NEP - Virtus Reaves Utilities ETF: Worth A Look For Utility Exposure

2023-08-09 12:11:19 ET

Summary

- Virtus Reaves Utilities ETF is an actively managed ETF that's managed by the infrastructure specialists Reaves Asset Management.

- In originally looking at this fund, I wanted to see if it was a potential alternative to UTG, but that isn't the case.

- The funds are positioned quite differently, but an investor looking for utility exposure and avoiding leverage could still see UTES as an alternative.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Reaves Asset Management is a management firm that is focused on infrastructure investing. The company was founded in 1961, but in 1978 is when Reaves began their focus on infrastructure investing. They aren't necessarily the largest operation, where they manage only one of each closed-end, open-end and exchange-traded fund. They also manage separately managed accounts for investors.

Reaves Utility Income (UTG) has become one of the more popular CEFs. This has largely been driven by its consistency in the distribution that it has paid out to investors. It's one of only a handful of CEFs that have inception before the 2008/09 Global Financial Crisis and haven't cut their payout to investors. UTG has total managed assets, which includes its leverage, of around $2.628 billion.

Then they have their traditional open-ended mutual fund, Reaves Utilities and Energy Infrastructure Fund (RSRFX). Interestingly, this fund was launched shortly after UTG in 2004. UTG launched on February 24th, 2004, and RSRFX was incepted on December 22nd, 2004. This fund is quite tiny, at only around $31 million in total assets.

Finally, there is the Virtus Reaves Utilities ETF (UTES). This is an ETF that is managed by the Reaves, with John Barlett being the manager of both UTES and UTG. Timothy Porter is the other manager that's associated with UTG, while UTES has Joseph Rhame III. UTES is also equally small similar to Reave's open-ended fund, with just over $45 million in assets. However, with an inception in the latter part of 2015, it doesn't have long of a history of operation either.

I've been exploring more ETF potential now that leverage expenses have been rising, which can make it more difficult for leveraged funds to operate in this environment. I recently explored the iShares Cohen & Steers REIT ETF (ICF) as a potential alternative for REIT exposure.

Continuing this quest, I came across UTES as a potential replacement for UTG. However, the funds are quite different, despite some overlap in terms of utility names. So while it doesn't look to be a direct comparison, there could be some merit to investing in UTES anyway.

The Basics

- Dividend Frequency: Quarterly

- Dividend Yield: 2.19% (SEC yield 2.66%)

- Expense Ratio: 0.49%

- Leverage: N/A

- Managed Assets: $45 million

- Structure: Active ETF

UTES' investment objective is "to provide total return through a combination of capital appreciation and income." To achieve this, the fund will invest "in equity securities of companies in the utility sector." This is fairly straightforward and simple.

It should also be noted that it is an actively managed fund too, so there is no benchmark that they are looking to replicate passively. Though for performance comparisons, they benchmark against the S&P 500 Utilities Index.

The management team will take "Qualitative (management interviews, field research, macro factor analysis) and quantitative (modeling, valuation, technicals) analysis inform bottom-up security selection through a dynamic investment process emphasizing disciplined risk management."

Being an actively managed fund, the expense ratio being relatively higher than its passively managed peers makes sense. However, the 0.49% expense ratio comes out to the exact median of all ETFs currently, providing a relatively reasonable expense ratio overall.

{kind=link}

Performance Comparison To Passively Managed XLU

In looking at the performance of UTES, it can make sense to measure it against something passively managed, such as the Utilities Select Sector SPDR ETF (XLU). In terms of total returns, UTES has been able to outperform since its inception. That's despite the 0.10% expense ratio charged by XLU. Though admittedly, there is quite a close correlation.

Ycharts

In general, 2023 hasn't been overly kind to the utility sector as a whole. Higher interest rates mean higher borrowing costs on utilities that often employ heavy amounts of borrowing to fund large Capex needs.

Additionally, simply having higher interest rates means that money market funds now often can provide higher yields than utility stocks themselves, making utility companies less impressive.

As it is now, the yields offered on money market funds such as (SPAXX) at Fidelity offer double the rate at around 4.75% compared to UTES 2.19%. XLU itself is only around a 3% yield currently.

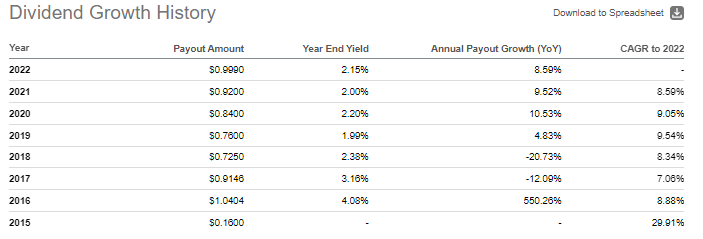

Compensation for a lower yield can often come in the form of at least a growing dividend. UTES has been able to deliver that since 2018. However, it's still actually down from the 2016 dividend peak that it paid out of ~$1.04, with last year coming in at just shy of $1.

{kind=link}

With that being said, YTD's performance for both of these funds has been a struggle. However, UTES still comes out slightly on top in this time frame as well.

Ycharts

Performance Comparison To UTG

With UTG, the fund invests quite differently as UTES contains only utility holdings while UTG is actually quite diversified. So a comparison between these funds isn't necessarily going to be that telling. Still, if one is looking to avoid leverage and discount/premiums, which both combine to create added volatility, then UTES could still be an alternative.

To better represent a more accurate picture of UTG's performance since UTES inception for comparison, we'll also be included the total NAV return performance. This is because CEFs can trade at discounts/premiums to NAVs, which can cause a significant divergence between the fund's market performance and how its actual underlying portfolio performs.

In this time period, the results are quite close between both metrics. In fact, the share price return basis would present UTG in an even better light, meaning that the fund experienced elevated performance due to discount reduction and/or premium becoming more elevated.

Ycharts

With that being said, UTES has been able to outperform during this period over UTG despite UTG's utilization of leverage that is attempting to enhance return potential. I think the reason for this is quite simple and one we've discussed in our updates on UTG over the last few years.

As a quick recap, I believe that it comes down to primarily 2 mistakes that UTG had made.

- The first was voluntarily deleveraging during the Covid crash, only to have the market rebound quite swiftly. The idea here made sense that the market could have kept dropping, and they wanted spare asset capacity to take advantage of further drops. Unfortunately, it didn't play out that way.

- The second misstep from UTG was they had started to push more into REIT exposure into 2021 and carry it into 2022. At fiscal year-end 2020 , UTG had around 15% in REITs, and by the fiscal end of 2021 , it was up to 21.25%. This was also up from fiscal year-end 2019 , where it showed less than 6% dedicated to REITs. All this was just in time to ride REITs lower as real estate was one of the w orst-performing sectors during 2022. Personally, I'm a big fan of REITs, but it ended up being poor timing to start adding more infrastructure REIT exposure.

UTES' Portfolio

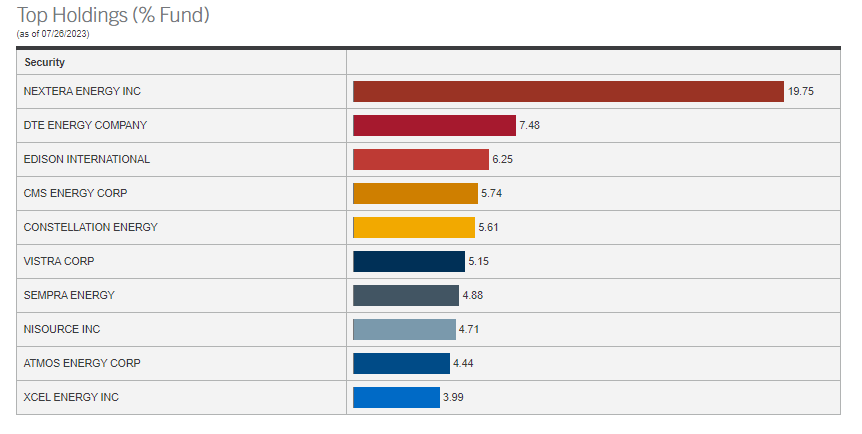

This is where UTES could also be seen as a negative or a positive, depending on one's own position. The portfolio carries a rather narrow focus of only around 20 total positions. However, there is very clearly a tilt to the portfolio, with the largest position carrying an oversized ~20% of the portfolio.

{kind=link}

This isn't a one-off either, as NextEra Energy (NEE) generally represents a very outsized position when looking at other time frames. From what I've seen, it's often over double the weighting of the next largest position, which is also fairly consistently DTE Energy (DTE). DTE has been more of a recent position that they've been adding to. As of January 31st, 2023, in their semi-annual report , it wasn't actually the second-largest holding. Going back a year ago to their annual report , DTE wasn't even 2% of the fund's assets.

Besides NEE, the fund also carries its subsidiary, NextEra Energy Partners (NEP). That would add more exposure to the same management team and overall NextEra operations.

Now, both NEE and NEP (as well as DTE) are personal positions of mine, so I'm quite happy to see they are getting so much love from the experts in the space. However, some investors would probably expect to see a bit more diversification when it comes to holding an ETF. At the very least, one probably wouldn't anticipate such a large position for NEE.

Interestingly, if you are an investor in XLU, you would actually be seeing a similar weight as NEE represents over 15% of XLU as well. UTES has been able to outperform XLU over the years, even while NEE has represented the largest holding for both.

However, one of the driving factors could be the larger weighting to NEE for UTES relative to XLU. NEE has been the clear winner in the utility space over the last five years. Therefore, suffice it to say whichever fund is running with NEE at an even larger position is going to experience even better performance historically.

Ycharts

Conclusion

UTES is an actively managed ETF managed by the respectable Reaves management team with a specific focus on infrastructure. While it definitely doesn't represent a clear alternative to UTG, its cousin, who's a leveraged CEF, one who's looking for less volatility and utility exposure, could still be served by UTES. With UTES, you wouldn't have to worry about the discount/premium or leverage costs that come with UTG.

The main caveat is that you might be a bit surprised if you expect to get diversified utility exposure. At least not at this point, given the oversized NEE position carried in this fund for a while. Which is actually similar to XLU, so you aren't necessarily getting diversified exposure there, either.

Additionally, the dividend yield of UTES will probably be less appealing than the distribution rate for UTG. UTES pays out only the income that the fund generates, while UTG pays out income and capital gains. So there will never be a time when UTES can compete with that. As of the latest dividends paid, XLU also carries an even higher rate currently too.

For further details see:

Virtus Reaves Utilities ETF: Worth A Look For Utility Exposure