HL - Victoria Gold: Tracking Well Against Fiscal Year 2023 Guidance

2023-07-06 14:16:02 ET

Summary

- Victoria Gold Corp. reported a 47% YoY increase in gold production to ~83,200 ounces in H1, following a strong Q2 report, with a record ~45,600 ounces produced.

- This has marked a shift from the company previously missing by a wide margin on guidance to over-delivering year to date and being on track to beat its FY2023 cost guidance ($1,350-$1,550/oz).

- That said, while Victoria is reasonably valued, I see more attractive bets elsewhere in the sector, and would only become interested in the stock below US$5.55 in its updated low-risk buy zone.

Just one month ago, I wrote on Victoria Gold Corp. ( VITFF ), noting that while the stock didn't offer enough margin of safety at US$6.30, pullbacks below US$5.65 would present a low-risk buying opportunity and that a production beat looked likely in 2023 with the bar set quite low. Since dropping into this buy zone last week, Victoria Gold ("Victoria") has rallied over 12% on the back of a solid Q2 production report , and a much better H1-2023 performance.

Victoria's solid execution is evidenced by gold production increasing over 47% year-over-year to ~83,200 ounces, and this has placed the company in a position to easily deliver into FY2023 guidance, a welcome departure from the previous trend of over-promising and under-delivering in H2-2020, 2021, and 2022, with significant guidance misses in the latter two periods. Let's dig into the preliminary Q2 report a little closer below and whether the stock is worth paying up for at current levels.

All figures are in United States Dollars unless otherwise noted with a C$ in front of the dollar figure.

Eagle Mine Operations (Company Website)

{kind=link}

Q2 Production

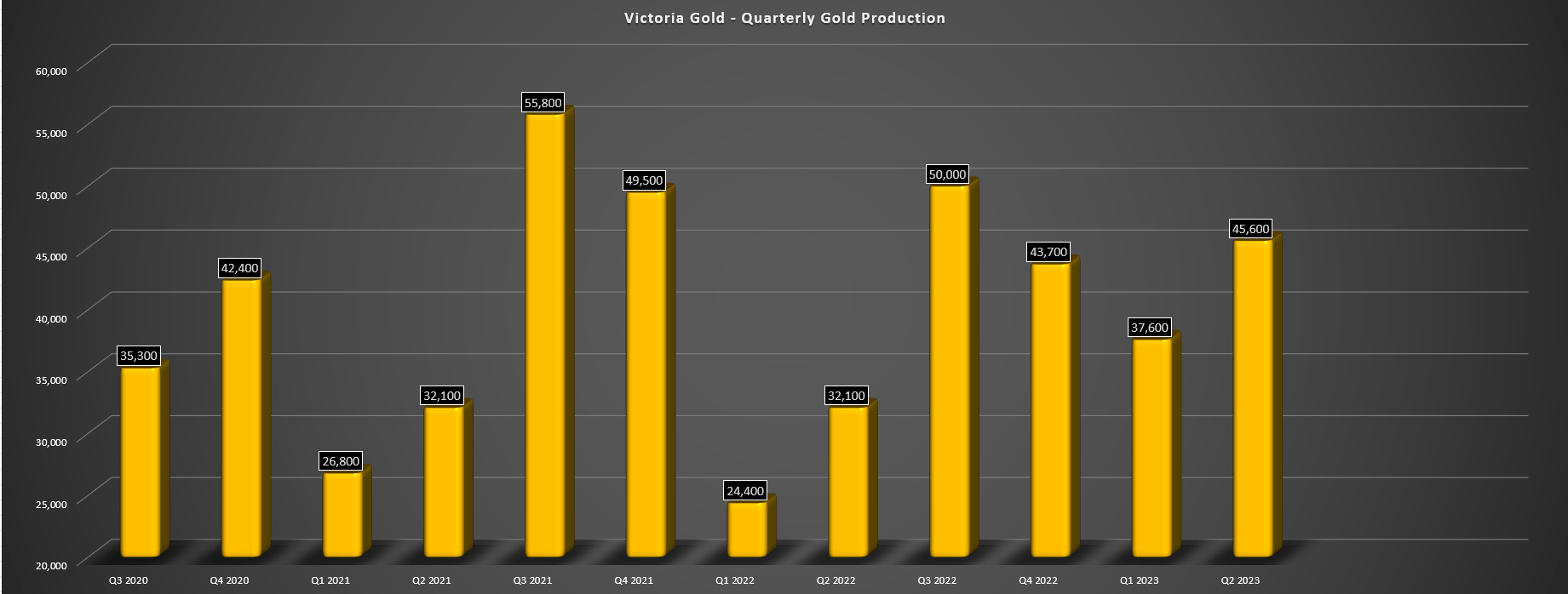

Victoria Gold released its preliminary Q2 results this week, reporting quarterly production of ~45,600 ounces of gold, a new Q2 record which trounced its previous record of ~32,100 ounces. The sharp increase in production was related to the successful implementation of its year-round stacking strategy that set the company up for a better Q2 and higher mining rates year-over-year of ~49,000 tonnes per day (Q2 2022: ~48,000 tonnes per day) or ~2.3 million tonnes mined and ~2.5 million tonnes stacked in the period. Notably, the improved stacking rate offset the slightly lower grade of ore stacked in the period, which dipped to 0.77 grams per tonne of gold, down from 0.85 grams per tonne of gold in the year-ago period. Just as importantly, the company noted that gold grades and metallurgical recoveries continue to track well against the reserve model at its Eagle Mine in the Yukon.

Victoria Gold - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

The Q2 production increase of ~42% was a significant step towards regaining the market's trust regarding guidance, but the H1 performance was even more impressive. This is because we saw a 47% increase in gold production in H1-2023 vs. H1 2022 to ~83,200 ounces of gold (H1 2022: ~56,400 ounces), and this was despite flat grades in the period and primarily on the back of operational improvements. And while the unusually cold weather in Q1 2022 resulted in easier comparisons on a year-over-year basis, this is a phenomenal start to the year for the company and we should see a material improvement in its Q2 financial performance even after factoring in inflationary pressures that continue to affect the sector, with stickier areas being labor and cyanide costs. In fact, Victoria looks set up to generate significantly more free cash flow in FY2023 compared to last year despite the slow start to the year (Q1 2023: free cash outflow of ~$31 million), with the potential to generate over $30 million in free cash flow this year.

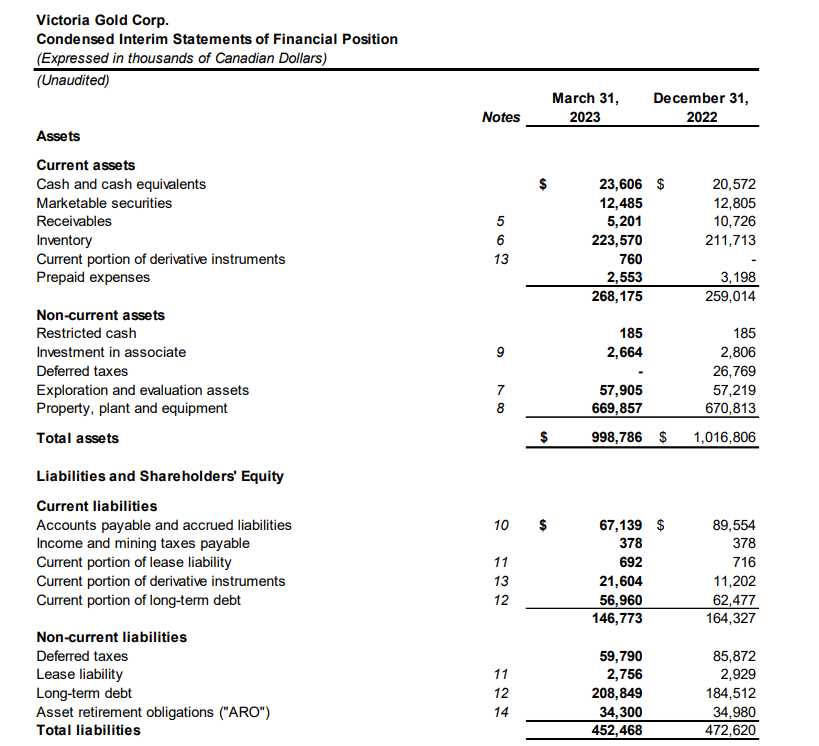

Victoria Gold - Q1 Financial Position (Company Filings)

{kind=link}

Obviously, a return to positive free cash flow is important for a company with a relatively high debt load like Victoria (~$190 million in net debt), but the shift from over-promising and missing by a mile to over-delivering is just as important to improving sentiment for the stock. And this is certainly what Victoria has accomplished with a second consecutive solid quarter, with production currently sitting at ~48.9% of its guidance midpoint (170,000 ounces), and with the company positioned to come in near the high end of its full-year guidance range (160,000 to 180,000 ounces). In addition, the company should beat its cost guidance with ease (assuming no hiccups like last year) with all-in sustaining costs likely to come in below the low end of guidance near US$1,330/oz vs. its stated guidance range of US$1,350-$1,550/oz, benefiting from higher ounces sold and a lower oil price year-to-date. In summary, there's certainly lots to like about the H1 performance.

Recent Developments

Moving over to recent developments, the company's opportunistic for ATAC Resources (a Yukon explorer with a massive land package of 1,700 square kilometers) expired earlier this year, with Hecla ( HL ) coming over to the top with a sweeter offer (C$0.14 per share) to ensure it locked down the property. While this might be a little disappointing, as Victoria's offer certainly came at the right price (C$0.12 per share), I think it was smart to be disciplined and not overpay. This is because even if this was a very attractive price at the proposed offer (if accepted), with a sub $10.00/oz cost on measured, indicated, and inferred ounces, the company isn't in the financial position to ramp up exploration and development work at the Rackla Gold Property, and I think the better move is paying down its debt.

Rackla Gold Property (ATAC Resources Presentation)

{kind=link}

As for Hecla, the company is also busy having just come off the acquisition of Keno Hill in the Yukon, but it can afford to develop ATAC's projects with a stronger balance sheet and much less leverage than Victoria. Plus, Hecla has much higher margins than Victoria, so if we were to see a violent cyclical bear market in the gold price, Victoria would have potentially been in a more vulnerable position vs. Hecla that can easily stomach a further 15% decline in commodity prices from current levels at most of its operations. To summarize, while I think the opportunistic bid for ATAC was a surprising move and one worth exploring at the price offered, I'm glad to see Victoria hasn't got into a bidding war with Hecla which has deeper pockets and is in a better position to advance the asset from a financial standpoint.

As for other developments, Victoria continues to report solid exploration results from its nearby Raven deposit, with a phenomenal intercept of 3.59 grams per tonne of gold over 83.5 meters reported earlier this year, which was 300 meters outside of the Raven resource (~1.07 million ounces at 1.67 grams per tonne of gold), and certainly well above the average Raven resource grade. This continued resource growth is certainly encouraging, especially given that Raven remains open along strike and at depth, pointing to further upside in this resource base when accounting for step-outs to the east. Hence, while the bid for ATAC didn't progress as hoped, Victoria already has a solid pipeline already at its Dublin Gulch Property, with multiple regional targets and one of the longer mine lives among its peer group, suggesting it's not nearly as desperate for M&A as some other junior and or small-cap producers that are staring down shorter mine lives, like Fortitude Gold ( FTCO ), First Majestic ( AG ), and Guanajuato Silver ( GSVRF ).

Valuation

Based on ~68 million fully diluted shares and a share price of US$6.22, Victoria Gold trades at a market cap of US$423 million. This is a relatively low valuation compared to other 200,000 to 300,000-ounce producers elsewhere in the sector like Ramelius Resources ( RMLRF ) and Silver Lake Resources ( SVLKF ) at enterprise values closer to ~$700 million, but some of this valuation discrepancy is bridged by Victoria's relatively large net debt position, with its enterprise value closer to ~$610 million when including net debt. Plus, Victoria Gold is a single-asset producer even if in a Tier-1 jurisdiction while Ramelius and Silver Lake are multi-asset producers, giving them increased diversification and multi-asset producers typically trade at slightly higher multiples, assuming similar margin and jurisdictional profiles.

If we compare Victoria's market cap to its estimated net asset value of ~$630 million (including exploration upside), Victoria trades at 0.67x P/NAV, making it one of the lower-priced producers in Tier-1 jurisdiction sector-wide. However, although a discount to some of its peers from a P/NAV standpoint, the stock is much less undervalued from a free cash flow standpoint, trading at ~12.7x EV to FY2024 free cash flow estimates (~$48 million). Hence, I see more attractive relative value bets elsewhere in the sector, with some producers trading at less than 6.0x FY2024 EV/FCF. And, while I see a fair value of US$9.25 for Victoria based on 1.0x P/NAV, I am looking for a minimum 40% discount to fair value for small-cap producers, with Victoria's ideal buy zone coming in at US$5.65 based on this required discount to fair value.

This doesn't mean that Victoria can't head higher from here and trade back to US$7.00, but I prefer to pay the right price or pass entirely, and following the stock's recent rally, it has moved well outside of its ideal buy zone. In addition, the stock now has an unfilled gap below, which I would argue has a good chance of being filled, translating to an elevated risk of paying up for the stock at US$6.25. So, while I think Victoria is one of the more reasonably valued producers sector-wide after two years of underperformance and it's coming up against easy comps in H2-2023 (vs. H2-2022) after the conveyor belt failure last year, I continue to see better value elsewhere in the sector, and I don't see any reason to pay up for the stock above US$6.25, a level that's 13% above its updated ideal buy zone of US$5.55, especially when there are other names trading at higher free cash flow yields and stronger balance sheets.

Summary

Victoria Gold Corp. put together an impressive Q2 and H1 performance and is on track to beat cost guidance and deliver into the high end of its FY2023 production guidance if it can maintain its strong momentum with its strongest quarter of the year on deck (Q3). And combined with a gold price that has spent a record 16 consecutive weeks above $1,900/oz, the company certainly picked the right time to start delivering on its production targets.

That said, the updated low-risk buy zone for Victoria comes in at US$5.55, and with the stock 13% above this level, I no longer see the stock in a buyable position and don't see any reason to chase the stock above US$6.30. This is especially true when other small-cap producers are less sensitive to gold price weakness and trade at deeper discounts to fair value. To summarize, while I see Victoria Gold Corp. stock as a Speculative Buy at US$5.55, I see more attractive bets elsewhere currently.

For further details see:

Victoria Gold: Tracking Well Against Fiscal Year 2023 Guidance