VIRT - Virtu Financial: A Powerful Hedge

2024-01-18 08:16:05 ET

Summary

- The stock is trading cheap, below 1 P/S and offers a high margin of safety even in the unlikely case of 0% growth.

- Market maker Virtu Financial serves as a sophisticated hedge, benefiting from volatility and volume in markets.

- Virtu Financial is returning high capital returns to shareholders through dividends and buybacks.

- Current market conditions are ripe for Virtu, the business is set to thrive when the $6 billion in money market funds flows back to equities.

Investors associate hedging with a loss in the same way we look at insurance. Pay up for an insurance in the hopes of never having to use it, but if disaster strikes, we are happy we had it. But what if you could have insurance that pays you handsomely to sit and wait for that disaster? I like having my cake and also eating it.

Market maker Virtu Financial ( VIRT ) is serving my portfolio as a sophisticated hedge because it not only thrives in volatility and high volume, Virtu also pays us to be patient. Add the fact that it's undervalued looking at the intrinsic value, we now have a company that is well positioned to reap rewards regardless of market sentiment in 2024.

A built-in hedge in the business model

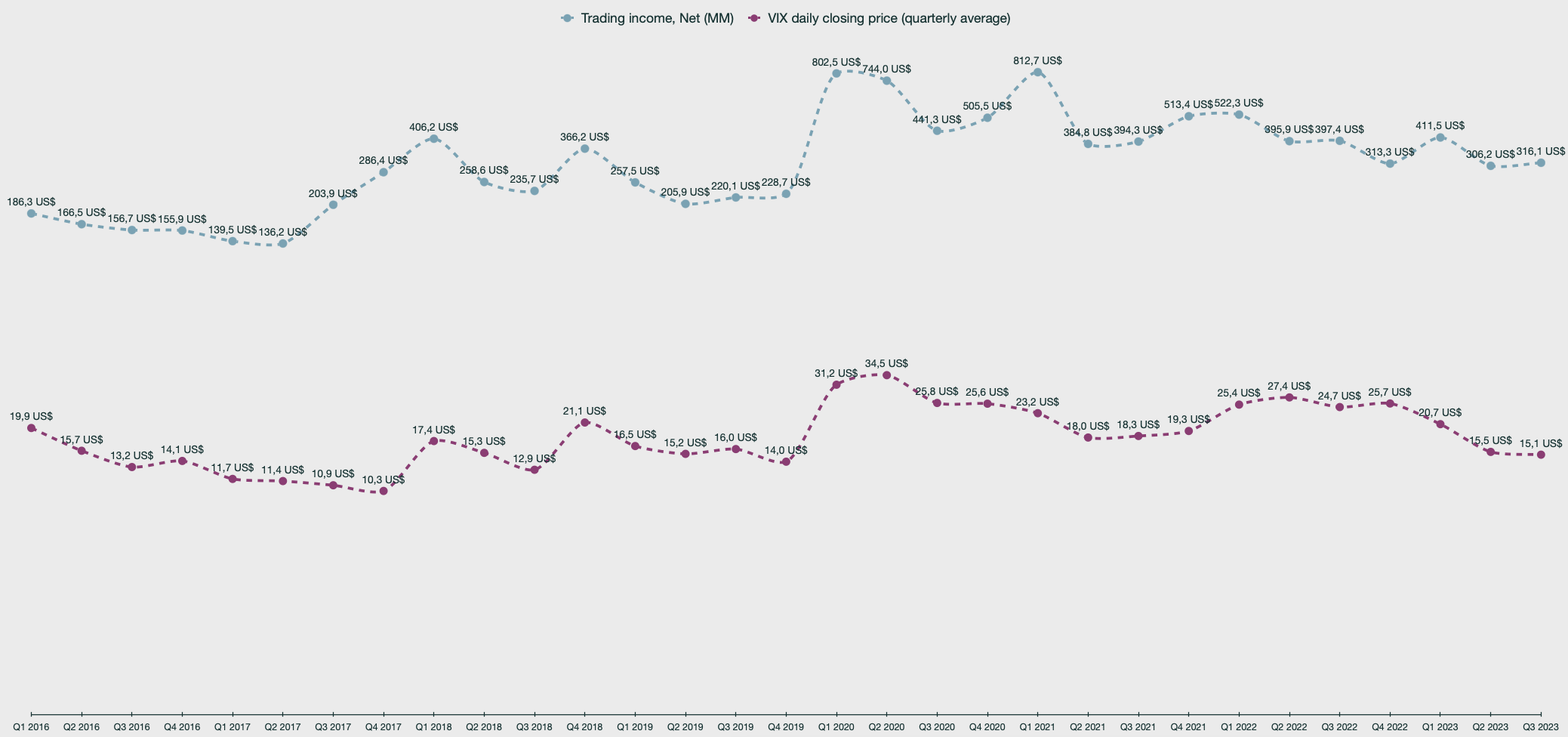

Virtu Financial is a market maker that handles roughly 25% of individual investor trades in the US. They operate as a liquidity provider in the equities market, they operate within the options market, the fixed income market as well as the crypto market. They also offer technology services and raise capital on behalf of clients, but the main income is from trading, namely market-making and execution services.

What drives income opportunities within the trading segment is bid-ask spread opportunities. When markets have a lot of volume and/or volatility, the opportunity to have wider spreads increases and so does Virtu's income.

Emir Mulahalilovic, Virtu Financial SEC Filings, Yahoo Finance

{kind=link}

I have plotted Virtu's trading income against the quarterly average closing price of the VIX . We can see a clear correlation between spikes in income and spikes in volatility, particularly during the peak pandemic fears and in the 2021 market euphoria. The direction of markets are not important to Virtu, what's important is that there is a lot of trading, either through fear or euphoria.

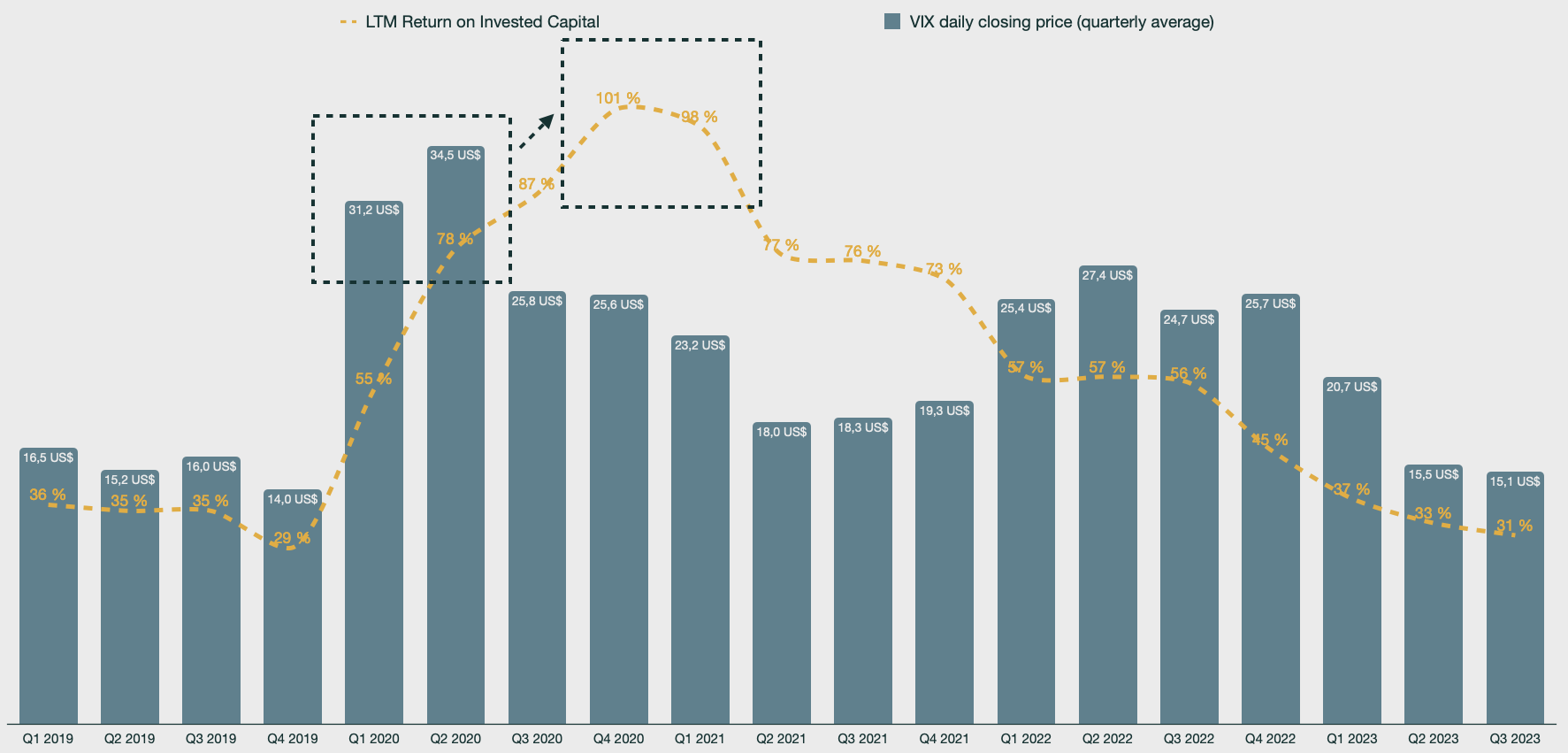

This correlation also shows up in the return on capital invested. I have plotted the last twelve months return on capital against the quarterly average closing price of the VIX. After high-volatility events, the return on capital increases.

Emir Mulahalilovic, Virtu Financial SEC Filings, Yahoo Finance; calculated as LTM Adjusted EBITDA divided by LTM Invested Capital

{kind=link}

That's against volatility, but what if we don't have a volatility event in the coming period? During the recent high interest rate environments, markets were pleasant, volumes were lower, and less activity took place. Investors fled to money markets to farm high yields, making a dividend stock like Virtu Financial suffer. Virtu not only took a hit in loss of bid-ask spread opportunities but also from dividend investors feeling more comfortable in treasury bonds than equity.

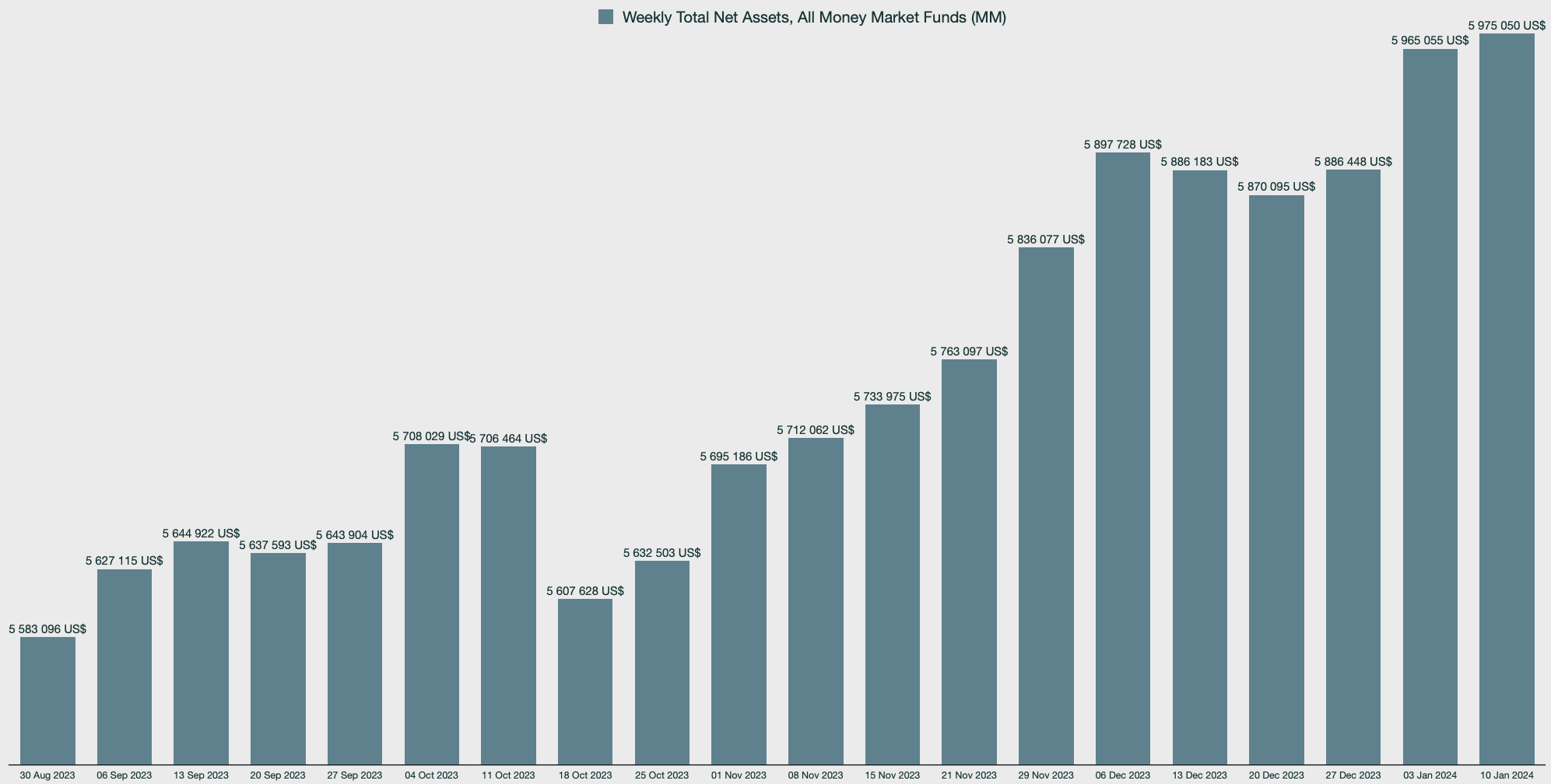

The ever-growing pile of cash on the "sidelines" is now upwards of $6 trillion as of January 10th. As monetary policy eases and yields become less attractive, this cash pile should find its way back into markets, creating a surge of activity. Activity which Virtu Financial will benefit from due to the bid-ask spread opportunities that volume in the markets provide.

Emir Mulahalilovic, Investment Company Institute (ICI)

{kind=link}

Some investors look to capitalize on the return of equity- and crypto market volume by owning Robinhood Markets ( HOOD ) and Coinbase ( COIN ). While brokerages indeed benefit from volume, they currently do not offer much shareholder return should the volume be absent; Virtu does.

Having the cake and eating it, too

If markets stay stale for another extended period, the outlook is still positive. Virtu consistently provides high capital returns to shareholders through a steady dividend payout as well as continuous share repurchases.

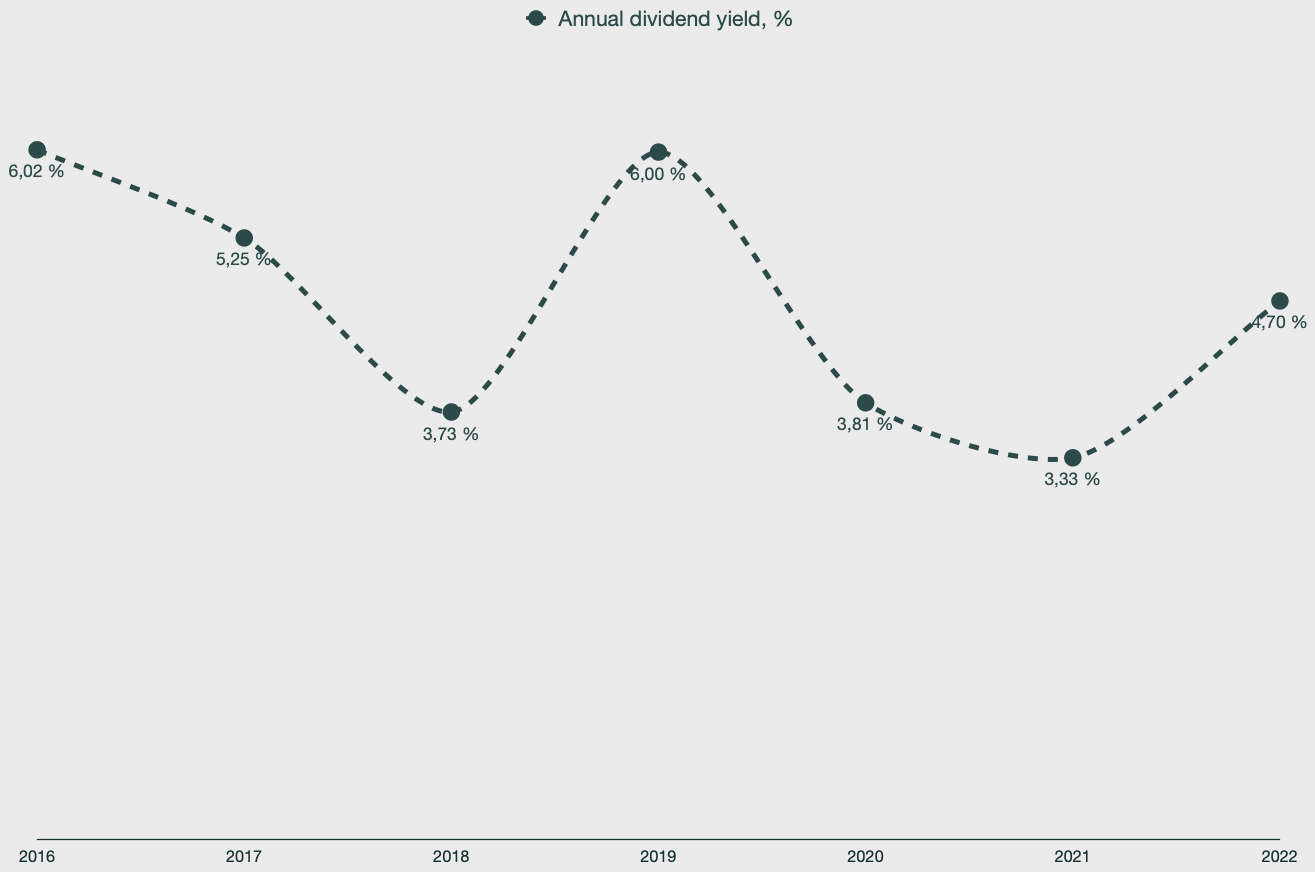

The quarterly dividend has been consistent at $0.24 for a great many years, and will likely stay around for a lot longer. Where Virtu is currently trading, that's around a 5% annual dividend yield. Very attractive, but not in the face of recent risk-free government bond yields, currently at 4,68% for the 1-year bonds. It will, however, turn very attractive as monetary policy eases.

Emir Mulahalilovic, Virtu Financial

{kind=link}

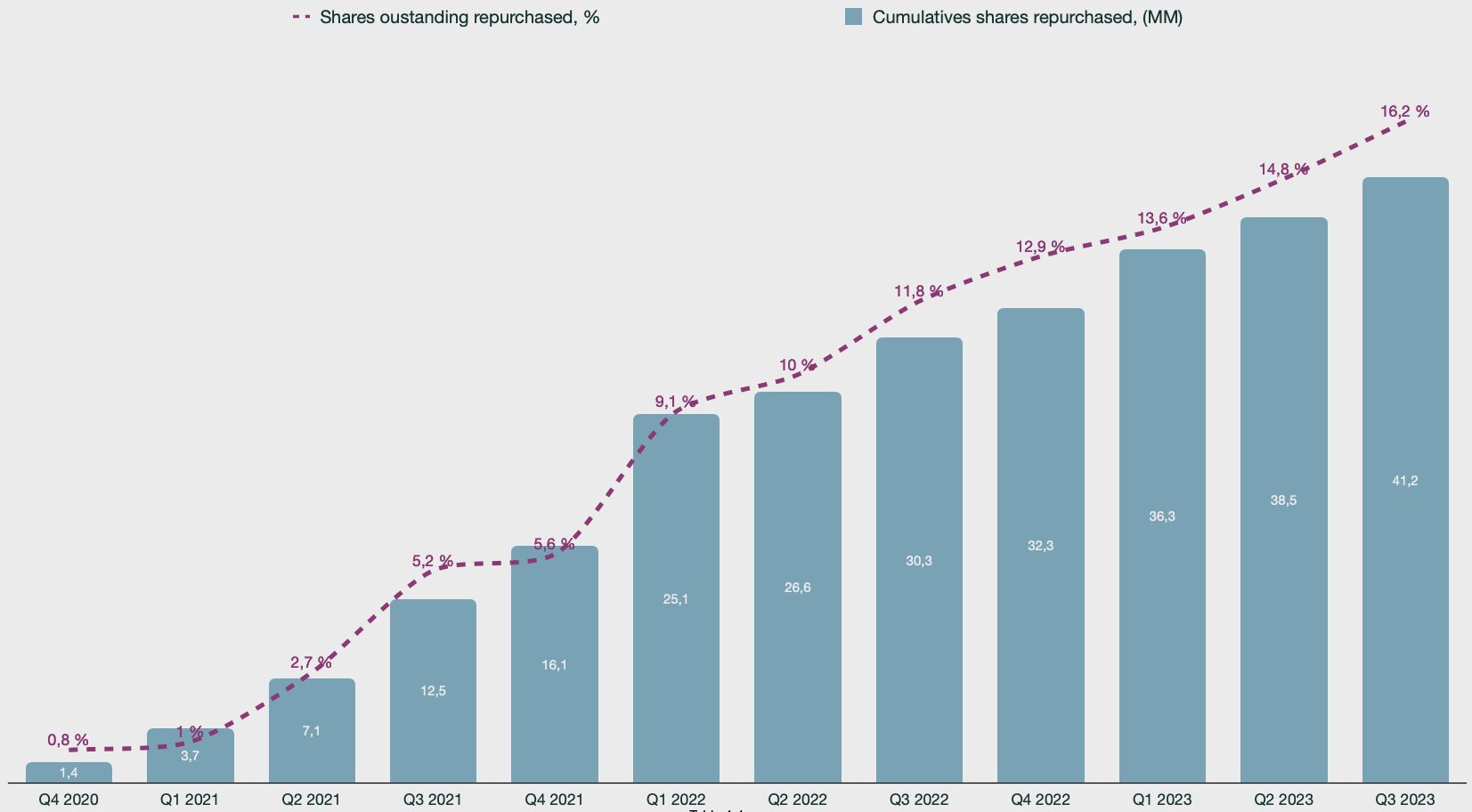

Besides offering a steady dividend, Virtu has repurchased a significant amount of its own shares. On a cumulative basis since Q4 2020, they've repurchased 41,2 million shares, which equates to 16,2% of the shares outstanding.

Emir Mulahalilovic, Virtu Financial

{kind=link}

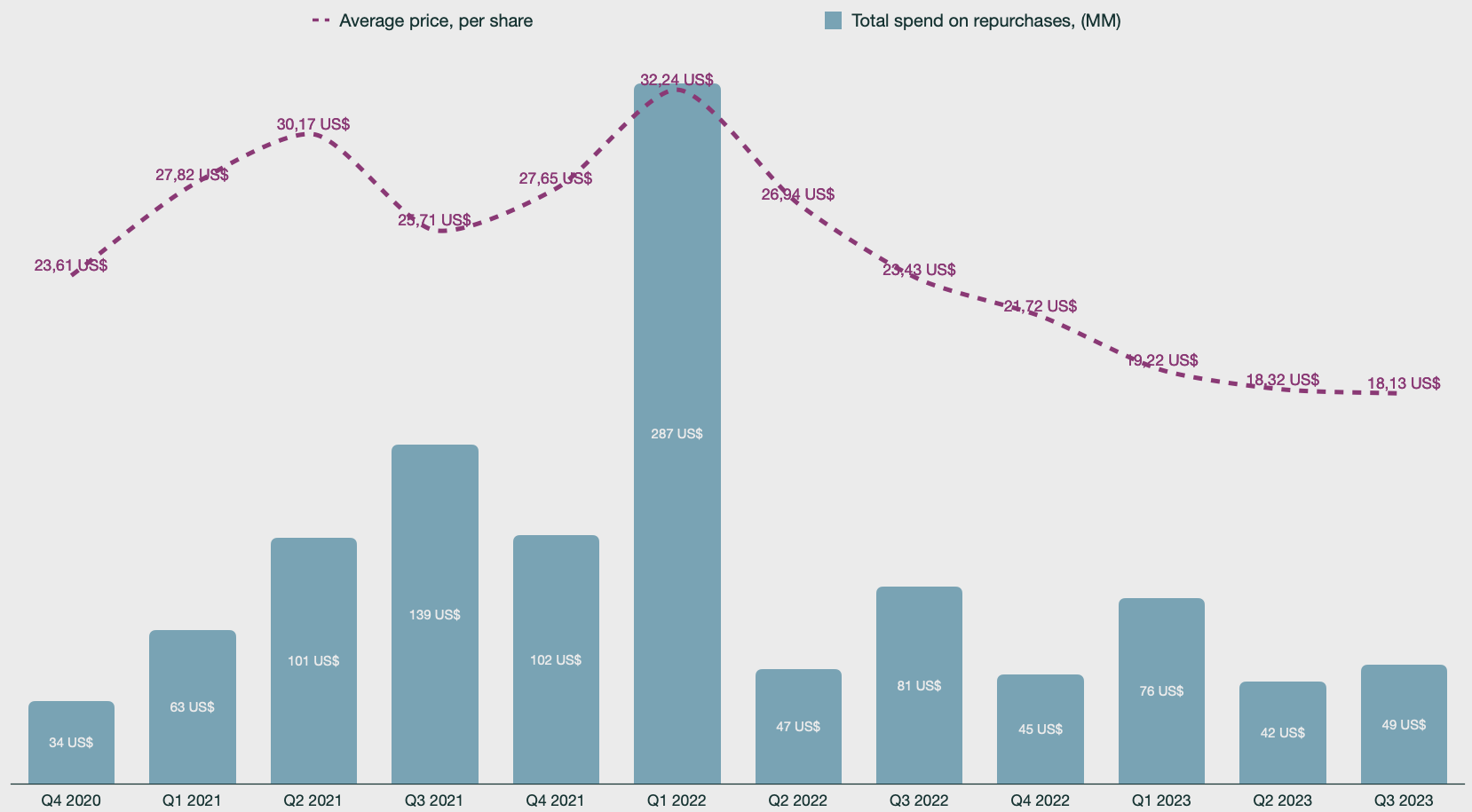

We also have data on the distribution of the buybacks and the spend. Unfortunately, Virtu Financial spent the most money on share repurchases at the average share price peak. It's not a disaster, but that large block would have been a lot more effective below the $20 price point. Cumulatively through 2024, Virtu may repurchase 20% of their outstanding shares, which is still impressive and an efficient way of providing shareholder value.

Emir Mulahalilovic, Virtu Financial

{kind=link}

The conclusion is that we are hedged for a market depression or a market rally. In the absence of such an event, we are handsomely rewarded for being patient simply by holding on to Virtu stock.

An undervalued stock

So far, we have covered the hedge for market events and how we are to be rewarded should there be none. However, there's a third reason for owning Virtu Financial at these levels; the valuation.

Intrinsic valuation for a market maker like Virtu Financial poses some issues. Any sort of market event can't reliably be captured in projections, as it equates to trying to time the market. We need to normalize the operational numbers but make sure to capture growth initiatives on the business side.

Virtu Financial has several organic business growth initiatives:

- Fixed income, developing credit and rates offerings

- Options market-making, increasingly expanding across venues and geographies; both individual tickers and indices

- Virtu Capital Markets, raising capital on behalf of clients

- ETF Block, expanding their offering to cover more products across more regions

- Digital assets, Virtu is a part of recent spot crypto ETFs

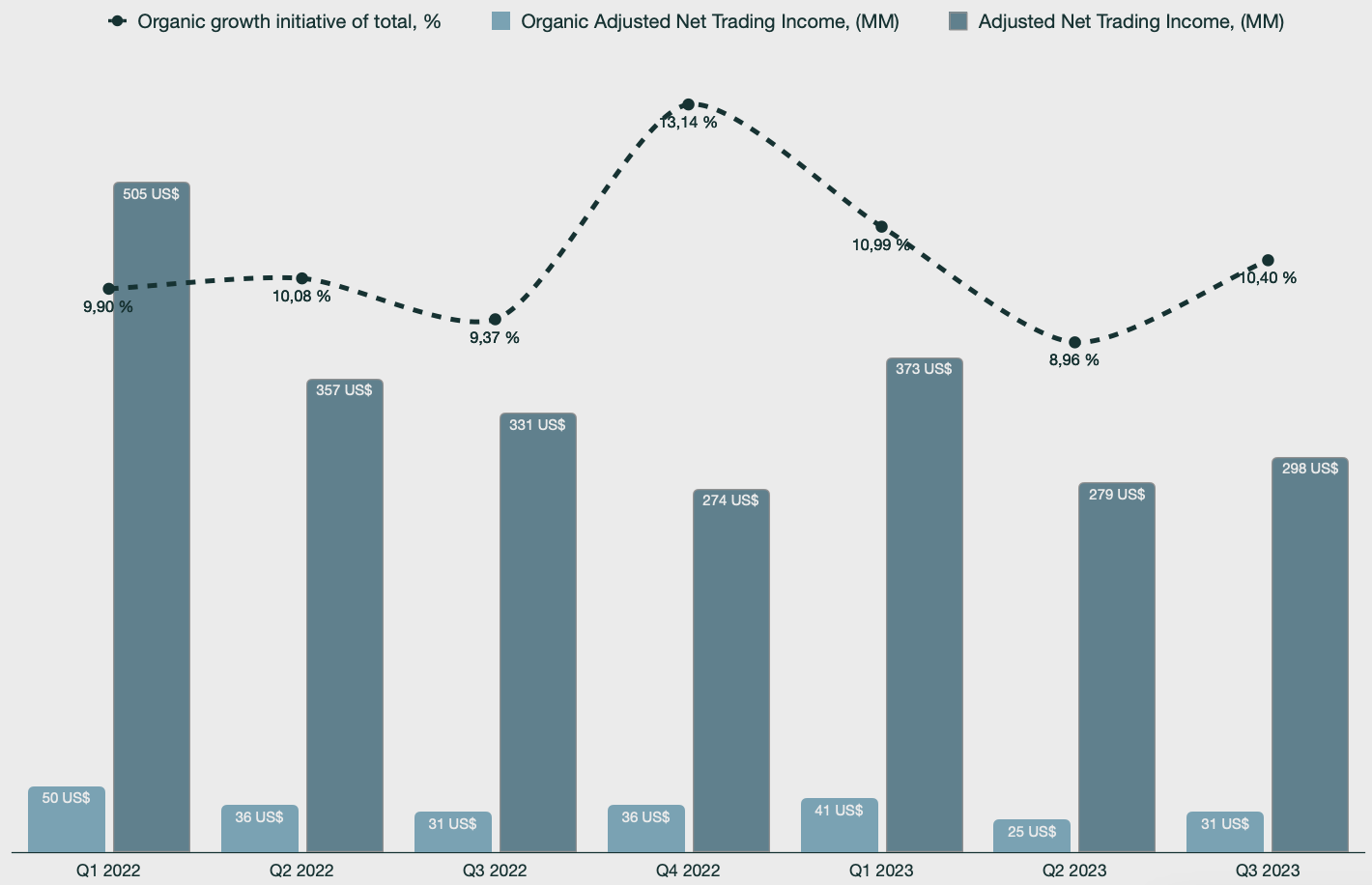

These initiatives, among others, are adding growth to the core business, which includes providing liquidity, high-frequency trading and other market making activities. On average, 10,4% of net trading income is from organic growth initiatives, which speaks to Virtu not staying stale, but are instead seeking out new opportunities to grow.

Emir Mulahalilovic, Virtu Financial

{kind=link}

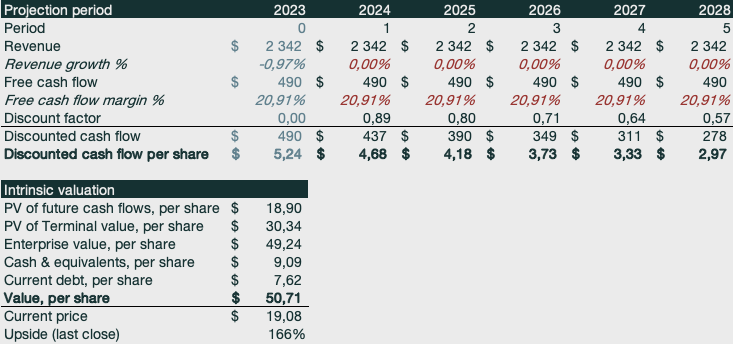

One of the first models I execute is one where I assume zero growth for any forward period. This allows me to gauge a margin of safety for stocks that I expect to continue having growth in the future. I extrapolated 2023 quarterly revenues by averaging them and then adding the average as the fourth quarter assumption to complete twelve months. Using this method, revenues land at $2,342 billion.

Free cash flow ((FCF)) margins are volatile for Virtu due to bid-ask spread opportunities, but it averages ~28% since 2015 to current date. The current trailing twelve months FCF margin is 20,91% , lower than the historical average, but I will use that margin assumption for the forward periods.

The model uses 12% Weighted average cost of capital ((WACC)) and 2% terminal growth rate. The intrinsic value per share output is $50,71, a staggering 166% return from current levels.

Emir Mulahalilovic, Virtu Financial SEC Filings

{kind=link}

It is a bit alarming whenever you see a zero-growth scenario yielding a 166% increase to reach intrinsic value. The coming periods may be volatile, but 2023 has a pretty average VIX level, so it should represent a normalized fiscal year result. $50.71 per share would represent a 2.02 Price to Sales (P/S) ratio today, which isn't at all outrageous. However, if we look at historical P/S ratios, we can see that Virtu is seldomly rewarded for its sales.

YCharts, Seeking Alpha

Historically, Virtu Financial has posted a 14,22% revenue compounded annual growth rate ((CAGR)). We know that Virtu Financial's current trading income is comprised of ~10% organic growth, which makes me confident that Virtu will have revenue growth moving forward. The FCF margins average ~28% which is a fair bit higher than the ~21% margin used in my DCF model. To me, buying Virtu Financial stock at current prices represents a high margin of safety.

Risks

One of the important risk factors to Virtu Financial's business model is the fact that it involves a lot of leverage. Being a liquidity provider means that Virtu needs to keep a lot of debt on its books. However, the debt was refinanced early 2022 and is dated 2029 with a blended interest rate of ~5%. Management was asked about this in the Q3 earnings call and Joseph Molluso, co-COO replied:

On the leverage ratio, I don't really feel like we are worried about whether it's 3x, 3.25x, 2.5x. We reset our debt. We were very fortunate and very happy that we did this in early 2022 when we had - we are in a different interest rate environment, obviously. We have got swaps on our debt. And we always look at it and try to keep that quantum as cheap as possible. We want to optimize that from a cost standpoint. But the question that we ask ourselves is, does the rate environment change the quantum of debt that we are comfortable with. And the answer is not really. I mean we will always look to make it as cheap as possible. But we are pretty comfortable with that total level.

The current debt levels do not worry me, they're a core necessity for the business model to work. Debt will likely stay around ~$2 billion as it has been, because it is easier to make returns with a smaller amount of capital. The excess cash is used for dividends and buybacks, barring any other opportunity the management finds.

Another core risk is the potential regulation of payment for order flow (PFOF). This is not a current risk, as PFOF is deemed beneficial for investors. Namely, it allows for commission-free trading at brokerages that allow it; it allows for better liquidity in markets and also helps investors get better execution prices. CEO Douglas Cifu commented the following during the Q2 2022 earnings call :

Importantly, over the last 20-plus years, the SEC has on several occasions examined the retail trading ecosystems, including payment order flow and wholesaling, and they favorably concluded that it provides material benefits to retail investors. The law is perfectly clear. The burden is entirely on Gensler to unequivocally demonstrate that his idea materially improved this ecosystem. This will prove to be an impossible task.

The thesis

I rate Virtu Financial a buy at this level because the company is set to thrive in the coming periods. The hedging component in the business model is extraordinary in how effective and protective it is.

- Trading income soars in case of a volatility event, protecting my portfolio

- There is a significant amount of capital on the sidelines; currently, ~$6 billion is hiding and farming yield in money markets

This means that Virtu Financial will do well regardless of the market direction, as long as there is activity. However, we may get another stale year in the markets where fear is present but not enough to spike the VIX, resulting in low volumes and fewer bid-ask spread opportunities.

In the case of a slow market, we are handsomely rewarded to sit tight in the boat and simply wait. Virtu has repurchased 16,2% of outstanding shares, which could reach 20% by the end of 2024 at the current pace. Beyond buybacks, Virtu Financial offers a steady quarterly dividend of $0.24, roughly a 5% annual dividend yield. Combined, it is a significant return to shareholders.

Virtu Financial is providing high shareholder capital returns; their business model serves as a fantastic hedge; and the stock is also undervalued. Assuming no FCF growth in the coming 5 periods, we still have a 166% upside to intrinsic value. The stock is trading below 1 Price to sales; it's very cheap, and the largest risks to the business are currently subdued.

For further details see:

Virtu Financial: A Powerful Hedge