AVO - Vital Farms: Only Catalysts Playing Out Can Justify Current Pricing

Summary

- Vital Farms is a niche business that generates most of its revenue from the sale of pasture-raised eggs.

- Sales growth in recent years has been great, but profitability has not fared all that well.

- Shares look incredibly expensive, but current catalysts could help to justify this price.

In this world, there are only a handful or so of things that are universal across the human race. One great example of this is the need to eat in order to survive. Naturally, this need has led to a significant market dedicated to providing the world's nearly 8 billion people with the sustenance they require. Many times, investors look to the larger food players to generate returns. But there are some smaller players in the market, including some that have fared well in particular niche markets, that should be considered. One of these companies is Vital Farms ( VITL ). In recent years, management has done well to grow the company's top line and that top line growth is likely to continue for the foreseeable future. Having said that, the company's profitability has been something of a problem, with no clear trend demonstrated and such a low level of profitability that shares of the company currently look quite pricey. Although I fully anticipate the continued growth of the enterprise for the foreseeable future, the high price at which shares are trading has more than offset any of that. If it weren't for the company's existing initiatives aimed at boosting revenue further, I would rate the company a 'sell'. But instead, I'm rating it a 'hold', if only barely.

The opposite of egg-cellent

The management team at Vital Farms describes the company as an enterprise that's focused on ethically-minded food. Up until several years ago, little thought was given about the treatment of the animals that result in the food we consume today. This particular business set out to address those concerns, viewing this as a way to distinguish itself from more traditional food providers. So far, this strategy has paid off. According to management, the company has grown to become the largest brand in the US serving pasture-raised eggs and it is the second largest US egg brand by retail dollar sales.

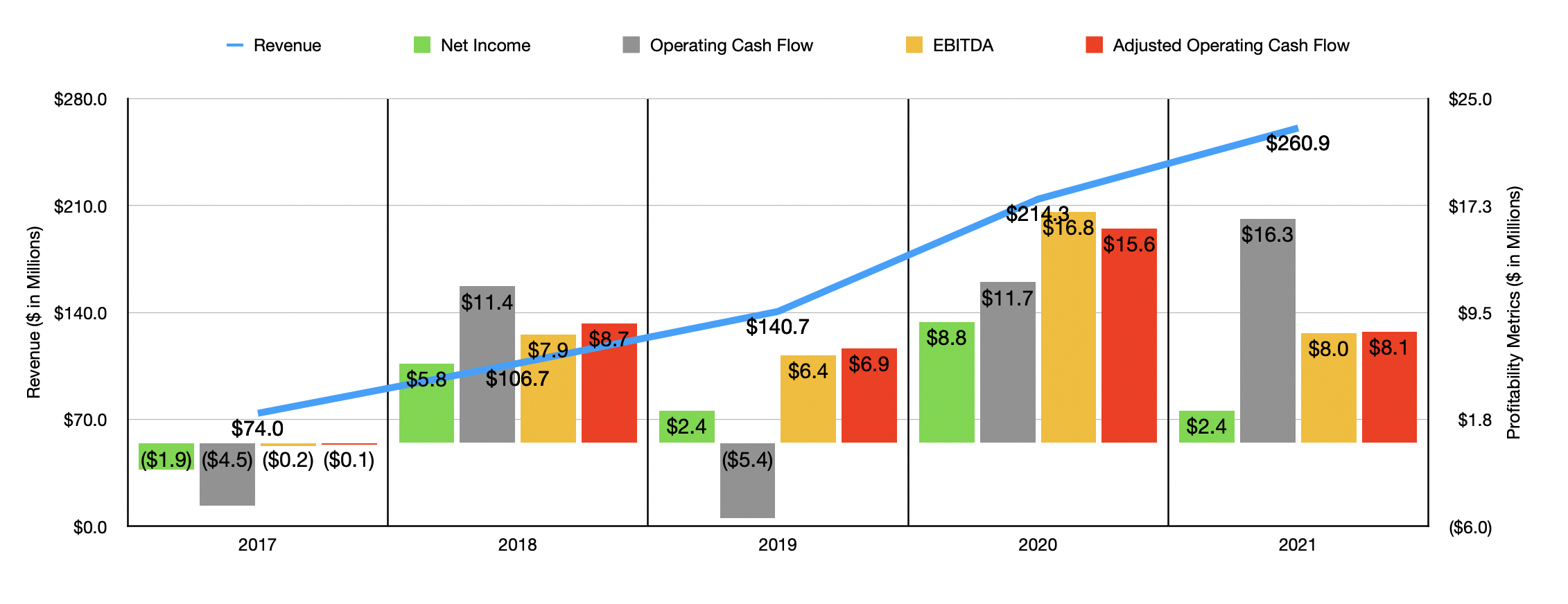

Dubbed 'Conscious Capitalism', the company prioritizes the long-term benefits of all of the stakeholders in their environment. This includes farmers and suppliers, customers and consumers, employees, the community, the environment, and stockholders. To illustrate with a company means by this, their claim is that, as of the end of their 2021 fiscal year, they had established a network of more than 275 family farms that, collectively, have set a national standard for the production of pasture-raised eggs. The idea behind pasture-raised eggs is that, as opposed to keeping hens locked up and tight and unhealthy confines, they are exposed to greater freedom that should result in happier, healthier, and hopefully longer lives than hens used in traditional egg production operations. Clear Lake, the strategy has been well received by consumers, as evidenced by the fact that the company grew its revenue from just $1.9 million in 2010 to $260.9 million last year. At present, the company's products are sold in over 20,000 stores across the nation, representing an annualized growth rate of 31% compared to the 5,359 stores the company sold to back in 2016.

{kind=link}

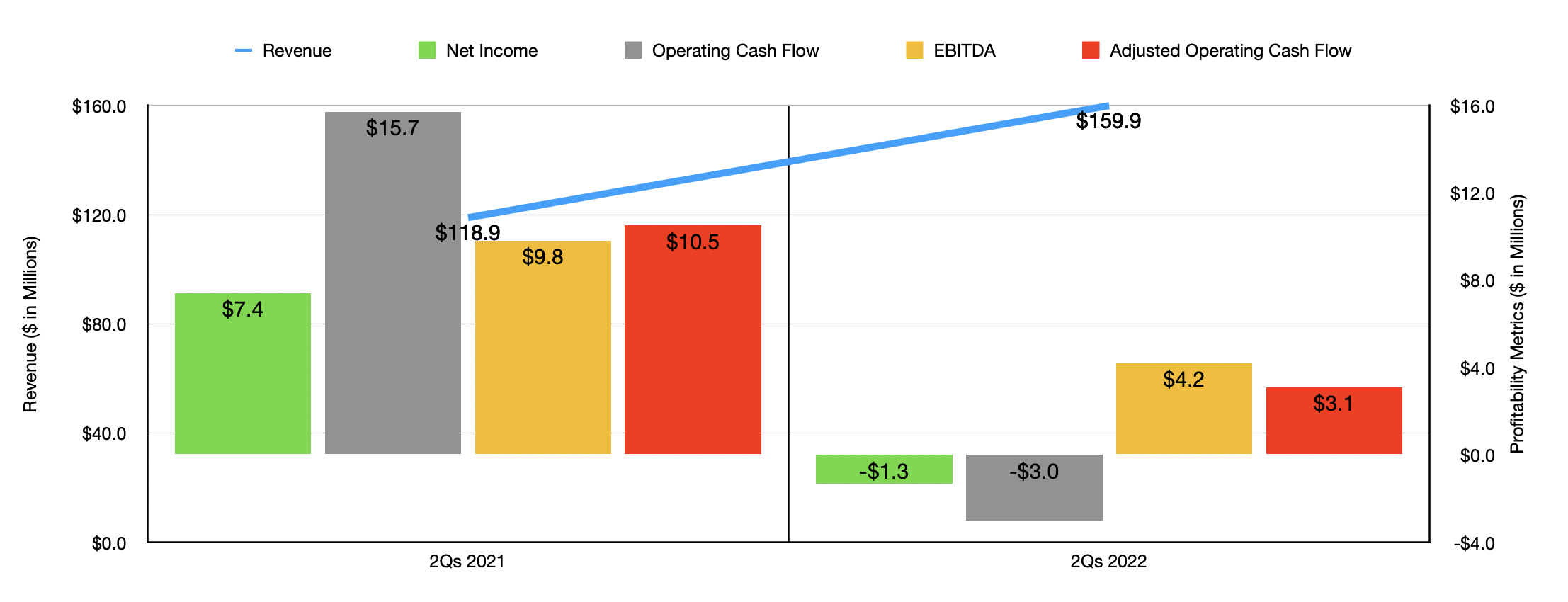

I mentioned already that sales have been growing rapidly in recent years. From 2017 to 2021, for instance, revenue jumped from $74 million to $260.9 million. That growth has continued into the 2022 fiscal year, with sales of $159.9 million generated in the first two quarters of the year. That represents an increase of 34.5% over the $118.9 million generated at the same time one year earlier. Although we are experiencing inflation across the economy, price increases have not been a significant driver to the company's growth. In fact, of the $41.1 million in additional sales the company has generated in the first half of this year, only $5.5 million came from increased pricing. By comparison, greater volume caused by higher demand for the company's particular offerings added $35.6 million to its revenue.

{kind=link}

When it comes to the 2022 fiscal year as a whole, management expects revenue declined by at least 30%. That should take sales up to roughly $340 million or more. This growth has been facilitated, in large part, by continued initiatives aimed at growing the company's production and innovating in ways that distinguish them from its peers. In May of this year, for instance, management announced the expansion of its Egg Central Station, which is the egg washing and packing facility that the company has in Missouri. This facility alone is expected to contribute over $300 million in additional revenue for the company moving forward. On the side of innovation, the company more recently announced the launch of what it refers to as 'new restorative eggs'. These are pasture-raised eggs produced using regenerative agriculture principles such as perennial rotations and cover crops. The goal here is to create balanced environments between pastures and the animals that benefit from them in order to create benefits on both sides. And earlier this year, in April, management also announced the introduction of blue pasture-raised eggs. These eggs, called True Blues, are produced by heirloom breeds of hens such as Azure hens that generate a unique pigment that causes the eggs they lay to be naturally blue.

Although the trajectory for revenue for the company has been quite impressive, the opposite can be said of profitability. As you can see in the initial chart in this article, net income has ranged from a low point of negative $1.9 million to a high point of $8.8 million, with no clear trend from year to year. The same thing can be said of operating cash flow and even EBITDA. I also looked at it through the lens of adjusted operating cash flow, which ignores changes in working capital. And there really was no trend there, with the metric peaking at $15.6 million in 2020 before plunging to $8.1 million last year. This year, profitability has proven to be a bit of a challenge for the company. Net income has gone from $7.4 million in the first half of 2021 to negative $1.3 million this year. Operating cash flow dropped from $15.7 million to negative $3 million, while the adjusted figure for this has gone from $10.5 million to $3.1 million. Even EBITDA has declined, dropping from $9.8 million to $4.2 million.

{kind=link}

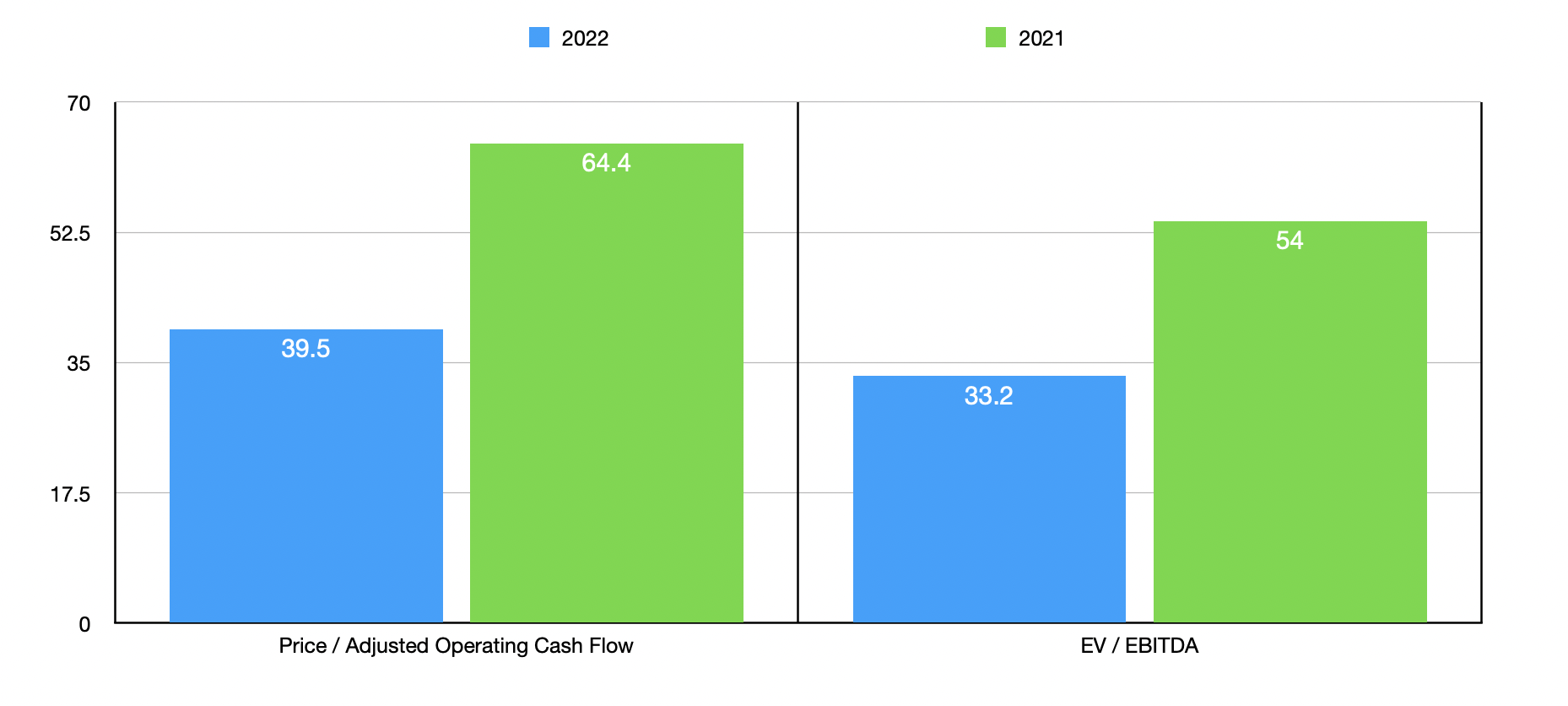

When it comes to the 2022 fiscal year, management does expect EBITDA to come in at roughly $13 million. If we assume that adjusted operating cash flow will rise at the same rate, then that figure should be roughly $13.2 million. This implies a forward price to adjusted operating cash flow multiple on the company of 39.5 and an EV to EBITDA multiple of 33.2. Although these multiples are incredibly high, they are lower than the 64.4 and 54, respectively, that we get using 2021 results. As part of my analysis, I did compare the company to five similar firms. On a price-to-operating cash flow basis, these companies ranged between a low of 5.5 and a high of 33.2. And when it comes to the EV to EBITDA approach, the range was from 7.1 to 21.1. In both cases, Vital Farms was the most expensive of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Vital Farms |

| 39.5 |

| 33.2 |

| SunOpta ( STKL ) |

| 29.1 |

| 19.3 |

| Mission Produce ( AVO ) |

| 21.1 |

| 19.0 |

| Calavo Growers ( CVGW ) |

| 30.9 |

| 21.1 |

| Whole Earth Foods ( FREE ) |

| 33.2 |

| 7.9 |

| Dole plc ( DOLE ) |

| 5.1 |

| 7.1 |

Takeaway

All things considered, Vital Farms is proving itself to be a really interesting growth story. Revenue expansion is impressive, but the company has not fared particularly well from a profitability perspective. If it weren't for the growth catalysts management has outlined, namely the expansion of its capacity, I would certainly rate it a 'sell' because of how pricey shares are both on an absolute basis and relative to similar firms. But at best, even with that, the company appears to me to only be a 'hold' candidate at this time.

For further details see:

Vital Farms: Only Catalysts Playing Out Can Justify Current Pricing