VIST - Vista Energy: Great Quarter Upside Potential Remains

2023-10-25 13:44:21 ET

Summary

- Vista Energy engages in oil and gas exploration in Latin America, with significant assets in Argentina's Vaca Muerta shale reserve.

- Despite slightly lower-than-expected financial results, Vista's improved fundamentals and growth projections support its current valuation.

- If, within a year, it were to trade at the current EV/EBITDA multiple, the stock should rise 34%.

Investment Thesis

Vista Energy (VIST) engages in the exploration and production of oil and gas in Latin America. The company's principal assets are located in Argentina, more specifically in Vaca Muerta. Vaca Muerta is the world's fourth-largest shale oil reserve and the world's second-largest shale gas deposit. Vista also owns producing assets in the US and Mexico.

The stock has been on fire since 2021. However, the rapid growth and improved fundamentals can support this valuation, and we believe that after the last quarter and the projections management made during the investor day, the stock can continue to climb and reach new highs.

Financial Results

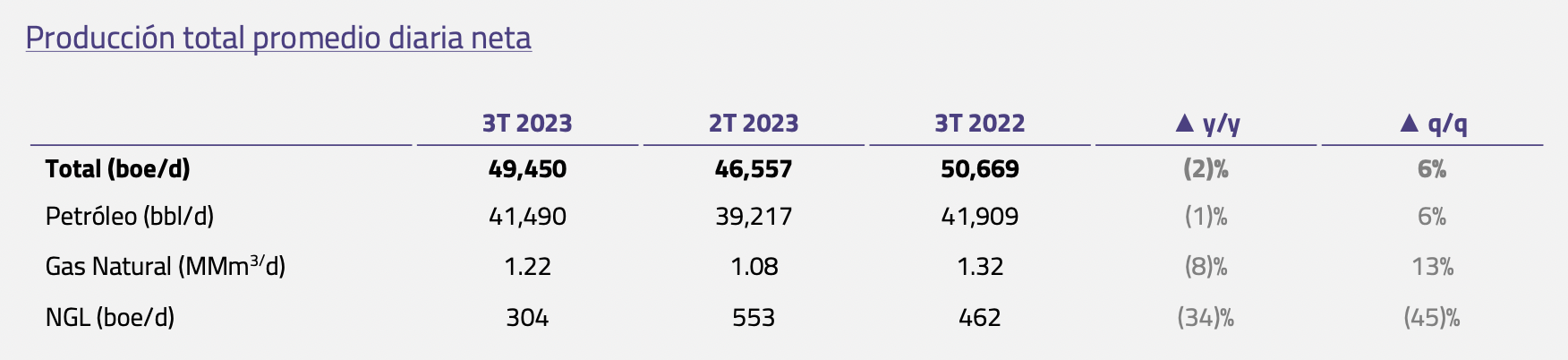

Vista reported its Q3 2023 financial results on October 24. In general, the numbers came in a little below the consensus: sales were $290 million vs. $327 million expected, EBITDA was $226 million vs. $239 million expected and net profit was $83 million vs. $86 million expected.

Total production was 49,450 boe/d, representing a 2% decrease year-over-year but a sequential improvement of 6% quarter-over-quarter. However, on a pro forma basis, when adjusting for production from the Conventional Asset Transaction , production increased by 12% year-over-year. Q3 2023 oil production reached 41,490 bbl/d, showing a sequential increase of 6%, primarily driven by the connection of 12 new wells at Bajada del Palo Oeste, with a 1% decrease year-over-year.

{kind=link}

Sales were up 25% compared to the previous quarter due to a higher volume (+22% crude oil vs. 2Q23) and a better average price (+5% for oil, thanks to the export mix). Sales from oil and gas exports represented 57% of total sales vs. 52.8% a year ago.

The production cost remained at USD 4.80 per bbl, which is very competitive. Thus, EBITDA increased by 49% compared to 2Q23, and the margin expanded strongly - two data points that we believe should give the market peace of mind.

In the quarter, it had a negative FCF of $43.5 million, and net debt increased by $86 million. Why? Because the company invested more ($181 million), had to pay taxes of $22 million, and increased working capital by $66 million. It continues to have a comfortable financial position, and we are confident that it will be able to finance its growth plan with its own cash flow generation.

Outlook

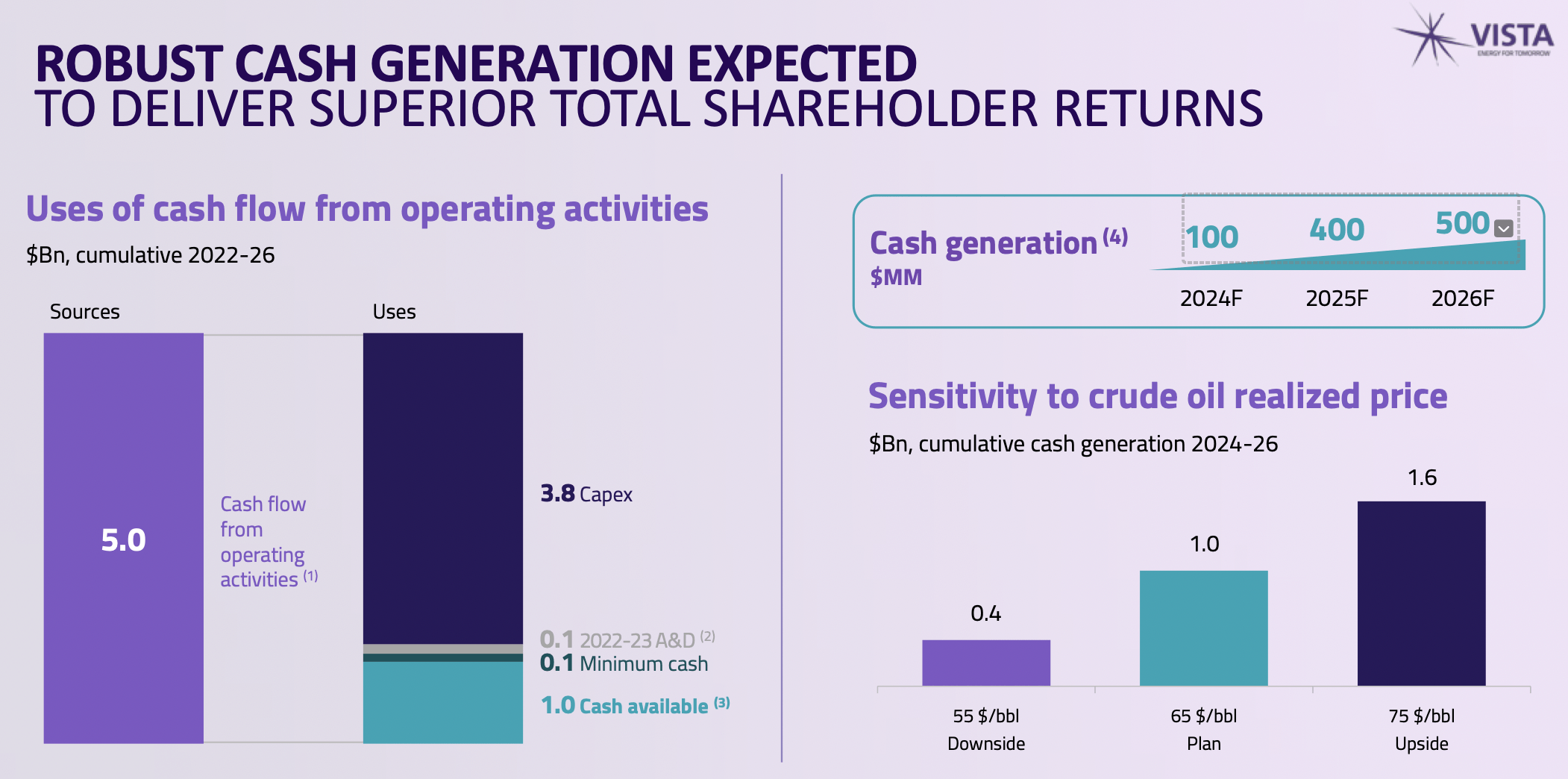

Vista had their investor day on September 26 . They raised the guidance for production, sales, EBITDA and FCF generation between now and 2026. They expect:

- Total production of 100Mboe/d

- $2.35 billion in sales

- $1.7 billion in EBITDA (~72% margin)

- $1 billion in FCF generation between now and 2026

As evident by the next image, these financial projections depend greatly on the international price of oil, which cannot be hedged today.

{kind=link}

Moreover, the financial projections also depend on Argentine sectoral policy. The adjustment of relative prices would mean an increase in gasoline in the assortment and it is not clear if it is politically viable. If gasoline at the pump does not increase, the local price of crude oil will necessarily continue to be well below the international price.

Beyond these risks, there is the known good (very good) part: if things go as projected, and the previous points do not affect it, we believe that the cash generation will be so much that there will be no way that it will fall short of projections. And the stock should respond accordingly.

Takeaway

With the stock at $30.50, guidance of $850-900 million EBITDA by 2023 and $1.1 billion by 2024 assumes multiples of 3.4x and 2.7x EV/EBITDA, respectively. If, within a year, it were to trade at the current multiple, the stock should rise 34%. We like VIST, but we pay attention to the fact that until this year, the share price responded to operational improvements, and the EV/EBITDA multiple was more or less constant. This year, we had multiple expansion, and the multiple is closer to regional peers (Remember that Vista is expected to double production in 3 years).

But what could go wrong? There is a high political risk. Argentina is currently in the middle of an election with candidates who have very different policies that could either hurt or benefit the industry. Moreover, depending on who wins, there could be negative sentiment regarding Argentine stocks and the country's economic prospects.

In conclusion, Vista is in great shape. Even after the enormous price increase during the past couple years, we believe there is still upside for the stock.

For further details see:

Vista Energy: Great Quarter, Upside Potential Remains