COCO - Vita Coco: Ignore The High Valuation And Keep Buying

2023-08-10 12:01:18 ET

Summary

- Consumer demand for coconut water is growing rapidly and COCO now has a 50% market share in the US and a dominant international presence.

- COCO's margins have improved significantly in 2023 amid a decline in inflation, endearing the stock to investors who have bid it up more than 100% YTD.

- Despite a high valuation, COCO could continue going higher due to its ability to drive volume growth and at the same time increase prices.

- COCO's future growth prospects are bolstered by its move into adjacent sectors in the beverage market such as alcoholic drinks.

- The stock could be a potentially rewarding investment for investors willing to take the risk of buying a richly valued company with a limited operating history as a publicly traded company.

Consumer demand for coconut water in the US and globally has exploded in the past decade, in line with consumers’ growing preference for anything perceived to be natural and healthy. The size of the US market, as measured by total revenues, steadily increased from $350 million in 2013 to $1.49 billion in 2022, according to data from Statista , which projects total industry sales in the US to reach $2.08 billion by 2024. Globally, coconut water sales are expected to reach $8.3 billion this year.

US coconut sales growing (Statista)

One of the major beneficiaries of the coconut water industry’s robust growth is The Vita Coco Company ( COCO ). Founded in 2004, the company produces its eponymous coconut water brand Vita Coco, which had an approximately 50% market share in US as at December 25 2022, according to the company’s form 10-K . Styled as a premium lifestyle drink, the Vita Coco brand also has a loyal following internationally, including in the UK where it has an 82% market share, according to company filings. The brand is available in over 30 countries, with its primary markets in North America, the United Kingdom and China.

Margins recovering amid continued topline growt h

COCO’s brand leadership in the fast-growing coconut water category has resulted in phenomenal commercial success, with revenues , net income and EPS having grown steadily in recent years.

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| Revenues |

| $427.8 M |

| $379.5 M |

| $310.6 M |

| $283.9 M |

| Cost of revenues |

| $324.4 M |

| $266.4 M |

| $205.8 M |

| $191.0 M |

| Net income |

| $7.8 M |

| $19.0 M |

| $32.7 M |

| $9.4 M |

| EPS |

| $0.14 |

| $0.35 |

| $0.56 |

| $0.17 |

As the table above illustrates, COCO’s revenues have grown at a healthy clip over the past four years. However, in 2021 and 2022, cost of revenues increased significantly due to inflation, which resulted in higher importation and transportation costs (it imports all its coconut water via seaborne routes). This surge in costs offset the increase in revenues in 2021 and 2022, leading to a decline in net income and EPS in both years.

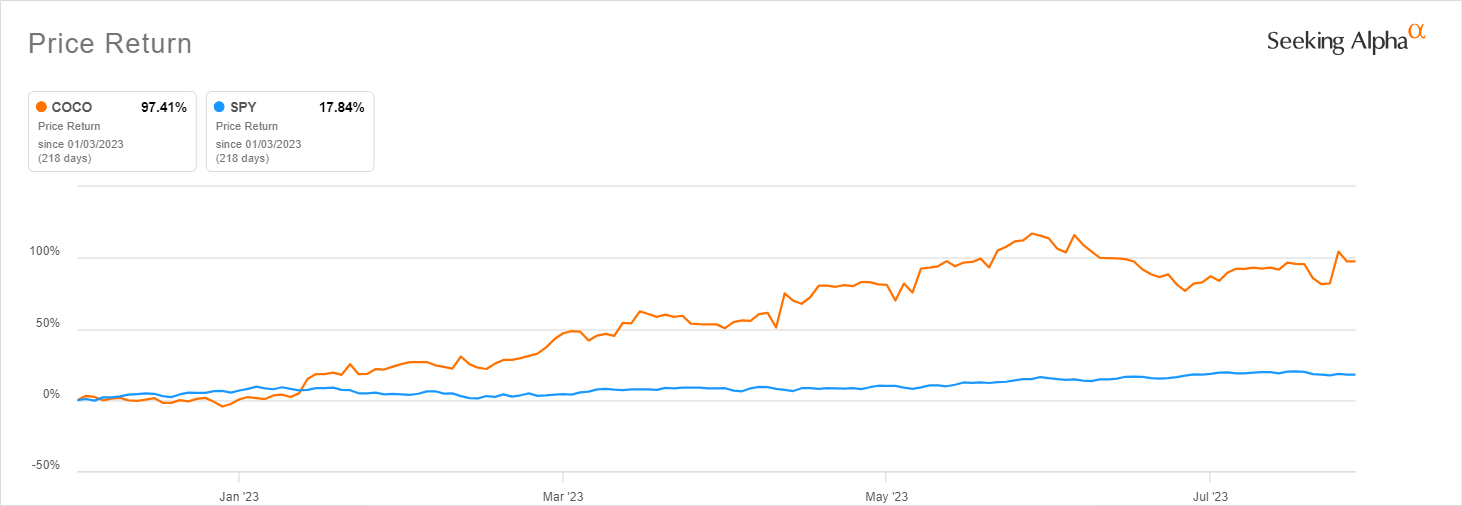

Now that inflation has eased, COCO’s margins are improving. For the second quarter ended June 30 , gross margin increased approximately 11 percentage points to 36.6% as compared to 25.4% in Q2 2022. Similarly, Gross margin for the first half of 2023 increased to 34.0% as compared to 22.8% for the first half of 2022. Investors have taken note of these improvements and the stock's movement seems to reflect this renewed optimism. YTD its up a whopping 97%, dwarfing the S&P 500’s 17.84% return over this period.

{kind=link}

Investor confidence has been strengthened by the management’s bullish guidance. In the Q2 earnings call , the company raised its full-year net sales guidance to growth of 10% to 12% year on year. It also expects continued improvements in margins and adjusted EBITDA. “We expect gross margins in the second half to improve slightly over Q2 and be between 35% and 37% for the full year. Our revised non-GAAP adjusted EBITDA guidance is $56 million to $60 million,” noted Corey Baker, CFO, on the earnings call.

The big question for existing and potential investors is whether the stock can record continued gains in coming quarters after having close to doubled since the year started. Looking at the valuation , one may be tempted to stay away and look for capital gains opportunities elsewhere. COCO is trading at a forward P/E of 37.12x and a forward EV/EBITDA of 24.41x. The consumer staples sector's median forward P/E is 20.19x and forward EV/EBITDA is 11.79x, suggesting that COCO is among the more highly valued stocks in the consumer staples sector. While this can be interpreted as a sign that the stock has limited upside, I hold the contrarian view that COCO’s rich valuation signifies the huge unlocked value in the stock, which I view as a potentially rewarding long-term buy.

Making sense of the high valuation

Buying a stock with a high valuation is risky if the company’s future growth prospects do not match investors’ elevated expectations. In my view, COCO’s future growth prospects are strong and could in fact exceed investors’ expectation due to the quality of the growth the company is generating. This makes the stock relatively safe despite its rich valuation.

To assess the quality of growth, its first important to look at the building blocks of revenue —that is, price and sales volumes. When a company is able to grow its revenues by increasing both price and volumes, it is a strong bullish sign as it indicates both pricing power and brand strength. COCO has been able to do precisely this. Its 10-Q shows that it sold 27.23 million case equivalents ((CE)) in the first half of the year vs 24.04 million CEs in the first half of 2022, a 13.2% year on year growth. A CE is a standard volume measure used by COCO’s management and is defined as a case of 12 bottles of 330ml liquid beverages. Interestingly, amid the volume growth, the company implemented several price increases, underscoring the consumer brand loyalty it has managed to build with the Vita Coco brand. Typically, there is an inverse relationship between unit price and sales volume in the consumer staples sector, so seeing volumes grow at a time of price increases is a positive sign.

The fact that COCO is growing revenues through a combination of price increases and volume growth amid a normalization in costs and improvement in margins is highly bullish for the stock. It could lead to faster-than-anticipated earnings growth, helping to push the stock higher despite the current high valuation.

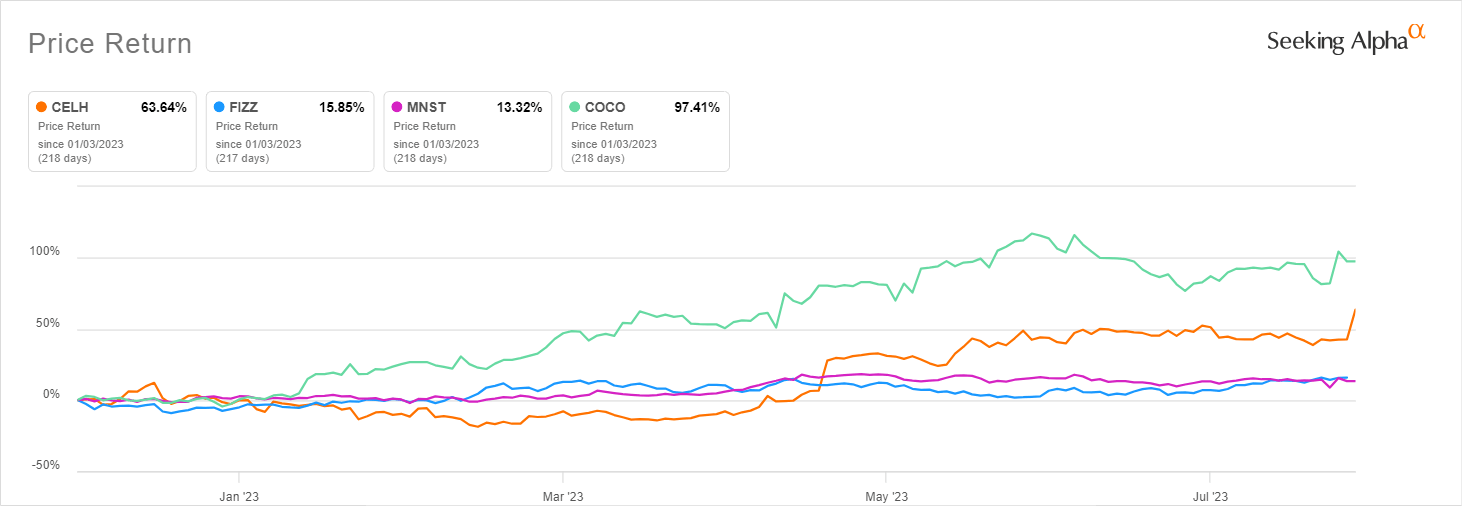

Another important factor to think about when looking at COCO’s valuation is the history and valuation of other similarly successful companies in the broader functional beverage market. These include the likes of Celsius Holdings ( CELH ), National Beverage Corp. ( FIZZ ), and Monster Beverage Corporation ( MNST ). All these companies have made a mark on the beverage industry by tapping into the growing demand for functional beverages. Interestingly, they have all performed well YTD, with COCO leading the pack and CELH closely after investors aggressively bid up the stock following its impressive Q2 earnings when it more than doubled sales.

{kind=link}

Because of these strong rallies, COCO and its peers all have high valuations. Compared to COCO’s forward P/E of 37.12x, FIZZ has a forward P/E of 29.43, MNST of 37.66 and CELH of 103.04. COCO’s forward EV/EBITDA of 24.41 is higher than FIZZ’s 20.23 but lower than MNST's 26.96 and CELH’s 61.82.

The high valuation of COCO and peers like FIZZ, MNST and CELH in my view reflects investors’ growing interest in the functional beverage market. According to Science Direct , functional beverages are non-alcoholic drinks containing nontraditional ingredients like minerals, vitamins, amino acids, dietary fibers (DFs), probiotics and added raw fruits, among other ingredients. They are marketed as offering additional health benefits beyond their nutritional value. Energy drinks, sports drinks, and functional bottled water are among the drinks in the functional beverage category that have shown immense growth in the recent years.

Demand for these products has grown compared with traditional beverages. CELH's commercial performance in recent quarters and years is a perfect case in point, but COCO is also shaping up to be another rising star in the functional beverage category. Importantly, COCO is worth an EV of $1.46 billion while CELH is worth and EV of $11.24 billion, suggesting that there could be more upside for COCO’s stock if it keeps churning out strong commercial results and gains the attention of large institutional investors, including potential suitors who can drive M&As or strategic partnerships. It's worth noting that CELH in 2022 inked a deal with PepsiCo ( PEP ) that saw the soft drinks giant come on board as a significant investor and strategic distribution partner. Likewise, MNST, which is significantly more successful than CELH, followed that some path when it secured significant investments and partnership from Coca-Cola ( KO ) in 2015 following its success in energy drinks.

Buy high, sell higher

COCO is the perfect candidate for a “buy high, sell higher” investment strategy. I believe that it still has significant underlying value despite current high multiples. Key catalysts that could unlock this value going forward are the growing demand for coconut water and the fact that COCO is growing sales volumes while demonstrating remarkable pricing power.

It's also worth mentioning that it has a pristine balance sheet with an immaterial amount of debt largely related to vehicle loans. Its supply chain is also asset-light, as COCO sources its coconut water from a diversified global network of 14 factories across six countries and operates co-packing facilities in its main markets of North America and Europe. These factors mean its high and improving margins are sustainable.

When it comes to future growth, the company is currently making forays into adjacent beverage categories. This includes its recent partnership with leading alcoholics drinks company Diageo ( DEO ). COCO and DEO have partnered to launch a line of premium canned cocktails called Vita Coco Spiked with Captain Morgan . It will be available in three offerings. This product line could add significant momentum to topline growth in coming years if the newly launched brand gains market acceptance and both companies leverage their strong brands and expansive distribution networks to win the hearts and pockets of cocktail lovers.

Bullish bet but take heed of the key risks

The main risk when it comes to COCO at this stage is its ongoing business transition in its smaller but still important private label business. COCO supplies private label products to key retailers in both the coconut water and coconut oil categories. In the first half of 2023, the private label business achieved net sales of $49.1 million vs $164.14 million for the Vita Coco brand in the US markets. Internationally, the private label business achieved net sales of $7.71 million vs $22.2 million for the Vita Coco brand.

While evidently smaller than the Vita Coco brand, the private label business is still instrumental to strong overall performance. The company disclosed in its most recent 10-Q that it discontinued a relationship with a key customer for its private label products, stating that “we expect a significant decline in our private label net sales over the next 12 months with potential impact beginning as early as the fourth quarter of 2023.” This is a risk worth tracking given the contribution of the private label business to overall performance.

It's also important to note that, although COCO has been in operations since 2004, it went public in November 2021. Barely 2 years have lapsed since its IPO. Young public companies can sometimes be disappointing long-term investments, as anyone who has ever tried investing in new and recent IPOs can attest. Sentiment can shift sharply due to one disappointing quarter. Bad news or other prevailing market trends can depress the share price of a stock like COCO more disproportionately when compared with more established public companies that have a stock chart with more historical data to look at. This means that COCO is an investment that requires some active customized risk management in order to secure returns. Its bullish long-term prospects notwithstanding, it's not a set-and-forget type of investment and investors need to be mindful of this.

For further details see:

Vita Coco: Ignore The High Valuation And Keep Buying