V - Visa Vs. Mastercard Vs. American Express: Unveiling The True Champion

2023-11-29 09:53:46 ET

Summary

- Visa, Mastercard, and American Express have significant growth potential as cash transactions still hold a significant share of global transactions.

- Visa's revenue growth will be fueled by the increasing convenience of card-based transactions and the adoption of digital payment solutions.

- Mastercard has a larger size and potential for growth, leading to its premium valuation over Visa, but Visa has consistently demonstrated growth and maintains a competitive edge in efficiency and profitability.

Visa Inc. (V), Mastercard Incorporated (MA), and American Express Company (AXP) are globally recognized brands trusted by billions of individuals to facilitate their payments worldwide. Despite their remarkable track record of outperformance and impressive high double-digit growth, I believe there is substantial potential for further upside as cash continues to hold a significant share of global transactions.

Addressing the question that frequently arises among investors-"Who emerges victorious in this grand competition?"-let us embark on a collaborative journey to identify the ultimate winner.

Company Overview

Visa stands as a global trailblazer in the realm of digital payments, enabling transactions across over 200 countries and territories. The company's overarching mission is to seamlessly connect the world through the most innovative, dependable, and secure payment network. Visa's diverse array of products and services empowers consumers, businesses, and governments to make payments, transfer funds, and access financial services effortlessly.

While Visa's ubiquitous presence permeates our daily lives, understanding the intricacies of its revenue streams remains somewhat elusive. The company meticulously categorizes its revenue into four distinct sources: Data Processing, Service, International Transactions, and Other Revenue.

Created by the author using data from Visa's 10-K (.)

Visa's overarching strategy is to accelerate revenue growth by fostering increased volume in consumer payments, net flows, and value-added services, while simultaneously fortifying the foundational pillars of its business model. Visa remains steadfast in its mission to seamlessly transition trillions of dollars in consumer spending from traditional cash and check transactions to cards and digital accounts within its intricate network of networks.

In existing consumer payments, growth will be fueled by the ever-increasing convenience of card-based transactions. Innovations such as tap-to-pay, tokenization, and click-to-pay are steadily gaining traction, propelling the adoption of digital payment solutions.

In new flows, Visa has a ' network of networks ' approach, enabled by Visa Direct, which creates opportunities to capture value from new sources of money movement like peer-to-peer, business-to-consumer, business-to-business, and government-to-consumer. These kinds of transactions are all still a small portion of the company's business, yet they account for a huge portion of worldwide volumes. In 2022, Visa Direct had 5.9 billion transactions, which is a 36% increase from 2021.

In value-added services, Visa offers issuing solutions, acceptance solutions, risk & identity, open banking, and other advisory services.

Overall, with cash transactions totaling $7.6 trillion in 2022, I believe Visa still has a lot of growth opportunities ahead.

Created by the author using data from Mastercard's 10-K (.)

Payment Network Revenues

Mastercard's core offering is its payment network, which orchestrates the intricate four-party transaction that occurs when a cardholder (an individual or entity holding a card or other payment instrument) transfers funds from their issuing bank (the cardholder's financial institution) to the acquiring bank of the merchant (the merchant's financial institution).

Value-added Services Revenues

Before 2022, Mastercard's revenue streams were categorized into four distinct segments, mirroring Visa's reporting structure. However, in a strategic move to refine its financial reporting, Mastercard introduced the Value-added Services category last year.

This newly established category encompasses six primary subcategories: cyber and intelligence, data and services, processing and gateway, open banking, digital identity, and automated clearing house ((ACH)) real-time batch. While these solutions are inextricably linked to Mastercard's payment network, they differ in that their revenue generation is primarily independent of gross dollar volume ((GDV)).

Created by the author using data from American Express's 10-K (.)

Non-interest revenue and interest revenue

Non-interest revenue encompasses earnings derived from sources other than interest-bearing assets, such as fees, commissions, gains on asset sales, and other miscellaneous income streams. This type of revenue contributes to diversifying a company's earnings and reducing its dependence on interest rates.

Interest revenue

On the other hand, originates from interest-earning assets, including loans, investments, and securities. Financial institutions heavily rely on interest revenue as a primary source of income. Interest revenue typically exhibits stability due to contractual agreements; however, it is susceptible to fluctuations in interest rates, increasing when rates rise and decreasing when rates fall.

Is The Premium Over Visa Justified?

Investors seeking exposure to one or both of the payment giants have been inundated with a barrage of "Mastercard vs. Visa" analyses. Today, we'll add another heavyweight to the ring: American Express.

At first glance, Mastercard and Visa appear virtually indistinguishable, offering remarkably similar products and services. American Express, however, stands out from its peers with a unique business model. Unlike Visa and Mastercard, American Express acts as both a card issuer and a network processor, assuming direct credit risk for its cardholders.

While I believe all three titans are poised for long-term outperformance, as an individual investor striving to surpass the S&P 500 ( SPY ), I see no compelling reason to hold both Mastercard and Visa.

Given the acknowledged lack of substantial qualitative differences between the two companies, let's delve into their financial fundamentals to uncover potential differentiating factors.

Over the past five years, Visa has never traded at a premium to Mastercard in terms of their respective PE ratios. At the time of writing, the gap between the two companies' PE ratios is approximately 14.4%. Interestingly, this gap tends to contract during market downturns and widen when the market is bullish.

In my view, the primary reason for Mastercard's premium valuation over Visa is simply its larger size. Generally, if all else is equal, a smaller company has a higher potential for growth compared to a larger peer. This suggests that the market may be assigning a premium to Mastercard's growth prospects.

American Express currently trades at a PE ratio of 15.36x, significantly lower than both Visa and Mastercard. This lower valuation can be attributed to American Express's larger size compared to Visa and Mastercard. American Express is approximately 1.7x larger than Visa and 2.3x larger than Mastercard in terms of sales.

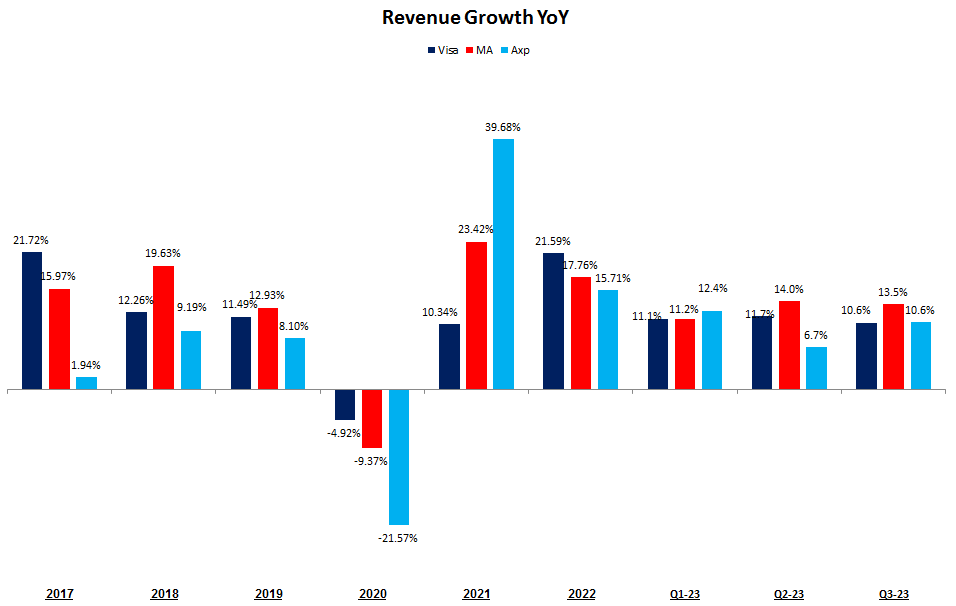

Revenue growth

Created by the author using data from the companies' reports (.)

{kind=link}

As illustrated above, between 2017 and 2022, Visa outperformed Mastercard in three out of six years and outgrew American Express in five out of six years. Over the entire period from 2017 to 2022, Mastercard's revenues grew at a 12.2% CAGR, while Visa's revenues grew at a CAGR of 11.6%, and American Express's revenues grew at a CAGR of 8.20%. It's important to note that Visa's and Mastercard's fiscal years are not perfectly aligned, as Visa's Q1 is Mastercard's Q4. This slight misalignment could affect some of the annual numbers, but it has no significant impact on the long-term CAGRs.

In the third quarter of 2023, Mastercard emerged as the winner in terms of sales growth. Mastercard's sales grew by 13.5%, while Visa's grew by 10.6%, and American Express's grew by 10.6%. In absolute dollars, Visa outgrew Mastercard by $46 million as a result. However, when considering overall revenue growth, Mastercard emerges victorious.

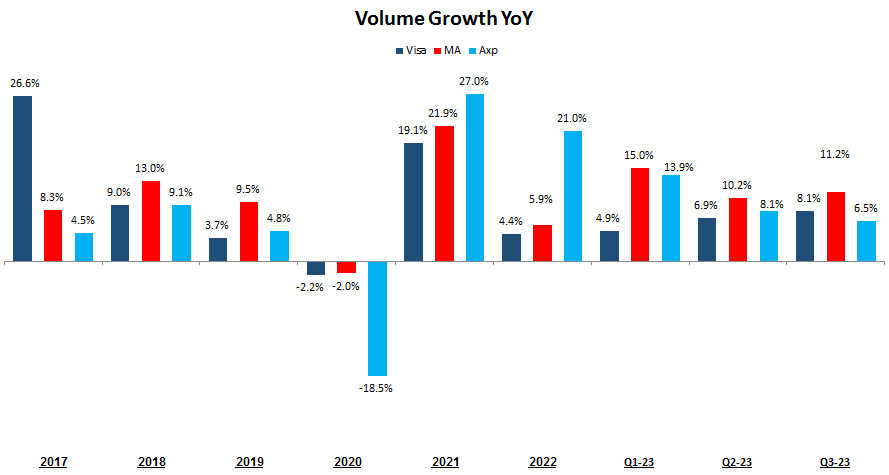

Volume Growth

Created by the author using data from the companies' reports (.)

{kind=link}

The volume growth comparison between Visa and Mastercard is somewhat complex due to Visa's significant outperformance in 2017. Despite this, Mastercard has outgrown Visa in five of the past six years. While Visa holds a slight edge in terms of CAGR for the entire period (9.7% compared to Mastercard's 9.2%), American Express has exhibited inconsistent volume growth. Mastercard outperformed Visa by 3.1 percentage points on a reported basis and American Express by 4.7 percentage points on a reported basis. These figures indicate that Mastercard continues to gain market share over both Visa and American Express.

Despite its relative growth, Mastercard still processes a significantly smaller volume of transactions compared to Visa, with Visa processing 65.9% more transactions than Mastercard. Additionally, Visa's transaction volume is over 800% higher than American Express's.

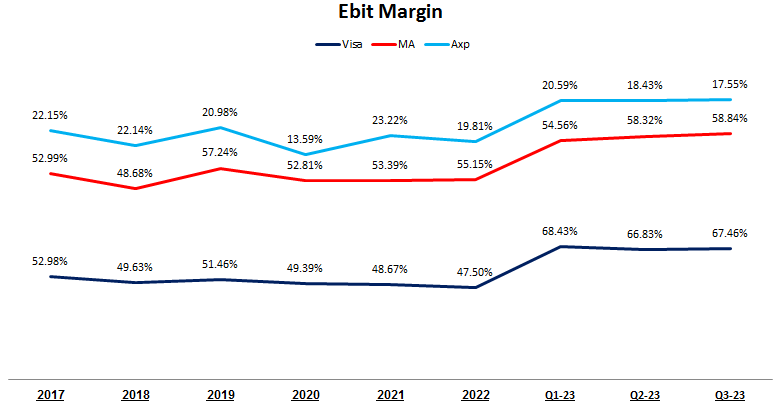

Margins - The Key Point

Created by the author using data from the companies' reports (.)

{kind=link}

Visa stands out as the clear frontrunner in terms of EBIT margins. Its operational efficiency significantly surpasses that of Mastercard and American Express by a substantial margin. While it could be argued that Mastercard's lower margin is a factor contributing to its premium valuation, stemming from investor optimism about its potential to eventually match Visa's margin, the margin gap between the two companies narrowed in Q3, reaching an apparent all-time low. However, it's important to note that the calendar third quarter is seasonally the lowest for Visa in terms of margin, while it's the highest for Mastercard.

In simpler terms, for every additional dollar in revenue, Visa generates $0.68 in operating income, while Mastercard and American Express extract $0.59 and $0.17, respectively. Consequently, to achieve the same rate of growth in absolute operating income as Visa, Mastercard would need to outgrow revenues by 16%, while American Express would require a staggering revenue growth of over 300%.

The Q3 2023 Fight Remains Close

Overall, a comparative analysis of the three companies reveals that American Express currently appears to be the least attractive investment option. This is largely due to the company's lackluster performance in terms of volume transactions and EBIT margins.

In contrast, the two dominant payment networks, Visa and Mastercard, continue to exhibit remarkable similarities. However, despite being the larger company, Visa has demonstrated consistent growth on par with Mastercard. Additionally, Visa maintains a competitive edge in terms of efficiency and profitability. Furthermore, Visa's innovative spirit is evident in its 18% growth in value-added services during the quarter, surpassing Mastercard's 17.0% growth. Consequently, the current premium valuation of Mastercard over Visa appears unwarranted.

However, I believe Mastercard is an amazing company, that is currently undervalued.

Visa Valuation

Employing a discounted cash flow ((DCF)) methodology, I have estimated Visa's fair value to be $295 per share. This valuation is underpinned by the assumption that the company will achieve a compound annual growth rate ((CAGR)) of 8.8% in revenue between 2024-2031, which is according to the company's long-term growth targets. This projection incorporates a weighted average cost of capital ((WACC)) of 8.5% and accounts for Visa's net debt position. Additionally, the FCF yield for the 2024 exit is 3.75%.

Author's assumption (Created and calculated by the author)

Mastercard Valuation

Employing a discounted cash flow ((DCF)) methodology, I have estimated Mastercard's fair value to be $440 per share. This valuation is underpinned by the assumption that the company will achieve a compound annual growth rate ((CAGR)) of 9.2% in revenue between 2023-2030, which is according to the company's long-term growth targets. This projection incorporates a weighted average cost of capital ((WACC)) of 7.7% and accounts for Mastercard's net debt position.

Author's assumption (Created and calculated by the author)

American Express Valuation

American Express presents valuation challenges due to the volatility of its cash flows. I have adopted an alternative valuation approach for AXP.

I anticipate double-digit revenue growth for AXP in the coming years, driven by its expanding customer base, increasing transaction volume, and favorable industry trends. This revenue growth is expected to be accompanied by similar growth in net income, as the company benefits from improved operating efficiencies and the positive impact of share buybacks on earnings per share ((EPS)).

AXP has a long history of share buybacks, and I believe that this trend will continue in the coming years. The company aims to repurchase 3% of its outstanding shares annually, which will help to reduce the number of shares outstanding and boost EPS. This commitment to shareholder value is a key factor in my investment thesis for AXP.

Based on my analysis, I believe that AXP has the potential to deliver a low double-digit return over the next five years. This is consistent with the company's historical performance. I am confident that AXP's strong fundamentals, growth prospects, and commitment to shareholder value will make it a rewarding investment for years to come.

Visa emerges as the most attractive investment opportunity among the three credit card companies, as I am confident in Mastercard and American Express' ability to deliver market-beating returns over the next five years.

Conclusion

A comprehensive evaluation of Visa, Mastercard, and American Express reveals Visa as the most appealing investment prospect among the three credit card giants. Its steady growth, unparalleled efficiency and profitability, and unwavering commitment to innovation make it an irresistible choice for investors seeking long-term value.

In my estimation, Visa and MasterCard stand as two of the most exceptional enterprises in the world. History has repeatedly demonstrated that disregarding distractions and prioritizing fundamental strengths is a proven strategy for achieving market-beating returns.

Despite projected double-digit revenue growth, American Express confronts hurdles in terms of transaction volume and EBIT margins.

I rate Visa a Strong Buy, Mastercard a Buy, and also assign a Buy rating for American Express, yet I consider Visa the more compelling investment due to its attractive valuation and superior profitability.

For further details see:

Visa Vs. Mastercard Vs. American Express: Unveiling The True Champion