VITFF - Victoria Gold: Wildfire Evacuations Dent H2 Outlook

2023-09-01 13:46:34 ET

Summary

- Victoria Gold Corp. reported a record Q2 performance with 45,600 ounces of gold produced.

- Unfortunately, this didn't translate to much improvement in margins or free cash flow generation, and H2 will be softer than expected due to wildfire evacuations (since resolved).

- In this update, we'll look at Victoria's valuation and whether it's finally moved into a low-risk buy zone after its ~70% correction from its highs.

The Q2 Earnings Season was a disappointing one for the gold sector, with the record average realized gold price being offset by inflationary pressures plus one-time headwinds for several producers. The result was that we saw minimal margin improvement for most companies, and FY2023 all-in sustaining cost margins should come in nearly 35% below peak levels enjoyed in Q3 2020 (~$600/oz vs. ~$860/oz), which explains the ~35% correction we've seen in the VanEck Gold Miners ETF (GDX) since Q3 2020, especially after factoring in share dilution, the negative impact to NAV because of inflationary pressures, and the violent decline in free cash flow generation.

Fortunately, while Victoria Gold Corp. ( VITFF ) has consistently been producing at costs above the industry average and struggling to meet its guidance, the company reported a record Q2 in August, with ~45,600 ounces produced. However, the stock hasn't been able to hold on to its gains following two evacuations related to wildfires near the Eagle Gold Mine in central Yukon. And while this won't affect guidance, which has been maintained, it has flipped the script from a potential beat on output and cost guidance midpoints to a likely miss, with Victoria guiding for costs near the top end of guidance.

The silver lining is that mining activities are back on track with no disruptions since, which at least removes the uncertainty that was present in early August. Let's inspect the Q2 results below:

Eagle Mine Operations (Company Website)

{kind=link}

All figures are in United States Dollars unless otherwise noted with a C$ in front of the dollar figure.

Q2 Production & Sales

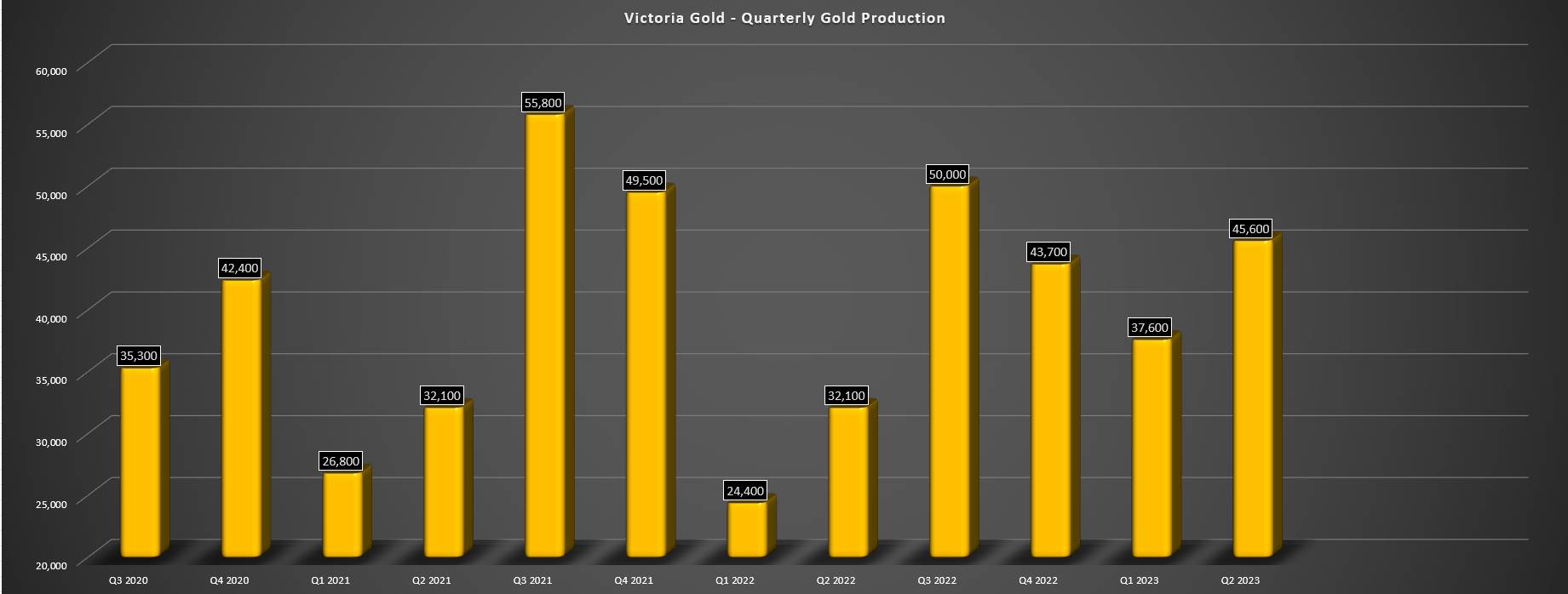

Victoria Gold released its Q2 results in August and reported quarterly production of ~45,600 ounces of gold, a record Q2 performance for the company. This was driven by year-round stacking and improved operating performance through the winter, which contributed to increased inventory on its heap leach pads. The result is that Victoria Gold has produced ~83,200 ounces year-to-date (56,400 ounces in H1 2022), and is tracking at ~49% of its annual guidance midpoint of 170,000 ounces, which would imply a beat on output given that production is usually back-end weighted.

Unfortunately, as noted above, this won't be the case because of the negative impact of the evacuations in late July and early August, with a total impact of nearly two weeks related to the stops and starts before the mine could ramp back up to normal operations.

Victoria Gold - Quarterly Production - Company Filings, Author's Chart

{kind=link}

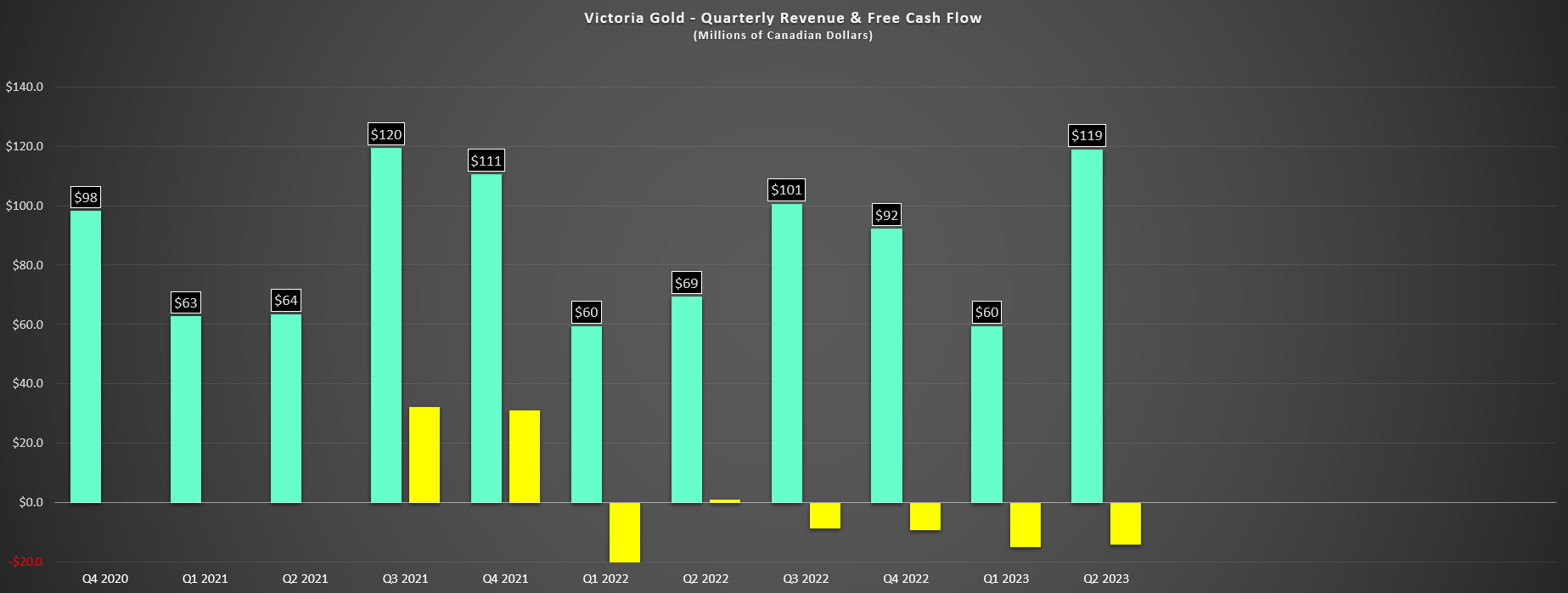

As for the results from a financial standpoint, Victoria Gold saw a 71% increase in revenue year-over-year, benefiting from a record average realized gold price of US$1,981/oz and higher ounces of gold sold in the period (~44,700 ounces). However, this unfortunately didn't translate to positive free cash flow, with adjusted free cash flow of negative C$13.5 million in Q2 2023, down from C$0.50 million in Q2 2022. Victoria's negative free cash flow in Q2 2023 was related to negative working capital adjustments, a C$13.4 million settlement of gold call options, offset by lower capital expenditures in the period (C$17.6 million vs. C$31.1 million). The result was that Victoria ended the quarter with just C$27.5 million in cash and ~C$186 million in net debt, leaving it with one of the weakest balance sheets among its junior producer peers.

Victoria Gold - Quarterly Revenue & Free Cash Flow - Company Filings, Author's Chart

{kind=link}

Costs & Margins

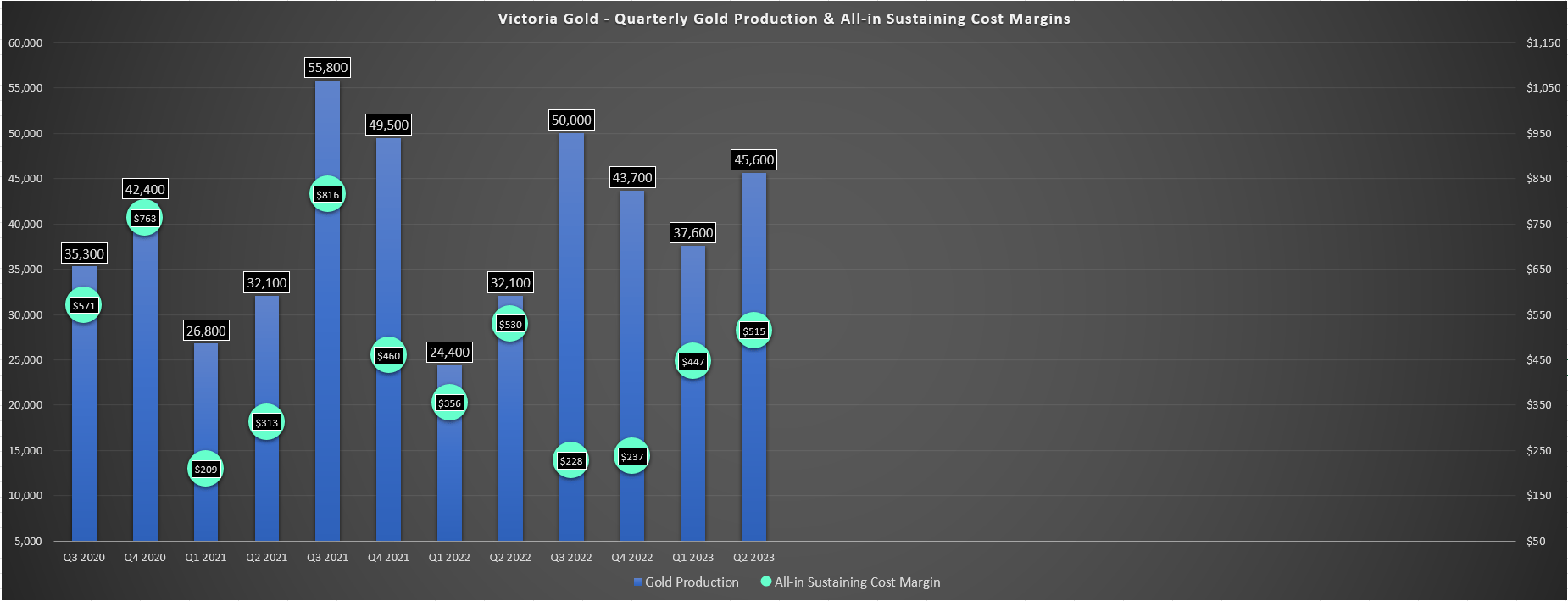

Moving over to costs and margins, the results weren't nearly as pretty as the record production with minimal improvement. This was evidenced by cash costs of $1,253/oz and all-in sustaining costs [AISC] of $1,466/oz in Q2 2023, which were both up sharply on a year-over-year basis. Regarding the ~7% higher AISC, this was despite the benefit of lower sustaining capital and an increase in ounces sold, affected by higher cash costs and increased corporate G&A. The result was that AISC margins actually fell year-over-year despite the record average realized gold price, with AISC margins of $515/oz, down 3% from $530/oz in Q2 2022. Victoria noted in its prepared remarks that while it has benefited from lower fuel costs, labor/contractor costs have remained sticky, consistent with what we've seen sector-wide.

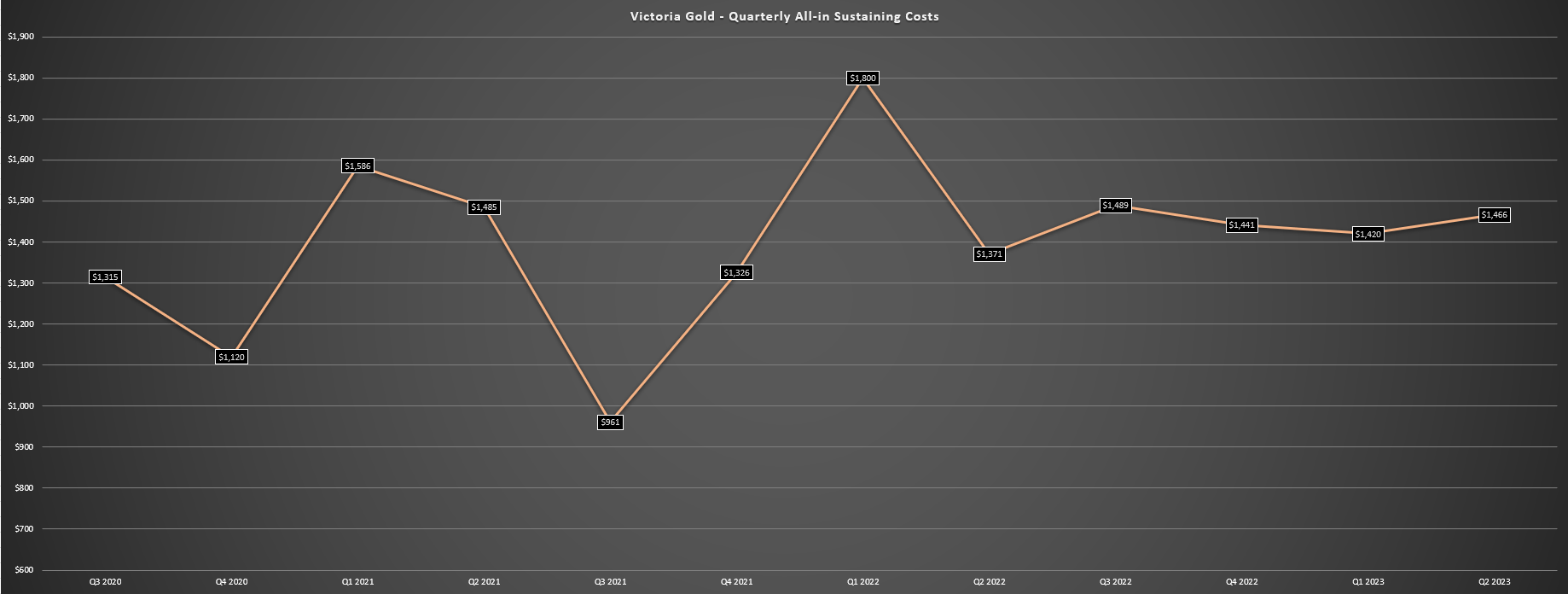

Victoria Gold - Production & AISC Margins - Company Filings, Author's Chart Victoria Gold - Quarterly AISC - Company Filings, Author's Chart

{kind=link}

{kind=link}

From a negative standpoint, all-in sustaining costs are likely to increase in H2 as implied by the company's guidance, with fewer ounces produced and sold than initially expected because of the disruption to mining activities in early August. Meanwhile, we have seen a rise in energy prices as of Q3, providing less of a tailwind than we saw in the first half of the year. That said, Victoria noted it is working on cost improvements, including drill/blast optimization for improved ore fragmentation, wider haul roads to reduce congestion, and reduced contractor support, assuming turnover levels improve, which is what was called out in the Q2 results. So, while I would expect AISC to come in above $1,510/oz this year and over 10% above the industry average, we should see Victoria's costs return to more respectable levels next year (sub $1,400/oz), especially if these initiatives can yield some minor gains.

Valuation

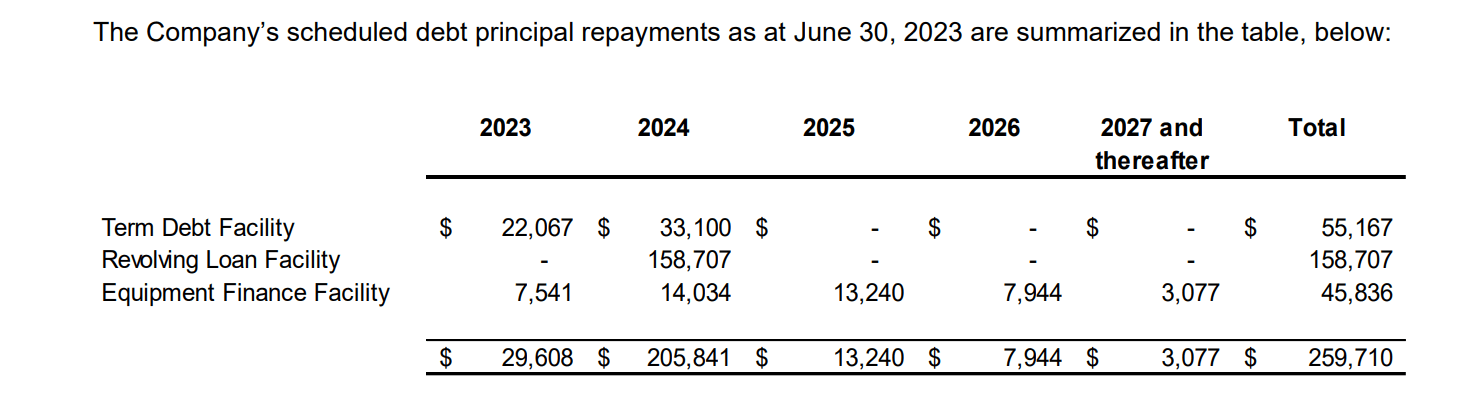

Based on ~68 million fully diluted shares and a share price of US$5.15, Victoria Gold trades at a market cap of ~$350 million and an enterprise value of ~$540 million, giving it one of the lowest market caps sector-wide among the junior producer space. This has come on the back of a ~72% correction in the stock since its all-time highs hit in 2021, with much of this correction being justified given the inflationary pressures that have put a severe dent in margins and NAV, the inability to deliver on guidance consistently, and its higher leverage relative to peers with just shy of $200 million in net debt. However, with the company set to generate upwards of $100 million in free cash flow in FY2025 using conservative gold price assumptions ($1,850/oz), much of this is becoming priced into the stock, with Victoria trading at just ~5x FY2025 EV/FCF.

Victoria Gold - Total Debt & Debt Repayments - Company Filings

{kind=link}

That said, the recent downside momentum in the stock has put a dent in its technical picture, with the low-risk buy zone dropping to US$4.65 vs. US$5.50 previously after the break of its previous low at C$6.56 (Q3 2022). So, while Victoria may check the boxes from a valuation standpoint, it is still a relatively high-risk bet within the gold space being a leveraged single-asset miner, a high-cost producer (making it more sensitive to gold price weakness), and it also being very sensitive to energy prices with Eagle being a low-grade and high-volume operation. Plus, while some producers have the benefit of being highly likely M&A targets if the weakness in their share price persists, I don't see Victoria Gold being a top takeover target given that most producers are looking for operations to improve their cost profile, and Victoria's life of mine costs are now only slightly below the industry average and in line with the mid-tier/major producer average after considerable inflationary pressures.

Summary

Victoria Gold Corp. had a solid H1, but its H2 results will come in softer than I expected because of two evacuations related to wildfires near the Eagle Mine. The good news is that the company has less seasonality in its business, so we won't see the usual drop-off from H2 to H1, it is seeing reduced turnover and working to drive cost improvements, and while 2023 will be another year to forget (~163,000 ounces at US$1,520/oz estimates), patient investors should a meaningful turnaround in costs and free cash flow post-2024 (similar grades at lower strip).

That said, while Victoria Gold Corp. is a solid name trading at a very reasonable valuation, I continue to see more attractive bets elsewhere, with similar FCF multiples available with higher quality mines and or producers with great diversification (lower risk relative to VITFF as a single-asset producer). In summary, I remain focused elsewhere, but would strongly consider Victoria Gold Corp. stock from a swing-trading standpoint at US$4.65 or lower.

For further details see:

Victoria Gold: Wildfire Evacuations Dent H2 Outlook