COCO - Vita Coco: Taking To 'Hold' After Loss Of Large Private-Label Customer (Rating Downgrade)

2023-08-31 10:02:00 ET

Summary

- Vita Coco continues to see solid growth and take market share.

- The loss of a major private label customer, however, will impact the company's results in the medium term.

- With more uncertainly in the name, I'm moving to the sidelines.

While Vita Coco (COCO) recently put up some strong results, the loss of a major private label customer changes the story in the medium term. The stock is up about 15% since my July bullish write-up on the name.

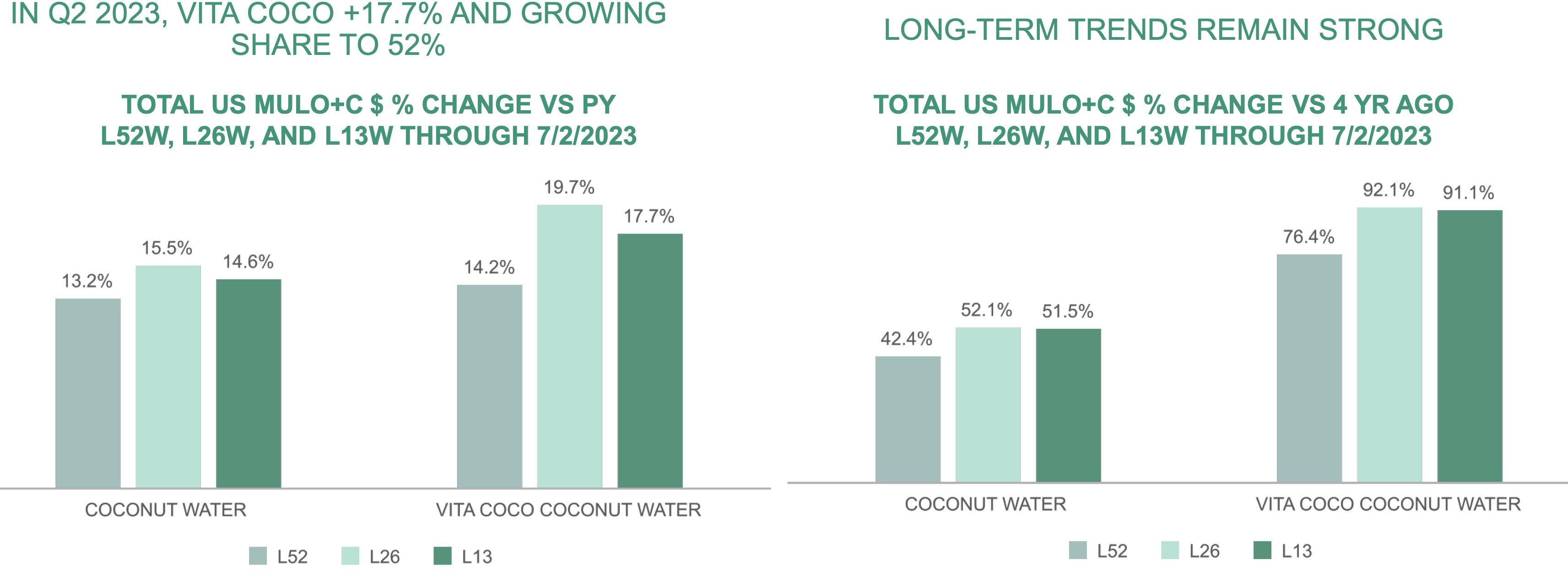

Q2 Results

For Q2, COCO saw revenue jump 21% to $139.6 million, up from $115.3 million a year ago. That easily surpassed analyst expectations for sales of $130.2 million.

Net income soared to $18.0 million, or 31 cents per share, compared to $1.1 million, or 2 cents per share, a year ago. That topped the consensus by 13 cents.

Adjusted EBITDA more than tripled from $7.3 million a year ago to $24.0 million.

Gross margins improved 1,120 basis points to 36.6%, up from 25.4% a year ago. On a sequential basis, gross margins rose 590 basis points.

Looking at segments, Americas Vita Coco Coconut Water saw revenue jump 24% to $95.0 million. Volumes rose 21%. Americas Private Label, meanwhile, climbed 17% to $24.1 million, with volumes up 22%.

On the international side, Vita Coco Coconut Water sales rose 14% to $12.7 million, with volumes up 8%. Private label sales soared nearly 72% to $5.1 million. Volumes climbed 54%.

The company ended the quarter with $48 million in cash and no debt.

The company noted that according to Circana that it had a 51.9% market share in the coconut water category. It noted the category grew 15% in the U.S., while its U.S. retail dollar sales were up 18%, showing that it is still taking market share.

{kind=link}

Overall, this was very strong quarter from COCO, with strong sales and volume growth. Despite already having a leading market share in the U.S., the company still has been taking share. The margin improvement was also very impressive, which was part of my investment thesis given improved ocean transport costs.

Outlook

Looking ahead, the company guided for full-year revenue to grow 10-12%. That's up from an earlier outlook of 9-12% sales growth and original guidance of 9-11% growth. Vita Coco Coconut Water sales are projected to rise in the mid-teens, while it will see some Q4 weakness in private label due to a customer loss.

It is looking for gross margins to be between 35-37%, helped by lower transport costs, better brand pricing, and more of a mix towards branded sales. That's up from prior guidance calling for full-year gross margins of 32-34%.

Adjusted EBITDA is projected to come in at between $56-60 million. That's up from earlier guidance of $54-59 million, and original guidance of $52-58 million.

Discussing the impact of the loss of its largest private label customer, Co-founder and executive Chairman Michael Kirban said:

"We have consistently talked about the goal of growing our branded business as our priority and our desire to reduce our reliance on our private label business, which is typically lower priced and lower margin. In recent negotiations with our largest private label customer, the proposed terms required to maintain the business were contrary to our margin targets and long-term goals. We have, therefore, jointly made the decision to transition the supply relationship at this time. We greatly value our long-term partnership with this customer who remains a key retailer for our branded products. We're more enthusiastic than ever about the strength of our core business and are especially excited by our branded initiatives where we see opportunities for even faster growth. However, it is unlikely that these initiatives will fully offset the net revenue loss from this large private label customer in the immediate term. As this decision was reached very recently, we're still developing the transition plans and building our 2024 commercial initiatives. But based on information, we believe that we can deliver mid-teens adjusted EBITDA growth in 2024 over the adjusted EBITDA communicated in our updated 2023 guidance with improved gross margins over 2023 levels, and we can accelerate our trajectory towards our long-term EBITDA margin targets. While the timing and magnitude of the impact on net sales is hard to quantify, we estimate that we will see some impact starting in Q4 and that our 2024 net sales could decline as much as mid-single digits. This preliminary estimate captures our current assumption on the timing of this transition and the current assessment of the offsetting impact of successfully implementing our 2024 growth initiatives. We'll update our view on the impact of this decision with our next earnings release. By then, we expect to have a better understanding of the transition timing and better visibility to the speed and size of our 2024 growth initiatives. As demonstrated by our track record, we're confident that our continued prioritization of margin accretive growth over margin dilutive growth can only strengthen our business going forward."

While COCO's lifted guidance was a positive, the big news is the loss of one of its largest private label customers. This is a lower margin business and thus the company thinks it will still be able to solidly grow adjusted EBITDA in 2024. However, revenue is now expected to decline next year. While it makes sense not to walk away from the business if the terms were not attractive, it's still a disappointment.

Valuation

COCO trades around 26x the 2023 consensus EBITDA of $59.6 million and 22x the 2024 consensus of $70.1 million.

It trades at a forward PE of nearly 40x the 2023 consensus of 72 cents. Based on 2024 analyst estimates of 82 cents, it trades at 23.5x.

COCO is projected to growth its revenue between 12% this year, and then see it decline -2.5% in 2025 become accelerating to 13.5% in 2025.

It's difficult to find a good comparison for COCO, given the loss of its private label business. Growth consumer product companies usually command high multiples, but that growth now isn't as strong as expected and revenue is expected to decline next year.

Conclusion

While initially falling after its Q2 results, COCO has quickly rebounded and is now nicely above where it traded prior to announcing the loss of one of its largest private label customers. In the long term, this loss might not be a big deal, as its branded business is more important. However, it does put a bit of a cloud over next year.

As such, and with the stock rallying, I'm going to lower my rating to "Hold" and move to the sidelines, as there is now more uncertainty in the name. COCO has a growth multiple, but won't see any revenue growth next year, which could be an issue given its valuation.

For further details see:

Vita Coco: Taking To 'Hold' After Loss Of Large Private-Label Customer (Rating Downgrade)