VTRU - Vitru Limited: Cheap Student Headcount Growth And Geographic Expansion

2023-08-17 05:41:28 ET

Summary

- Vitru Limited has experienced impressive quarterly student headcount growth and an increase in undergraduate tuition.

- The company's business model focuses on offering hybrid educational services in Brazil through educational centers and personalized tutorials.

- VTRU has a large market potential in Brazil, with centers established in over 1,340 cities, and plans to expand in São Paulo, Rio de Janeiro, and Minas Gerais.

Vitru Limited ( VTRU ) recently delivered an impressive increase in quarterly student headcount growth and a recent increase in the undergraduate tuition. I am optimistic about the future of the company, mainly because VTRU has many potential clients, and may enjoy significant net sales growth from expansion in São Paulo, Rio de Janeiro, and Minas Gerais. I see risks coming from the total amount of debt and their interest rate. With that, I think that the company could trade at a larger valuation.

Business Model

With a history of more than twenty years in the digital education ecosystem in Brazil, Vitru Limited is a company that offers hybrid educational services in the country, through platforms for university or postgraduate students.

In addition, the company offers continuing education programs and campus for postgraduate courses, with the aim of democratizing education and access to professional improvements for students. Vitru has activities solely in Brazil, the largest market in South America and one of the largest by population in the world.

Currently, the company has more than 2,000 educational centers, which are the core of its business model. Through these educational centers, the company offers its educational services that include personalized tutorials, a hybrid platform between digital and face-to-face education, and a series of activities aimed at the educational community and its consolidation. Its nationwide educational platform is one of the largest in Brazil, and its asset-light strategy allows it to adapt to national and international macroeconomic conditions.

The company's business is divided into three segments related to its types of services: postgraduate digital education courses, face-to-face courses on campuses and educational centers, and continuing education courses. Of these three segments, the bulk of the annual income comes through payments for postgraduate courses in digital education. The other segments also offer a series of facilities and differentials within the framework of private education in Brazil, and are an important point of contact in its partner strategy for educational centers. Vitru owns a large number of centers, and establishes commercial and strategic relationships with different private institutions for the development of joint educational platforms.

As a last comment in this regard, it is important to measure the magnitude of the market in Brazil, since Vitru has centers established in more than 1,340 cities, and in little more than 10% of the cities with more than 40,000 inhabitants. In this sense, the potential expansive capacity is very high.

The recent information delivered in the last quarter includes very optimistic figures. The total number of students enrolled increased by close to 13%, with more undergraduate students as well as more digital education students.

Source: Quarterly Release

Another interesting and beneficial fact is that undergraduate tuition is also growing at a significant pace. With more students and more money received from each student, I believe that we could expect net sales growth and FCF margin to grow north in the coming years.

Source: Quarterly Release

FCF Expectations

I believe that the expectations of other analysts are worth having a look, mainly because they are quite beneficial. 2025 net sales would stand at close to R$2467 million, with net sales growth of 10%, 2025 EBITDA of $922 million, and operating margin of 30%. Additionally, with 2025 net income close to $393 million, 2025 free cash flow would stand at close to $381 million.

Source: Market Screener

Assets Are Increasing Driven By Inorganic Growth

So far, in 2023, I saw an increase in the total amount of assets, mainly driven by increases in cash, short-term investments, intangible assets, and prepaid expenses. I believe that the growth strategies implemented by management, which include new course offerings, M&A, and increase of market penetration, are having beneficial effects in the book value per share. In this regard, I believe that the recent increase in CFO driven by inorganic growth also enhanced the current cash in hand.

Adjusted Cash Flow from Operations amounted to R$160.6 million in 2Q23, an increase of 119.4% compared to 2Q22. This substantial improvement in cash flow generation was primarily a result of the contribution of UniCesumar's results to our consolidated figures: UniCesumar has certain characteristics, such as more positive working capital dynamics in the DE Undergraduate segment and the strength of its medical business, which make it a strong contributor to our consolidated cash flow generation. Source: Quarterly Release

As of June 30, 2023, Vitru Limited reported cash and cash equivalents worth R$83.5 million, with short-term investments close to R$254.4 million, trade receivables of R$280.4 million, prepaid expenses of about R$36.2 million, and total current assets close to R$734.8 million. I do not appreciate that the ratio of current assets/current liabilities is lower than 1x.

Besides, the net debt/EBITDA stands at close to 4.5x, which is not small. With all that being said, it is worth noting that Vitru promised to lower leverage to about 3x by December 2024. In my opinion, lowering the leverage would most likely have a beneficial effect on the stock valuation.

{kind=link}

With regards to the long term assets, Vitru reported trade receivables of about R$46.8 million, indemnification assets of R$11.5 million, deferred tax assets worth R$254.1 million, and right-of-use assets close to R$341 million. Finally, with property and equipment worth R$194.5 million and intangible assets close to R$4391.8 million, total assets stood at R$6045.9 million.

Source: Quarterly Release

Total Liabilities Are Decreasing

The list of liabilities included trade payables worth R$92.6 million, with loans and financing of about R$229.2 million, lease liabilities close to R$51.1 million, and labor and social obligations worth R$77.4 million. Besides, with payables from acquisition of subsidiaries worth R$526.8 million, total current liabilities stood at R$1055.6 million.

Trade payables were also equal to R$2.3 million, including loans and financing worth R$1563.4 million, lease liabilities of about R$266.1 million, and provisions for contingencies close to R$32 million. Finally, with share-based compensations worth R$12 million and other non-current liabilities of R$22.4 million, total liabilities stood at R$3717.6 million.

Source: Quarterly Release

I understand that investors may be a bit concerned about the total amount of debt. With that, it is worth noting that net debt decreased significantly in 2022 and 2023. I believe that we can assume a low cost of capital as Vitru is significantly reducing its debt levels.

Source: Quarterly Release

Highly Fragmented Market

The private education market in Brazil is highly fragmented, with some large companies occupying important shares and a number of small companies offering private or specific courses. In this sense, Vitru is confident that none of its competitors has a similar structure in terms of its hybrid digital education platform, certifications, and professional outreach for future students. With its 20 years of experience and credit to this development, it is difficult to imagine that a company can in the short term manage to establish a platform with a similar national scope.

Cash Flow

Under my financial model, I assumed that the company would most likely enjoy a growing market driven by the need for postsecondary education in Brazil. Close to 67% of the total population may need to represent the target market for Vitru. It is quite impressive.

According to the OECD, as of 2020, Brazil has one of the lowest postsecondary education penetration rates in the world, with only 23.0% of the Brazilian population between 25 and 64 years having completed any sort of postsecondary education degree. This is much lower than the average across OECD countries of 47.0% and also below other countries in Latin America, such as Chile with 41.0%. Source: 20-F

I also identified other revenue catalysts, which include the opening of new educational centers and the expansion to new regional markets such as São Paulo, Rio de Janeiro, and Minas Gerais. With know-how already proven in some regions, I believe that we may see further sales growth once Vitru implements its methods in new regions.

Additionally, I am optimistic about the mix of courses and the innovation in the thematic offer, generating added value and the interest of professionals from different industries such as nursing or engineering.

I also think that Vitru Limited will most likely be able to find further debt financing if necessary. If new M&A opportunities arise, Vitru may find financing. The company received R$1.95 billion at interest rates indexed to the CDI , which is in line with the credit market in the country. I believe that access to capital markets means that market participants do expect future growth, and are optimistic about the future. In my view, if we see a generalized decline in the interest rates in the coming years, the company may be worth a lot more as the cost of capital would most likely decline.

Vitru Brasil Empreendimentos, Participações e Comércio S.A. (Vitru Brasil), a wholly owned subsidiary of Vitru Ltd., completed the issuance of two series of simple, secured, non-convertible debentures (Brazilian bonds denominated in R$) in an offering with restricted distribution efforts directed solely at professional investors in Brazil. The two series of debentures amounted to R$1.95 billion at interest rates indexed to the CDI (Certificado de Depósito Interbancário) for a five-year term in total. Source: Quarterly Release

Taking into account previous net sales growth, FCF growth, and the market in which Vitru operates, I believe that we can expect positive FCF in the coming future.

Source: Ycharts

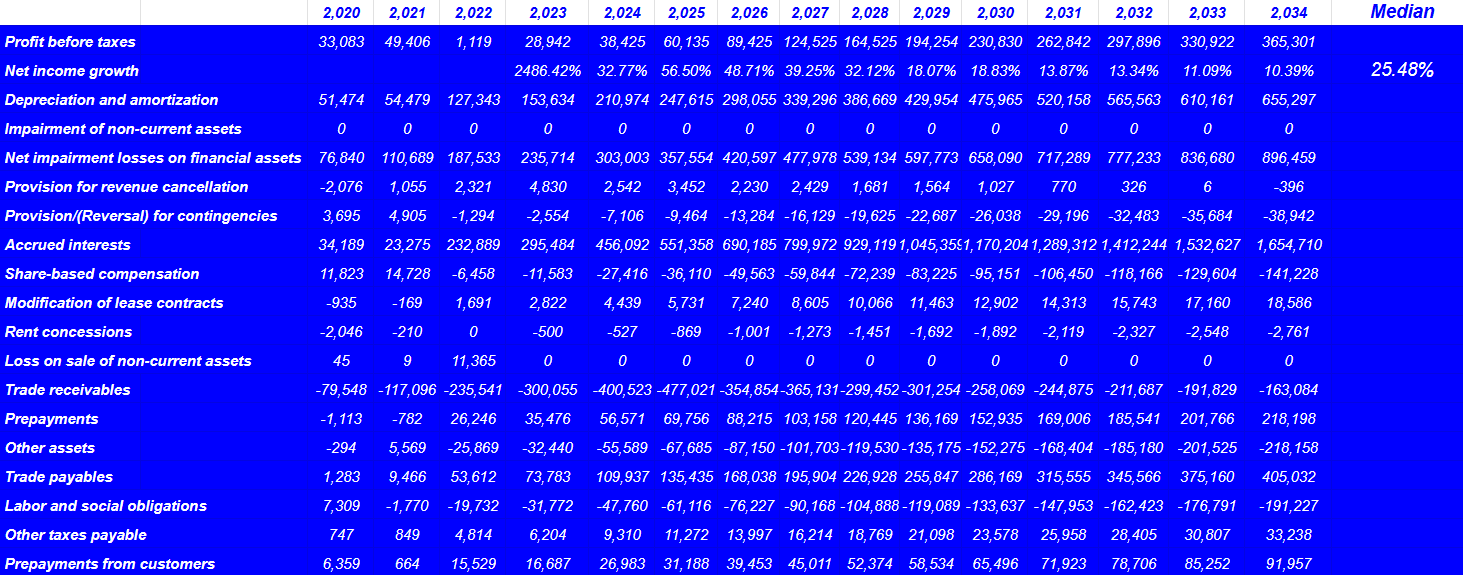

My future cash flow statement model includes 2023 profit before taxes worth R$365 million, with net income growth of 10% and a median net income growth of close to 25.4%. I believe that my figures are quite conservative.

I also included depreciation and amortization close to R$655 million, with provision for contingencies close to -R$39 million, and modification of lease contracts of close to R$18 million.

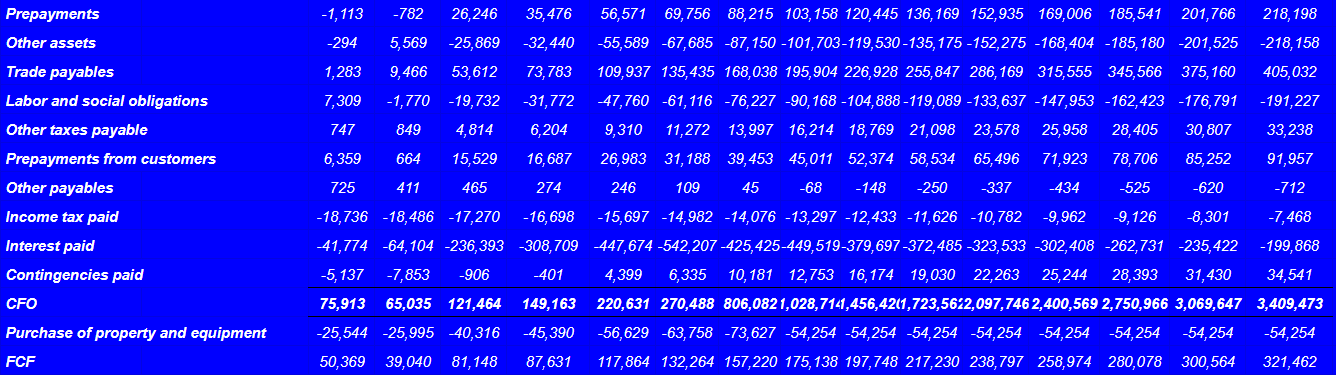

Also, with rent concessions of close to -R$3 million, changes in trade receivables of -R$164 million, and changes in prepayments worth R$218 million, I also included changes in labor and social obligations of about -R$192 million.

{kind=link}

Finally, with changes in prepayments from customers of close to R$91 million and changes in interest paid close to -R$200 million, the implied 2034 CFO would be close to R$3409 million. I also assumed 2034 purchase of property and equipment worth -R$55 million, which implied 2034 FCF of about R$321 million.

{kind=link}

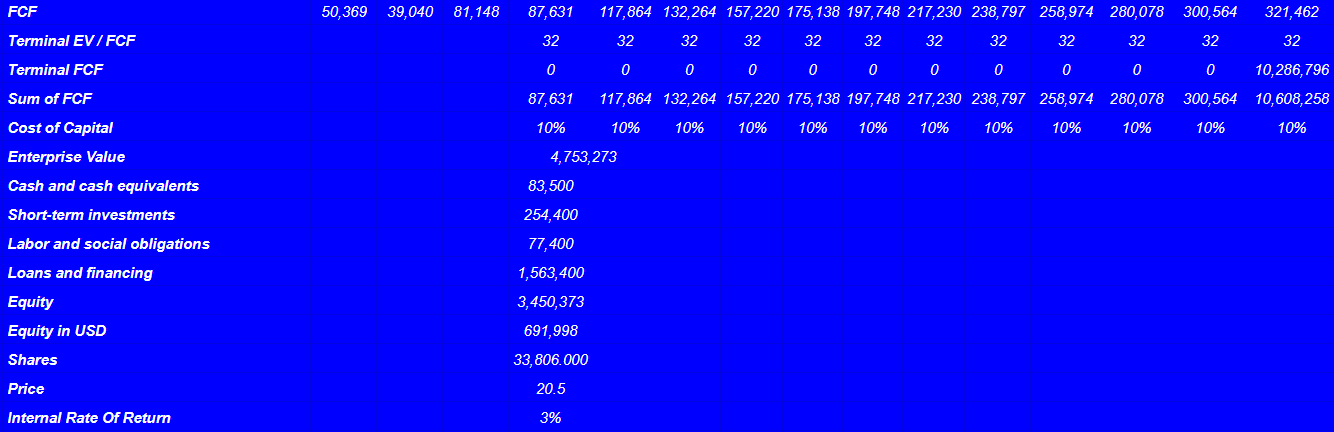

If we assume a terminal EV / FCF close to 31x-32x and cost of capital of 9.5%, the implied enterprise value would be close to R$4753 million. If we add cash and cash equivalents of R$83 million and short-term investments of R$254 million, and subtract labor and social obligations of R$77 million, with loans and financing of R$1563 million, the implied equity would be R$3450 million. Finally, the implied price valuation would stand at close to $20 per share with an internal rate of return of 2.7%.

{kind=link}

Risks

First of all, we must point out the political and economic instability in Brazil, which can mean changes in the company's infrastructure. This is accompanied by legal situations and regulations in relation to private education. In economic terms, the perception of risks in major markets and the variation in this sense can drastically alter local conditions.

In an operational sense, a large portion of Vitru's revenue comes from commercial agreements with other educational centers, and the inability to keep renewing these agreements can affect the company's economic flow. In this framework, we can also name the series of legal conditions for the exercise of education as well as the taxes and financial regulations that fall in risk factors in case they are changed. In relation to the competition, the reading of digital trends and technological innovations in the educational field as well as the proposal of courses superior to that of its competitors are important points for the development of its growth strategy. Managing this growth is one of the most important factors in the short term, since due to the structural conditions of the company and the private education market in Brazil, it is difficult to imagine that it will not at least be able to establish itself in new regional markets.

Takeaway

Vitru Limited is operating in a massive market, and the number of potential clients is large. With recent quarterly figures that indicate students growth and an increase in the number of tuitions, I believe that net sales growth and FCF margin momentum could surprise in the future. Besides, expansion into new regional markets in São Paulo, Rio de Janeiro, and Minas Gerais could also accelerate the business. I would be a bit concerned about the total amount of net debt and the cost of capital. However, in my DCF, I assumed a decrease in interest rates, which may lead to an enhancement of the stock valuation. Yes, there are risks, but I believe that Vitru Limited could see even a higher increase in its stock price.

For further details see:

Vitru Limited: Cheap, Student Headcount Growth, And Geographic Expansion