VIST - Vista Energy: A Booming Buy With A Strong Upside Potential

Summary

- The share price of VIST has been steadily rising over the past year, gaining by more than 116% and outperforming the market by over 130%.

- Equally impressive improvements have matched the strong share price growth in the company's financials.

- The excellent performance is driven by high oil prices and the company's increased productivity in the profitable market.

- The company's low price and growth potential make it a good investment, in my opinion.

Investment Thesis

Through its subsidiaries, Vista Energy, S.A.B. de C.V. ( VIST ) explores and produces oil and gas in Latin America. The company has been on a solid upward trend over the past year, with share prices increasing by more than 116% and beating the market by a margin of about 130%.

Its financials have been dramatically improving and are attractive, complementing the robust share price growth. The high oil prices and the enhanced productivity of the company in the profitable market are the primary drivers of good performance.

VIST is continuing to make substantial investments in expanding production capacity to maximize its identified profitable opportunities. The fact that the corporation can increase output while incurring only a little increase in costs per unit indicates its cost-cutting prowess. Because of the promising market potential and the low marginal cost of producing more, I expect strong growth from this firm. This stock is a buy recommendation because I believe the company is undervalued and has substantial potential for growth.

Increasing Production Capacity

As oil prices have risen , VIST has increased production to cash in on the boom. I would call the company's current strategy of expanding output while keeping expenses constant a case of production efficiency since the marginal cost of producing an additional output unit is negligible. It's a given that this will give them a financial windfall.

" Lifting costs per B.O.E. was $7.5 for the quarter, reflecting our success in containing cost pressure as well as dilution of fixed costs through incremental production volumes." - Miguel Galuccio

Total production in Q3 2022 was an average of 50.7 BOEs per day, up 26% year-over-year, as reported in the call transcript. The timely completion of the final three pads in Bajada del Palo Oeste contributed significantly to a 35% year-over-year increase in oil production. In addition, the company spent $162.8 million on capital expenditures [CAPEX] during the quarter, with the money going toward the completion of 3 pads and the drilling of 6 wells. To put this increased productivity in perspective, consider that adjusted EBITDA for the quarter grew to $233.7 million, more than doubling year over year.

" Production growth, coupled with the strong realization prices amid flat lifting costs, boosted adjusted EBITDA to $233.7 million for the quarter, more than doubling year-over-year."- Miguel Galuccio

Recently, a modular improvement to the oil treatment facility in the Bajada del Palo Oeste and Aguada Federal cluster was completed, increasing the processing capacity from 40,000 to 47,000 barrels of oil per day, which is essential for treating the crude oil produced.

The company plans to boost the plant's capacity from 47,000 to 63,000 barrels of oil per day in the first half of 2023 and to drill three more wells in the fourth quarter of 2022. Since increasing output has been a critical factor in the company's meteoric expansion, I believe this decision will serve to further boost the company's growth in the years to come.

Financials: A Sign Of A Bustle

The company's financials have improved due to favorable market conditions, with high oil prices and output ramping up. The benefits are seen in strong and healthy growth. VIST has a YoY revenue growth rate of 92.6%, an EBITDA growth rate of 123.88%, an EBIT growth rate of 394.71%, and an EPS growth rate of over 16,000%.

These numbers attest to the thriving state of the oil industry. Most intriguingly, VIST is not only capitalizing on industry trends to fuel its expansion but also outperforming its rivals in this regard. Its growth rates are significantly higher than average in the sector, demonstrating this. When compared to its competitors, VIST represents a genuine risk in this market.

Seeking Alpha

The growth of the business has resulted in increased cash flow. Currently, it has $182.98m in cash on hand, which is 2.16 times as much as the company needs to cover its average quarterly total operating expenses ($84.83m) to stay afloat. VIST also has a cash flow from operations balance of $613.25M and a levered FCF balance of $230.37M. I see this as a positive trend, and I am confident that these numbers will continue to rise.

Considering the above-mentioned growth, the company's profitability margins round out this section. VIST has very healthy margins, which I believe appeal to investors. It has a gross profit margin of 74.24%, an EBIT margin of 43.88%, a net income of 22.25%, a return on equity of 36.19%, and a return on assets of 16.30%, which I strongly attribute to the strong growth exhibited by the company.

Seeking Alpha

I anticipate these margins to grow as the company continues to scale up output in response to rising oil prices. I believe these profit margins will improve because the marginal production has a meager marginal cost, as reported during the Q3 2022 transcript call.

Valuation

The company's T.T.M. and forward valuation metric are an oasis of green, with all relative valuation multiples being lower than the industry median due to inflated prices and revenues. In the eyes of long-term investors, the stock's current low price represents a golden opportunity to enter this booming industry at a discount.

Seeking Alpha

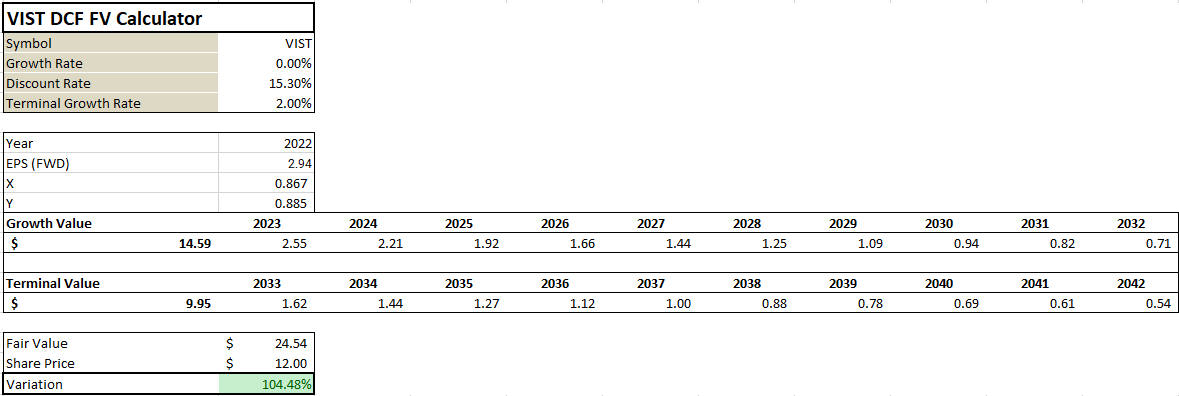

In addition, I calculated the company's fair value and growth potential using a discounted cash flow model based on earnings per share. Below is the output.

{kind=link}

In running the model, I used a conservative growth rate of 05, a discount rate of 15.3%, and a terminal growth rate of 2%. Given these assumptions, the output of the model showed that the company's fair value is $24.54 per share as opposed to the current price of $12. More importantly, it has a potential upside of 104.5 %, lending credence to my claim that the firm is underpriced. This potential gain indicates the future rewards value investors can reap if they enter the company at this time. Potential investors should consider investing in this promising company.

Risk

Even though I have an optimistic outlook on this stock, I recognize that investing in the company is not without its share of dangers. With oil prices at an all-time high, businesses across the board are scrambling to make the most of this lucrative opportunity. If this pattern maintains, there will be an excess supply on the market, leading to prices returning to normal. The current boom will cease if prices return to normal, as this will wipe out the abnormal profits being made at the moment. According to Fitch's analysis , rising production across the board will keep prices constant. This analysis supports the veracity of this major risk of investing in this firm.

Conclusion

Price increases have marked the oil market's profitability. VIST took advantage of the situation by increasing its investment in expanding its production capacity. The strategy has paid off handsomely for the company, as evidenced by its rapid expansion and high-profit margins, as well as the more than 100% increase in share price over the past year.

Due to the high prices expected to persist and the company's commitment to increasing production while holding costs steady, I anticipate the company will continue to expand rapidly. Nonetheless, investors should exercise caution because the market could become oversaturated due to oversupply if every business aims to capitalize on the current boom in profits. Overall, I think the company is worth investing in because of its cheap value and promising future growth.

For further details see:

Vista Energy: A Booming Buy With A Strong Upside Potential