VMEO - Vimeo: A Buy In View Of Profitable Growth Low Debt And AI

2023-09-15 08:23:48 ET

Summary

- The video-sharing platform is currently facing a revenue growth problem.

- On the other hand, it is profitable, has generated cash during the last reported quarter, and has a healthy balance sheet.

- It also has a strong Enterprise business and recently launched an AI tool for improving customer engagement.

- There are risks too.

- The price target of $4.9 represents a trade-off between the opportunities and risks.

With revenues regressing since the middle of last year, video-sharing platform Vimeo's ( VMEO ) shares have gone south, and it now trades at around $3.89, or more than $50 below its 2021 peak of $57. This may be an opportunistic buy as this thesis aims to show, especially after the progress made on the profitability front despite evolving in a highly competitive industry.

Also, Vimeo has recruited a new CEO experienced in the SaaS business and developed an AI tool for creating videos, while, there has been an improvement in the consensus earnings estimate . However, I will also highlight risks and start with disaggregating revenues for the second quarter of 2023 (Q2) to identify a bright spot in the form of Vimeo Enterprise.

Going into Details

As per the table below , it is found that the Self-Serve & Add-Ons segment which constituted about 70% of overall revenues during Q2 has regressed by 9.5%. Another important segment, Other, which consists of the video-monetizing business like customers sharing their creations through internet-enabled TV apps like Magisto and Livestream against payment of a fee, has seen deterioration too. On the other side of the spectrum, the Vimeo enterprise appears as a bright spot and has grown by 31.7%.

SEC Filings (Seeking Alpha)

Now, Self-Serve essentially includes the company's subscription services (ranging from the starter, standard, and advanced plans) together with add-on fees like bandwidth services given that video unlike other media like text and image consumes much more internet capacity. This segment seems to have suffered as a result of marketers prioritizing more face-to-face meetings and physical marketing events after COVID-19 which reduces demand for video-related services, while at the same time, there is competition from the emergence of new platforms and services. Some of the most important are Wistia , BombBomb, Cincopa, Vidyard, Brightcove, CloudApp, and Hippo Video, just to name a few.

Furthermore, 28% of consumers globally were expected to cut down on their streaming expenses as per a study carried out in December last year due to inflation-led pressures facing household budgets. A more recent article comparing Alphabet's ( GOOG ) YouTube and Vimeo differentiates their revenue-generating models. Thus, while YouTube which is ad-based provides access to a massive user base, it is notorious for advertisements that pop up all the time.

On the other hand, while giving access to a relatively smaller user base, Vimeo gets revenues through subscriptions and has a privacy system in place whereby only certain users can view the content and there is a possibility to password-protect videos too. Noteworthily, it is these profiling and security features that explain the company's success in the corporate world, which is different from individual users where one uploads a video in the hope of being seen by millions.

Therefore, facing competition both from peers and a giant and in an industry where costs are high as there is a need to employ highly-skilled people while also investing in high bandwidth data center infrastructure, Vimeo's strategy to focus more on the Enterprise segment makes more sense than being involved in an unprofitable price war implying reducing costs to favor higher subscription volumes.

Emphasizing ARPU and Profitable Growth

Furthermore, founded in 2004 , or before YouTube , Vimeo has been able to gradually expand how customers make use of video products. Initially, from just uploading multimedia content, the company has put tools at the disposal of its subscribers the option to create, amend, and distribute videos. These tools have found traction in enterprises, often starting from the marketing and then moving on to the HR department before going to the finance department.

Talking finances, this strategy to focus on enterprises makes sense as it is more revenue-generating as measured by the ARPU (Average Revenue per User) as seen in the table below. Thus, ARPU figures for enterprises which are around $20K (average for the first and second quarters) are 100 times higher than for Self-Serve. In addition to squeezing more sales, enterprise bookings, which provide an idea of future sales, have also increased by 72%.

{kind=link}

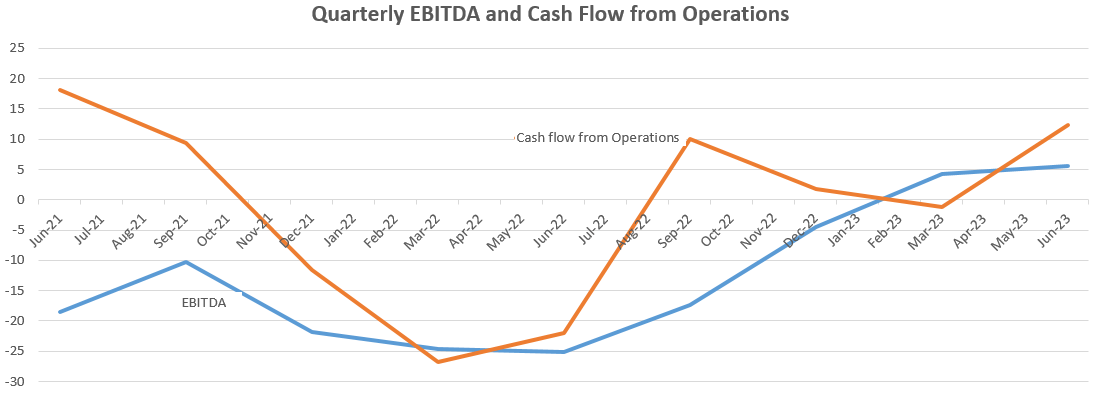

Shifting to profitability, with a gross margin in the 78% to 80% range during the last four quarters, this is a business whose platform approach demonstrates strong profit potential. However, diving deeper into the income statement, there are administrative expenses too, but the fact that these have been closely controlled has resulted in positive EBITDA numbers for the last two quarters as seen in the blue chart below.

Table Built Using Data From (Seeking Alpha)

{kind=link}

However, the upward trajectory is not likely to be sustained in the third quarter as about $2 million of expenses have to be effected earlier than expected, but still, full-year 2023 EBITDA guidance has been upgraded to $12.5 million (midpoint) from $7.5 million.

Valuing in View of Opportunities and Risks

As a result, the consensus EPS for fiscal 2023 has been revised higher from $-0.42 to $-0.07 , which represents a big improvement. Previous estimates put the figure at $-0.51, which means that analysts view the company as making significant progress on profitability.

Consensus EPS Revision (Seeking Alpha)

{kind=link}

Another factor that can help with better sales and profitability is the recent launch of the AI creation tool, whereby users can decrease the time it takes to create a video while making the process simpler too. In this case, by lowering the barrier to entry for creating and distributing videos, Vimeo could help democratize this medium of communication further while at the same time seeing more traction for its platform. Also, the tool using a prompt to produce a video script reminds us of OpenAI's ChatGPT way of functioning.

In this context, the company has already used analytics to learn viewers' preferences and communicate the information to its customers so that they can make appropriate decisions, but, according to research by Harvard Business Review , covering the impact of Generative AI on video platforms, "the economic impact will be huge". The study further adds that this will especially be the case for the vast majority of less popular content which goes unnoticed today and will get more visibility, aided by algorithmic recommendations as AI goes mainstream. Therefore, this looks to be advantageous to small players like Vimeo at the expense of giants like YouTube, who already have such tools in-house.

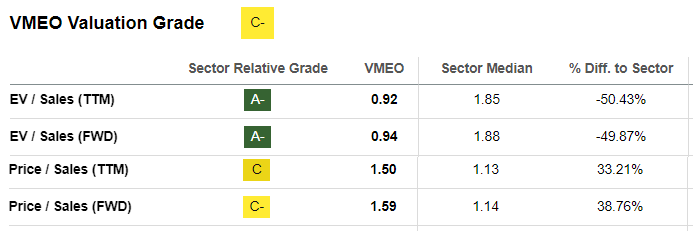

Talking valuations, the company looks overvalued based on the Price-to-Sales multiple of 1.5x . However, this is a comparison with the communication services sector, where according to my calculation, the average debt-to-equity ratio is 179.5%. In contrast, Vimeo's debt-to-equity is only 4% and the company had $278.4 million in cash at the end of Q2 compared to only $14.1 million in debt, which means that has a surplus of $264.3 million. This surplus also explains why its EV or Enterprise Value is less than its market cap since the debt is not included.

Valuations Grade (Seeking Alpha)

{kind=link}

Therefore, for a fair comparison that also considers the strength of its balance sheet, I consider the EV instead of the share price, which is related to the market cap. Thus, considering the forward of EV/Sales of 0.95x which is undervalued with respect to the communications sector by 50%, I have a target of $4.85 based on adjusting the current share price of $3.89 by 25%.

On a cautionary note after targeting a 25% upside, when you have a disruptive technology like ChatGPT which in addition to allowing people to generate insightful reports also enables them to create realistic images or videos, and, combined with the fact that OpenAI (the developer) makes its technology available through the cloud in subscription mode, you can expect other smaller companies to also take advantage of the opportunities. The result could be the emergence of a disruptor that enables video production to be accomplished in a much more autonomous mode, or a big one like YouTube reorienting its product mix to offer more targeted usage, thereby infringing on Vimeo's turf.

Therefore, be prepared for volatility, which could also occur when financial results for the fiscal year 2023 are announced in 2024. In this case, the estimated topline represents around a 5% decline from 2022, and some growth investors reminiscent of its double-digit historical performance may choose to dump the stock.

Justifying the Target Price

However, for those focused on the longer term, the management's objective is to achieve overall growth including for Self-Serve where stabilization has been noted as to the NRR (net revenue retention) on a sequential basis while for Vimeo Enterprise, it was over 100%.

Moreover, coming back to the profitable growth strategy, according to the new CEO, there are opportunities to integrate the Self-Serve segment with the Enterprise business. In this respect, based on his experience working at Salesforce ( CRM ) and Dropbox ( DBX ), the use of a self-service portal minimizes tickets or requests for support as the users themselves can solve the issue by browsing through troubleshooting videos or related articles on the subject. This frees up support agents' time to accomplish more productive tasks, and having users self-supporting themselves is also good for profitability.

Finally, the $4.9 target represents a trade-off between negative but profitable growth, investing in innovative AI, and showcasing a strong balance sheet to ensure that there is enough cash in case the transition period (to revenue growth) takes time. Additionally, as evidenced by the orange chart above, the company has managed to generate cash from operations in Q2, after a long streak of negative numbers.

For further details see:

Vimeo: A Buy In View Of Profitable Growth, Low Debt, And AI