VSH - Vishay Intertechnology: Debt Reduction New Go-To-Market Strategies And Undervalued Stock

2024-01-14 23:35:15 ET

Summary

- Vishay Intertechnology recently refinanced its balance sheet and canceled revolving debt.

- VSH's extensive semiconductor manufacturing portfolios and passive electronic components have a strong presence in various end markets.

- Despite mixed earnings and lower EPS revisions, the Company appears to be significantly undervalued, trading at low multiples compared to its competitors.

Vishay Intertechnology, Inc. ( VSH ) recently refinanced its balance sheet, canceled revolving debt, and announced new go-to-market strategies for 30 key product lines. With a significant amount of cash in the balance sheet, I believe that we could see new acquisitions and inorganic growth, which may lead to further FCF growth. Even considering M&A risks or the actions of competitors, I think that VSH does trade significantly undervalued.

Vishay's Products

Vishay maintains one of the largest semiconductor manufacturing portfolios in the world, as well as other passive electronic components that have a great output in various end markets, such as the automotive and industrial sectors.

Semiconductors include diodes, optoelectronic components, and MOSFETs, to which are added resistors, inductors, and capacitors as passive elements, used mainly in the management of energy flows, and especially electrical energy.

With more than 60 years of experience in developing electronic products and currently participating in a series of joint developments for industrial automation processes, as well as 5G and IoT networks, I believe Vishay could grow significantly in the coming years. Besides, the fact that many large, well-established, and innovative conglomerates work with Vishay may imply that many existing clients are ready to receive new developments .

{kind=link}

Although production for Vishay is organized under a single segment, the company distinguishes two market outlets based on the type of product it manufactures: semiconductors and passive components. Semiconductors are mainly used in integrated systems to control and manage energy processes and performance functions in ignition and flow routing.

On the other hand, the passive components business includes, as I said before, inductor resistors and capacitors that are frequently used in electrical systems to control and manage the flow of electricity.

Beyond the technical particularities of each of these products and the facilities it offers to its customers, in my view, the fundamental thing is to highlight the extensive production capacity that Vishay currently has as well as the international distribution network that allows it to locate its products in an extensive series of end markets.

Mixed Earnings, Lower EPS Revisions, But The Company Appears To Trade Undervalued At 3-4x EBITDA

I am unhappy about the recent mixed results delivered in November, which included lower EPS and quarterly net sales growth than expected. EPS was close to $0.47, and revenue was about $853 million. Additionally, it is not ideal that, in the last 90 days, the last EPS revisions were pessimistic.

Source: SA

In my view, the expectations for 2024 and 2023 are optimistic. Investors expect an operating margin of close to 14%-13%, a net margin of 9%-7%, and a 2024 EPS of close to 1.76. I do not think the expectations could help explain the current trading multiples.

Source: Market Screener

Vishay appears to be trading at close to 3x-4x EBITDA, which, in my view, is not only below the multiples seen in the semiconductor industry. These multiples seem low even if we look at any other industry.

Source: Ycharts

Negative Working Capital, A Significant Amount Of Cash, And Some Debt

As of September 30, 2023, Vishay reported a significant amount of cash of close to $1095 million, with short-term investments close to $78 million and accounts receivable of $442 million. In addition, with a total inventory of $643 million, total current assets are close to $2.440 billion.

The current ratio is not only larger than 1x, which means liquidity seems fine. Vishay also reports negative working capital, which means that the company does not need debt financing or anything related to finance its operations.

Source: Ycharts

Besides, with net property and equipment close to $1.180 billion, deferred income taxes of about $128 million, and goodwill worth $200 million, total assets stand at $4.241 billion. The asset/liability ratio is more significant than 2x, so the balance sheet appears solid.

Source: 10-Q

I am not concerned about the total amount of debt because cash in hand appears significant. However, it is worth noting that long-term debt has recently increased. Specifically, trade accounts payable stood at close to $207 million, with payroll and related expenses of about $162 million, long-term debt of about $817 million, and total liabilities of approximately $2.098 billion.

Source: 10-Q

Recent Debt Reduction Could Imply Higher EV/FCF Multiples

I revised the company's long-term debt and recent debt agreements to understand the cost of capital Vishay. I saw debt agreements, including SOFR plus 1.60%, but Vishay also noted 2.25% convertible senior notes due in 2030. Given these figures, I believe that assuming a WACC of close to 7% would be conservative.

Based on Vishay's current total leverage ratio, borrowings bear interest at SOFR plus 1.60%, including the applicable credit spread. Vishay also pays a commitment fee, also based on its total leverage ratio, on undrawn amounts. The undrawn commitment fee, based on Vishay's current total leverage ratio, is 0.25% per annum.

In September 2023, the Company issued $750,000 aggregate principal amount of 2.25% convertible senior notes due 2030 to qualified institutional buyers pursuant to an exemption from registration provided by Rule 144A under the Securities Act. The Company used the net proceeds from this offering to repurchase $370,242 principal amount of its outstanding 2.25% convertible senior notes due 2025, to reduce the outstanding balance of its Amended and Restated Credit Facility, to enter into capped call transactions (as further described below), and for other general corporate purposes. Source: 10-Q

Concerning the total amount of leverage, it is fair to say that the financial debt/EBITDA ratio declined significantly. In my view, as soon as other investors see these declines in the debt levels, we could see demand for the stock. From 2016 to 2023, the financial debt/EBITDA ratio decreased from 1.5x to about 0.6x.

Source: Ycharts

I also appreciated that Vishay reported new refinancing agreements, reduced the revolver balance to zero, and lowered future interest expense. With the demand for Vishay's debt, I think the business model is still well recognized. Thanks to the new debt conditions, I cannot discard more stock demand.

{kind=link}

Moving Production Facilities To Jurisdictions With Low Taxes Or Better Labor Laws May Bring FCF Growth

Vishay intends to move production facilities and labor to other territories where the company finds benefits due to the cost or tax facilities. In addition, the long-term gross growth, as stated in their reports, is based on the possibility of acquisitions of similar technology businesses while maintaining an amortization of ongoing investments through the permanent cost restructuring strategy.

Considering the total amount of cash, I think Vishay could acquire many new targets. As a result, we could see significant FCF growth driven by inorganic growth. Given the recent increase in goodwill and previous acquisitions, I assumed that Vishay knew well how to acquire targets, integrate new teams, and obtain cost synergies.

Source: Ycharts

New Initiatives, Expansion Projects, And New Product Lines Could Bring Net Sales Growth

In the last presentation to investors, management promised to develop go-to-market strategies for 30 key product lines. Besides, the company expects to increase its capex to finance expansion projects.

{kind=link}

These new initiatives could lead to capacity increases, net sales growth, and FCF growth acceleration in the coming years. As a result, we could see stock demand increase.

My Financial Expectations Based On Previous Assumptions, And Previous Financials

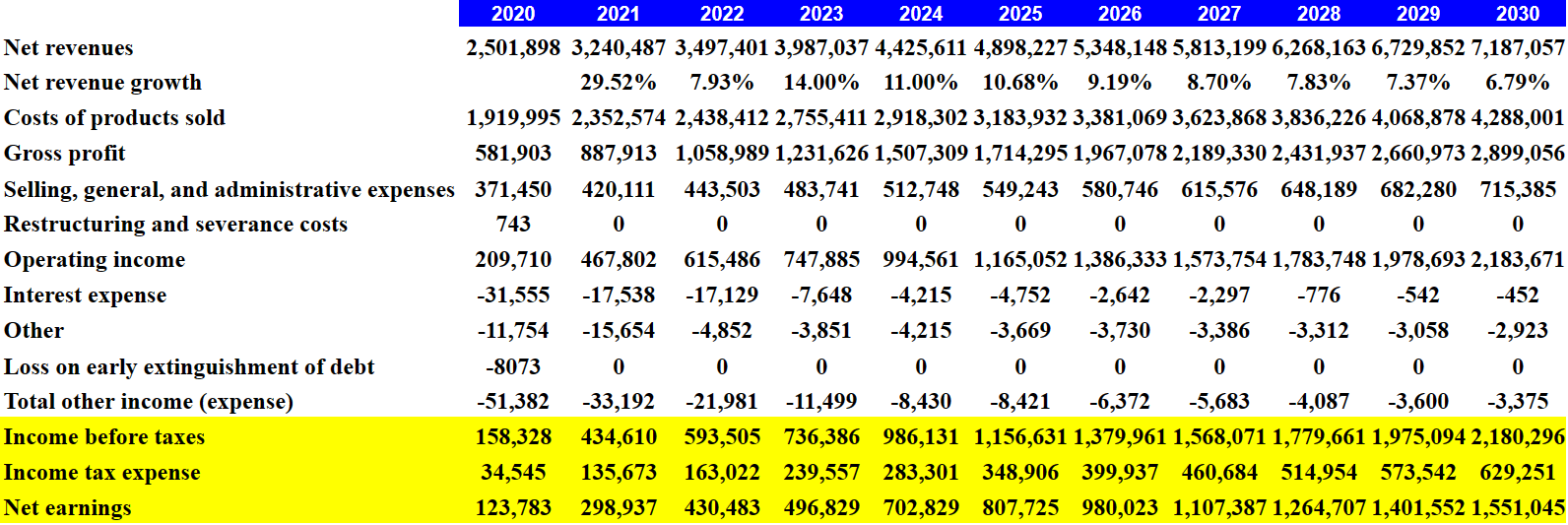

The global semiconductor manufacturing equipment market is expected to grow at close to 7.9% from 2023 to 2030. However, Vishay's revenue grew 29% in 2021 and 7.9% in 2022. Hence, I included net sales growth between 14% and 6% under my income statement projections, which I believe is fair for Vishay.

The global semiconductor manufacturing equipment market size was estimated at USD 103.1 billion in 2023 and is expected to expand at a compound annual growth rate of 7.9% from 2024 to 2030. Source: Semiconductor Manufacturing Equipment Market Report

My expectations for Vishay include 2030 net revenues of $7.187 billion with costs of products sold of $4.288 billion, and 2030 gross profit of $2.899 billion. In addition, with selling, general, and administrative expenses worth $715 million, and net earnings of close to $1.551 billion.

{kind=link}

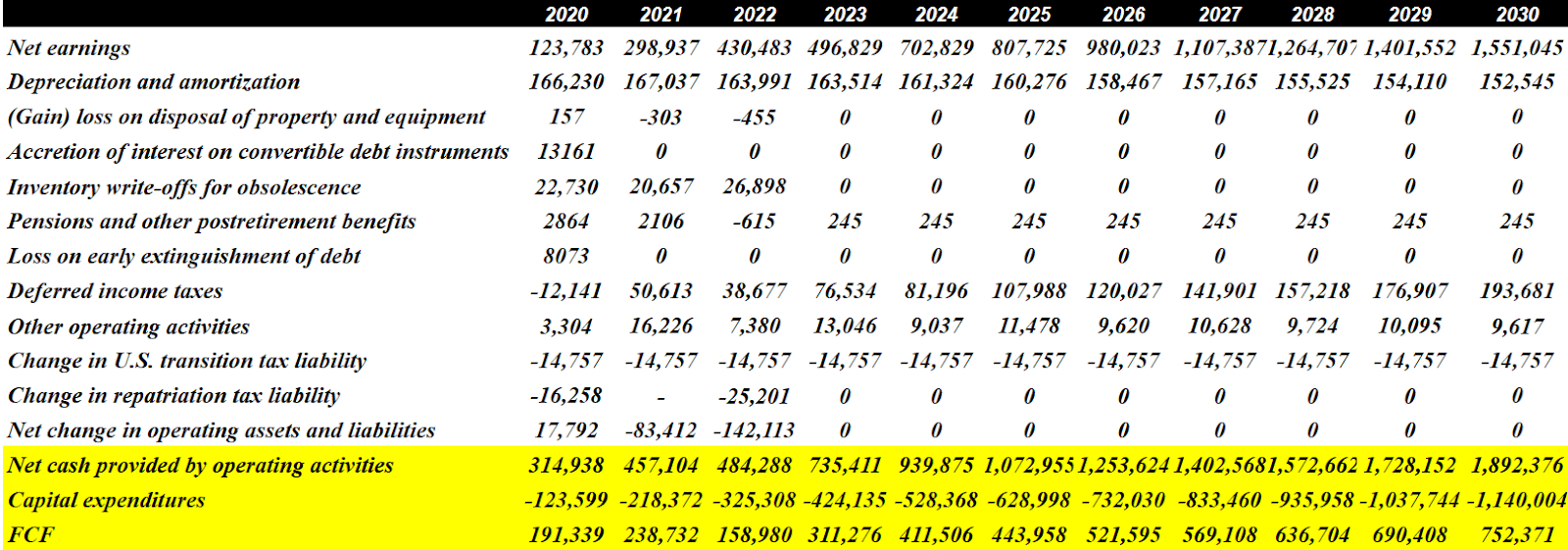

My cash flow expectations include 2030 depreciation and amortization of about $152 million. I did not have losses on disposal of property and equipment, accretion of interest on convertible debt instruments, or inventory write-offs for obsolescence because they're not recurrent parts of the business model. I also included the 2030 change in U.S. transition tax liability of nearly $15 million and the 2030 net cash provided by operating activities worth $1.892 billion. Finally, with 2030 capital expenditures of close to -$1.141 billion, 2030 FCF could be close to $752 million.

{kind=link}

I looked at the competitors' valuations to assess the exit multiples in my DCF model. According to Seeking Alpha, the sector median stands at close to 15x EBITDA, the median PE is close to 23x, and the price/cash flow is close to 22x-20x. Vishay is trading at multiples that are significantly lower than that of competitors, so I assumed a valuation of 6x FCF, which I believe is quite conservative.

Source: SA Source: SA

With the assumptions made below, a WACC of 7.9%, the total implied enterprise value would be close to $2.4 billion. However, adding the cash in hand, which is significant, and subtracting the debt outstanding, the forecast price would be close to $41 per share. Finally, the internal rate of return would stand at close to 11.6%.

Source: My DCF Model

Risks

Generally, the competition for this type of business is excellent and maintains low market entry costs in import and transportation capacities. Below, I detail the main competitors according to the kind of product.

Source: 10-k

As we see, some participants maintain product lines in several of the businesses and these other minority competitors. This also demonstrates the consolidation that has existed in this industry recently, which Vishay hopes to take advantage of by positioning itself as a second supply company.

First of all, it should be noted that the growth that the company has experienced in recent years has occurred mainly through its strategic assignments. And this does not mean that the trend will continue in the future. The inability to distinguish businesses or future integration after their acquisition are risks to be taken into account as part of this company's core strategy.

Class B stock shareholders own almost 50% of the company's voting power, and these shares are in the hands of few people who can decide the company's future and not give rise to future financial instruments to acquire debt for the purchase of other companies. Besides, in my view, investors dislike when companies report two or more share types because the share count is sometimes inaccurate.

We have two classes of common stock: common stock and Class B common stock. The holders of common stock are entitled to one vote for each share held, while the holders of Class B common stock are entitled to 10 votes for each share held. At December 31, 2022, the holders of Class B common stock held approximately 48.5% of the voting power of the Company. The ownership of Class B common stock is highly concentrated, and holders of Class B common stock effectively can cause the election of directors and approve other actions as stockholders. Source: 10-k

Conclusion

The recent reduction of the revolving debt obligations and the lower net leverage could bring new inventors interested in Vishay Technologies. Besides, the company recently noted new initiatives, including new go-to-market strategies for about 30 key product lines and new expansion projects. Even considering the existence of class B shares risks related to competitors, or failed acquisitions, Vishay looks cheap at the current EV/EBITDA ratio.

For further details see:

Vishay Intertechnology: Debt Reduction, New Go-To-Market Strategies, And Undervalued Stock