VIST - Vista Energy: Still An Opportunity Despite Recent Appreciation

Summary

- VIST is a pure play in Argentina's Vaca Muerta unconventional basin.

- The company has expanded production, driving down operating costs per barrel and increasing efficiencies.

- My profitability models indicate adequate returns at Brent prices at or above $69, and breakeven at prices below $50.

- VIST is still investing heavily but has financed most of that investment internally, while also repaying debts, decreasing risks on a downturn scenario.

Vista Energy ( VIST ) is a company that specializes in shale oil production in the Vaca Muerta basin in Argentina.

In October 2021, I wrote a bullish article on the company (the first ever published in Seeking Alpha about VIST after its IPO). Since then the stock has returned 160%.

In this review, I provide a more complete cost model to anticipate VIST's future earnings. I believe the stock is still undervalued, and that it can still deliver an interesting return at realized oil prices (about 80% of Brent) below $55/barrel.

Note: Unless otherwise stated, all information has been obtained from VIST's filings with the SEC .

Business description

For a more detailed description, please visit my article on VIST from October 2021.

Almost pure play on Vaca Muerta shale oil : 90% of VIST's production is oil, and approximately 73% of total production is from unconventional sources.

Fast grower : Hydrocarbon production grew 24% YoY in the 9M22 period , and was 100% higher than in the same period of 2020 (50k/boe per day in 3Q22 versus 25k/boe per day in 3Q20).

Financing growth internally : unconventional exploitation requires capital because well useful life is low. This is even more true when considering production expansion. For that reason it is not strange to see the enormous levels of CAPEX sustained by VIST in the last few years. Fortunately, these have been mostly internally financed by CFO.

Low leverage and decreasing : As of 3Q22, VIST sustains a debt level of $550 million, paying an average of fixed 5.6%. Against these, it holds to reported $180 million in cash. Unfortunately, the company does not disclose how much of that cash is dollar denominated, and how much is peso denominated.

Low breakeven cost : Total operating costs per barrel have averaged $33 per boe since 3Q20. These costs include depreciation but exclude royalties at the provincial and federal level (at about 13% ad valorem average). With Argentina's export prices (Medanito or Escalante price) averaging 80% of Brent price, this implies a breakeven below $50 at the Brent level.

Positive regulatory environment : The Argentinian government is very interested in increasing oil and gas production. This was shown when the current government, considered by many anti-market in many fronts, established a $45 minimum price per barrel for oil exporters during the bear market of 2020. Another example is the preferential taxes for oil exports, at 8% ad valorem, against as much as 35% ad valorem for soybeans.

Perspectives are also positive, given that the current government is considered the most leftist in the political spectrum. Argentinian politicians tend to think in mercantilist international trade terms, and therefore most political factions want to increase oil and gas output.

Recent developments

Production keeps increasing : Quarter after quarter, VIST continues increasing its production of oil and gas, with two to three pads added per quarter. Annualized production at 3Q22 levels should reach 18 million barrel equivalents.

Expanding from Bajada del Palo Oeste : VIST's flagship property is called Bajada del Palo Oeste. This property generated more than 90% of the shale production for most of VIST's public history. However, in 2022, another two properties started exploitation at similar productivity levels, Bajada del Palo Este and Aguada Federal. The (probably) higher probed and developed reserves from these two properties have not been communicated yet.

Prices have benefited the company : In the last few quarters, VIST has been able to sell at prices around $75 per barrel. It is probable that Q4 prices will come down a little bit, given that oil prices have receded internationally. Still, the company is well above breakeven.

Scale efficiencies are showing off : While the average variable cost per barrel stood between $33 and $35 per barrel, in the last two quarters that same cost decreased to $30 per barrel.

Warrant conversion eliminates some dilution risks : VIST early investors were granted warrants convertible into 30 million shares (30% of the shares outstanding), at an exercise of $11.5. However, VIST has negotiated a cashless exchange , converting those warrants for 3 million shares, at an equivalent of $9.5 per share.

A profitability model

Some of the assumptions:

- A production as-is model, with no new CAPEX for expanded production. Depreciation can be used as a proxy for previous CAPEX because wells are depreciated using barrels produced over total expected production (this means new wells are depreciated faster as their productivity tends to decrease fast).

- Variable costs of $33 per barrel which includes all operating costs and depreciation, but does not include royalties and sales taxes.

- Royalties and sales taxes (like Argentinian export taxes) for 15% of revenue.

- A 35% income tax rate.

- $40 million in interest expenses, which covers $30 million of a 5.5% average rate on $550 million of debts, plus financing expenses in pesos. Interest expenses should decrease as debt is repaid.

With these assumptions, I create a table of expected net income, depending on realized prices per barrel and millions of barrel equivalents produced.

Net income as a function of prices and quantities (Own, based on VIST's filings with the SEC)

Additionally, this same model allows to understand the company's return on invested capital based on productivity assumptions at the well level. The table below obtains returns based on the model above, but adding two sets of assumptions: one with a cost of $10 million per well and EUR (estimated ultimate recovery) of 1.5 million barrel equivalents, and another one with a cost of $12 million and EUR of 1 million. VIST operated at the $12 million and EUR of 1 million assumption, but the company modified its expectations to the first set on its latest Investor's day . This model does not incorporate depreciation as it is cash based.

VIST's ROIC at the well level, based on oil price, well cost and EUR assumptions (Own, based on VIST's filings with the SEC)

Again, returns are more than satisfactory under current assumptions at many price levels, although much less desirable under the previous set of assumptions (higher well cost, lower EUR).

How to proxy realized oil prices : A good proxy of VIST realized prices is the Medanito price (the price at the beginning of the pipeline in Vaca Muerta). According to data from the Secretary of Energy of Argentina , Medanito prices have averaged 80% of ICE Brent futures.

Valuation

VIST currently trades at a market cap of about $1.4 billion. At current production levels, which the company plans to continue expanding, VIST would generate a very interesting accrual return at prices close to $55 local ($69 Brent).

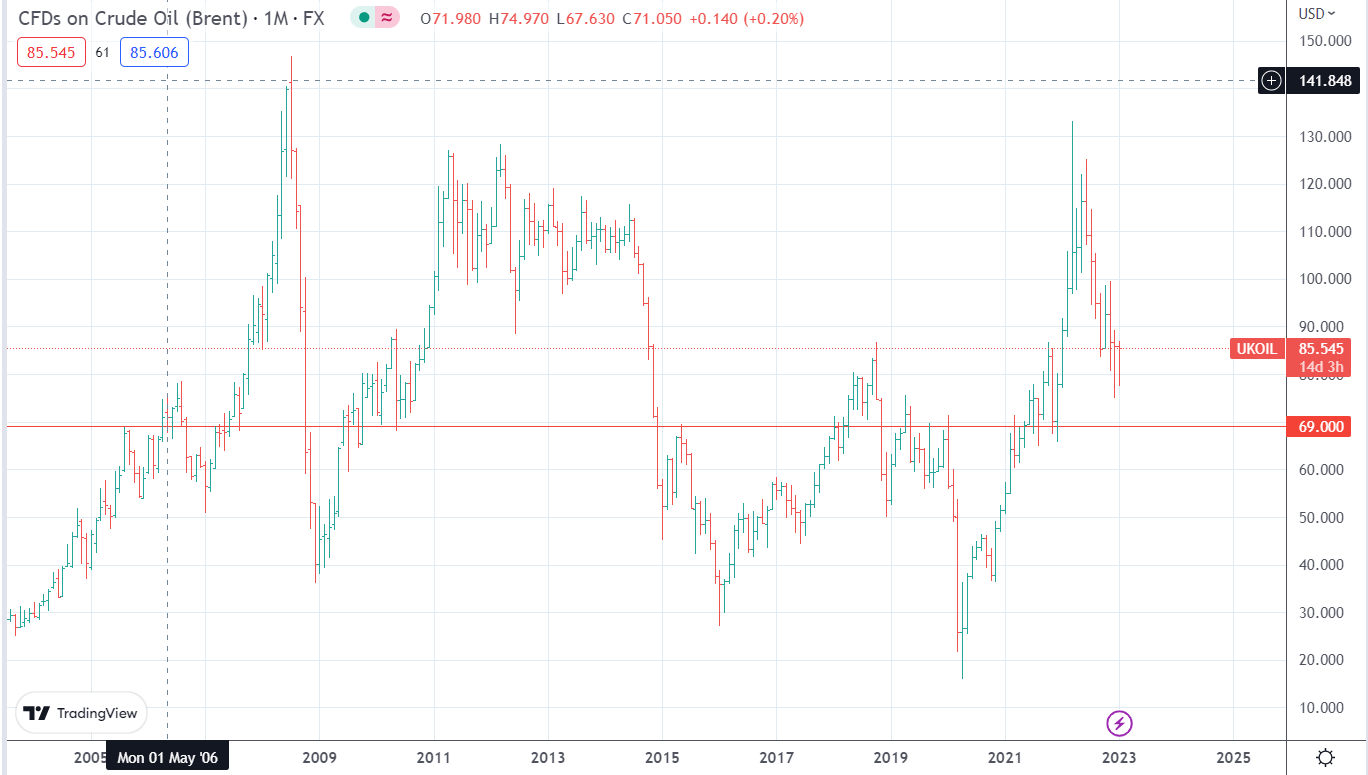

The risk of oversupply : Oil production is growing in Argentina and all around the world, as current prices make extraction profitable. VIST is indeed following the classical capital investment cycle, and could very well find itself in the midst of an oversupplied market. The $69 Brent line for an adequate return (plus a $50 Brent line for breakeven) has been surpassed for most of the current century.

Historical Brent prices, and a $69 dividing line ( TradingView )

{kind=link}

However, cash flow returns are higher than accrual returns, and therefore cash flow breakevens are lower. If the company faced lower prices, it may constrain investment and start returning capital to investors in the form of dividends or repurchases. If competitors were over leveraged, then it could invest in acquiring some of their assets.

For these reasons, I believe VIST is still an opportunity, despite having more than tripled in price since January 2022.

For further details see:

Vista Energy: Still An Opportunity Despite Recent Appreciation