VNOM - Viper Energy Partners: Good Income But Still Not A Fan

2023-04-27 20:54:01 ET

Summary

- In February, Viper Energy Partners, an MLP of Diamondback Energy, announced a Q4 (base+variable) distribution of $0.49/unit.

- Annualized, that equates to a 6.9% yield given Thursday's close of $28.43. However, investors should consider that oil and gas prices have weakened from Q4.

- Meantime, distributions would have been considerably higher had VNOM not been spending unitholder capital on buybacks as compared to distributions directly into unitholders' pockets.

- There are certainly worse investments than VNOM in the energy sector, but there are better investments as well. Including the GP itself: FANG.

Last August, I recommended investors sell Viper Energy Partners, LP ( VNOM ) and buy its General Partner, Diamondback Energy ( FANG ) instead. See: VNOM Emphasizes Buybacks Over Distributions (Not A Fan) . Since that time, FANG has outperformed VNOM by 14% - not too bad. But that's looking backwards. Today I'll take a look at VNOM's most recent earnings report and the LP's prospects going forward. I also will take a look at what VNOM investors can expect in terms of shareholder returns (i.e. the distributions and share buybacks), and the allocation of shareholder capital between the two.

Investment Thesis

VNOM is a Permian centric royalty lease owner and receives income from operators that produce oil and gas on its leasehold. Diamondback Energy, the GP, is the primary operator, but third parties also operate wells on VNOM's lease.

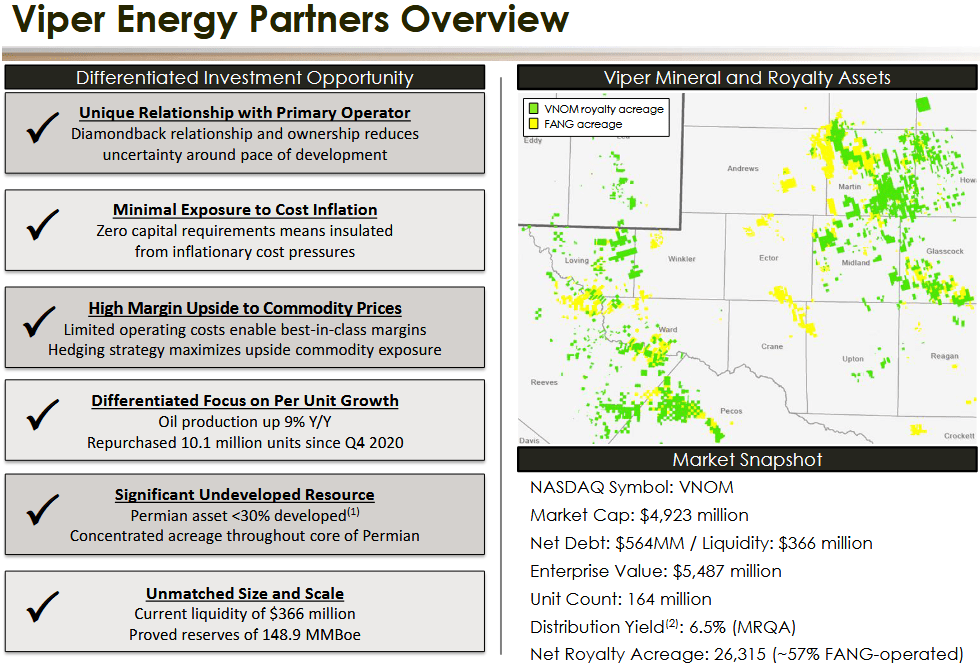

The slide below was taken from VNOM's Q4 Earnings Presentation and is an excellent overview of the LP:

{kind=link}

Viper Energy Partners

As can be seen in the graphic, the primary operator (57%) is VNOM's General Partner: Diamondback Energy. And, as the old saying goes, an LP is only as strong as its GP. Diamondback has demonstrated, for years now, that it's a top-tier producer in the Permian Basin.

As also shown in the graphic, VNOM is structured such that it has limited capital requirements, has a large resource base (148.9 million boe), and less than 30% of its leasehold has yet to be developed. Of the proven 148.9 million boe, 53% is oil, and 72% are PDP (proved, developed, producing).

As a result, VNOM is in an excellent position to reward shareholders based on the royalty income it receives from oil and gas production on its leasehold. With that as background, let's take a look at VNOM's latest earnings report and what investors might expect going forward.

Q4 Earnings

VNOM announced its Q4 and full-year 2022 results in February, and it was a relatively strong report:

- Q4 2022 average production was 34,935 boe/d (19,978 bpd oil), an increase of only 1% from Q3 2022, but +9% yoy.

- Q4 2022 consolidated net income (including non-controlling interest) was $145.2 million; net income attributable to Viper Energy Partners LP was $21.7 million, or $0.29/unit. That was down from $0.50/unit in the year earlier quarter.

- Q4 2022 cash available for distribution to Viper’s common units was $66.4 million, or $0.91 per common unit.

Viper’s Q4 average un-hedged realized prices were $83.30 per barrel of oil, $3.74/Mcf of natural gas, and $25.65 per barrel of NGLs, resulting in a total equivalent realized price of $57.92/boe.

The average hedged prices were generally lower: $82.71 per barrel of oil, $3.03/Mcf of natural gas and $25.65 per barrel of natural gas liquids, resulting in a total equivalent realized price of $56.66/boe.

Shareholder Returns

For Q4, the company announced a (base+variable) distribution of ($0.25/unit+$0.24/unit), or a total of $0.49/unit, both of which were payable on March 10.

Also during the quarter, VNOM repurchased 1.0 million common units for $31.7 million. That equates to an average price of $32.40/unit. The units closed today (Thursday, April 27) at $29.28. And this is exactly what I was warning investors about in my last article: energy companies have a long history of over-emphasizing share buybacks during commodity price up-cycles, when the share price is relatively high.

During Q4, VNOM's shareholder returns were allocation as shown below:

- Q4 Unit Buybacks: $31.7 million

- Q4 Total Distributions to LP unit holders: $35.7 million

That doesn't look too bad for public unitholders. That is, until you consider that the average number of fully diluted units outstanding actually increased from 68.39 million at the end of FY2021 to 75.68 million at the end of FY2022. The average number of fully diluted units at the end of Q4 was 73.88 million.

As the chart below shows, the $14.1 million shown for unit repurchases in Q4 only reflect the percentage of capital relative to public unit-holders. In other words, of the $31.7 million spent on unit buybacks in Q4, $17.6 million - more than half of the total, was to the benefit of the GP, Diamondback Energy, which owns a proportional number of the outstanding LP units.

Viper Energy Partners

Regardless, the payout ratio for public LP unitholders was 75% of the $66.4 million distributable cash that was available to them. Still, the repurchases don't seem to be benefiting the public unit-holders as much as distributions directly into their pockets would be.

Lease Developments

During the year, Viper divested 1,099 net royalty acres of non-core assets. That included divestiture of VNOM's entire position in the Eagle Ford Shale, which equated to 681 net royalty acres of third party operated acreage.

For full-year FY2022, Viper acquired 375 net royalty acres for an aggregate net purchase price of ~$65.9 million. Of those acres, ~254 net royalty acres are operated by Diamondback - a good percentage in my opinion.

Proved reserves at year-end 2022 were 148,900,000 boe (79,004,000 bo). That represents a 16% increase yoy. The year-end 2022 proved reserves have a PV-10 value of ~$4.1 billion.

Net proved reserve additions of 33,294,000 boe resulted in a reserve replacement ratio, or RRR, of 271%. The organic RRR was 280%. The robust reserve replacement bodes well for VNOM unitholders going forward.

2023 Production Guidance

Viper released the following production guidance for FY2023:

Viper Energy Partners

(Note: annotations in red by the Author)

As can be seen, VNOM management expects the midpoint of average daily production to grow 8% yoy and the company has a clear line-of-sight for ample future well development over the coming quarters based on operators' schedules and permits. At the time of the presentation, there were 44 rigs working across Viper's leasehold.

So far, the outlook for the price of oil in the Permian Basin (i.e. WTI), this year is highly uncertain in my opinion, and has generally been trending lower since last summer, but appears it may be trying to make a bottom:

MarketWatch

As you can see, the current price of WTI is considerably less than the average (after hedged) price that VNOM realized in Q4 ($82.71/bbl). That being the case, VNOM investors will likely see a reduction in the Q1 FY23 variable distribution.

I said that the WTI outlook was uncertain because the market seems to be pinging back-n-forth between a potential lack of supply later this summer during peak driving season, and concerns about a possible recession and a fall-off in demand. Honestly, your guess is as good as mine as to how it all works out.

On natural gas in the Permian (Waha), I'm more confident about the outlook and am downright bearish. As I mentioned in a previous Seeking Alpha article published in March, the outlook for Waha gas is poor given that associated gas production in the Permian (and elsewhere) keeps growing, while no new LNG export capacity is due to come online until next year. As a result, and in my opinion, the price of Waha gas could go negative again this year. See The Demise of NYMEX Gas (Not To Mention Waha) . Indeed, despite the naysayer comments left to that article and my opinion, note that the ( UNG ) ETF is down 20% in less than two months since it was published.

Risks

Obviously the greatest risk to a royalty taker like VNOM is the price of oil and gas that the royalties are based on.

As for the balance sheet, VNOM's is strong. As of the end of 2022, the LP had net-debt of $564 million and a net-debt to TTM EBITDA ratio of only 0.7x.

Summary and Conclusion

VNOM is a quality LP, and its GP - Diamondback Energy - is a top-tier Permian operator. However, as I have written many times on Seeking Alpha over the years, MLPs are typically and inherently designed to be of benefit to the GP at the expense of LP unitholders. I believe that is the case with the FANG/VNOM MLP, and continue to recommend investors own FANG stock rather than VNOM units. FANG has outperformed VNOM since my last Seeking Alpha article on the LP, and I believe that will be the case again for full-year 2023.

I'll end with a 10-year total returns comparison of VNOM the LP vs. FANG the GP, and just for added perspective, I added in the broad market averages as represented by the Vanguard S&P 500 ETF ( VOO ) and the Invesco Nasdaq-100 Trust ( QQQ ):

As clearly shown in the graphic, and while there's a need for income in a well-diversified portfolio, there's also a need to be long equities through the broad market averages.

For further details see:

Viper Energy Partners: Good Income, But Still Not A Fan