VIST - Vista Energy: Still At Attractive Levels

2023-03-09 00:26:19 ET

Summary

- Vista Energy remains on an impressive growth trajectory through its exposure to the Vaca Muerta shale formation.

- 2022 average daily production hit 48.7kBOE, increasing 25% YoY and is projected to average 55kBOE in 2023.

- Exports as a total share of production continue to grow, offering higher exposure to international market prices.

- The company is trading at slightly above 2x Forward EV/EBITDA, indicating that some upside potential remains.

Back in October I wrote an article about Vista Energy, S.A.B. de C.V. ( VIST ), highlighting it as a very attractive blend of growth and value. Since then, the share price has appreciated 67%. In the meantime, the 2022 results were released, indicating that the company is on track with its ambitious production growth program. Meanwhile, Argentina looks committed to support infrastructure development in the prolific Vaca Muerta formation, which is shaping as one of the most significant shale areas outside the US. Despite the surge in price, my calculations indicate that Vista Energy is trading at slightly above 2x Forward EV/EBITDA in an above US$70/barrel oil price environment, which suggests that there’s still upside potential.

Company overview

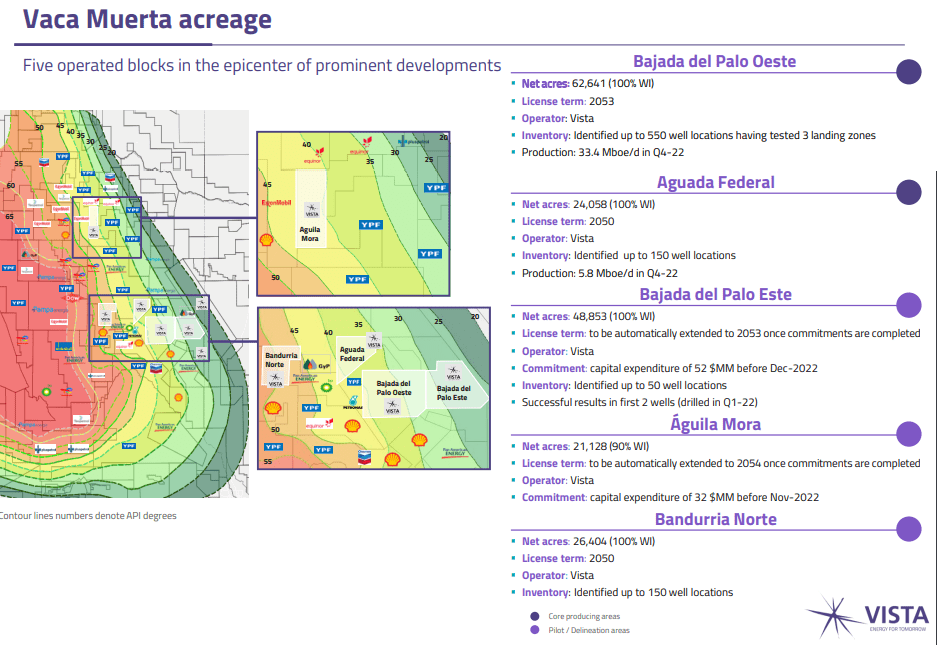

{kind=link}

Vista's assets in Vaca Muerta (Vista Energy)

Vista Energy is an oil and gas company with a primary focus on Argentina. Through its significant exposure to the Vaca Muerta shale formation, which holds one of the largest shale formations in the world and is still in development stage with lots of untapped potential. While many companies have exposure to this prolific area, including oil majors like Shell ( SHEL ) and Chevron ( CVX ), Vista Energy is pretty much the only not state-owned pure-play Vaca Muerta stock as the vast majority of its production comes from there.

Operational update

{kind=link}

Operational highlights (Vista Energy)

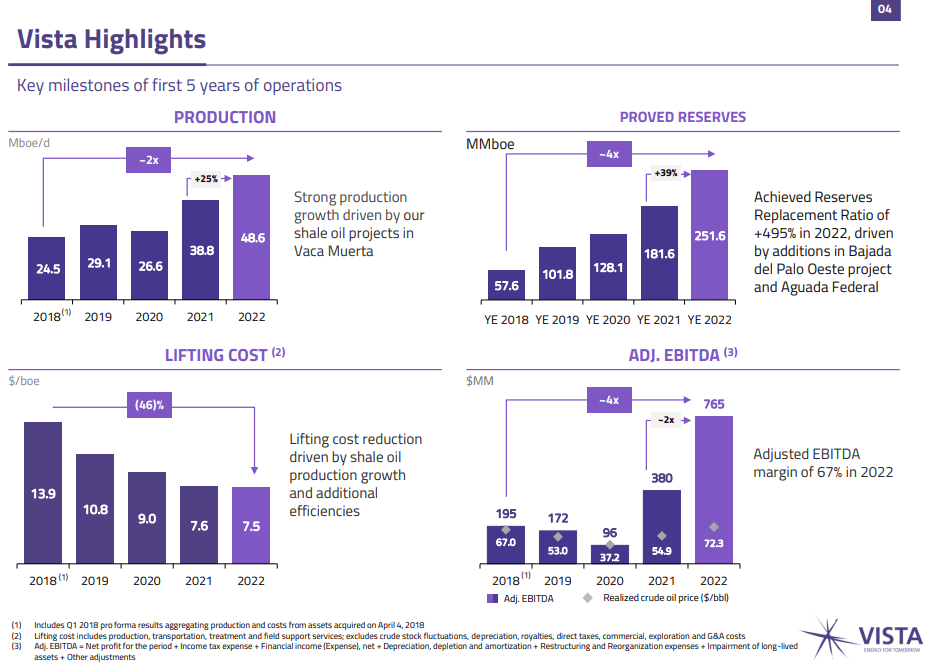

Due to its exposure to Vaca Muerta, Vista Energy is on a steep production growth trajectory. In light of that, Q4’22 total production reached 54.7kBOE/day (+33% YoY) with oil being the majority of it (45.7kBOE/day; +41% YoY). For the full year, average daily production hit 48.6kBOE (+25% YoY) with shale accounting for over 71% of it. At the same time, economies of scale kicked in and led to a decrease of lifting costs/barrel from US$8.00 to US$7.20.

Oil realization prices (Vista Energy)

In terms of pricing, the Argentinian domestic oil price, which is somewhat state-controlled and is generally lower than international markets, has continued shrinking the gap with export prices in Q4’22. 2022 average realized price was US$72.3/barrel or 32% higher YoY. This has positively impacted the cash flow generation of Vista as free cash flow grew to US$197M, compared to US$105.9M in 2021 and Adjusted EBITDA doubled to US$765M.

{kind=link}

Liquidity and debt profile (Vista Energy)

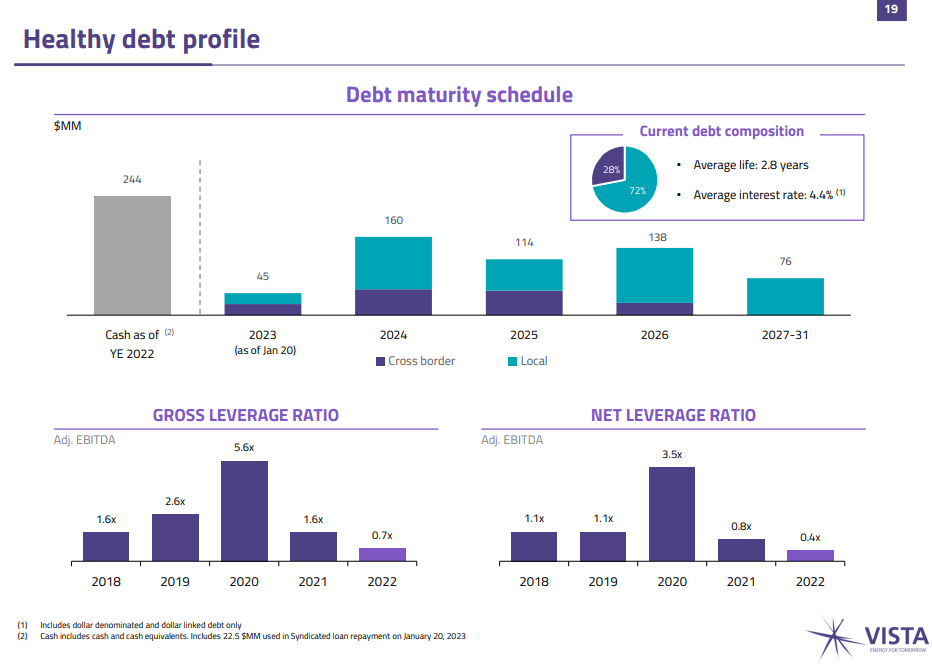

Throughout 2022, Vista Energy maintained a strong balance sheet as net debt slightly increased to US$304.9M (+3% YoY), but the surging EBITDA dramatically improved the net leverage ratio of the company from 0.8x in 2021 year-end to 0.4x in 2022 year-end. It has to be noted that the debt of Vista is spread out to 2031 as only US$45M is due in 2023. Also, over 90% of total debt is at fixed rates, making interest expenses relatively insensitive to the market environment.

Expansion outlook

{kind=link}

Expansion outlook (Vista Energy)

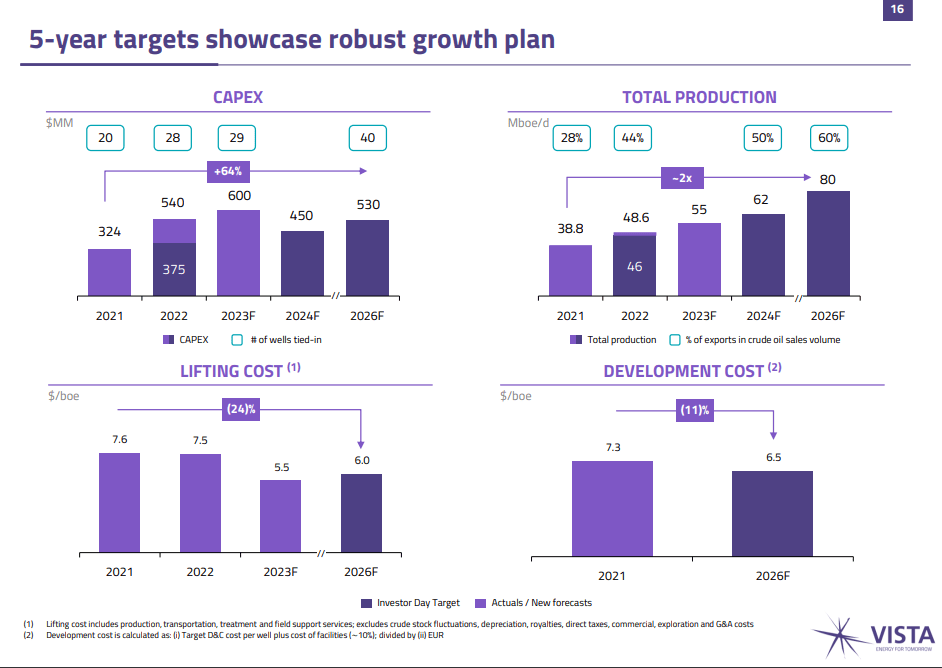

Vista Energy plans to remain on a steep growth trajectory. In order for that to happen, the company will have to spend a lot of cash on capital expenditures, projecting investments in 2023 to reach US$600M. However, the current oil price environment is supportive of such expenditures. According to 2023 guidance, production should average around 55kBOE/day and assuming average realized oil price of US$65-US$68/barrel Adjusted EBITDA should be in the range of US$850M-US$900M for the year. Note that with rising production, the share of exports, which are linked to international market prices rises, which in turn pushes the total average realization price up. In light of that, assuming average selling price of US$70/barrel, I estimate Adjusted EBITDA of around US$950M.

Production and exports' share (Vista Energy; compiled by the author)

One issue , outside Vista’s control, which may stall the production growth is the infrastructure development in Vaca Muerta. The oil that is produces has to be transferred so an adequate pipeline system must be build. In that regard, Argentina is so far supportive of the shale formation development, as it recently obtained financing for pipeline development. It appears that there’s a political consensus regarding the importance of Vaca Muerta, as part of the shale oil revenues will end up in the government’s budget.

Share price and valuation

During the past year, Vista Energy has significantly outperformed the US oil and gas sector, represented by the Energy Select Sector SPDR ETF ( XLE ). However, the impressive growth profile and prospects of Vista make the company rather an exception in the industry, as the typical oil and gas company won’t be able to achieve consistent double digit production growth for a few consecutive years.

In terms of enterprise value of Vista Energy, after the recent bull run, it stands at about US$2B. Using the midpoint of management’s EBITDA guidance of US$875M, the forward EV/EBITDA ratio stands at 2.3x. My estimate for 2023 EBITDA of US$950 indicates an even more attractive ratio of just 2.1x. This numbers are very similar to those of the state-controlled YPF and to some Colombian peers. However, in Colombia the government is notorious for its anti-oil stance and even wants to ban fracking – the very technology at the core of the Vaca Muerta’s shale boom. For these reasons, some premium of Vista Energy over the Colombian peers could be justified.

{kind=link}

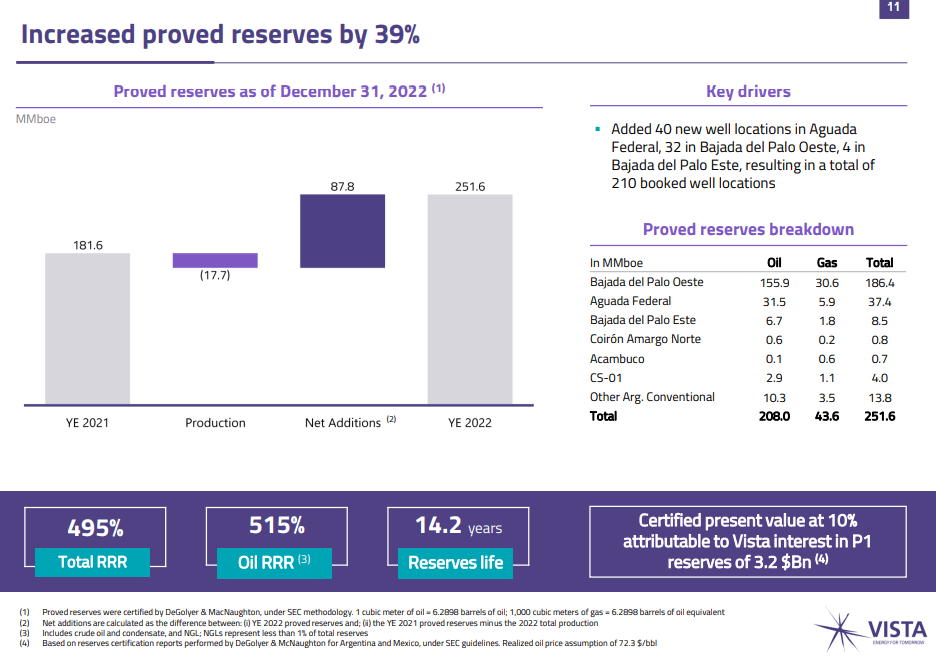

Reserves and economics (Vista Energy)

Turning to the reserves of the company, only the P1 reserves of the company have estimated NPV of US$3.2B, which implies around 70% upside to current prices.

Risks

The biggest risks for Vista Energy are related to the political risk of operating in Argentina. The country is in the bottom quartile in economic freedom , next to places like Uganda and Belarus. Domestic energy prices are controlled , resulting in suppressed oil price on the Argentinian market. On the upside, the growing production, mainly on Vaca Muerta makes the country a net exporter, which leaves more and more volumes for the international market. Also, the government looks committed to support the development of the shale formation, as it will benefit from it through tax revenues.

Conclusion

Despite the recent surge in share price, Vista Energy stock still holds upside potential as it trades at Forward EV/EBITDA slightly above 2x. The impressive growth profile and so far flawless execution of the expansion strategy still offer value to investors. At the same time, while political risk shouldn’t be neglected, it appears that the Argentinian government is pro-oil and is willing to support the development of the prolific Vaca Muerta shale formation.

For further details see:

Vista Energy: Still At Attractive Levels