VINP - Vinci Partners: A Differentiated Dividend Income Play

2023-08-19 03:50:45 ET

Summary

- Vinci Partners Investments Ltd (VINP) has been growing steadily in Brazil and offers a dividend yield of over 7%.

- The company operates in asset management and custody banks in Brazil and has seen impressive growth in assets.

- The CEO's remarks suggest positive market conditions and potential for higher dividends, making VINP an interesting hold.

Introduction

With operations in Brazil, Vinci Partners Investments Ltd ( VINP ) has been able to grow at a very solid rate over the last several years and has been dedicated to ensuring investors are getting a decent return. With the dividend yield at over 7%, I think investors are getting a very good deal here right now for holding shares.

VINP enjoys a similar valuation as major financial companies in the US does and is right now in my opinion at a very fairly priced level given the p/e of 10, but the book value is perhaps a little expensive, and until the company can grow the book value faster through more customer and client acquisitions then I don’t necessarily see it as a buy. Besides, given that the company is in Brazil, there is a currency hurdle that could hurt investors if there is a lot of volatility. However, with that, said, the dividend is too good to pass up on, and holding shares to extract and benefit from it seems like the most reasonable direction to go, rating VINP a hold.

Company Structure

As mentioned already, VINP operates in the Brazilian market of asset management and custody banks. The company has emerged very well over the last few years and the assets have grown by 78% annually in the last 3 years alone.

Interest Rates Brazil (tradingeconomics)

If you thought that the interest rates in the US were high, taking a quick look at Brazil should change your mind. They have very quickly increased the interest rates here, and they sit around the 14% mark. This has been very beneficial to VINP as the bottom line for the company continues to grow impressively.

As an asset management platform in Brazil, the company maintains a portfolio of private equity, infrastructure, real estate, and investment products as well. Founded back in 2009 the company has grown to a valuation of over $500 million.

Earnings Transcript

In the last earnings report by the company, the CEO Alessandro Horta had some good remarks worth including here.

-

“Vinci announced a quarter dividend of $0.20 on the dollar per common share. Over the last 12 months, we have distributed $0.73 per share as dividends that at the current stock price level represent a dividend yield close to 8%. Our fee related earnings totaling R$51 million in the quarter, or $0.94 per share, represented an increase of 11% year-over-year on a per share basis, driven by the ongoing fundraising across our private market vehicles and a higher contribution from advisor fees this quarter”.

This announcement is pushing VINP higher up as a dividend opportunity in my opinion. What would need to fuel higher dividends would be margin increases and a higher ROE than 18%. Historically the company has had a much higher ROE than that, so returning to that quickly would most likely result in both a higher share price and a higher quarterly dividend, both factors being very beneficial to shareholders.

-

“We are now entering a much more constructive scenario for Vinci to start seeing positive inflows into our liquid funds as local markets improve and the opportunity cost of a very high local interest rate lessens. On top of that, our public market vehicles, with the recent appreciation are trading at prices very close or above NAVs, which put us back in a position to raise capital through primary issuances. This contribution can be very meaningful to our numbers”.

Remarks on the conditions of the market were largely positive, and I think this further underscores that VINP might have a lot more to give still going forward. Raising capital to invest accordingly and drive higher equity returns are what I think makes VINP such an interesting hold right now still.

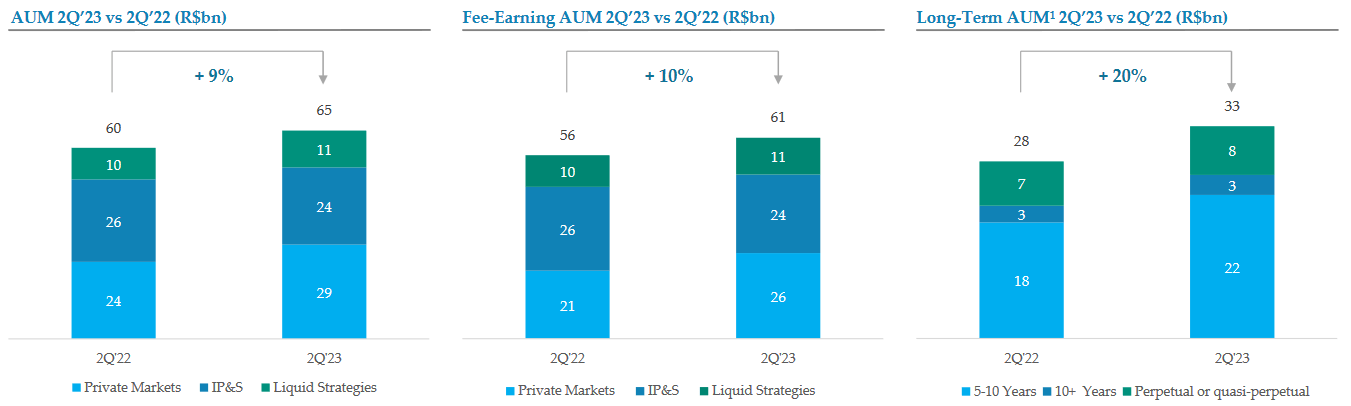

AUM Earnings (Investor Presentation)

Looking at the recent report as well, the company grew the AUM strongly at a 9% You rate and this ultimately resulted in DEPS growth of 18% YoY. The public market vehicles the company is engaging in also grew strongly at 20% just QoQ. All in all, the conditions look great for VINP and support the hold rating I have for them.

Valuation & Comparison

GGM Model (Author)

The GGM model above here very clearly showcases that VINP still is at an appealing price point to benefit and capture the dividend the company has and yield a strong return too. Despite the target price being above where it's now in 2023 I think there needs to be an improvement on the balance sheet and further growth of AUM before the p/b looks appealing enough. Sitting at nearly 2x is a hefty premium to pay still.

As for my projections, I think a yearly dividend growth of 8% is reasonable given the track record of the company and the fact they seem well on their way to growing ROE very quickly still.

Risk Associated

Lockup periods, or the absence of them, do pose an important risk of investing in VINP. In their 2022 Annual Report , Vinci underscored that a substantial 51% of their AUM is securely locked up for 5 years or more. This strategic move aims to ensure a stable foundation and consistency in their investment strategies. However, it's imperative to note that the remaining 49% of AUM doesn't adhere to a formal lockup structure, primarily concentrated within the IP&S segment.

{kind=link}

The absence of formal lockup in this 49% of AUM brings to the forefront an inherent risk—one that hinges on the vulnerability to sudden capital withdrawals by clients. In a scenario where clients simultaneously decide to pull out capital, the financial implications could reverberate significantly, particularly in terms of fee revenues.

Private equity stands as a formidable contender among various asset classes, vying for the attention and allocation of investor funds. However, it operates within an intricate ecosystem where competition from other investment avenues is undeniably prevalent. One such contender in this landscape is the realm of bonds, particularly when influenced by fluctuations in interest rates. If the interest rates in Brazil remain very high, the appeal of having to pay a high fee to financial companies like VINP isn't very high and keeping capital in relatively safe assets like bonds looks like a better option. AUM for VINP hasn't seen a decrease, but stagnation could be an indication that this trend is emerging.

Investor Takeaway

VINP is a solid business that has been growing impressively over the last several years, but what keeps me from rating it a buy is the high p/b right now for the company, nearing 2x. In comparison to the sector, that is a high valuation and one I would pass up on buying right now.

But with a fantastic dividend yield and one that sees sustainability and growing too, I think investors will be able to extract a lot of value here still through holding onto shares. Thai concludes to me rating VINP a hold right now, and potentially a buy if we see a significant correction in the share price, possibly reaching levels back in March of $8 per share.

For further details see:

Vinci Partners: A Differentiated Dividend Income Play