VIST - Vista Energy Is Still Undervalued

2023-04-30 03:44:22 ET

Summary

- The most recent quarter witnessed a net margin expansion to 42.4%.

- The last 4 quarters of operations have a combined annual return on capital of 29.55%.

- The company has a forward P/E of 5.54x, a trailing PEG of 0.01x, and a forward Price/Cash Flow of 2.47x.

- It has low debt and improving equity.

- Vista Energy stock is still a Buy.

Thesis

Finding undervalued companies with bright futures and appealing financials can be difficult. Every time I look over Vista Energy, S.A.B. de C.V. ( VIST ) I am reminded that they do exist. In my last article covering the company, I concluded that it still had plenty of upside. The most recent quarter showed further progress toward reaching maturity. I believe Vista Energy is still a Buy.

Company Background

Vista Energy was founded in 2017 by Miguel Galuccio , the former CEO of Argentina's state-owned oil company YPF. Their IPO raised $650M. Vista has acquired several exploration and production contracts for oil and gas which include operations in Mexico , Argentina, and Brazil .

{kind=link}

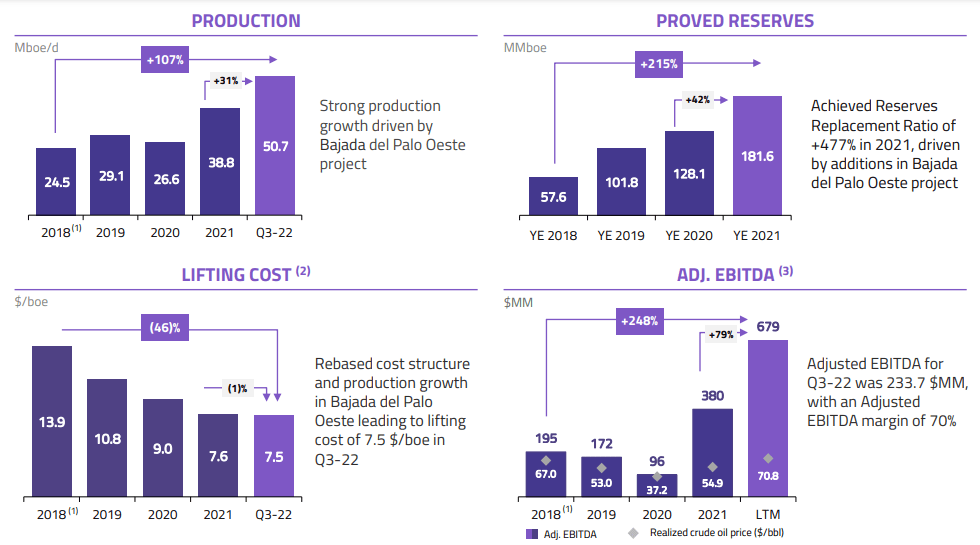

VIST Proven Reserves (Vista Energy Investor Presentation 2022)

In 2021 the company reduced emissions by 30% and has set the goal of becoming carbon neutral by the end of 2026. They have begun a large scale tree planting program, and work with environmental experts to establish healthy ecosystems around their well sites.

Statements made during the most recent earnings call indicate their recent production growth was the result of their shale oil projects. Recent test results have them increasing their estimated number of ready-to-drill inventory from 50 to up to 150 wells. This takes their total inventory to up to 1000 wells; they have only drilled and completed 74 of them. They also indicated they are expanding on their share buyback plan, increasing it from $20M to $50M.

Long-Term Trends

The global oil and gas market grew at a CAGR of 4.9% in 2022, and is projected to sustain a CAGR of 5.4% through 2028.

Financials

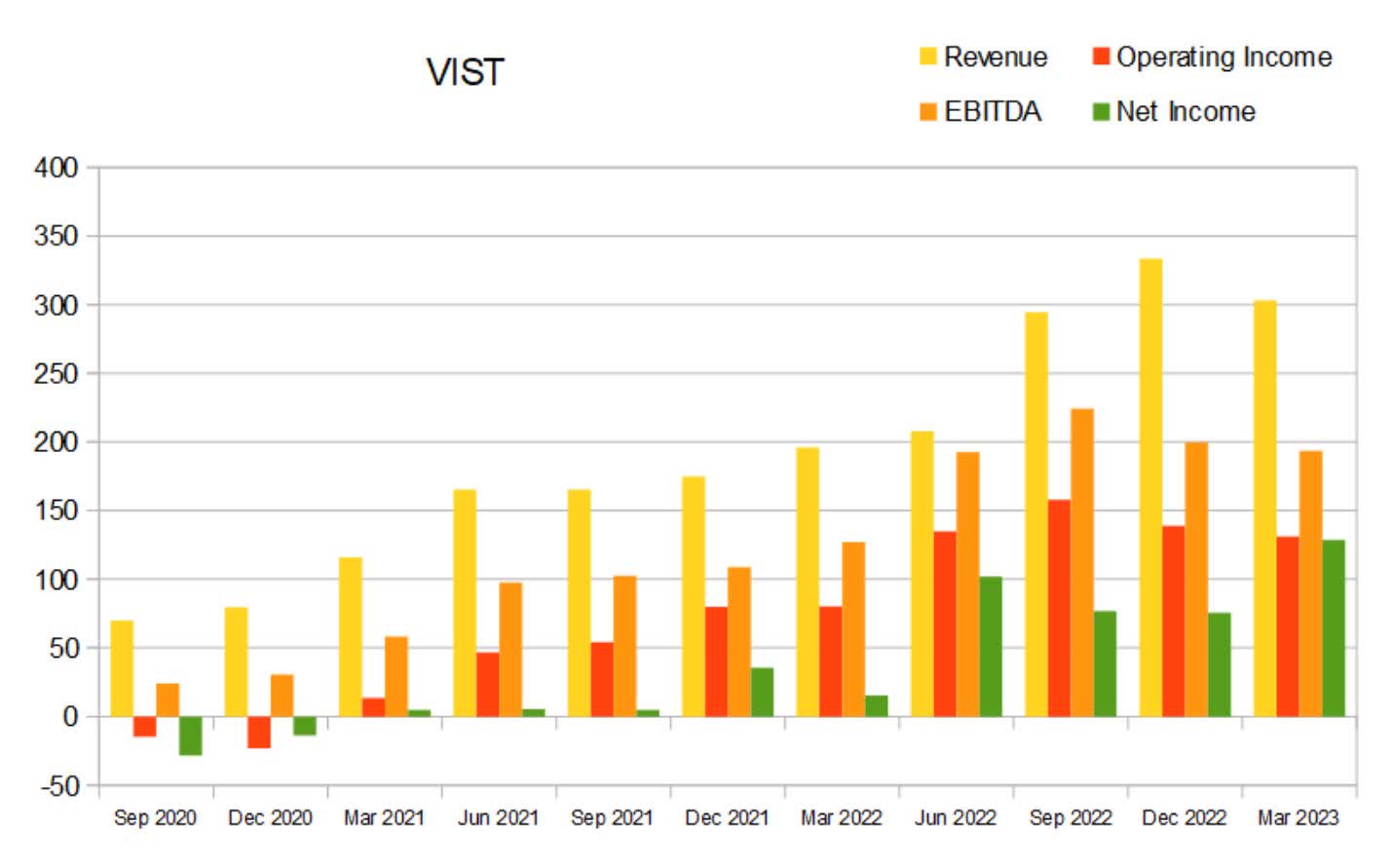

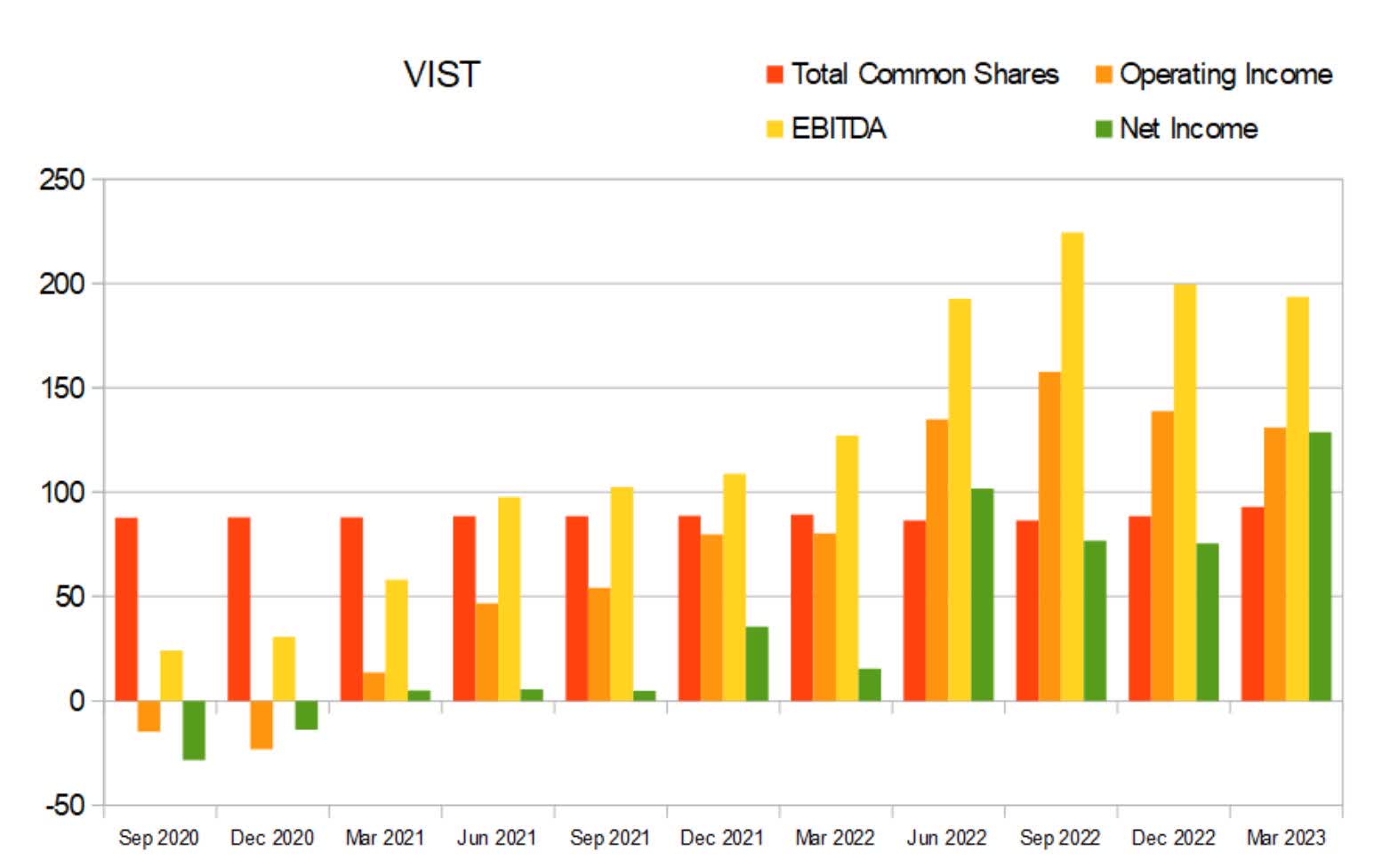

After several quarters of revenue growth, the company has finally experienced a revenue decline. Operating income has declined for the last three quarters. Net income has significant variance from quarter to quarter, but is clearly climbing.

{kind=link}

VIST Quarterly Revenue (By Author)

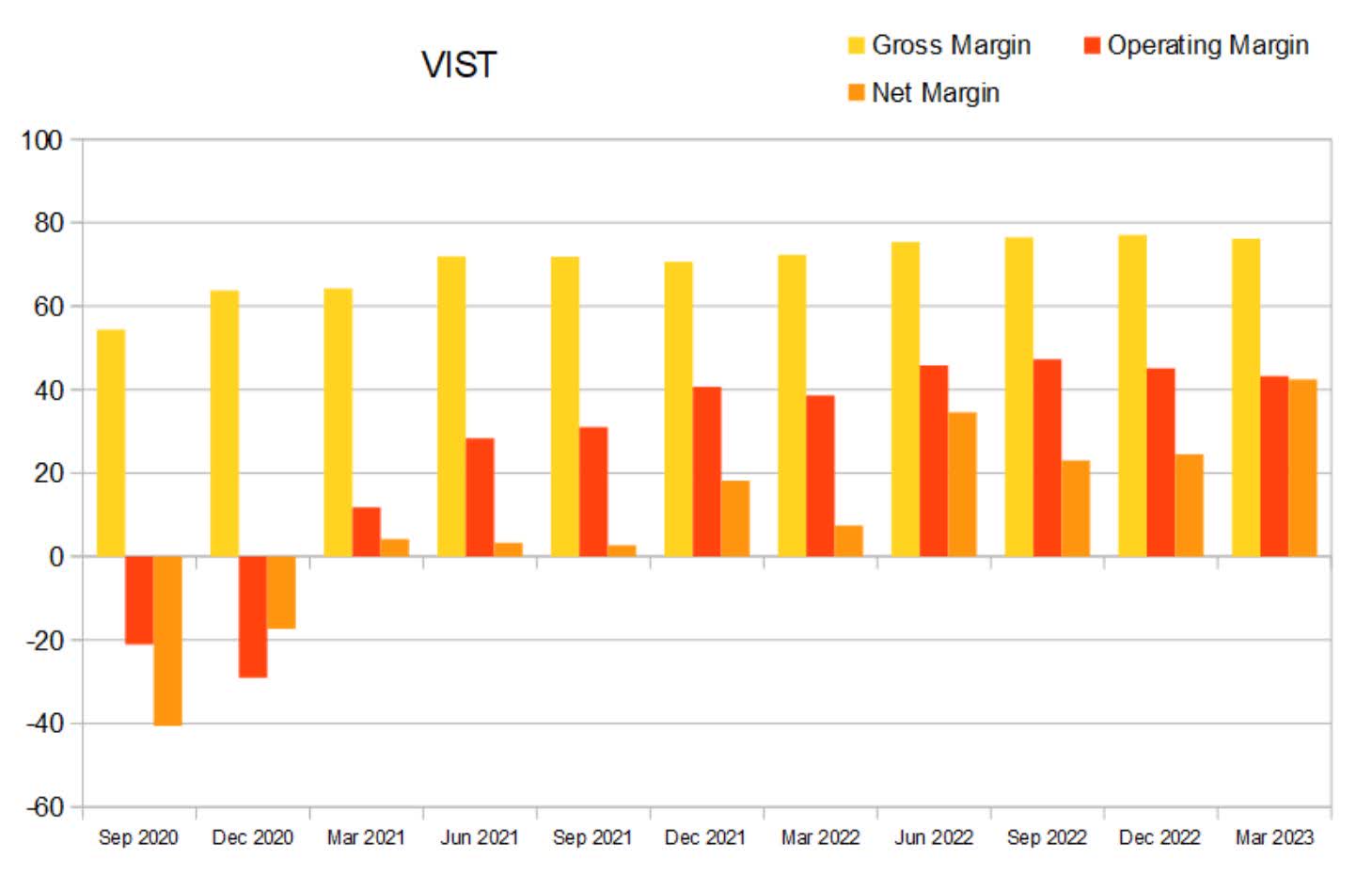

Margins also vary from quarter to quarter, but the overall picture is that they are improving. I should note that while achieving above a 40% operating margin is impressive, achieving a net margin above 40% is even more so.

{kind=link}

VIST Quarterly Margins (By Author)

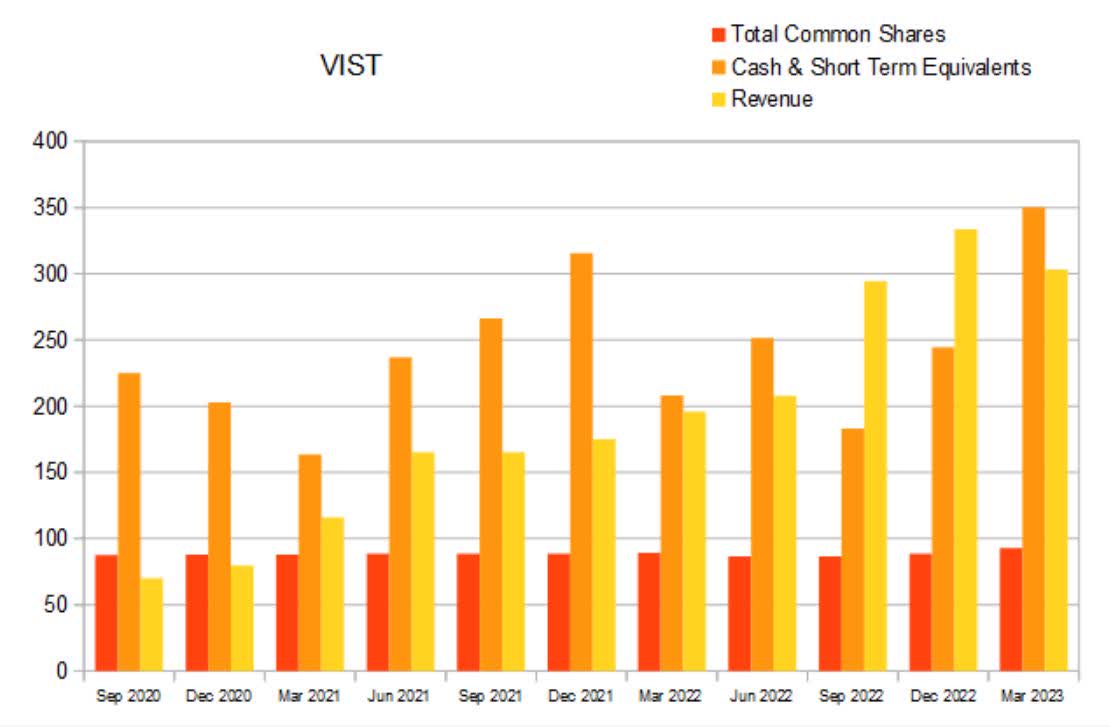

As with all growth companies it's important to take a look at the relationship between revenue and share count to see if the company is effectively translating any dilution into future revenue. When compared to their revenue growth, Vista Energy has very little dilution.

{kind=link}

VIST Quarterly Share Count vs. Cash vs. Revenue (By Author)

While the company is experiencing significant income growth, they will eventually run out of efficient places to employ their free capital, and revenue growth will decline. This is also near the point where they are likely to offer a dividend, or begin a buyback program, or both.

{kind=link}

VIST Quarterly Share Count vs. Income (By Author)

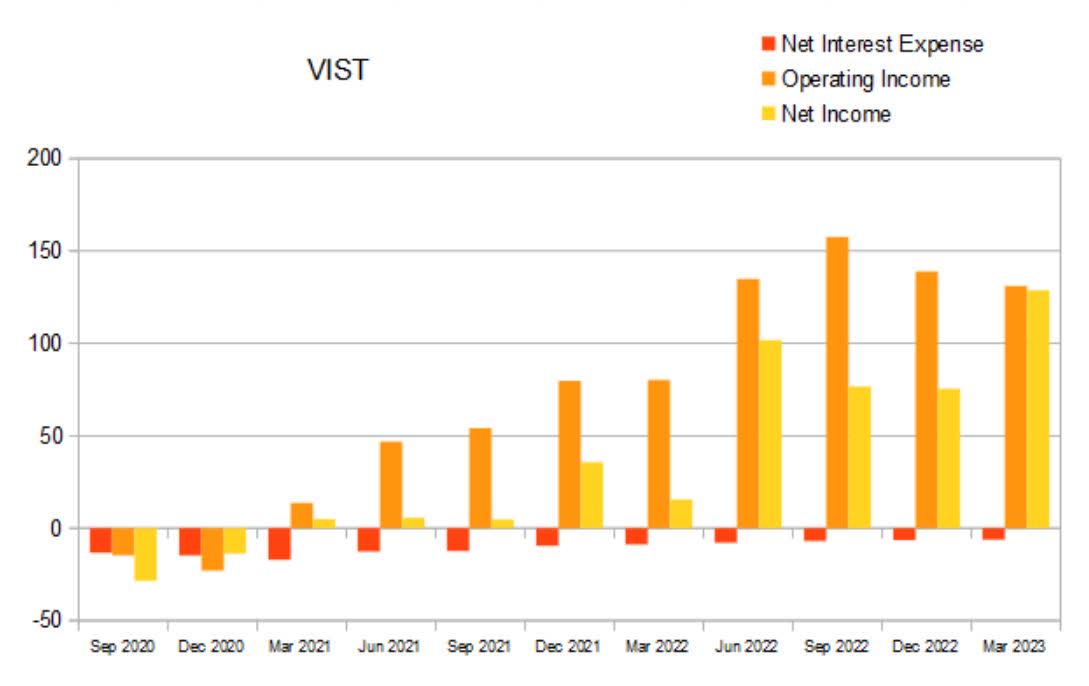

With all companies it's important to take a look at their debt burden. Vista Energy's debt situation is gradually getting better. Compared to their average quarterly income, this is a sustainable amount of debt.

{kind=link}

VIST Quarterly Net Interest Expense (By Author)

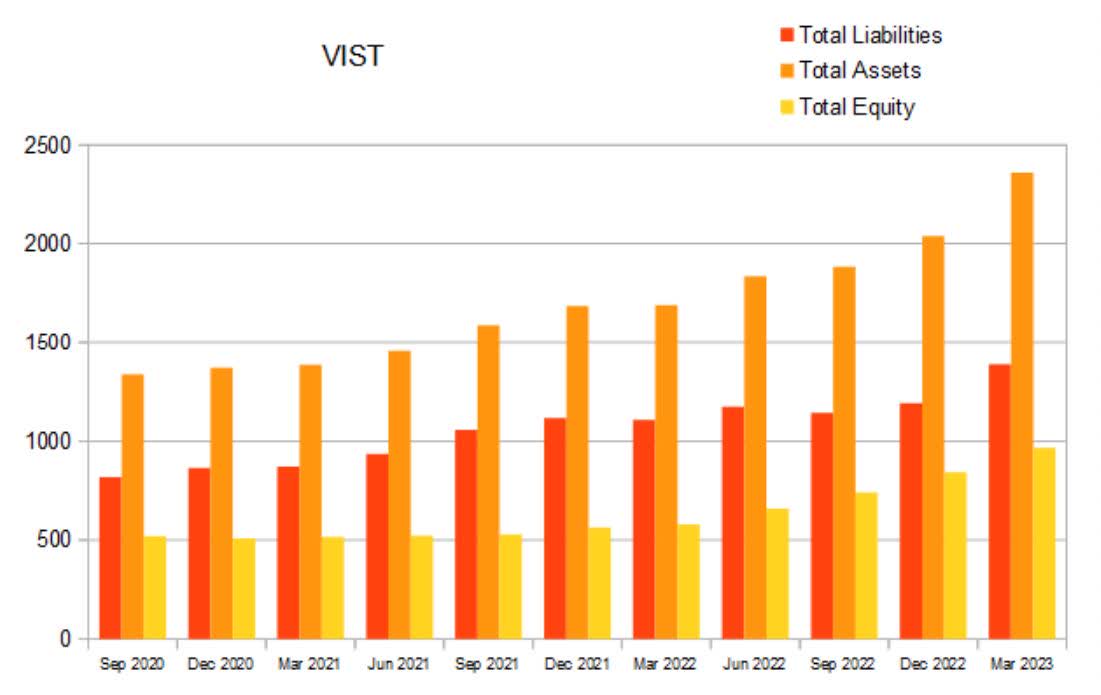

Vista Energy has an attractive equity curve. Temporary pullbacks are fine as long as the overall trend us upward.

{kind=link}

VIST Quarterly Total Equity (By Author)

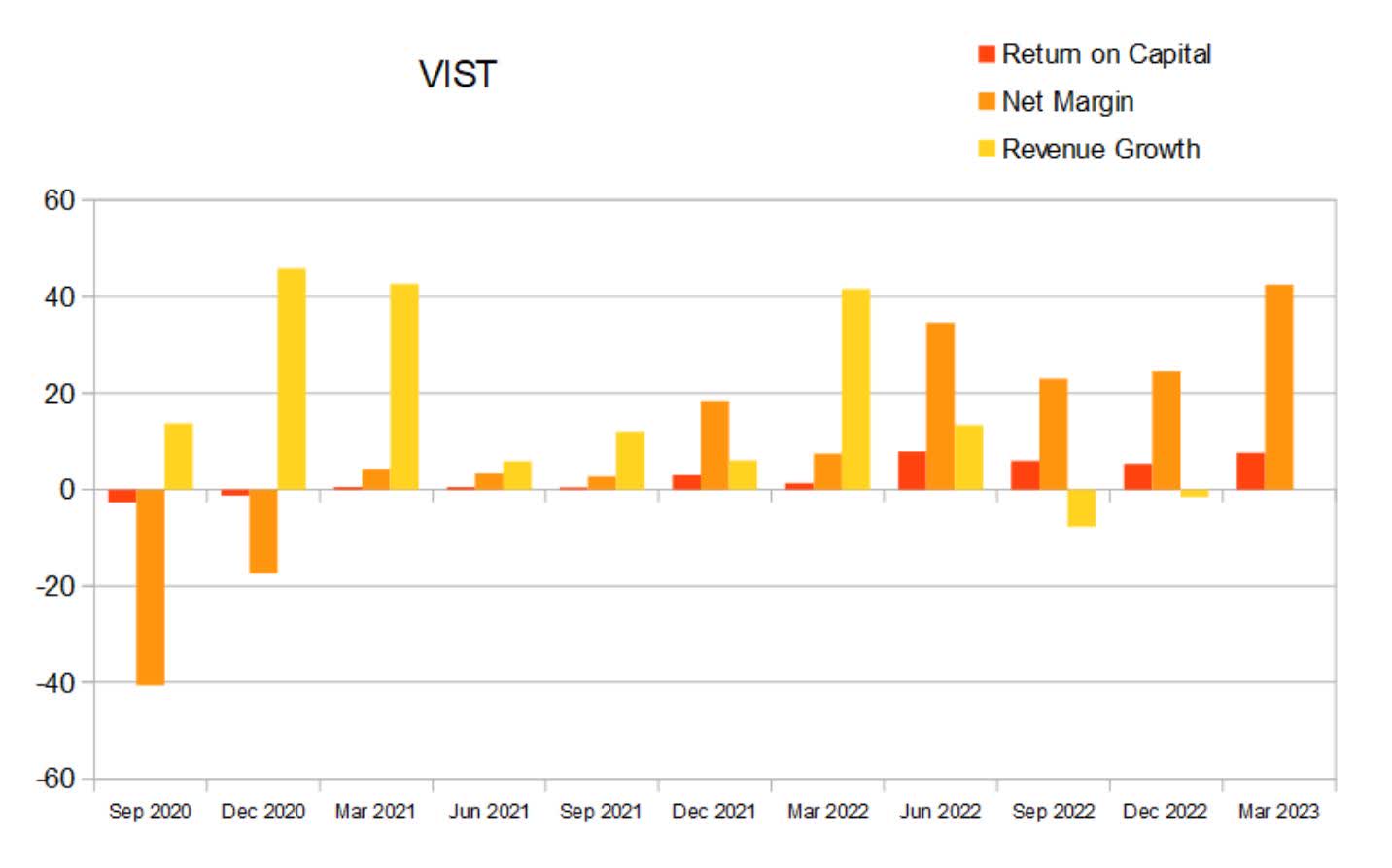

In June 2022, the company has managed to achieve a quarterly return on capital of 7.89%. In the following quarters it dipped to 5.94%, and then 5.31% before climbing back up to 7.61% this most recent quarter. These four most recent quarters have a mean of 6.6875%. If we were to use this average to calculate an annual return on capital, it would come out to 29.55%.

{kind=link}

VIST Quarterly Return On Capital (By Author)

Valuation

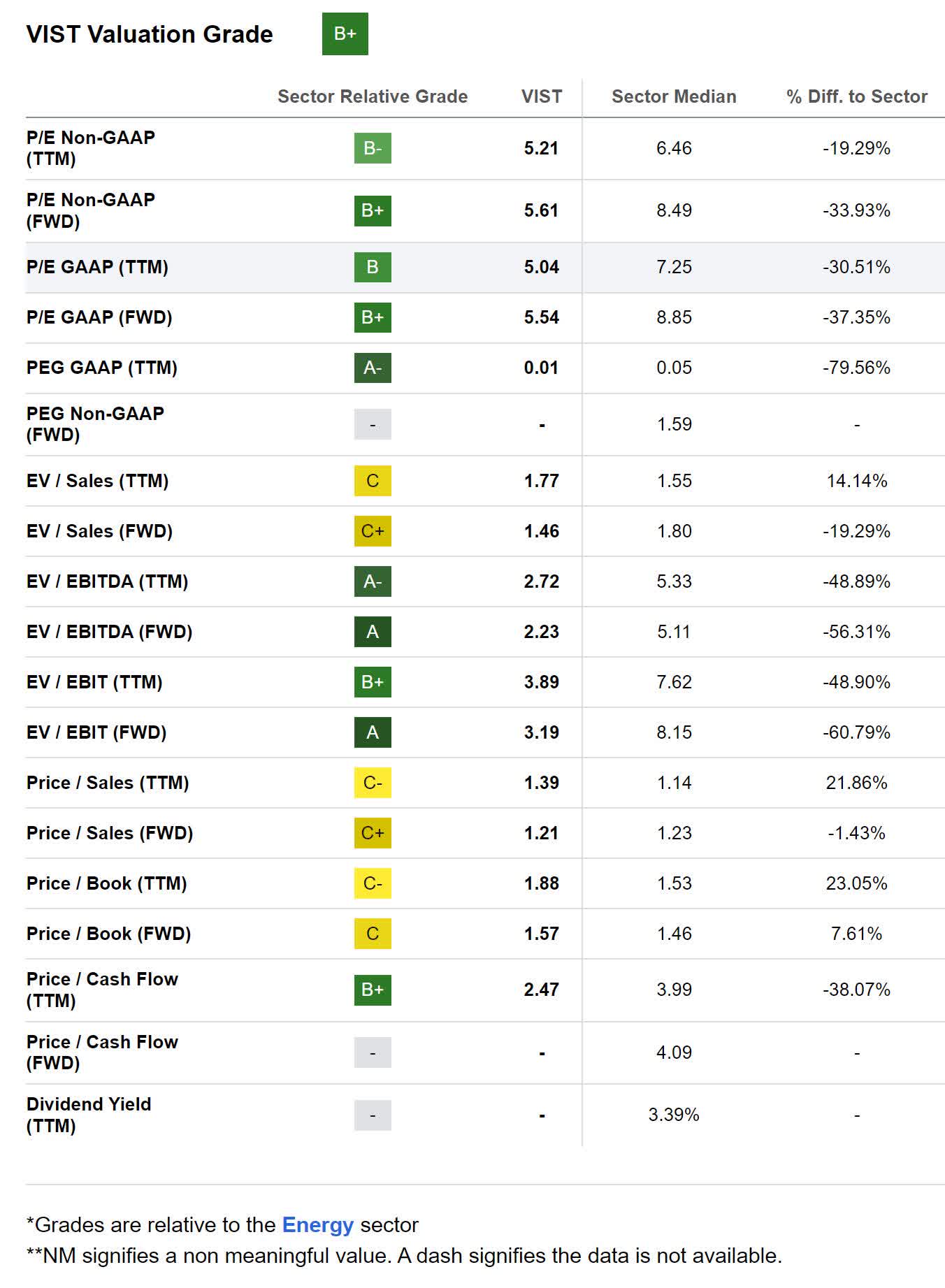

As of April 28th, 2023, Vista Energy had a market capitalization of $1.82B and was trading for $20.92 per share. The company has a forward P/E of 5.54x, a trailing PEG of 0.01x, and a forward Price/Cash Flow of 2.47x. According to its metrics, the company is currently significantly undervalued.

{kind=link}

VIST Valuation (Seeking Alpha)

I believe the company is undervalued when compared to the rest of the sector because it does not yet offer a dividend. Once it does, its valuation is likely to fall more closely in line with the sector median.

Risks

The oil and gas industry is known for being cyclical, so revenue and earnings are likely to be periodically impacted. Also, as with all energy providers and utilities, Vista Energy is at risk from operational issues ranging from things such as natural disasters and accidents.

Catalysts

Looking ahead, Vista Energy has plans to development its Vaca Muerta shale assets in Argentina. The company has a strong track record of discovering and developing new reserves. It is hard to judge how much more growth the company has planned. Until they begin offering a dividend, I expect continued expansion.

Once the company runs low on opportunities that are easy to expand into, they are likely to offer a dividend. Value investors like to use dividend growth rate as justification for purchasing, so the behavior of the share price will change as they begin regularly stepping in and buying dips.

Before I move away from risks and catalysts I want to bring up the company's goal to become carbon neutral. Not only has the company removed themselves from the risk of a carbon tax, its onset would only make them more competitive than many of their peers.

Conclusion

Vista Energy has excellent financials and appears to be undervalued. I do not know how far this initial phase of expansion will go, but when it's done I expect the company to begin paying a dividend. With this still being a relatively new company, they stand out in being able to achieve such high operating and net margins. If they sustain their high return on capital they should be able to continue growing equity. I believe this company is appealing as a long-term hold.

For further details see:

Vista Energy Is Still Undervalued