SKYE - Village Farms Is Deep Value

Summary

- I have been following Village Farms closely since it entered the cannabis industry in 2017.

- I have been impressed by their execution in the Canadian cannabis market, but the company's other operations don't appeal to me.

- The company sold stock with warrants at a very low price, and the stock collapsed to a remarkably cheap price.

Village Farms ( VFF ) was trading near a multi-year low at a deep discount to its tangible book value this past week even at the price of $1.68 on Monday at the close, which was up 25.4% YTD. It priced a 18.35 million share unit offering on Thursday morning that sent the stock below $0.90 briefly in the pre-market. I owned a small amount in my Beat the Global Cannabis Stock Index model portfolio and more than doubled the position size to what is now, after a small rally, 10% of the model portfolio. In this piece, I discuss the company's operations and its financials and explain why I like the stock so much.

Operations

I started following the Canadian cannabis industry closely in 2014. Village Farms was kind of late to the game, announcing its entry into cannabis in June 2017. I didn't really like their plan initially, as they were partnering with a company I didn't care for, Emerald Health Care, which is no longer a publicly-traded stock after merging with Skye Bioscience ( OTCQB:SKYE ), formerly Nemus Biosciences and then Emerald Bioscience. Skye's CEO Punit Dhillon is the nephew of Avtar Dhillon, who was the founder and CEO at Emerald Health Care until he was later arrested and then convicted of securities laws violations.

The plan that Village Farms announced made little sense to me. Village Farms was aiming to be a very large greenhouse grower of cannabis, an area where Emerald Health Care had no experience. The goal was to be a low-cost producer in the country that was moving from a medical market to full adult-use. In my view, Village Farms picked a poor partner. Still, they have done very well in cannabis. In the first three quarters of 2022, they generated sales of $82 million from cannabis in Canada, up 18% from the first three quarters of 2021. The company operates Pure Sunfarms in 2 facilities in British Columbia, and it owns 70% of Quebec-based ROSE LifeScience. It now reports about 8% market share in Canada. The company owns 85% of Leli Holland, one of 10 companies with a Dutch Cannabis Supply Experiment production license, and it owns 12% of Altum International Hong Kong and Australia. In January, it began exporting to Israel from Canada.

I am not a fan of the company's other businesses. The company was originally a produce company, and the majority of its revenue is generated by this unit. That business isn't profitable even at the gross margin level. It has two other segments, including the tiny Energy and also "Cannabis - United States", which is CBD. I think that there are many investors who like the company's ownership of produce assets in Texas that could theoretically be converted to THC production, but I think that this is not likely in the near-term given that the Governor of Texas is so anti-cannabis.

You can learn more about the company in this presentation that they published this month:

Financials

Village Farms has decent financials in my view. The company generates slightly negative adjusted EBITDA but doesn't have a lot of debt. It has used cash to fund its operations in 2022. In the first three quarters, it used $13.2 million, which was an improvement from the $21.1 million it used in the first three quarters of 2021. It invested $12.9 million in the purchases of property, plant and equipment, down from $15.1 million in the first three quarters of 2021. At the end of Q3, the company had $43.8 million net debt, which is due primarily in 2024 and 2025.

The company generated total sales of $224.1 million in the first three quarters of 2022, up 15% from 2021. Canadian cannabis sales represented over 36% of revenue year-to-date and were 43% of Q3 revenue at $30.4 million. Adjusted EBITDA for the year has been -$18.4 million. In Q3, adjusted EBITDA was -$2.2 million, with produce at -$4.9 million but Canadian cannabis at $5.4 million. The company has shifted its business in Canadian cannabis from wholesale flower and trim towards retail, which was 81% of Q3 cannabis revenue, up from 59% a year ago. I would like to see its derivatives business do better, as it fell from 7% a year ago to just 4% in Q3.

The company had issued a prospectus, so investors shouldn't have been blindsided by a capital raise. Still, the offering was atrocious! They priced the deal with warrants at $1.35, up $0.01 from its year-end 2022 closing price and down more than 10% from its prior close the day before. From the $1.68 close on 1/23, the stock was priced nearly 20% lower. The $1.65 warrants that mature in 5 years were worth about $0.47-$0.57 at 40-50% volatility. The decline in the price of the stock after the pricing was almost as much as the value of the warrants issued.

Valuation

One of the reasons I included VFF in my model portfolio that I set up at the end of the year was that it's market cap then was just 0.6X tangible book value. While the company lowered the tangible book value per share with this offering, the large decline in the price leaves it at just 0.43X tangible book value. I think that the stock should trade at or above tangible book value, though there are some other large Canadian LPs that currently trade below tangible book value.

Analysts project that revenue in 2022 was $294 million, up over 9%. They forecast overall revenue will increase 12% to $330 million in 2023 and then by 9% in 2024 to $359 million. Adjusted EBITDA is expected to be -$20 million in 2022, ending years of profitability, but it is forecast to recover to $10 million in 2023 and $27 million in 2024.

As I look at year-end, I am expecting the Village Farms enterprise value to trade at 8X adjusted EBITDA projected for 2024, which would be $216 million. Adjusting for the cash and debt, this works out to be $1.58, short of the warrant exercise price but 61% higher. I think my valuation outlook may be conservative. 10X would convert the warrants and yield a price of $1.94, nearly a doubling of the price.

In my view, the company's produce unit is worth more than zero, but it doesn't resonate with investors. I think the company should separate it out, but that doesn't seem to be on management's agenda. The Canadian LP business is worth more in my view than the entire market cap of $107 million, which is less than 1X annual federally legal cannabis sales in Canada. The stock is very cheap.

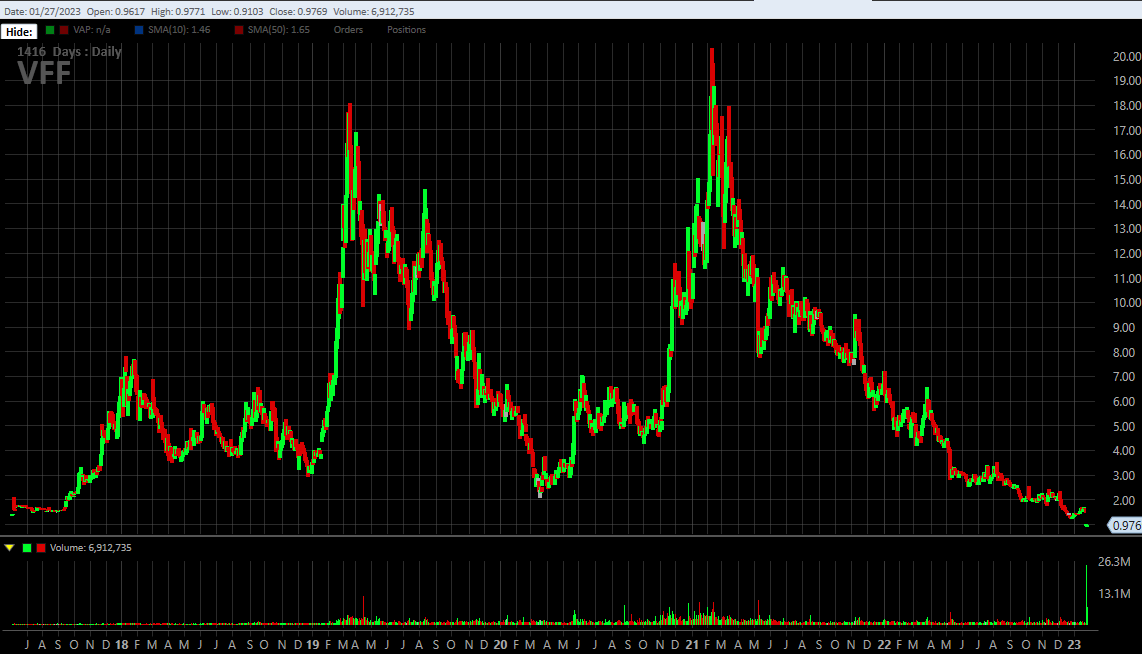

Chart

Village Farms was trading at $1.40 when the entry into cannabis was announced, and it now trades below $1 more than 5 years later:

{kind=link}

Charles Schwab StreetSmart edge

The price set a new low on the financing as a record number of shares traded the day of the pricing (with a high number the next day too). This price is down more than 95% from two years ago. It's possible that the buyers sold the stock just to keep the warrants, but it's more likely investors just concluded that the sale was very bad for the company's float, with shares outstanding increasing by 20% after a sale below tangible book value.

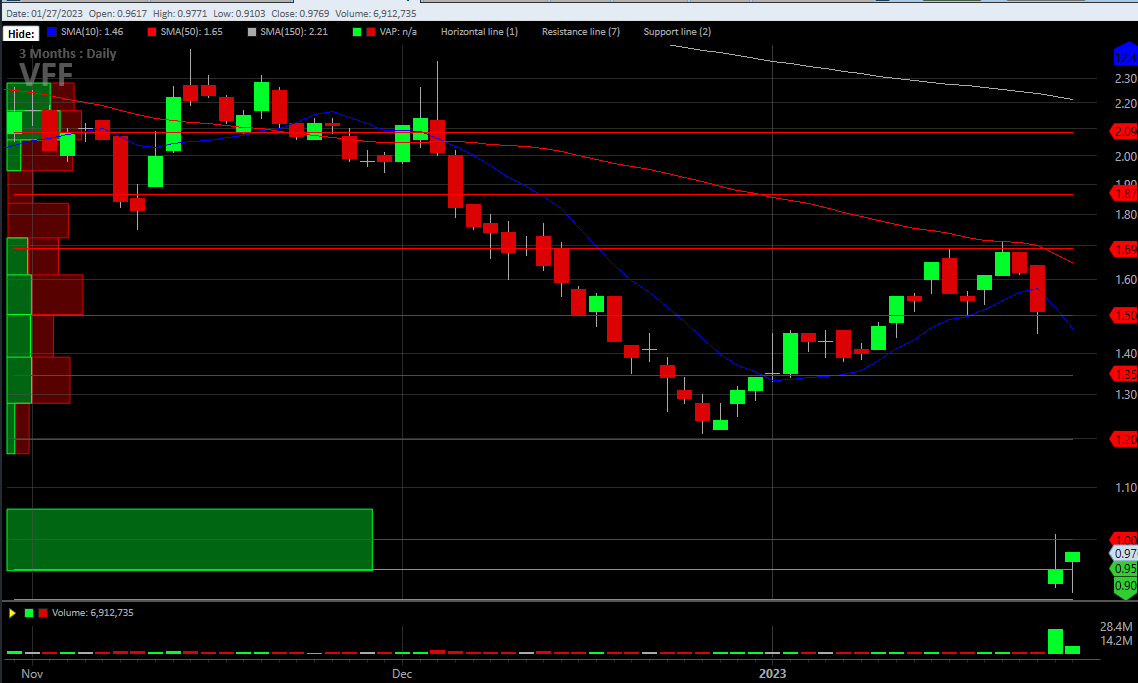

I believe that the company's financial health was fine and is now better, and the stock should recover to fill the entire gap. A return to its former multi-year low would offer more than 20% upside, but a complete gap fill would lift it 48% to $1.45, which is still very cheap in my view. A short-term chart shows the action more clearly:

{kind=link}

Charles Schwab StreetSmart edge

Conclusion

I think that Village Farms is very cheap. I thought so before the offering, but I had reduced my position size in my model portfolio. I see both fundamental and technical reasons to own it in size. The New Cannabis Ventures Global Cannabis Stock Index, up 7% in 2023 so far, includes Village Farms, which, after the decline, is only 2.7% of the index. I currently invest 10% of my model portfolio in this stock, and I think that it can recover a lot of its recent losses and 2022 losses as well.

For further details see:

Village Farms Is Deep Value