VST - Vistra Energy: Buy Hold Or Sell?

Summary

- So far this year, VST has outperformed the market by around 25%.

- This outperformance has been driven by aggressive buybacks and investment spending.

- But there is a catch that makes us hesitant to jump back in.

Vistra Energy ( VST ) is a Texas-based electricity and natural gas utility company that boasts the title of the largest competitive (and unregulated) power generator in the United States as well as one of the largest competitive electricity providers in the nation. Though VST serves customers across 20 states, the bulk of the company's customers are located in Texas, which has a mixed utility market where private retail electricity providers are largely unregulated.

Though being a retail electric and natural gas ( UNG ) utility is VST's bread and butter, the company also boasts a large and growing power generation business, which includes the 75-MW battery storage facility (the largest of its kind in the world) in Moss Landing, California.

Indeed, VST is a growing player in the green energy ( ICLN ) transition, with a particular emphasis on development of solar ( TAN , RAYS ) and battery storage ( LIT ) projects.

While we like VST's business model and shareholder-friendly capital allocation, it is important to understand that the company is investing heavily in transitioning its own power generation portfolio toward zero-carbon energy sources. And it is doing so while aggressively buying back stock and paying a generous, $300 million annual dividend.

Unsurprisingly, VST has not had enough free cash flow to cover all of these capital allocation priorities and has had to increase debt over the last few years.

How long can this pattern of leveraging up to buy back stock and invest in renewable energy development last? Let's delve into the details to try to find out.

Vistra Energy Midyear Update

As previously stated, VST's bread and butter business is its retail electricity and natural gas utility segment. The company operates as a competitive, unregulated utility provider to residential and commercial customers through its wholly owned subsidiary, TXU Energy.

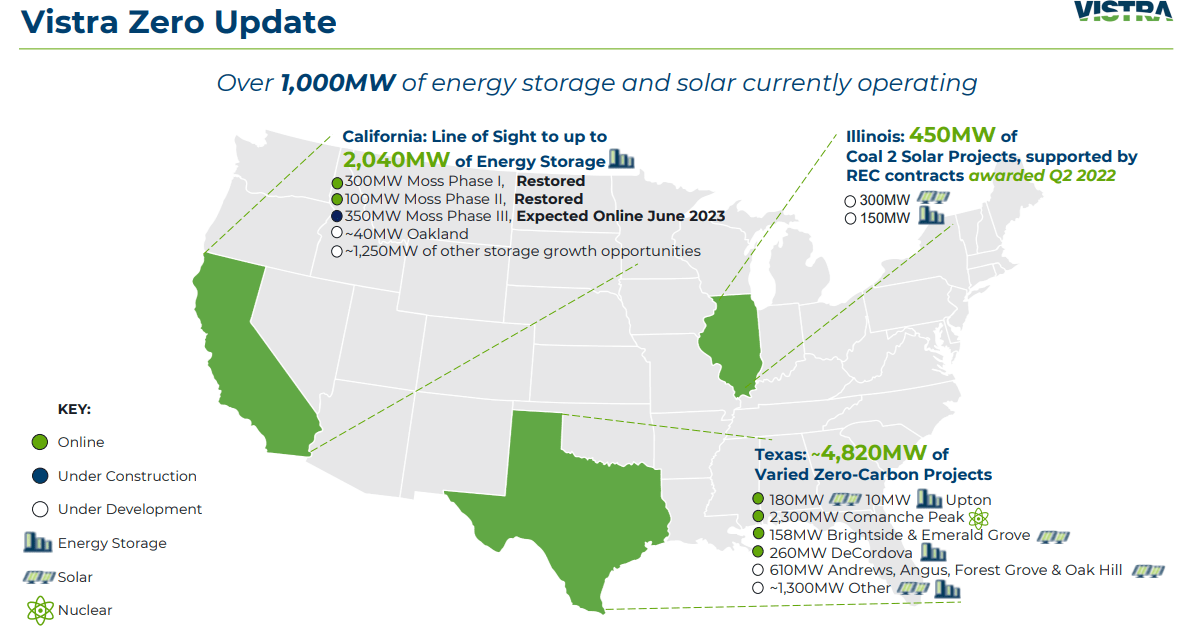

But VST is aggressively growing its power generation business segment as well, led most notably by Vistra Zero, the company's renewable energy and battery storage business.

{kind=link}

These zero-carbon projects are concentrated in Texas, California, and Illinois so far, but more states may be added to the list over time.

Despite a ~$107 million drop in operating EBITDA for VST's retail segment, the company actually grew its residential customer count and electricity sales. The decrease there is due to a one-time beneficial income boost last year.

VST Q2 Presentation

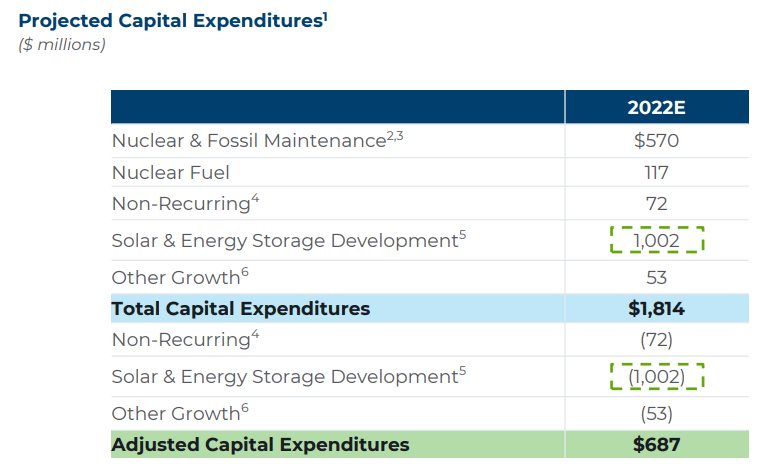

Moreover, it is important to note that most of VST's capex categorized as "growth" spending is directed toward the "Generation" segment. Two of VST's power plants ceased operations in 2022, which means that "Generation" EBITDA would have been even higher if not for these plant closures.

Indeed, most of the capital expenditures VST categorizes as "growth" investments are really just renewable energy replacements for the ~8 gigawatts-worth of fossil fuel plants it plans to retire by 2027.

That puts VST's free cash flow before growth ("FCFbG") metric in a different light. FCFbG is projected to be between $2.07 billion and $2.57 billion this year...

VST Q2 Presentation

...but that does not include the $1.05 billion of spending for "growth" projects that are mostly just replacements for soon-to-close fossil fuel plants.

{kind=link}

So that puts VST's true free cash flow ("FCF") closer to around $1.2 billion for 2022. That is how much free cash VST has to work with in order to perform the following capital allocations:

- $300 million dividend payout

- $2 billion+ in share buybacks

Now, due largely to VST's active commodity price hedging actions taken recently, the company expects adjusted EBITDA to rise to a range of $3.5 billion to $3.7 billion from 2023 to 2025. This should translate into higher FCFbG in the coming years as well. But that doesn't fix the cash shortfall this year.

From November 2021 through August 2nd, 2022, VST repurchased ~14.6% of its total shares outstanding. Management has been authorized to repurchase another $1.25 billion of shares (10-12% of market cap) through the end of 2023 (in addition to the $400 million of capacity remaining on its other buyback authorization program), but it will be interesting to see if new legislation from Congress levying a 1% tax on stock buybacks changes or slows VST's buyback plans at all.

So, where is the money coming from to cover the shortfall in FCF for VST's capital allocation priorities?

Answer: debt.

Since the beginning of 2021, long-term debt has increased by ~30% to nearly $12 billion. That is nearly half of VST's $24.7 billion enterprise value (market cap plus debt, minus cash).

This does not include the $1.3 billion that has been drawn on VST's credit facility this year. If we include that, then VST's debt to enterprise value rises to ~54%. And this, of course, is floating rate debt that had a weighted average interest rate of 4.05% at the end of the second quarter.

Fortunately, however, VST's total interest expense actually fell during Q2 because of interest rate swaps that had been in place for several years.

Management's plan is to begin deleveraging its net debt to EBITDA ratio soon, which will involve:

- Paying down $2.5 billion of total debt outstanding by the end of this year

- Raising non-recourse, project-level debt for its renewable energy assets

- Selling joint venture stakes in some of its renewable energy assets

- Maintaining net debt to EBITDA below 3x

Currently, net debt to EBITDA sits at 4.0x, excluding margin deposits. It is unclear to me whether management considers margin deposits in their target net leverage ratio. Either way, by the company's own leverage targets, VST is hitting up against the ceiling of leverage it should take on.

And yet it has $1.5 billion+ more in share repurchase capacity that management seems intent to use in the coming quarters. That could mean yet further leveraging up before the real deleveraging begins, perhaps coinciding with an increase in EBITDA and FCF in the coming years.

Investor Takeaway

This discussion should be considered in the shadow of the Inflation Reduction Act, which would have a few significant effects on VST:

- Increase and extend the tax credits available for VST's renewable energy projects

- Impose a 1% tax on stock buybacks

While it is impossible to predict the future, we believe the first point could have a beneficial effect even while the second point could cause VST's management to pull back on buybacks and to instead prioritize deleveraging. It would be a marginal shift, of course. We doubt a 1% buybacks tax would cause VST (or very many other companies, for that matter) to cease buybacks altogether.

Given how much interest rates have risen this year, we believe this could be a positive development for the safety of VST's dividend, if it plays out as we envision it.

Interestingly, both the Invesco BuyBack Achievers ETF ( PKW ) and iShares US Dividend and Buyback ETF ( DIVB ) have narrowly outperformed the S&P 500 ( SPY ) since the Inflation Reduction Act became a near-certainty.

This could be a signal that the buybacks tax will have little to no effect on management capital allocation decisions.

After a 7.5% rally this year (against the market's 16%+ slide), we remain on the sidelines for VST, at least for now. We remain bullish on the stock but believe there are better opportunities elsewhere.

For further details see:

Vistra Energy: Buy, Hold, Or Sell?