VNOM - Viper Energy: Projected 2023 Distributable Cash Flow Remains Strong Despite Low NG Prices

Summary

- Viper has no Henry Hub hedges for 2023. It does have a large amount of Waha basis hedges though.

- Around 21% of Viper's production is natural gas compared to 58% oil.

- Thus, its projected 2023 distributable cash flow has only been reduced by a few percent compared to November despite a sharp drop in natural gas price expectations.

- Royalty companies are escaping the impact of the significant service cost inflation compared to a couple years ago.

Viper Energy Partners ( VNOM ) still looks capable of generating around $3.41 per unit in distributable cash flow in 2023 despite a significant reduction in 2023 natural gas price expectations over the last few months. Viper does not have any Henry Hub hedges, but it at least has a large amount of Waha basis hedges.

As a royalty company, Viper isn't directly affected by service cost inflation, and I'd estimate that its margins (not including cash income taxes) improve by around $5 per BOE more than an upstream company such as Diamondback in a move from $60 WTI oil to $80 WTI oil.

I remain moderately positive on Viper at its current unit price. It is trading at pretty close to fair value for a long-term $75 WTI oil scenario, but is also capable of delivering an 11% distributable cash flow yield for 2023 at current strip.

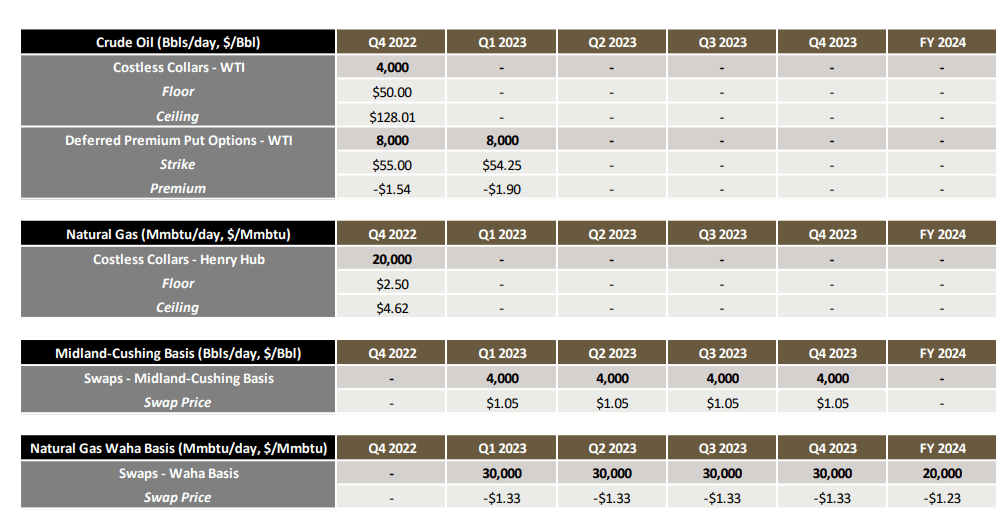

Viper's Hedges

At last report, Viper had a limited amount of 2023 hedges. It has deferred premium put options for Q1 2023 that look to be well out of the money, and the deferred premiums add up to approximately $1.4 million. Other than that it has some basis hedges, including around 65% of its natural gas production covered with Waha basis hedges at negative $1.33.

{kind=link}

Viper is still exposed to fluctuations in Henry Hub prices, but appears to be well protected against basis differential changes. Diamondback noted that two-thirds of its 2023 gas production was expected to go to Waha, while the remaining one-third gets Gulf Coast pricing exposure. Around 60% of Viper's production involves Diamondback operated properties, so Viper may have minimal unhedged exposure to Waha prices in 2023.

Royalty Vs. Upstream Cost Structure

I've modeled a couple scenarios below to answer the question of how royalty companies benefit from increased commodity prices in comparison to upstream producers.

At $60 WTI oil and $3 Henry Hub natural gas (along with more normalized differentials), a royalty company such as Viper (with a high-50s oil cut) may be able to realize $41.75 per BOE before hedges for its production. It doesn't have much in the way of costs, so after subtracting production and ad valorem taxes and cash G&A costs, it would net around $38.28 per BOE. This doesn't include the potential effect of cash taxes or interest costs.

An upstream company such as Diamondback with a similar oil cut has more expenses to deal with such as lease operating expenses and capital expenditures to keep production flat. In a $60 oil environment the upstream company would net around $20.33 per BOE after subtracting those items. This is around $18 per BOE less than what the royalty company would receive.

| $ Per BOE |

| Royalty |

| Upstream |

| Revenues |

| $41.75 |

| $41.75 |

| Less: Production And Ad Valorem Taxes |

| $2.92 |

| $2.92 |

| Less: Cash G&A |

| $0.55 |

| $0.70 |

| Less: Lease Operating Expenses |

| $0.00 |

| $4.50 |

| Less: Gathering And Transportation |

| $0.00 |

| $1.80 |

| Less: Maintenance Capex |

| $0.00 |

| $11.50 |

| Margins |

| $38.28 |

| $20.33 |

In an $80 WTI oil environment (along with $3 gas), the unhedged revenue per BOE increases to $55. The royalty company would net $50.60 per BOE in this example, an increase of $12.32 per BOE (or 32%) compared to the $60 WTI oil scenario.

The upstream company would net $27.65 per BOE in this $80 WTI oil scenario, an increase of $7.32 per BOE (or 36%) compared to the $60 WTI oil scenario. I've assumed a close to 40% increase in maintenance capex, reflecting the large amount of service cost inflation we have seen over the past couple years with higher oil prices. As well, there is an 11% increase in lease operating expenses due to inflation as well.

In terms of the percentage increase in margins, the upstream company gains several percent more than the royalty company. However, the royalty company gains more in terms of the absolute dollar increase, with its margins increasing by $5 per BOE more than the upstream company.

| $ Per BOE |

| Royalty |

| Upstream |

| Revenues |

| $55.00 |

| $55.00 |

| Less: Production Taxes |

| $3.85 |

| $3.85 |

| Less: Cash G&A |

| $0.55 |

| $0.70 |

| Less: Lease Operating Expenses |

| $0.00 |

| $5.00 |

| Less: Gathering And Transportation |

| $0.00 |

| $1.80 |

| Less: Maintenance Capex |

| $0.00 |

| $16.00 |

| Margins |

| $50.60 |

| $27.65 |

Updated 2023 Outlook

The current 2023 strip for WTI oil is now in the high-$70s, but Henry Hub natural gas has fallen to around $3.15. As well, the Waha basis differential is fairly wide, so Viper may only realize around $1.65 for its natural gas (before hedges) in 2023 based on strip.

Thus Viper is now projected to generate $712 million in revenues after hedges in 2023. Viper's hedges (including its Waha basis hedges) have around $6 million in positive value.

| Type |

| Barrels/Mcf |

| Realized $ Per Barrel/Mcf |

| Revenue ($ Million) |

| Oil (Barrels) |

| 7,628,500 |

| $77.00 |

| $587 |

| NGLs (Barrels) |

| 2,764,328 |

| $31.00 |

| $86 |

| Natural Gas (MCF) |

| 16,921,035 |

| $1.65 |

| $28 |

| Lease Bonus and Other Income |

| $5 |

| Hedge Value |

| $6 |

| Total |

| $712 |

This leads to a projection that Viper can generate $563 million in distributable cash flow in 2023, including the amounts that are attributable to non-controlling interests. This is around $3.41 per unit in distributable cash flow.

| $ Million |

| Production and Ad Valorem Taxes |

| $49 |

| Cash G&A |

| $8 |

| Cash Interest |

| $32 |

| Cash Taxes |

| $60 |

| Total Expenses |

| $149 |

Conclusion

Despite weaker natural gas prices (and a lack of Henry Hub hedges), Viper is still projected to generate $3.41 per unit in distributable cash flow in 2023, or an approximately 11% distributable cash flow yield. Viper is helped by oil prices remaining much stronger, with around 58% of its production being oil compared to 21% natural gas. As well, although Henry Hub prices are down significantly, at least Viper has hedged its exposure to Waha basis prices.

Viper is close to being fairly priced for a long-term $75 WTI oil scenario, with unit price upside of several percent by my estimate. Combined with its distributable cash flow yield, this could result in a mid-teens return over a year.

For further details see:

Viper Energy: Projected 2023 Distributable Cash Flow Remains Strong Despite Low NG Prices