MMSC - Viper Energy Partners: Best Of Days Time To Look For An Exit

- Viper Energy Partners just declared a record quarterly distribution that, if continued, would see a very high near-11% yield.

- This was driven by their booming operating cash flow during the first half of 2022, which almost matched their entire full-year result during 2021.

- Whilst Viper Energy's unitholders are likely rejoicing, these are seemingly the best of days, and thus, after looking ahead, it now seems to be time to look for an exit.

- I do not expect oil prices to rally significantly higher for a prolonged time, and as a result, it seems their distributions are not likely to increase much higher, nor should their unit price rally much higher.

- I see no rush to sell, but at the same time, I feel it would be prudent to steadily unwind any significant investment, and thus, I believe that downgrading to a hold rating is now appropriate.

Introduction

Despite seeing a strong performance during the recovery of 2021, Viper Energy Partners LP ( VNOM ) was still held back by their hedges that created prospects for investors to grab a higher yield for 2022 thanks to their hedges rolling off, as my previous article highlighted. Since more than half a year has subsequently elapsed, it now feels timely to provide a refreshed analysis after they just declared a record quarterly distribution that, if continued, would provide a very high 10.93% yield.

Whilst VNOM unitholders are likely rejoicing for this cash windfall, when looking ahead, these are seemingly the best of days. Thus, in my eyes, it is now time to look for an exit.

Executive Summary & Ratings

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Author

*Instead of simply assessing distribution coverage through distributable cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and also best captures the true impact upon their financial position.

Detailed Analysis

{kind=link}

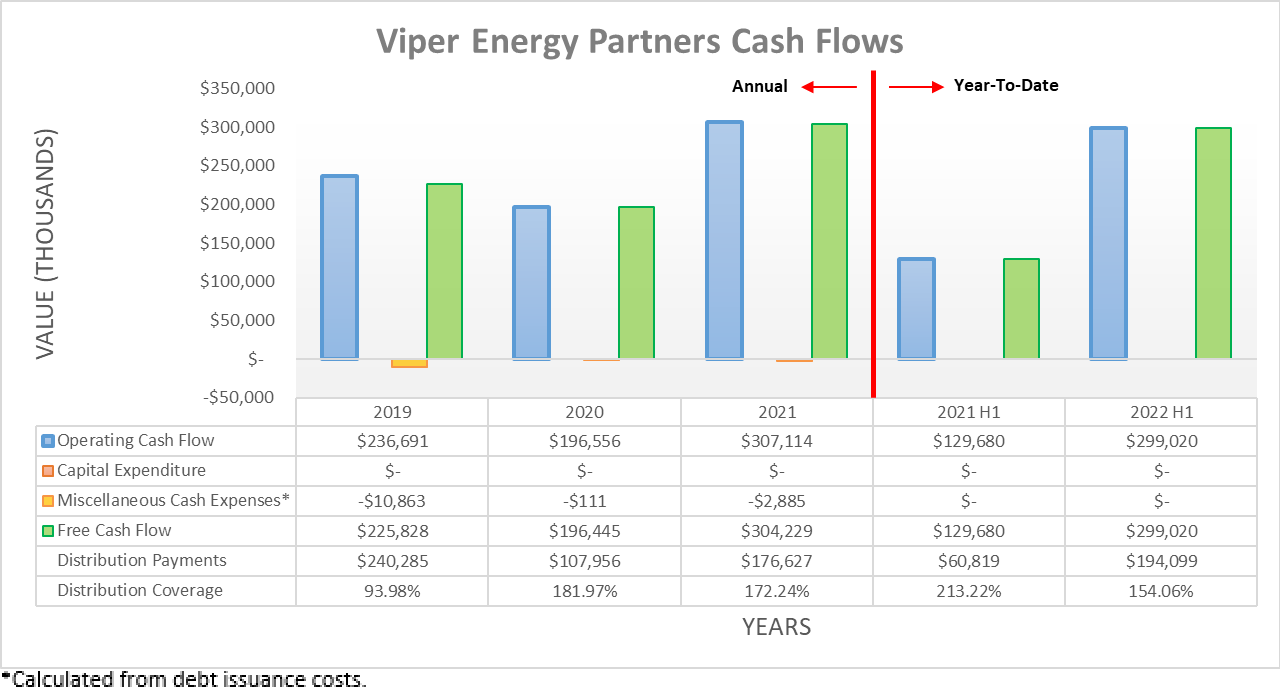

The benefits of these booming oil and gas prices are easily visible when reviewing their cash flow performance during the first half of 2022 with their operating cash flow of $299m almost matching their full-year result of $307.1m during 2021, despite obviously being only half the time. Thanks to their non-existent capital expenditure, this was entirely translated into free cash flow and saw management declaring a record quarterly distribution of $0.81 per unit along with a new tweaked unitholder returns policy, as per the quote included below.

"Additionally, the Company announced today that beginning in the third quarter of 2022, the Board of Directors of Viper's General Partner (the "Board") has approved a base annual distribution of $1.00 per common unit as well as a return of capital commitment of at least 75% of cash available for distribution. Viper's base distribution is expected to be supplemented by additional return of capital in the form of variable distributions and opportunistic unit repurchases. As part of this enhanced capital return program, the Board also increased the authorization of its common unit repurchase program to $750.0 million, up from $250.0 million previously."

- Viper Energy Partners, Second Quarter Of 2022 Results Announcement .

Overall, VNOM's new unitholder returns policy is not a complete day and night difference, as it remains variable to match at least 75% of their cash flow performance but now includes a base annual distribution of $1.00 per unit. Considering this only amounts to a low 3.33% yield on their current circa $30 unit price, I doubt it moves the needle in the mind of any investor. Meanwhile, they also appear to be taking more of an interest in unit buybacks after now increasing their authorization by another $500m, which I personally see as unappealing. This is because, given their variable approach to unitholder returns, they are very likely to be weighted towards their cyclical highs and thus higher unit prices. This negates their ability to create value for unitholders.

The bigger consideration in my eyes is VNOM's short to medium-term outlook going forwards, as these seem to be the best of days with the prospects of a recession lingering on the horizon and tentative signs of gasoline demand destruction already emerging. Admittedly, the International Energy Agency ("IEA") warned of further market tightness still to come regardless of these economic risks. However, whilst I do not expect oil prices to plummet, the probability of prices rallying significantly for a prolonged length of time appears rather low given these risks on the horizon.

Even though every oil and gas company is a proxy for oil and gas prices to some extent, when it comes to mineral rights partnerships, I feel this dynamic is at its highest level. Unlike supermajor oil and gas companies, such as Shell ( SHEL ), VNOM does not invest to grow clean energy operations, refining and chemical production, or even a service station network. They merely act as a distribution post-box that collects money from their mineral rights and passes it along to their unitholders. Whilst there is nothing necessarily wrong with this method, it nevertheless means that unless oil prices rally higher for a decent length of time, they are unlikely to surpass these record distributions nor see their unit price rally significantly higher.

When looking elsewhere, VNOM's cash flow performance was not materially constrained by hedges during the first half of 2022, unlike during 2021, as my previously linked article discussed. During the first half of 2022, their cash flow statement alludes to a $17m payment for hedging derivatives, which equals only 5.69% of their $299m of operating cash flow. This pales in comparison to the equivalent $35.9m they saw during the first half of 2021 that amounted to a staggering 27.68% of their $129.7m of operating cash flow. Whilst obviously positive, it also means that they no longer have prospects to see significantly stronger financial performance just by simply waiting for their hedges to keep rolling off in the future.

{kind=link}

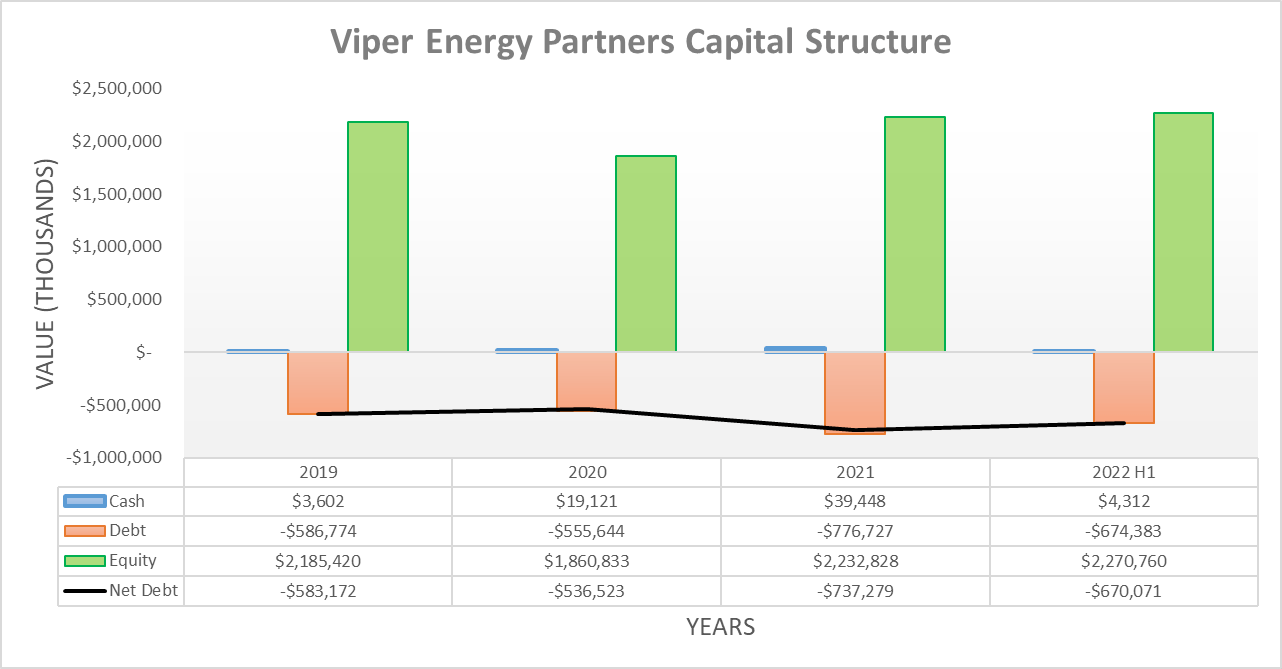

After funding their Swallowtail acquisition in the fourth quarter of 2021, VNOM ended the year with net debt of $737.3m and thus materially higher than its previous level of $536.5m when 2020 ended. Due to their booming cash flow performance during the first half of 2022, it subsequently decreased to $670.1m, which is modestly lower but still materially higher than the $522.9m when conducting the previous analysis following the third quarter of 2021. Meanwhile, their cash balance of $4.3m is on the low side historically speaking, versus where it ended 2021 at $39.4m.

{kind=link}

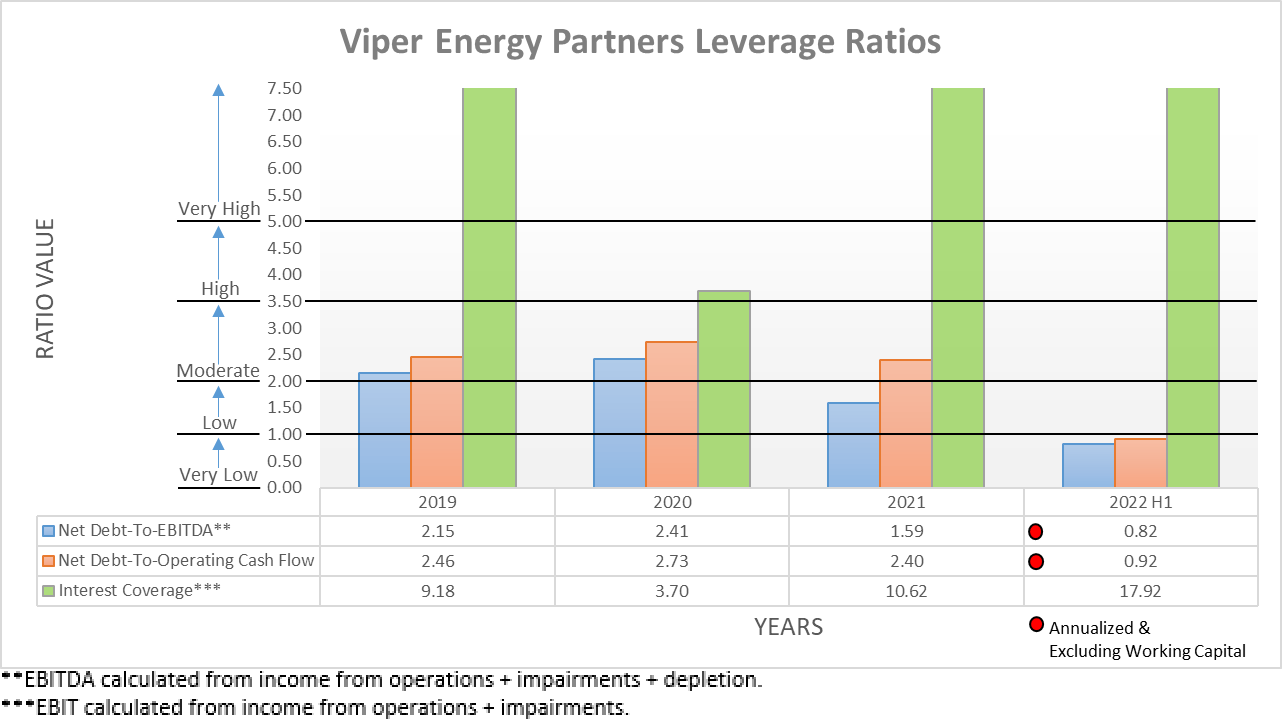

Even though their net debt increased materially during 2021, their leverage was kept in check, with their net debt-to-EBITDA and net debt-to-operating cash flow ending the year at 1.59 and 2.40 respectively. Following their booming financial performance during the first half of 2022 and modestly lower net debt, unsurprisingly, these slid significantly lower to 0.82 and 0.92 respectively, which now reside beneath the threshold of 1.00 for the very low territory. When looking ahead, their leverage will continue fluctuating, as oil and gas prices drive their financial performance up and down. Given as these are seemingly the best of days, the probability is more skewed towards the latter, and thus, by extension, skewed towards their leverage edging higher, all else being equal. Thankfully, even if their earnings were literally demolished by two-thirds, their net debt-to-EBITDA would still be less than 3.00 and thus within the moderate territory of between 2.01 and 3.50. Whilst this sees no material solvency risk, it still does not negate the fact that softer earnings would foretell lower distributions and thus very likely a lower unit price.

{kind=link}

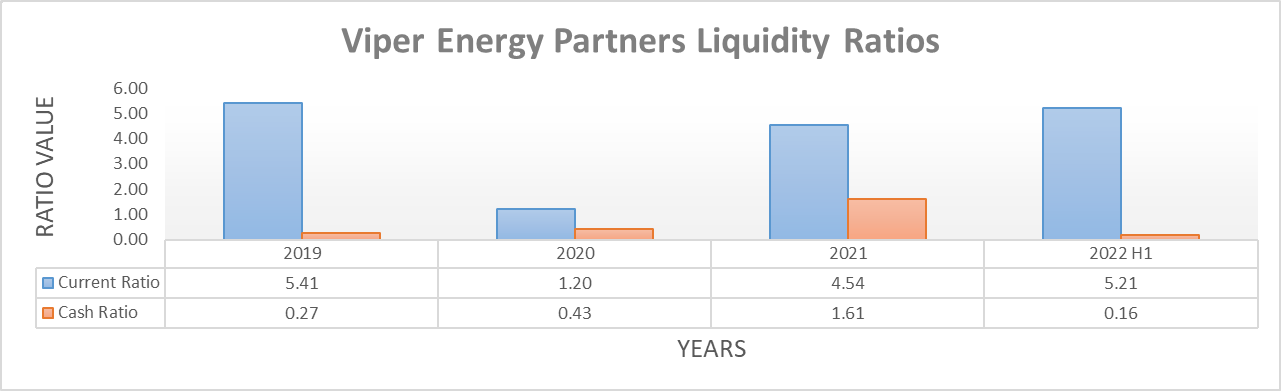

Even though VNOM's cash balance is on the low side, historically speaking, thankfully it does not materially hinder their liquidity with their current ratio at 5.21 sitting near its highest point in recent history, which clearly points to strong liquidity. Plus, their cash ratio of 0.16 is supported by a further $250m of availability under their credit facility that does not mature until 2025 with their other larger debt maturity not occurring until 2027, as the table included below displays.

Viper Energy Partners 2021 10-K

Conclusion

Even though the outlook for oil and gas prices is supportive, given the risk of a recession and tentative signs of demand destruction, the scope for sustained higher prices seems limited, barring another unexpected geopolitical shock. Since VNOM sports a variable distribution policy, by extension, this means that the scope for sustained higher distributions and unit price also seems limited. Thus, I believe that downgrading my previous buy rating to a hold rating is now appropriate. This is not to suggest that unitholders should rush to sell their holdings, more so, it suggests steadily unwinding any significant investment during the second half of 2022 because these are likely the best of days.

Notes: Unless specified otherwise, all figures in this article were taken from Viper Energy Partners' SEC filings , all calculated figures were performed by the author.

For further details see:

Viper Energy Partners: Best Of Days, Time To Look For An Exit