EKTAY - ViewRay: Shares Crater As Company Warns Of Slower Growth Higher Cash Burn

2023-04-13 19:28:13 ET

Summary

- Magnetic resonance imaging-guided radiation therapy system provider ViewRay, Inc. has shocked investors with a severe revenue and cash flow warning.

- Expected 2023 revenue growth range slashed from a range of 25% to 40% to a new range of 0% to 15%.

- Company has experienced increased cash outflows with less than 12 months of liquidity remaining. As a result, ViewRay's upcoming 10-Q is likely to contain a going concern warning.

- Vastly reduced growth expectations might result in ViewRay violating debt covenants later this year.

- While the BoD has retained Goldman Sachs to evaluate strategic alternatives, an outright acquisition looks unlikely at this point. Given the company's mounting debt and liquidity issues, investors should avoid ViewRay's shares for the time being.

On Thursday, magnetic resonance imaging ("MRI") guided radiation therapy system provider ViewRay, Inc. ( VRAY ) or "ViewRay" shocked market participants with a severe revenue and cash flow warning (emphasis added by author):

Coming off a strong growth year in 2022, our innovation, clinical and commercial pipelines remain strong. The demand for MRIdian continues to be encouraging. However, the first quarter was hindered by global macroeconomic headwinds . The timing of new installations and the corresponding payment schedules have increased the need to extend our working capital balances. (...)

The Company is reducing its revenue guidance range to approximately zero to 15% growth for fiscal 2023 compared to its previous guidance range of 25% to 40% growth. The Company also updated its Adjusted EBITDA guidance range to a loss of $75 million to $85 million for fiscal 2023 compared to its previous guidance range of a loss of $70 million to $80 million.

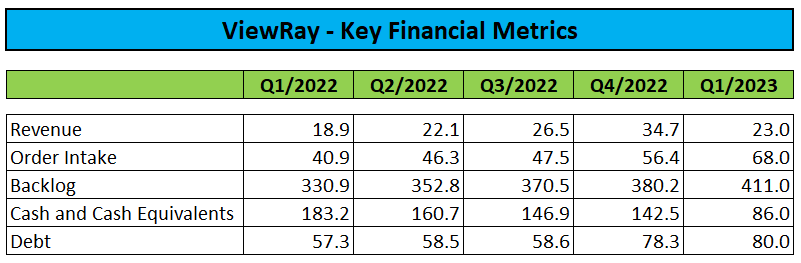

Cash usage in the first quarter of 2023 was approximately $57 million, primarily due to a working capital impact caused by delays in cash collections from international customers and outlays for inventory. As a result, we anticipate that our cash balance of $86 million will get us into the first quarter of 2024.

In response, the Board of Directors decided to retain The Goldman Sachs Group, Inc. ( GS ) as financial advisor " to undertake an evaluation of strategic alternatives, including a corporate sale, merger, or business combination. "

While the company has managed to increase backlog for its MRIdian system by almost 25% over the past twelve months, system implementation and related cash conversion remains way too slow to make ViewRay a viable business:

{kind=link}

In contrast, the company's sole competitor, much larger Sweden-based Elekta AB ( EKTAF , EKTAY ), or "Elekta," has been more successful in commercializing its competing UNITY radiation therapy system and recently achieved FDA clearance for a major upgrade to its offering. In addition, Elekta has ample financial resources to support further growth in this segment.

But ViewRay is not only about to run short on cash, the company might also face near-term debt issues as the terms of the company's secured credit facility with MidCap Financial Trust and the former Silicon Valley Bank require ViewRay, among other things, to maintain an undisclosed minimum net revenue threshold. Given materially reduced growth expectations, I wouldn't be surprised to see the company violating this covenant later this year.

Last month, the outstanding balance under the credit facility amounted to $80 million.

In addition, management will likely be required to include a going concern warning in the company's upcoming quarterly report on form 10-Q, as liquidity won't be sufficient to meet anticipated working capital needs, capital expenditures, and contractual obligations for at least the next twelve months.

Bottom Line

Given ViewRay, Inc.'s dire outlook and substantial, additional capital needs, it is difficult to envision an outright acquisition of the ailing company, not to mention a substantial premium to prevailing share prices.

At least in my opinion, the most likely outcome appears to be another, heavily dilutive capital raise of up to $100 million to provide for at least two years of additional runway based on the company's stated plans to decrease annual cash usage to a range of $25 million to $50 million next year.

Unfortunately, there's basically no way for the company to speed up system implementation and improve its cash conversion cycle in the current macro environment, so reductions in cash burn will have to come mostly from cost savings initiatives.

Should ViewRay, Inc. fail to find a suitor or raise sufficient capital, even a bankruptcy filing might be in the cards next year.

With an outright acquisition being an unlikely scenario and considering the company's mounting debt and liquidity issues, investors should avoid ViewRay, Inc. stock for the time being.

For further details see:

ViewRay: Shares Crater As Company Warns Of Slower Growth, Higher Cash Burn