VTSCF - Vitesco: EV Transition Remains Underestimated

2023-06-26 17:59:55 ET

Summary

- Vitesco was hit by inflationary cost pressures in Q1.

- But the near-term headwinds are more than outweighed by the long-term EV transition story.

- With valuations still undemanding as the market adopts a ‘wait-and-see’ approach, there remains ample upside from here.

Following an underwhelming spin-off from Continental ( CTTAY ), Vitesco ( VTSCY ) is finally getting the recognition it deserves as a best-in-class European electric vehicle supplier. Since I last covered the name, the stock is up a low-double-digits percentage, as the Street appears to finally be paying attention (note the recent Sohn pitch by hedge fund manager David Einhorn). Fundamentals have continued to trend in the right direction as well - the company has gained further share in the high-growth EV powertrain space and is moving closer toward its 2024 breakeven target (despite the near-term inflationary headwinds). Yet, forward valuations remain undemanding at 2-3x fwd EBITDA (~4x trailing) vs. management's mid-term target of over 30% annualized growth through 2030. As Vitesco continues to pare down its combustion engine exposure in favor of a rapidly growing electrification business, the stock has ample room to re-rate from here.

Inflationary Headwinds in Q1 Outweighed by Impressive Order Intake

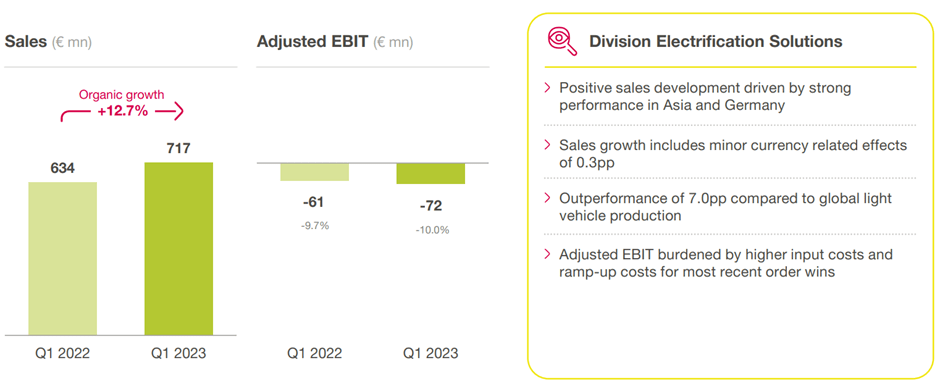

Vitesco started the fiscal year on a slightly underwhelming note, as adjusted EBIT margins were pressured by elevated input costs (mainly semiconductors) and higher wage growth. But management is in the midst of passing through the inflation via price increases ("cost transfers" per management), citing encouraging progress on pass-through negotiations thus far. Success here will be an important test of the company's pricing power, particularly in the context of last year's unabsorbed inflation. As most of the pricing is only set to flow through in Q2, keep an eye out for press release updates heading into the next quarter. Expect additional P&L tailwinds from easing supply chains globally along with lower commodity prices; depending on the extent of the Q1/Q2 pass-through, Vitesco could well offset all the 2023 inflation and potentially even recover some of last year's inflation as well.

{kind=link}

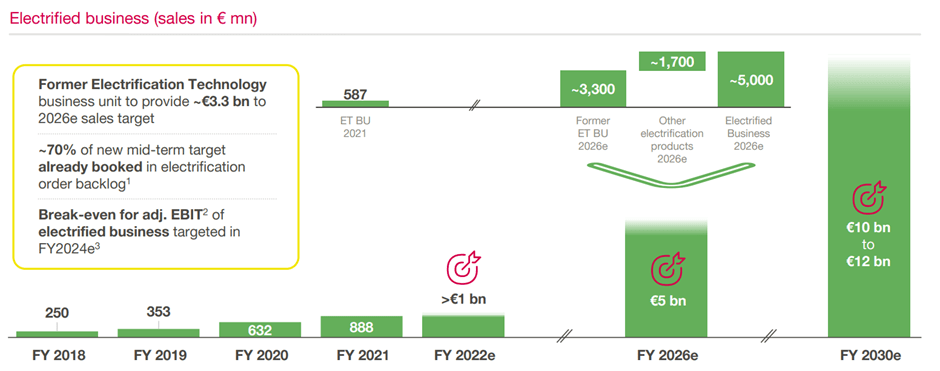

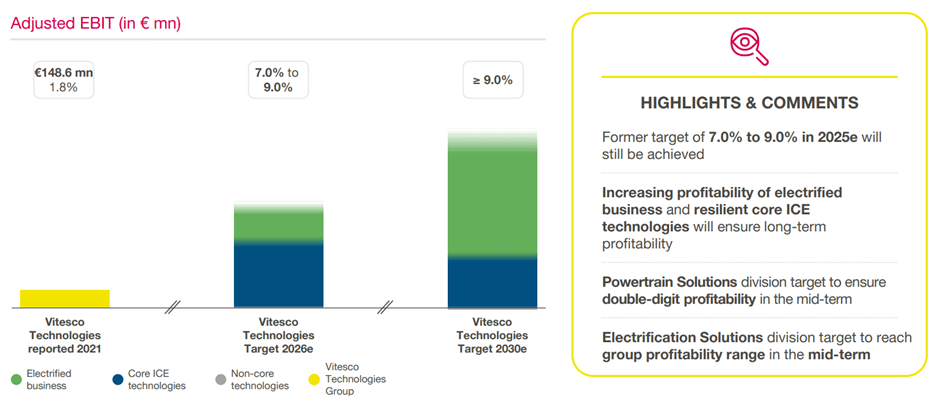

Another positive takeaway from the company's quarterly release was the strong electrification order intake. As of Q1, electrification order intake has reached EUR4bn (more than EUR800m added in Q1) - nearly halfway to its EUR10-12bn 2030 electrification organic sales target. In essence, the company isn't slowing down from its remarkable 2018 to 2022 sales growth (EUR250m to over EUR1bn) anytime soon. So while electrification sales only grew at a mid-teens percentage YoY pace in Q1 (well ahead of light vehicle production), upcoming ramp-ups should still get Vitesco to its 35-40% target growth algorithm this year. Expanded scale bodes well for margins, as reflected in the Q1 gross margin improvement to 6-7%; with the company well on its way to a high-single-digits percentage for 2023, EBIT breakeven (targeted by 2024) seems well within reach.

{kind=link}

Compelling Path to Mid-Term Growth and Profitability in EVs

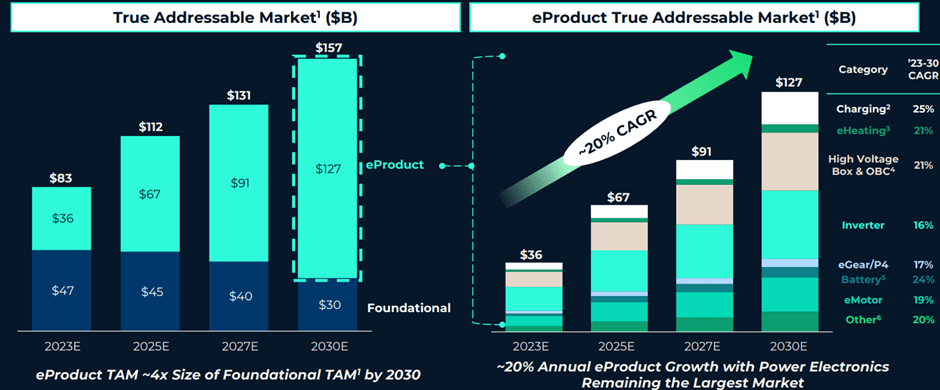

In a European auto supplier landscape featuring competitive players like Valeo ( VLEEY ) and Schaeffler ( SFFLY ), Vitesco's success in accelerating market share gains has been impressive. Gaining share in a rapidly growing market tends to be a recipe for success, and if the updated mid to long-term industry outlook by BorgWarner ( BWA ) at this month's capital markets day event is any indication, Vitesco's top-line runway (pegged at EUR10-12bn for electrification) could even prove conservative. To recap, BWA management now pegs its addressable EV market at an upsized $127bn through 2030 (+20% CAGR), driven by accelerated global EV penetration in China, followed by North America and Europe. Content density is another key factor, with both BWA and Vitesco citing enhanced content per vehicle with EVs vs. legacy combustion engine vehicles; hence, a transition to electrification should be net accretive to transitioning auto suppliers. As one of the few global suppliers with a full portfolio of EV products from thermal and battery management systems to electronics, Vitesco is firmly in a great position.

{kind=link}

One reason for the market skepticism (note Vitesco not only trades at a relative discount to its EU peers but also well below where it should trade vs. its mid to long-term targets) is likely the lag between order intake and sales. The issue is that sales conversion can take up to four years, yet the company has to fund its capex, R&D investments, and other opex to stay competitive in the meantime. The high funding requirements effectively create a barrier to entry for new entrants, while for incumbents, the key is to gain scale to tap into the operating leverage benefits. The encouraging electrification gross margin improvement in recent quarters, alongside the record order intake, indicates the company's EV business is on the right track here; as Q1 inflationary pressures fade, EBIT should soon follow suit. Hence, I feel comfortable underwriting the electrification business hitting breakeven by 2024 and even turning positive at the operating level by 2025. Achieving cash flow breakeven, on the other hand, will be more challenging given Vitesco isn't yet through with its R&D/capex cycle (mainly related to the EV transition). Any funding risk is negated, however, by the low net debt position and contributions from the cash-generating ICE business.

{kind=link}

EV Transition Remains Underestimated

Vitesco has shaken off any lingering post-Q1 concerns in recent weeks, with the stock re-rating to new highs. But at 2-3x fwd EV/EBITDA (~4x trailing), the valuation remains undemanding and should further re-rate as its market leadership in a fast-growing EV powertrain market shines through over the long run. In the meantime, management will need to navigate near-term cost inflation headwinds, though with management commentary already indicating successful pass-through, margin upside could well be on the cards as soon as Q2. Looking ahead, the company's order intake and sales conversion will be key to the next leg up, along with tangible progress on the ICE to EV transition roadmap.

For further details see:

Vitesco: EV Transition Remains Underestimated