VITFF - Victoria Gold: Weakest Quarter Of Year In Rear-View Mirror

2023-06-08 12:06:01 ET

Summary

- Victoria Gold's stock has suffered a 22% drawdown despite solid Q1 results, with it being a high-cost producer that has increased leverage to the gold price.

- The good news is that its turnaround thesis remains intact, with its year-round stacking strategy implemented successfully in Q1 2023 and margins recovering in Q1.

- That said, I still don't see enough margin of safety in the stock just yet, with the ideal buy zone for Victoria coming in below US$5.65.

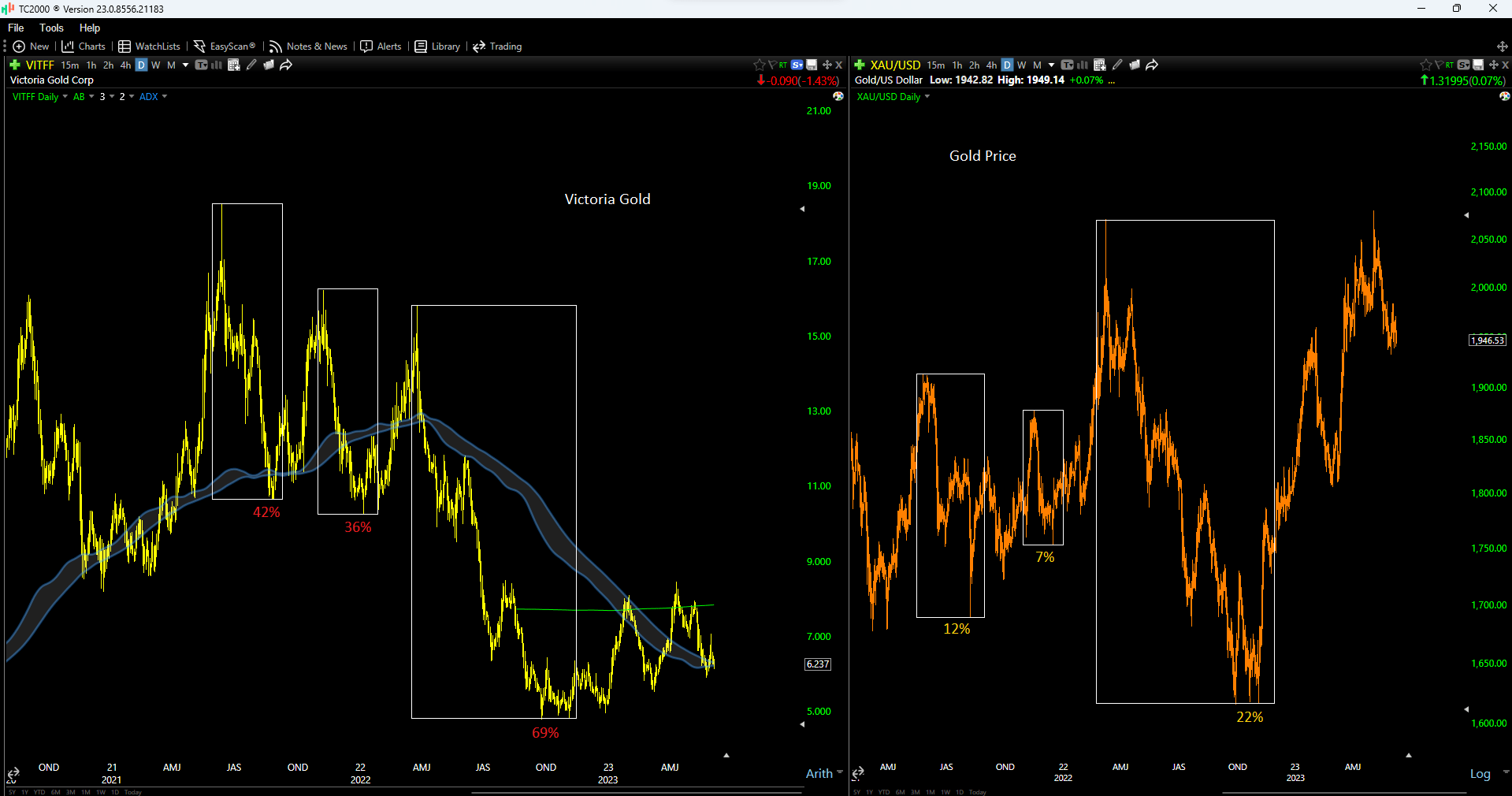

Just six weeks ago, I wrote on Victoria Gold (VITFF), noting that there was little reason to pay up for the stock above US$7.60 when the stock was getting closer to its fair value estimate and had already rallied 50% off its lows. This is because the stock was a high-cost producer that would be more vulnerable to any loss of momentum in the gold price, and the time to buy more leveraged producers is when they're hated, not after they've already rallied 45% off their lows. Since then, Victoria has put up solid Q1 results but has still suffered a 22% drawdown, which shouldn't be surprising for the late-to-the-party bulls, given that it has consistently had extreme negative leverage to the gold price (including a 36% correction from November to December 2021 during a mild 7% correction in the gold price).

{kind=link}

The good news is that the company appears to be turning things around, with the year-round stacking initiative being a success, evidenced by a 138% increase in tonnes stacked year-over-year on its heap leach pads. And while costs may be up over its mine life because of inflationary pressures and what continues to be a tight labor market sector-wide, the gold price has helped to offset some of this margin erosion, with Victoria reporting more respectable all-in sustaining cost margins of US$447/oz in Q1 2023. That said, turnaround stories require more patience and one must pay the right price to ensure a margin of safety, and while we may be in the early innings of a turnaround, I still don't see a compelling enough valuation setup just yet. Let's look at the Q1 results and dig into the valuation below:

{kind=link}

All figures are in United States Dollars unless otherwise noted with a C$ in front of the figure.

Q1 Production & Sales

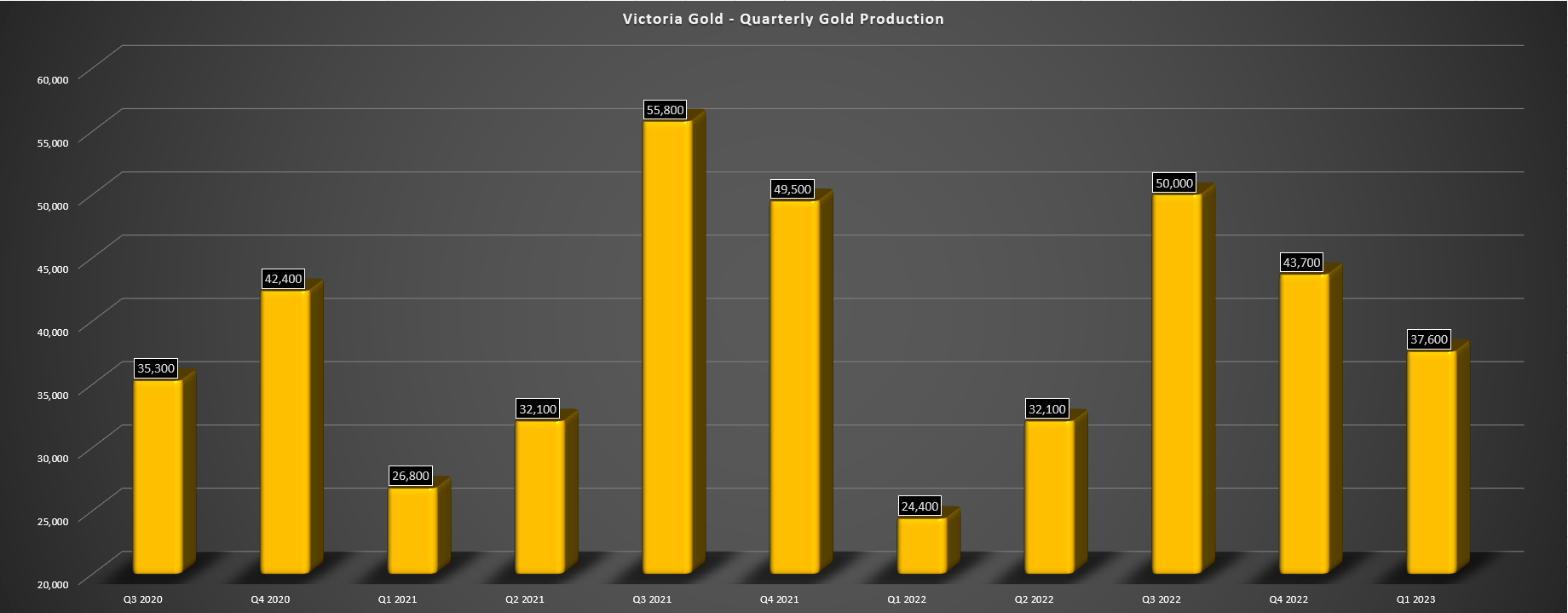

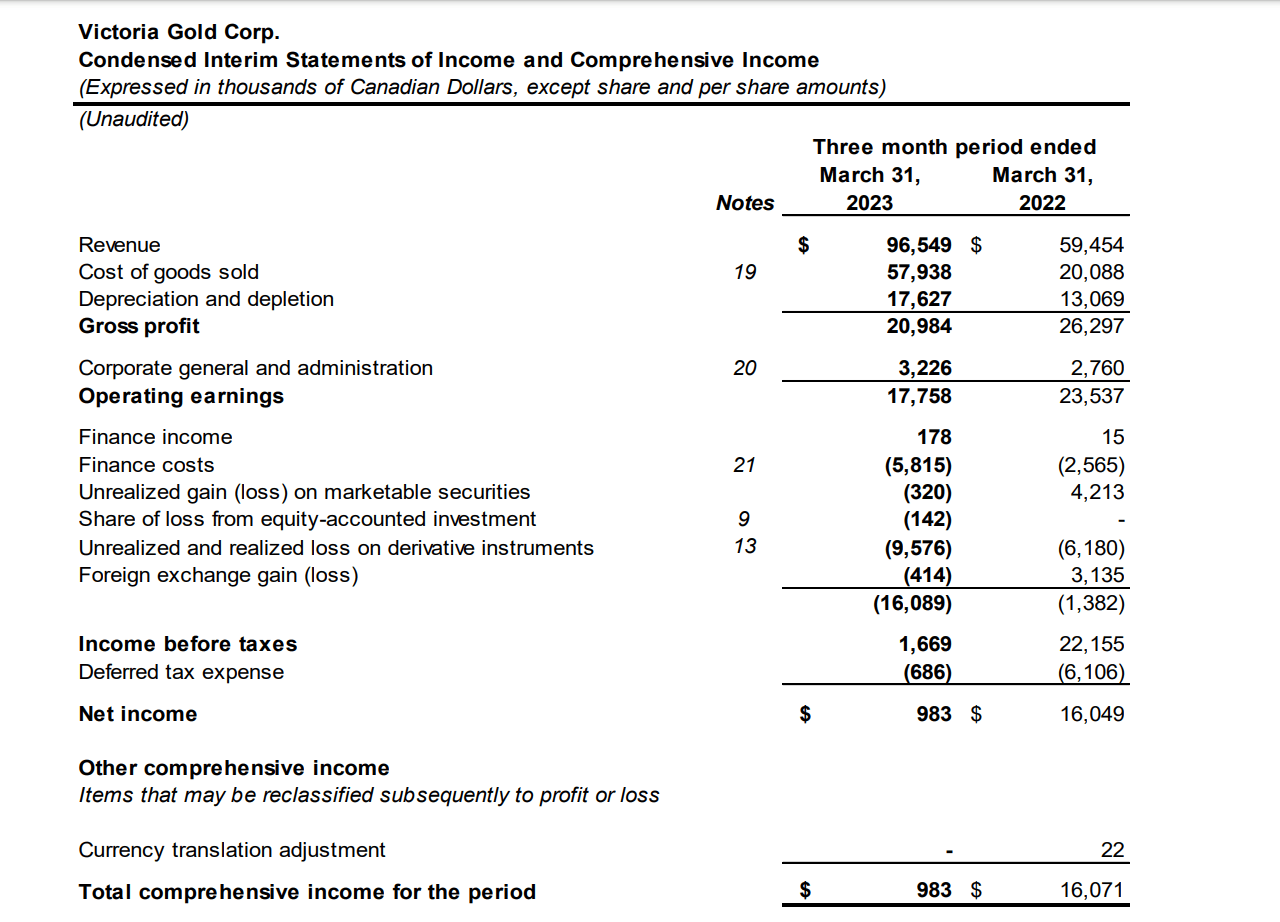

Victoria Gold ("Victoria") released its Q1 results last month , reporting quarterly production of ~37,600 ounces, a 54% increase from the year-ago period. This impressive performance was driven by a 138% increase in tonnes stacked on its heap leach facility (~2.09 million tonnes vs. ~0.88 million tonnes) at a higher average grade of 0.86 grams per tonne of gold. Meanwhile, tonnes of ore mined also increased materially, and waste mined was also higher, with the company benefiting from shorter waste hauls. This solid Q1 performance has set Victoria up to meet its FY2023 guidance of 160,000 to 180,000 ounces, with production sitting at 22.1% of its midpoint with the weakest quarter of the year in the rear-view mirror (coldest weather experienced in Yukon during Q1 leading to a seasonal dip in production). And this is certainly a much better start than the trailing-two-year Q1 output average of ~25,600 ounces, with its seasonal stacking strategy implemented successfully.

Victoria Gold - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

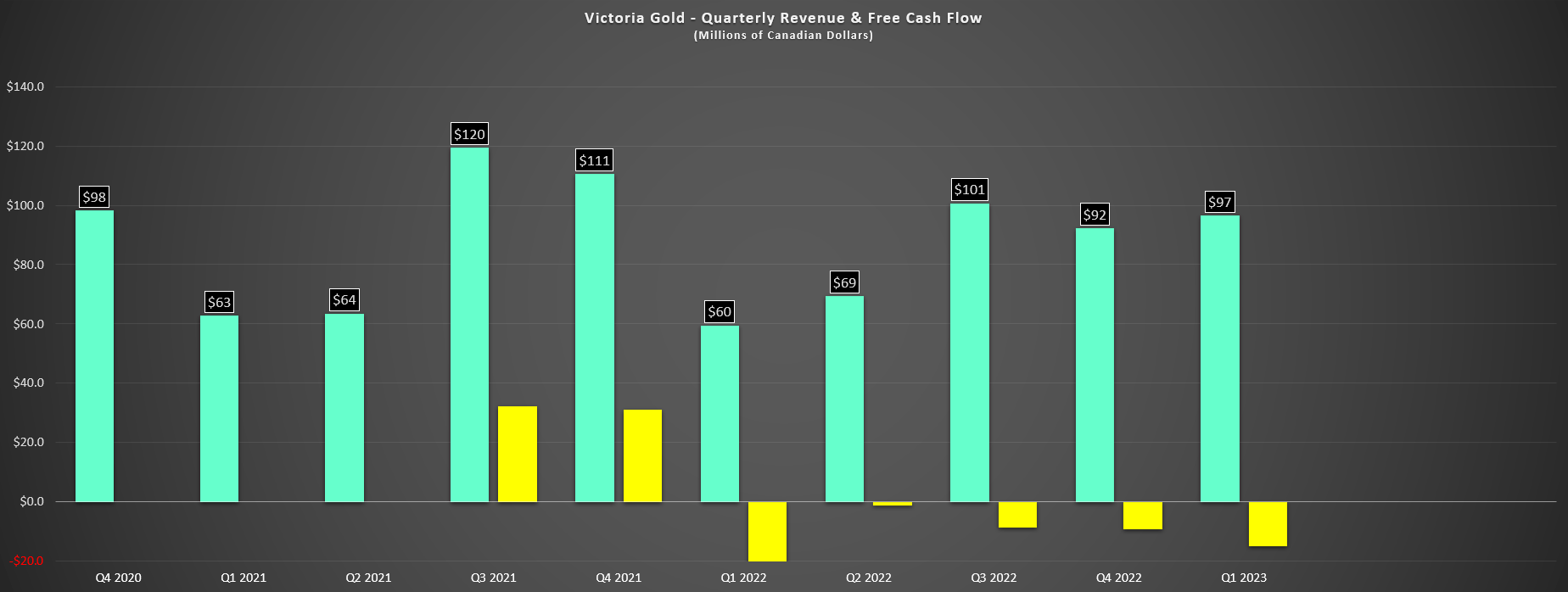

Given the increased production in the period from higher tonnes stacked and better grades, Victoria saw a material increase in revenue as well, benefiting from increased ounces sold (~38,200 vs. ~25,500) and a slight tailwind from the higher gold price of C$2,526/oz [US$1,867/oz]. That said, we continue to see free cash outflows with a cash outflow of C$15.1 million in Q1, albeit an improvement from the year-ago period (Q1 2022: C$40.0 million). The result was that Victoria ended the quarter with just C$23.6 million in cash despite drawing C$11.3 million on its debt. That said, the company remains in compliance with its covenants and its total debt remains manageable at ~$200 million vs. an estimated ~US$120 million in operating cash flow this year.

Victoria - Quarterly Revenue & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Looking out over the rest of the year, we should see production steadily increase as we've seen in past periods, and I wouldn't be surprised to see Victoria beat its guidance midpoint of 170,000 ounces, which would be a welcome development after two consecutive years of missed guidance. Meanwhile, from a cost standpoint, Victoria isn't likely to generate much free cash flow this year, but a return to positive free cash flow will also be a welcome development after an outflow of C$53.5 million in FY2022. That said, while the 2023 and 2024 results will be affected by increased waste tonnes mined, 2025 and 2026 are setting up to be phenomenal years, with average production of ~218,000 ounces and US$90+ million in free cash flow assuming a US$1,950/oz plus gold price, meaning that this story will pay off for patient investors.

Costs & Margins

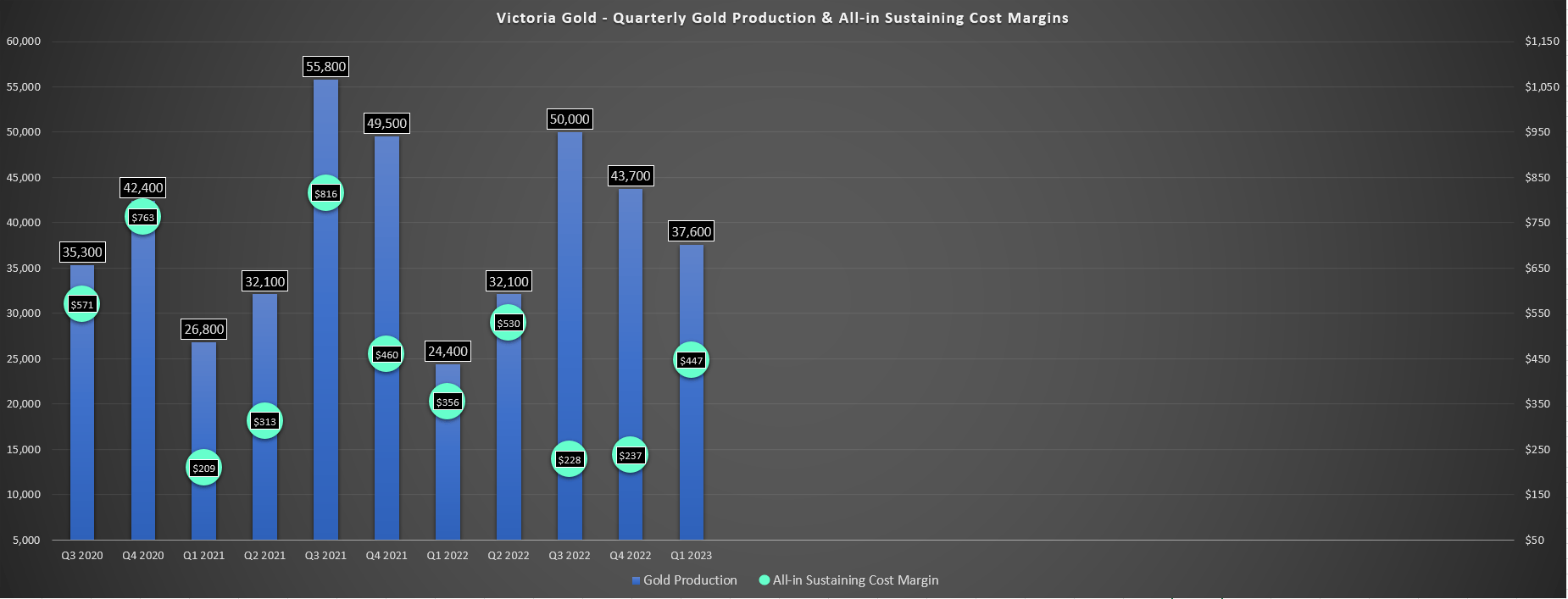

Moving over to costs and margins, Victoria reported all-in sustaining costs of US$1,420/oz in Q1 2023, a material improvement from US$1,504/oz in the year-ago period. Notably, this was despite inflationary pressures on a year-over-year basis and higher G&A expenses, partially offset by lower sustaining capital in the period and increased ounces sold. And when combined with a slightly higher average realized gold price, Victoria's AISC margins improved to US$447/oz, a 25% increase from US$356/oz in Q1 2022. Plus, given the lower oil price in Q2 2023 combined with a slightly higher average realized gold price, Victoria should see further sequential (Q2 vs. Q1) margin expansion. So, while Victoria's AISC margins may still be below the industry average, we're certainly seeing an improvement here.

Victoria Gold - Quarterly Production & AISC Margins (Company Filings, Author's Chart)

{kind=link}

Regarding sustaining capital, Victoria spent C$6.3 million in Q1 on capital component rebuilds on its mining fleet, upgrades and capital component rebuilds on its material handling system and the construction of the water treatment facility. However, it's tracking behind its FY2023 sustaining capital guidance on an annualized basis, suggesting that we could see elevated AISC continue in continue depending on the timing of sustaining capital spend. That said, the company looks to be in a position to easily beat its FY2023 cost guidance midpoint of US$1,450/oz, which is what's most important, and assuming AISC of US$1,405/oz and an average realized gold price of US$1,925/oz, Victoria would report more respectable margins of US$520/oz, up from US$333/oz last year.

Let's dig into the valuation and see whether the stock has moved into a low-risk buy zone:

Valuation

Based on ~68 million fully diluted shares and a share price of US$6.30, Victoria Gold trades at a market cap of ~$428 million, it continues to make Victoria one of the cheaper miners in the 180,000 to 200,000 ounce per annum producer space. And with the Eagle Gold Mine boasting an estimated After-Tax NPV (5%) of US$815 million at $1,850/oz gold (adjusted for continued inflationary pressures), the stock is certainly trading at a steep discount on a market cap to NPV (5%) basis. That said, even applying a 1.0x P/NAV multiple which is above where most junior producers (sub 200,000 ounces per annum) trade currently, and after subtracting out net debt of US$180 million and estimated corporate G&A of US$125 million, we can see that the discount is eroded materially.

{kind=link}

Using what I believe to be a conservative value of US$130 million for resources outside of reserves (Eagle/Olive [+] Raven), I see a fair value for Eagle of US$945 million (US$1,850/oz gold price). However, after subtracting net debt and corporate G&A, Victoria's fair value drops to US$640 million. If we divide this figure by ~68 million fully diluted shares, this translates to a fair value of US$9.40. Some investors might argue that including corporate G&A isn't necessary since a suitor is looking at the asset alone and debt obligations in a buy-out scenario. And while this is a fair point, I don't see Victoria being as likely a takeover target as I did pre-2022, with Eagle no longer offering margin expansion to potential suitors (AISC profile closer to $1,200/oz). And I would argue that suitors are looking for growth plus margin expansion, hence I don't see a high probability of Victoria being acquired, meaning that corporate G&A is relevant to the valuation and any fair value estimate.

Given that a US$9.40 price target implies a 49% upside from current levels, this might suggest that Victoria is worth investing in today. And while this might be a meaningful enough upside for some investors, I am looking for a minimum 40% discount to fair value to justify buying small-cap (and especially single-asset producers) given that they carry higher-risk. If we apply this discount to an estimated fair value of US$9.40, Victoria's ideal buy zone comes in at US$5.65 or lower. Hence, while the valuation is certainly more reasonable than it was six weeks ago above US$7.60 per share, I still don't see this as a low-risk buying opportunity. Plus, with the better years of the mine life still being 18 months away (2025/2026), I don't see any reason to rush into the stock now unless an adequate margin of safety is available (which would be present below US$5.65).

Summary

Victoria had a solid start to 2023 and is tracking well against its FY2023 guidance, which was certainly on the conservative guide, but understandably after two consecutive misses on guidance. That said, I prefer to buy turnaround stories when they're out of favor and at deep discounts to fair value, and while Victoria certainly has upside to fair value, I'm less confident that it's a takeover target with its updated cost profile, and I still don't see enough of a margin of safety just yet. Meanwhile, larger and more diversified producers are available at an even lower P/NAV multiple, like Pan American Silver (PAAS) which remains in the penalty box after two tough years. So, while I would consider starting a position in Victoria below US$5.65, I continue to see more attractive bets elsewhere for now.

For further details see:

Victoria Gold: Weakest Quarter Of Year In Rear-View Mirror