VIST - Vista Energy Q2 Earnings Preview: The Rally May Be Coming To A Temporary Halt

2023-07-07 09:00:00 ET

Summary

- Vista Energy's share price has more than doubled since October 2022, with Q2 2023 results expected to be released on 13 July.

- The company's production growth is expected to stall in Q2, with an estimated EPS of US$0.77, approximately 17% lower YoY due to lower oil prices.

- Despite impressive performance, I believe VIST share price appreciation trajectory will temporarily halt due to considerable multiples expansion and a valuation above its LATAM-focused peers.

Back in October 2022, I wrote an article about Vista Energy (VIST), rating the company as a Buy, because of its relative cheapness, compared to peers and amazing growth prospects. Since then, the share price has more than doubled and now Vista is relatively more expensive than other LATAM focused producers in terms of Forward EV/EBITDA ratio. In addition, the company is set to report its Q2’23 results on Thursday, 13 July, after the market closes. In light of this, I’m going to share my expectations about what to look for in the results as well as whether the impressive rally of the shares could continue at the same pace.

Vista Energy Q2 2023 expectations

Vista has been a growth monster with production doubling since 2020 on the back of the development of the prolific Argentinian shale formation – Vaca Muerta. However, production growth is expected to stall, at least when it comes to QoQ comparison, according to the Q1’23 earnings call :

So we are closing Q1 with an average of 52.2 in terms of production. We expect that Q1, sorry – we expect Q2 to be probably slightly lower the number since we are going to tie in.

- Miguel Galuccio, CEO of Vista Energy

So I’m going to assume around 51kboe of average daily production with 43.5kboe of it being oil, while the rest mostly natural gas. When it comes to pricing, oil prices have been slightly lower on average in Q2, compared to Q1, so I’ll assume average realized price of US$65/barrel, compared to US$66.6/barrel in the Jan-March 2023 period. It’s important to note, that the Q1’23 result included the sale of 0.23MM barrels of oil from inventory, which is obviously non-recurring and should be accounted for. For average realized prices of gas, I’ll assume US$3.5/MMBtu as they have been trending weaker throughout H1’23. When it comes to expenses, I’ve used the Q1’23 numbers as a starting point, making very slight adjustments.

| Unit |

| Revenue |

| US |

| 271 |

| Lifting costs |

| US |

| 30 |

| Depreciation |

| US |

| 65 |

| Royalties |

| US |

| 34 |

| COGS |

| US |

| 129 |

| Gross profit |

| US |

| 142 |

| SG&A |

| US |

| 34 |

| EBIT |

| US |

| 108 |

| Interest expense |

| US |

| 6 |

| EBT |

| US |

| 102 |

| Net income |

| US |

| 71 |

| number of shares |

| M |

| 92.9 |

| EPS |

| US$ |

| 0.77 |

* Author's own estimates and assumptions

The resulting EPS estimate of my calculations is US$0.77, which would be approximately 17% lower YoY, but it has to be kept in mind that realized oil prices in Q2’22 were much higher. This is a bit lower than the current analysts’ expectations of US$0.87 for EPS.

Analysts' expectations (Seeking Alpha)

What to watch for Vista's Q2 earnings call

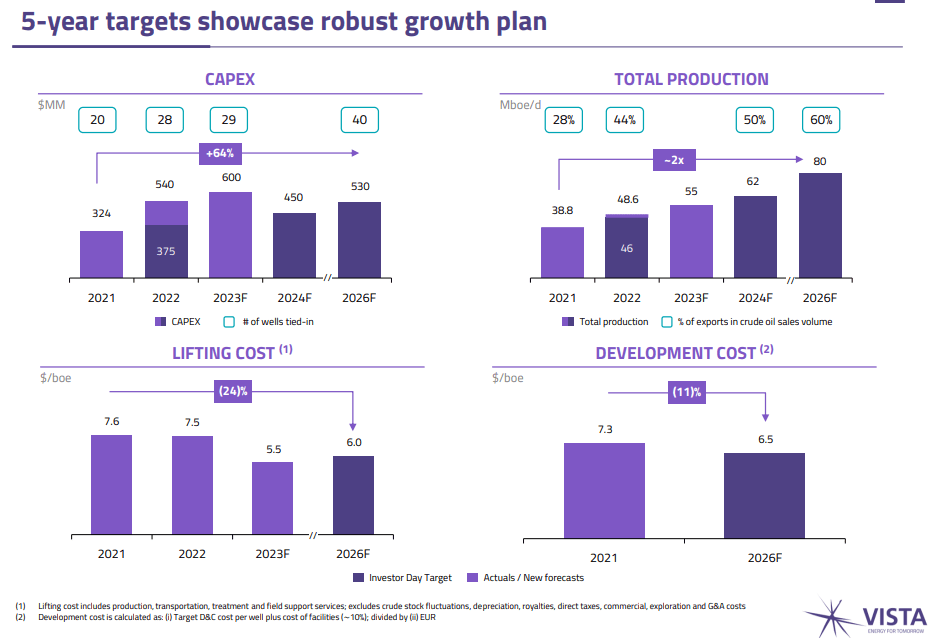

Vista Energy has the capacity to continue growing its production, with 80kboe/day rate being targeted for 2026. However, that requires the timely development of the supporting infrastructure. So the update regarding that should be quite important.

Vista's growth plan (Vista Energy)

{kind=link}

When it comes to potential news about changes in the shareholders’ return policy, I find them unlikely at this time – the company upped its buyback program to US$50M a year recently and additional increases or dividend introduction doesn’t seem prudent in the current oil price environment and considering the CAPEX needs of Vista.

VIST stock valuation

The performance of Vista Energy has been quite impressive, being up nearly 260% YoY. However, while in the meantime production growth continues, oil prices have fallen. Clearly, there’s been multiples expansion. Looking at the Forward EV/EBITDA ratio of Vista, it’s evident that it expanded and surpassed other LATAM focused oil producers, including ones with just as good growth prospects like PetroTal (PTALF), which I wrote about here .

While a Forward EV/EBITDA multiple is still low, compared to the LATAM cohort, it’s actually a bit on the high side. So for that reason, I think that the share price appreciation trajectory will come to a temporary halt and consider the stock a Hold at the moment.

Conclusion

I expect Q2’23 results to be weaker YoY, on the back of lower oil prices. At the same time, the result should still be decent, demonstrating Vista’s low cost profile. However, when it comes to valuation, Vista has undergone quite considerable multiples expansion and it currently above its peer group of LATAM focused producers. For that reason, I think it may be a time for a consolidation or maybe even a small correction of the back of profit taking.

For further details see:

Vista Energy Q2 Earnings Preview: The Rally May Be Coming To A Temporary Halt