their FCF. Several things could hinder large margins, one of which is higher energy prices. Also, Canada could raise taxes or royalties. And there is always the potential for worker stoppage over higher wages.

While the risk is high, the reward for Victoria is enticing if gold prices rise substantially. Plus, if Victoria finds a way to grow production, the reward could be even higher than I anticipate with my estimated future valuation.

Investment Thesis

Victoria appears to be well-positioned and well-leveraged for higher gold prices. They are somewhat unique, being an open-pit producer (moderate costs) in a great location (Yukon). These factors make it very attractive.

I want to own as many PM mid-tier producers in good locations as I can find. Why? Because I think they will be valued at a premium with high FCF multiples. I remember 2011, when marginal mid-tier gold producers in Canada were valued exorbitantly. San Gold was a 70,000 oz producer and was valued at $1 billion! And they didn’t have large resources (1 million oz deposit), and they didn’t have low costs. That could easily happen again.

The risk is high because of their debt and the potential for them to be acquired. If you allocate your funds, it might not pay off as expected. It usually doesn’t. That’s why I like to own a lot of PM miners and then let the winners appear.

Strategy to Manage Risk

{kind=link}

www.goldstockdata.com

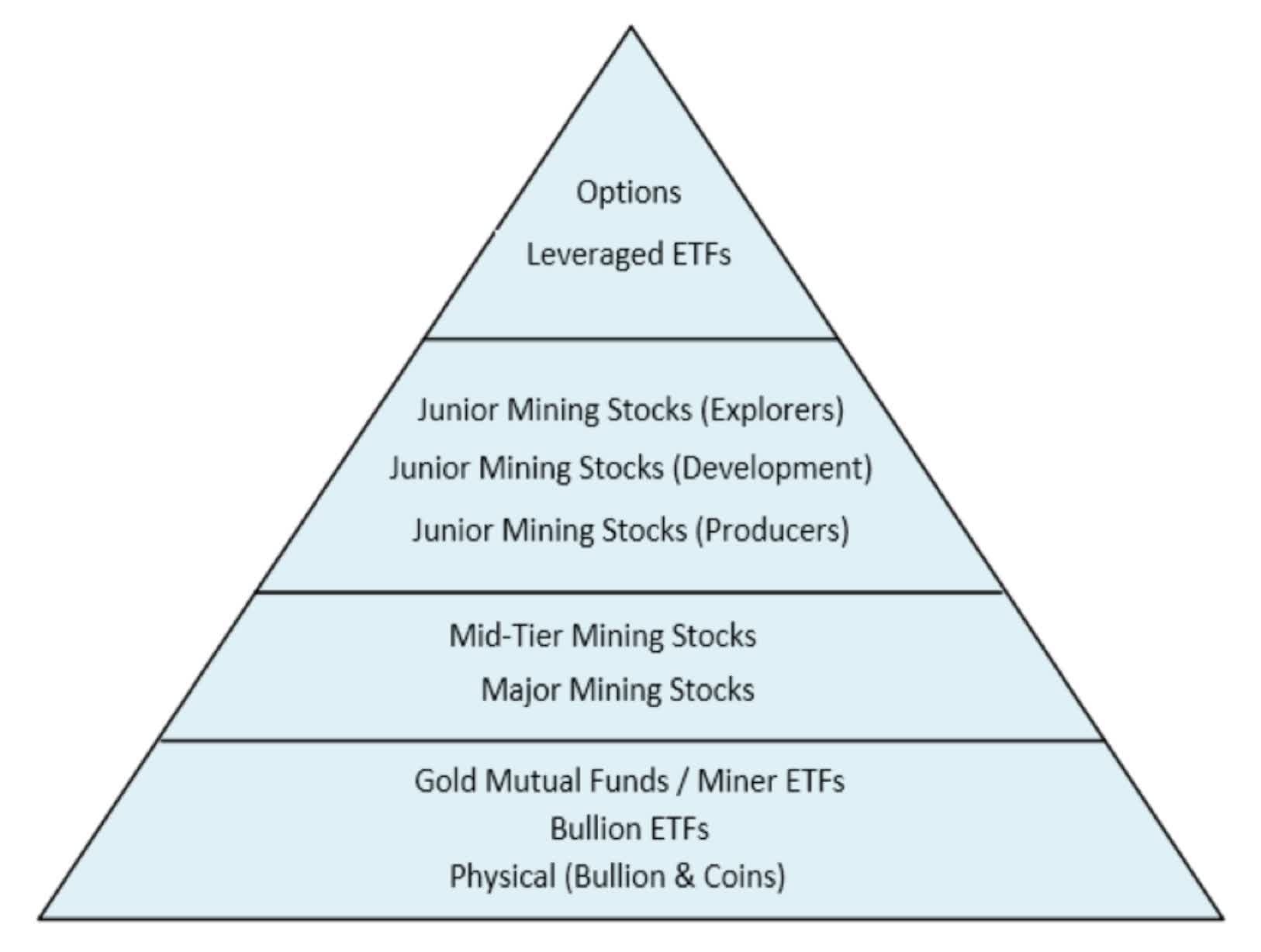

I use a pyramid approach (as discussed in my book) to manage risk, along with low allocations (normally less than 1% per individual stock), whereby I use less risky assets at the base of the pyramid and riskier stocks as I move up the pyramid.

As the shape of a pyramid implies, the bulk of my portfolio is on the lower half. This means that I hold fewer riskier stocks as a portion of my cost basis. Also, the base of the pyramid should be strong enough to withstand major corrections when the riskier stocks (exploration and development) higher up on the pyramid get obliterated (sometimes down 70% or more).

Victoria fits in the lower half of the pyramid, where I accumulate quality mid-tier producers. Ironically, it is also a high-upside stock because of its moderate costs, great location, and cheap valuation. In many respects, I think it is an ideal stock to own. Many are fortunate it is this cheap. I don't think it will be once gold reaches $2,300, when it will likely double in value.

I don't trade. Instead, I use a buy-and-hold strategy of accumulating stocks (expanding my portfolio). Sometimes I think I am more of a stock collector than an investor.

While I am constantly accumulating stocks (I currently hold over 150 stocks), I also have an exit strategy. In fact, I have an exit strategy for each stock. I often add to stocks that crash more than 50% if I still like the story, thereby reducing my cost basis.

I rarely add to stocks that fall less than 50%, unless I think I am underweight on an exceptional stock. Moreover, I always buy big stock market corrections to improve my portfolio (this is usually the best time to buy).

I currently have a list of about 10 stocks that I want to buy in the coming correction. Of these 10 stocks, about half I already own. This will improve my portfolio.

My New Investing Group is Coming in August!

I am pleased to announce that my Investing Group, "Gold Silver Mining Ideas" will be launching on Tuesday, August 29th. This is your opportunity to interact with me directly and join my community, so save the date to sign up.

I'm creating this Investing Group to have more flexibility on what I can post. It will add a lot more value than my current posts in SeekingAlpha. It will also include an ideal portfolio using my investing strategy.

For further details see:

Victoria Gold: Canadian Mid-Tier Gold Producer