VRAY - ViewRay: Sales Order Momentum Ratcheting Higher

Summary

- ViewRay has continued growth in order momentum.

- Its stock price has moved sideways into the new year, adding another attractive entry point.

- Net-net, reiterate buy.

Investment Summary

Since our last publication on ViewRay, Inc. (VRAY) shares haven't repriced to the level anticipated, but have congested sideways into the new year. As to the investment thesis, VRAY's 8-K in January establishing its preliminary FY22' results add additional weight to growth levers discussed in our buy thesis [see: here ]. Our last 2x notes on VRAY clarified several points for observation, namely 1) top-line sales growth percentages; 2) backlog expansion and work-through; 3) market generated data for price visibility; 4) valuation upside.

Data: Author's last note on VRAY

As to our reiterated buy thesis today, quoting from the last report, it was clear several of these points pulled through again into Q4:

- Met FY22 revenue guidance

- Reversal in broad market positioning/tighter market breadth

- Backlog growth

- Supportive valuations

Looking over its preliminary accounts, MRIdian order momentum was up 28% YoY securing a 36.5% YoY upshift in the division's sales revenue, with >50% of these occurring in the final quarter. The Company also appointed William P. "Bill" Burke as CEO from January 9th, previously CFO of Haemonetics ( HAE ) and chief integration officer of Medtronic ( MDT ). With multiple crosscurrents leading into its FY22' earnings, we reiterate our buy thesis.

FY22' results preliminary analysis

The company's revenue ramp is steepening and with language in the pre-announcement and we hope to see this reflected vertically down the P&L in its FY22' numbers. We observed the following data points worth noting to our readers:

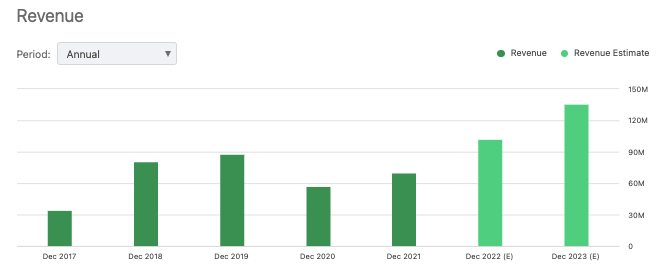

- With regards to quarterly revenue, we saw VRAY generate ~$35mm from the sale of 5 revenue units, ahead of the of 3 units in Q4 FY21'. Hence, order momentum is building, and added steam as the year progressed. This bodes in well for order growth into the new year, in our opinion. These growth rates were also carried through to the full year – VRAY generated $102mm in FY22' revenue from the sale of 16 revenue units, a 45% YoY gain. We look to this as positive affirmation of the company's growth model.

- Regarding the point above, when looking at order flow, VRAY experienced a substantial increase in its order acquisition, securing 9 new MRIdian system orders with a transaction value of ~$56mm in Q4. This compares to 7 orders at $41mm in the same quarter FY21'.

- Another supporting point was orders received for future delivery, that also lifted to a total of 32 by year's end [relative to 28 orders same time FY21']. Further weighting our buy rating, these results reflected in a significant rise in the company's backlog, which grew to $380mm, a $10mm increase from the last report.

- The company left the quarter with on-balance sheet cash and equivalents a $142mm by the end of the year. With respect to liquidity and cash burn, cash usage was estimated at ~$18 mm. Hence, we estimate VRAY's current position is sound, and it can continue allocating to its growth initiatives.

Exhibit 1. VRAY annual revenue ramp

{kind=link}

Data: Seeking Alpha, VRAY, see: "Revenues"

Additional catalysts for price change

We'd also point out three additional growth drivers in VRAY's engine noted early this year. The first , related to its order flow, announced that the University Hospitals Seidman Cancer Center ("UHSCC"), located in Cleveland, announced it will integrate the MRIdian MRI-guided radiation therapy system into its suite of treatment offerings. The deal is a master agreement that allows the centre to purchase up to 4 systems. Subsequently, UHSCC will be the first research and teaching hospital in Ohio to provide the MRIdian therapy to cancer patients across the region. In addition, we'd note the centre will collaborate with VRAY to conduct trials that compare the non-invasive MR-guided radiosurgery to traditional surgical methods and other treatments like HIFU, cryotherapy, and radiofrequency ablation, for a range of cancer sub-types.

Second, we noted that Chindex International ( CHDX ) also ordered 10 MRIdian systems. CHDX is a subsidiary of Shanghai Fosun Pharmaceutical, and we'd point investors to the fact MRIdian received regulatory approval in China in September FY22'. Subsequently the immediate uptake in orders illustrates demand in this region for the system and we'd look to this number adding to MRIdian's global installed base of 56 systems. Again, the tail of order momentum is building for VRAY and we estimate this to pull through to cash flow and the P&L throughout FY23'.

The above point rolls into VRAY's second update. It noted that results of its phase III MIRAGE RCT were recently published in The Journal of the American Medical Association ("JAMA") Oncology, providing further insights into the efficacy of MRI-guided stereotactic body radiation therapy ("SBRT") for the treatment of localized prostate cancer. We have been actively investing at several points along the prostate cancer treatment value chain, hence, this was an intriguing journal entry.

The trial, conducted by UCLA, enrolled 156 patients randomized to receive either MRI-guided or CT-guided SBRT. Results showed a significant reduction in acute genitourinary and gastrointestinal toxicity with MRI-guided therapy delivered by MRIdian compared to CT-guided therapy. Per Dr. Steinberg of UCLA noted, "this trial is the first phase III randomized controlled trial comparing MRI guidance to CT guidance in any disease site". Additionally, a higher percentage of patients experienced a reduction in urinary symptoms and bowel-related quality of life with MRI-guided therapy – a key differentiator from the current standard of care, where outcomes are often quite poor for patients.

Valuation and conclusion

Several factors feed into the valuation debate. First, is that sales and order momentum continue to garner for the firm. We've seen it grow top-line sales at 45% YoY and more than 100% from FY20, at a CAGR of 20% since FY17'. Hence, our comment that VRAY "isn't the same company it was 5-years ago" rings true here. That it trades at a 6.5% premium to its 5-year multiples at 9.2x trailing revenues rings true. We see sales growth ratcheting up this year and believe this continues to represent value for shareholders. At this multiple, we are still eyeing $5.20 from its FY22' numbers. This is supported by market generated data, that points to a $5.70 upside target on the point and figure studies below.

Exhibit 2. Upside targets to $5.70

Data: Updata

Net-net, we reiterate our buy rating on VRAY and welcome its upcoming FY22' earnings to scrutinize the 10-K in full. Nevertheless, it's clear sales and order momentum is inflecting higher, and this creates a strong tail of revenue growth for the company into this year. Rate buy at $5.20–$5.70.

For further details see:

ViewRay: Sales, Order Momentum Ratcheting Higher