COCO - Vita Coco: Brand Momentum Can Lift Shares Higher In 2023

2023-03-09 20:57:34 ET

Summary

- The Vita Coco Company reported its Q4 earnings highlighted by rebounding margins and strong guidance for the year ahead.

- Coconut water as a health beverage category continues to outpace alternatives with Vita Coco benefiting as the market share leader.

- Even as shares are trading at an all-time high, we are bullish and see room for more upside going forward.

The Vita Coco Company ( COCO ) has established itself as the leader in packaged coconut water, proving over the past decade that strong global demand for this healthy beverage option represents a major opportunity. The company just reported its latest quarterly result, and while 2022 was defined by supply chain disruptions and higher costs pressuring earnings, improving trends and positive guidance for the year ahead was the biggest development.

We last covered COCO stock back in 2021 with a bullish note highlighting the impressive growth as an IPO with a sense that shares were undervalued at the time. The update today reaffirms that view and we see more upside even as shares are currently trading near an all-time high. Fundamentals are positive with indications the Vita Coco brand is gaining market share.

COCO Q4 Earnings Recap

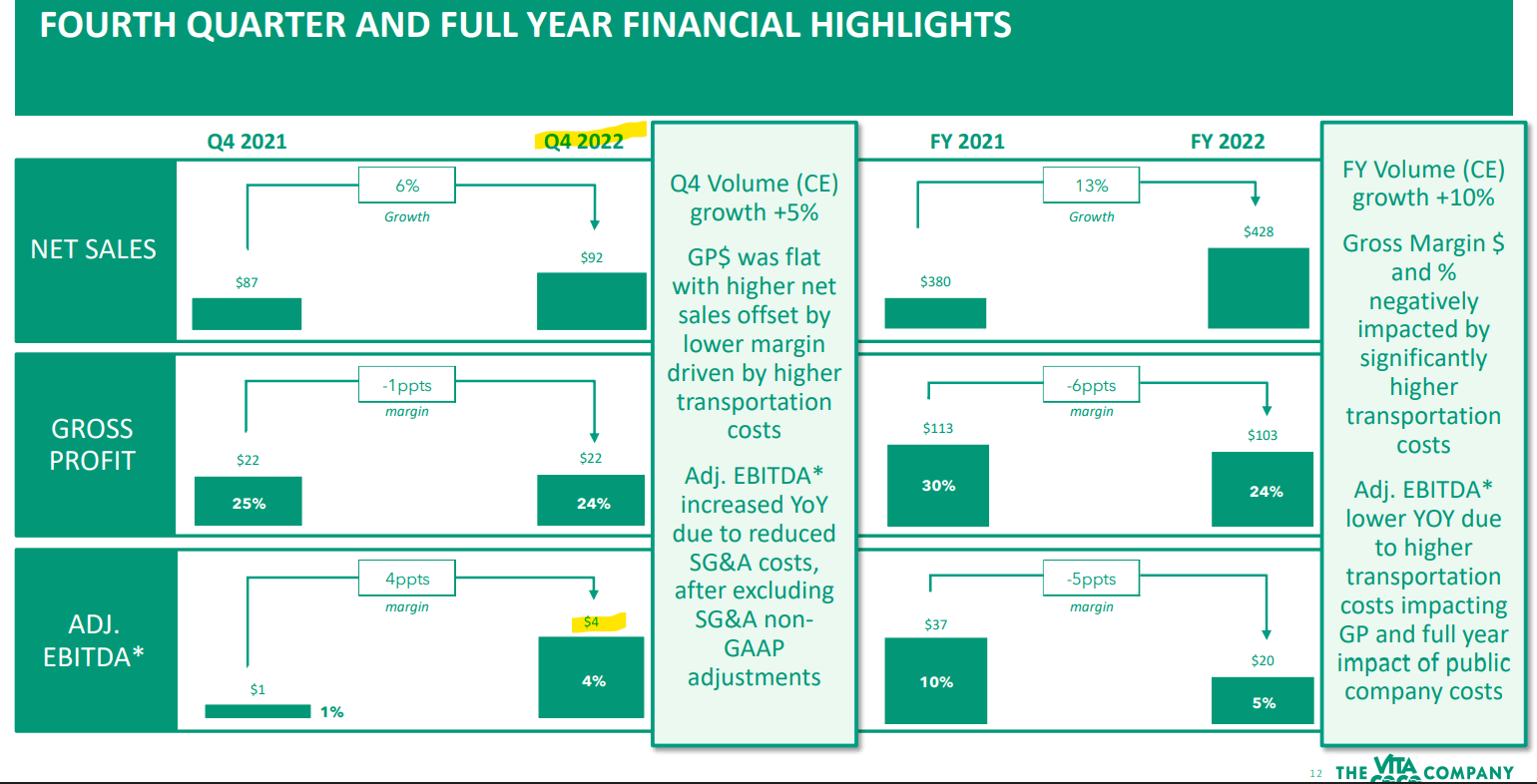

COCO Q4 EPS came in at -$0.05, $0.09 below the market consensus. The loss here is in the context of a specific impairment charge on the intangible assets related to the "RUNA" brand within the portfolio that goes back to the company's investment in the energy drink back in 2018. Simply put, this particular product has underperformed resulting in a write-off.

More favorably, the adjusted EBITDA in Q4 at $4.0 million, and a 4.4% margin reversed a weaker result in Q4 2021 when the company reported a larger loss based on inventory challenges in that period.

For Q4, net sales climbed by 6% to $92 million. Management explains that within that figure, the "core" Coconut Water has been stronger compared to some of the smaller specialty brands. The trends in North America between the U.S. and Canada have also outpaced a softer environment internationally.

{kind=link}

source: company IR

For the full-year 2022, net sales climbed by 15% while the Vita Coco Coconut Water product saw sales growth stronger at 18%, even including some FX volatility. One initiative from the company has been pricing increases which are working to support margins compared to higher transportation and logistics costs.

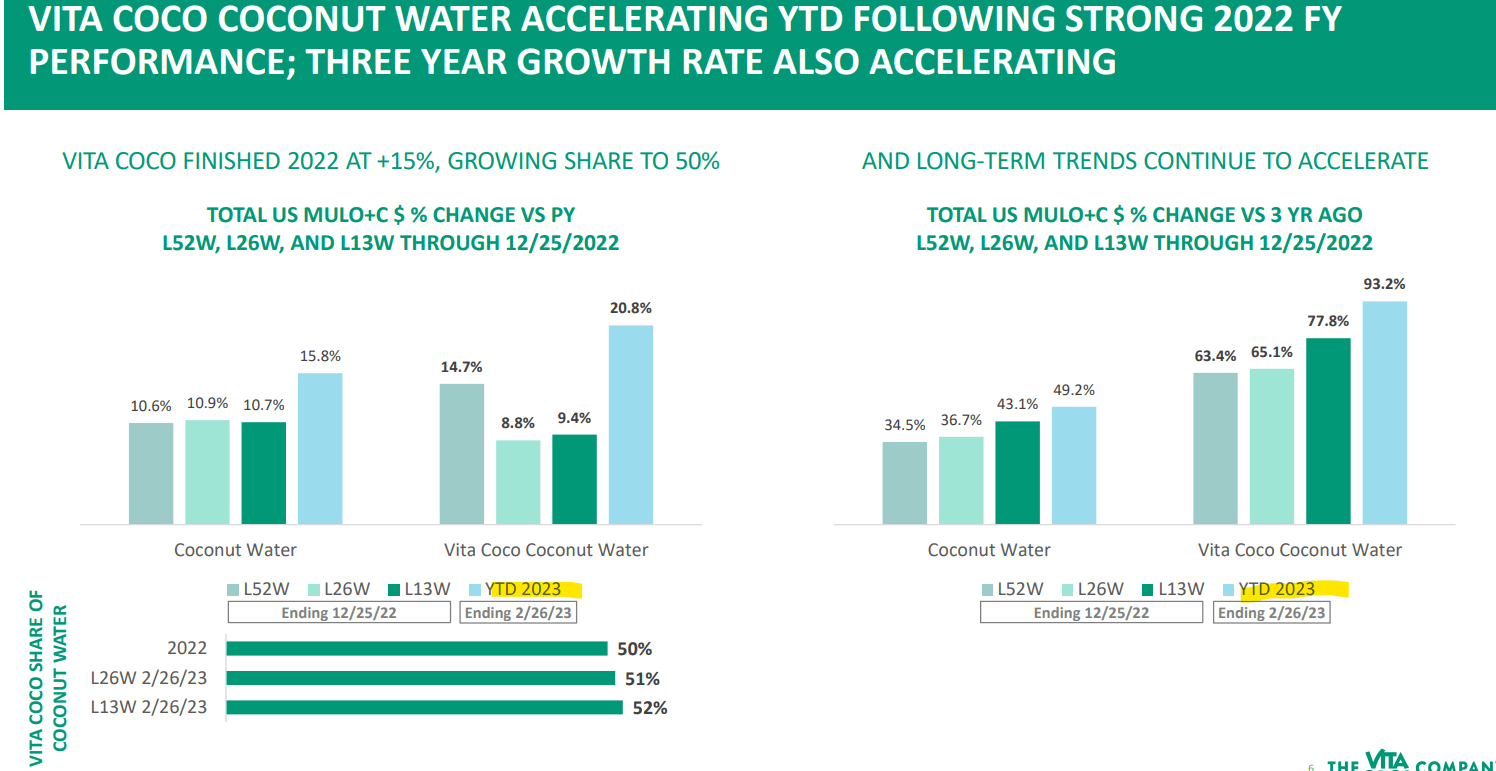

The takeaway here is that the Q4 report worked to present an improving picture of financial trends compared to a weaker first half of 2022. On this point, the early Q1 2023 data suggests a re-acceleration of growth based on the expanded distribution network. According to management, Year-to-date 2023 Vita Coconut Water sales are up in various channels like convenience stores, and grocery locations compared to the start of 2022.

{kind=link}

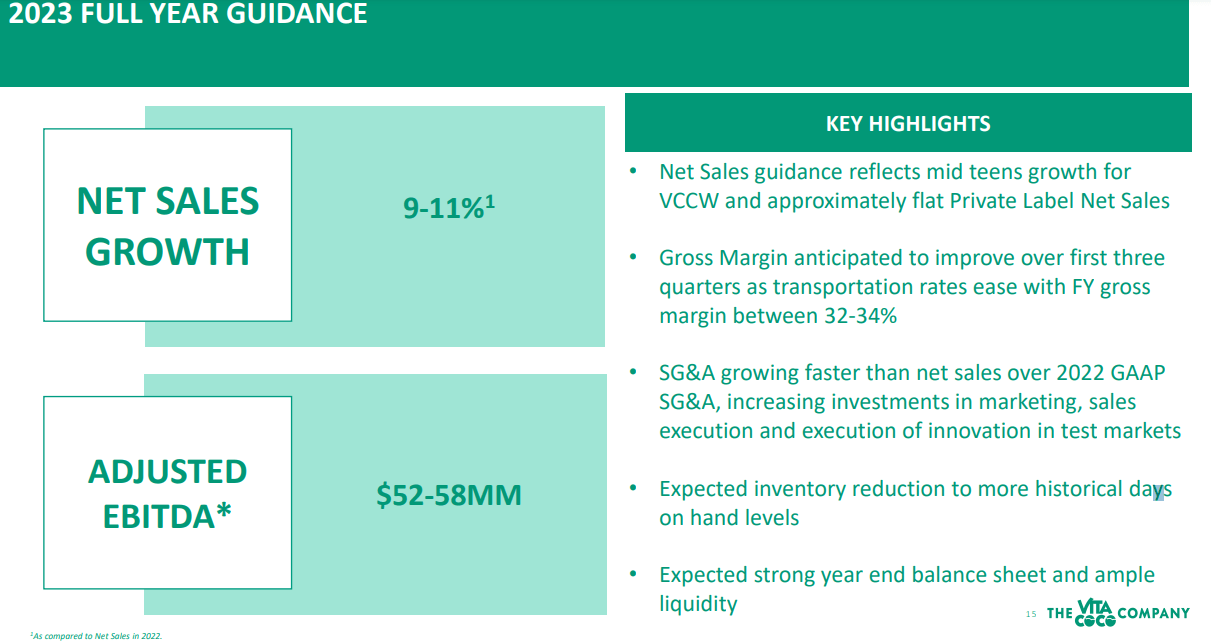

That strength is playing into positive guidance for the year ahead. Vita Coco is targeting 2023 net sales gains between 9% and 11%. The adjusted EBITDA target around $55 million, represents a 175% increase from the $20 million 2022 result. Notably, these forecasts were above prior consensus estimates which explains some of the post-earnings strength in the stock with shares rallying on the report.

{kind=link}

source: company IR

Is COCO a Good Stock?

There's a lot to like about Vita Coco which checks off several boxes in what we would consider a high-quality stock. The company is an established market leader in a differentiated product category benefiting from long-term growth tailwinds. Fundamentally, the balance sheet with more than $20 million in cash has no debt is a strong point in the investment profile. A path for earnings to climb higher beyond 2023 should allow shares to continue delivering positive returns.

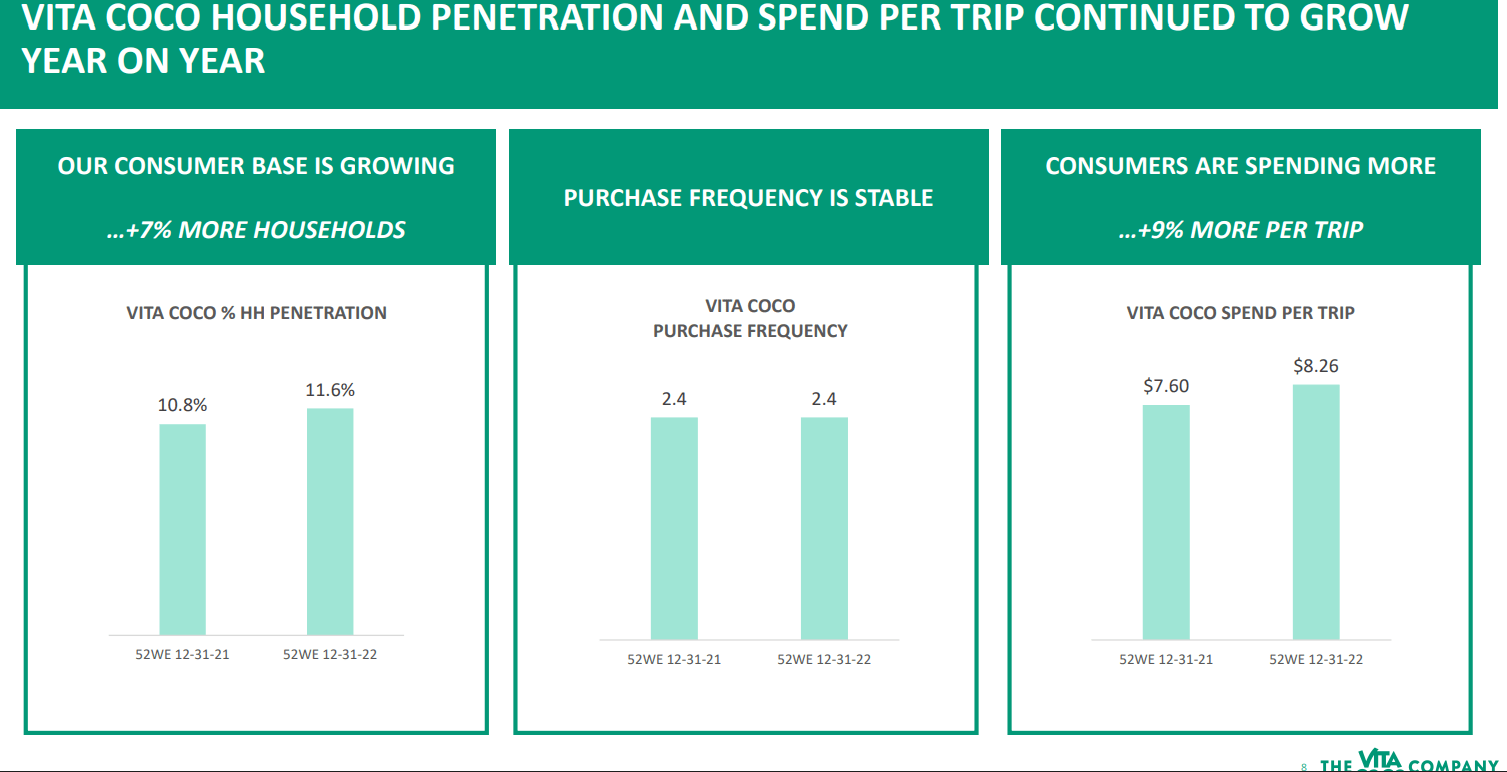

While the theme isn't necessarily new, consumers seeking more health-focused foods and organic options continue to be a growth driver. The company shares data that household penetration has climbed over the past year, with the average spending on Vita Coco increasing into bulk purchases like multi-serving cases.

{kind=link}

source: company IR

Our interpretation is that brand loyalty is strong, and once people try the product, a growing number convert into lifelong customers. The ability to mirror these dynamics in other markets outside the U.S. supports a positive long-term outlook. There is also specialty flavored brands and private label business that offer further strategic flexibility.

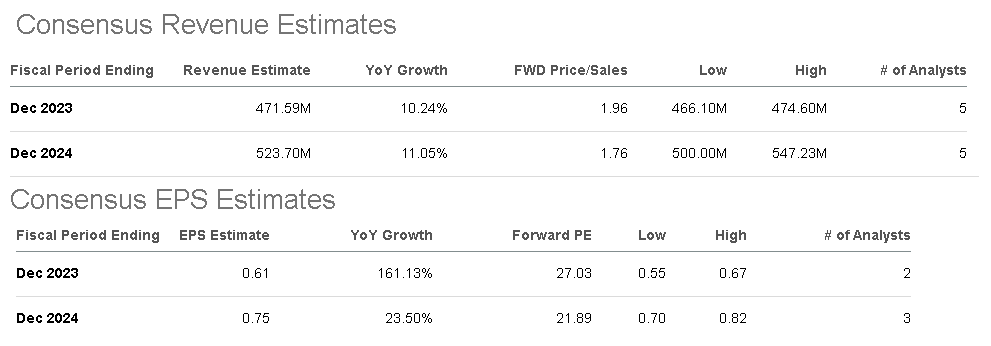

These factors are captured in the current consensus estimate for 2023 and 2024 annual revenue growth above 10%. The earnings rebound is evident through the market forecast for 2023 EPS to reach $0.61, up 161% from 2022. That momentum should be maintained into 2024 when EPS can climb towards $0.75 based on firming margins.

{kind=link}

Seeking Alpha

In terms of valuation, assuming management's 2023 EBITDA guidance, COCO trading at a 20x EV to forward EBITDA multiple appears attractive next to a group of pure-play non-alcoholic beverage stocks like Monster Beverage Corp ( MNST ) at 24x, National Beverage Corp ( FIZZ ) at 22x, or even Celsius Holdings Inc ( CELH ) at a higher 44x multiple.

Again, each of these companies focuses on different segments through various business models, but we can say that COCO stands out with the highest 2023 earnings growth expectations that can justify a higher premium.

COCO Stock Price Forecast

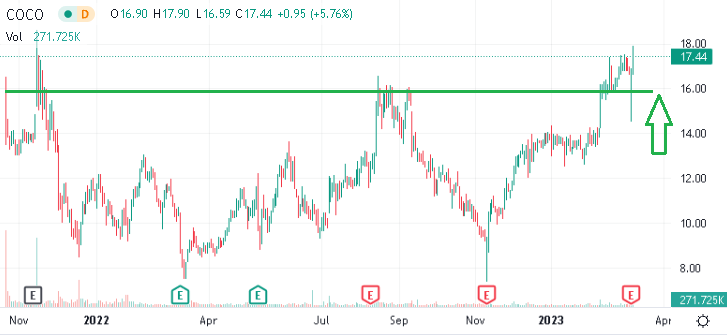

We rate COCO stock as a buy with a price target for the year ahead at $22.50 representing a 35x multiple on the current consensus 2023 EPS. From the stock price chart, it's encouraging to see shares break out toward the all-time high that was set around the time of the IPO in November 2021. In our view, the latest operating trends and earnings momentum suggests the outlook is stronger than ever today.

The way we can get to our price target this year will be through a string of solid quarterly reports confirming the brand momentum is capturing the global growth opportunities with expanding distribution.

On the downside, outside of disappointing results, a deeper deterioration in the economic environment would pressure sales trends, opening the door for renewed volatility in the stock. The adjusted EBITDA margin is a key monitoring point. It will be important for the stock to hold the $16.00 share price level as an area of support.

{kind=link}

Seeking Alpha

For further details see:

Vita Coco: Brand Momentum Can Lift Shares Higher In 2023