VMW - VMware: Subscription Revenue Status And Regulatory Update

2023-07-12 17:28:33 ET

Summary

- VMware is transitioning its revenue model from license to subscription, making most of its product offerings available as a service, which could lead to increased recurring revenues.

- The company's shift to a more network and security-focused role, along with its partnerships with equipment providers and software developers, has helped it maintain its market position despite competition from cloud-centric hyperscalers.

- Despite high valuations and potential economic uncertainty, VMware's product appeal and potential margin gains from the subscription model justify a "Hold" position, with its merger with Broadcom also on track to be approved.

With all those merger regulatory talks related to Broadcom ( AVGO ), little attention is being paid to VMware's ( VMW ) strategy to transition its products to be subscription based, which rhythms with faster revenue growth and profitability, as this thesis aims to show.

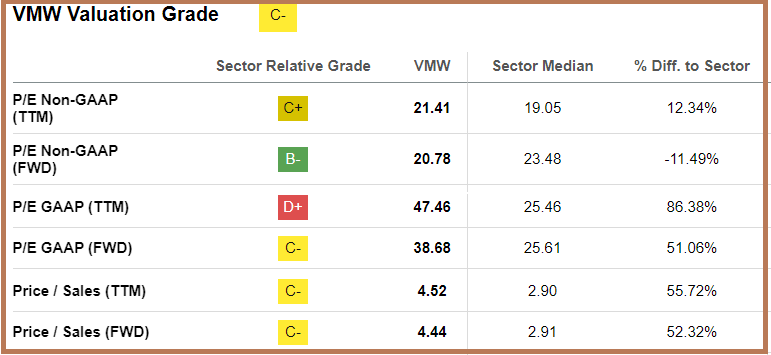

At the same time, by removing complexity and introducing a higher degree of automation, which means better productivity for its customers in a period characterized by economic growth concerns, VMware is managing to tilt the balance away from on-premises licenses to SaaS (Software-as-a-Service). I also assess whether the stock deserves its richer valuation grade of C- given that, at around $144, it still trades well below its 2019 high of over $200.

{kind=link}

Some Valuation Metrics (seekingalpha.com)

Fighting Against Network Complexity

First, VMware’s role has shifted from a software virtualization company to a more cloud-based one featuring both networking and security, which allows users to access their applications from anywhere in a secure fashion. As such, its products are now delivered mostly in an As-a-Service mode.

{kind=link}

www.vmware.com

In this way, it addresses one of the most pressing issues facing network administrators today which is the management of increasingly complex networks, engendered by changing work patterns. In this context, when the pandemic hit in 2020, many employees were forced to work from home, and to this day, not everyone has come back to the office in the same way as before. This has given rise to hybrid work whereby employees both work remotely as well as pop into the office a few days per week. At the same time, more companies have migrated their IT workloads to the cloud giving rise to new requirements in terms of connectivity.

These requirements can be satisfied by technology like SD-WAN (Software Defined Wide Area Network), which, by separating the software part from the hardware enables a higher degree of flexibility than traditional all-in-one-box devices. For recall, VMware expanded into SD-WAN by acquiring VeloCloud in 2017 and in 2020 started offering SASE (secure access service edge) services comprising items like firewall-as-a-service, with the intent of supporting organizations' needs for dynamic secure access.

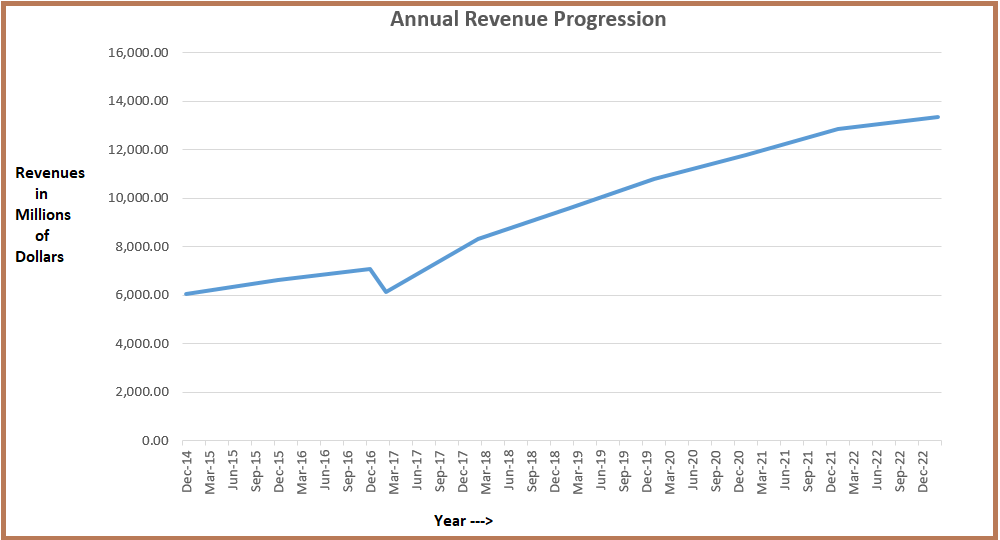

Looking at the competition, it was the ease of integrating SASE with SD-WAN in multi-cloud platforms that accounted for its broader adoption across both enterprises and service providers resulting in VMware's sustaining its topline in the 2019-2020 period as per the chart below, despite the emergence of cloud-centric hyperscalers like Microsoft ( MSFT ) or Amazon ( AMZN ).

{kind=link}

The chart was drawn using data from (seekingalpha.com)

Growth was also helped because VMware was not a supplier of hardware appliances like Cisco Systems ( CSCO ) or Juniper Networks ( JNPR ). In fact, its software and services were designed to work with all hardware suppliers which amounts to being vendor-agnostic. Also, the company partnered with strong players in the IT security space like Zscaler ( ZS ).

Shifting From License to Subscriptions

Now, this partnership approach involving working in tandem with hardware vendors or antivirus software developers has the merit that it not only limits the number of competitors it has to face but also increases the chances of the company winning contracts as part of joint projects.

However, on the flip side, VMware does not benefit from the same upfront revenue level as a company selling appliances plus software licenses. Thus, when there is a change in the mode of billing, namely from on-premises licenses bookable on an upfront basis, to a subscription-based one where revenue recognition is done over the term of the contract, software companies usually suffer from slowing sales. This also depends on the way sales are booked and subsequently reported.

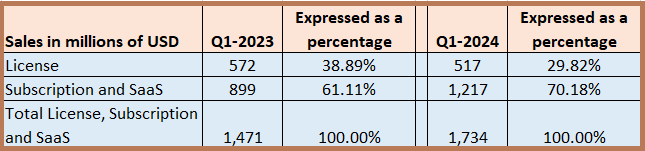

However, the bottom line for a successful transition is for the percentage of subscription and SaaS sales over total product revenues to be on an uptrend and this has indeed been the case with VMWare when comparing results from the latest reported quarter (Q1-2024) and Q1-2023.

{kind=link}

Table Built using data from SEC filings for the quarter ending on May 5 (www.seekingalpha.com)

Hence as shown in the table above, the percentage of sales derived from Subscriptions and SaaS has increased from 61% to 70% within one year. By comparison for the twelve months ending in January 2020 or the most part of 2019, less than 40% of sales were subscription-based. Additionally, despite VMware's topline progressing by only 5% during the last reported quarter, subscription sales jumped by 35% ((1217-899)/899).

Such an achievement has been made possible through cloud-based offerings like VMware Cloud Universal and vRealize Cloud Universal, and progressing on making other major products available through subscription, especially the SDDC (Software Defined Data Center) portfolio, which was precisely the CEO's objective during its Q4-2022 earnings call back in February 2022. This means the transition (from on-premise to SaaS billing) has been successful.

Now, looking ahead, subscriptions and SaaS have the potential to drive the top line higher, with analysts estimating revenue growth for the fiscal year ending in January 2024 to be 4.7% before accelerating to 8.23% in 2025.

Revenue estimates (seekingalpha.com)

Therefore, the stock deserves its higher valuations, but, given that the forward Price-to-Sales multiple is already 50% above the median for the IT sector, most of the upside, or 26% YTD, seems to have been priced in the value of the stock. Still, in light of economic uncertainty, there is a need to further justify such optimism, and for this purpose, I highlight the product appeal as well as the potential for margin gains.

Product Appeal Amid Economic Uncertainty And Margins

While the U.S. economy has been resilient up to now despite the unprecedented rise in interest rates since last year raising borrowing costs, it may not be the case for international markets which accounted for 52.5% of VMware's revenues in the last quarter. In this case, while developed markets like Europe still suffer from high inflation, emerging ones like China now seem to have a deflation problem as the post-Covid recovery remains uncertain. Therefore, there are risks of revenue shortfalls in case there is a weakness in service providers' uptake of VMware's solutions which may in turn impart volatility in the stock when the financial results are announced at the end of this month.

SEC Filing (seekingalpha.com)

However, the effects of a revenue shortfall could be offset by the relevance of products in the current economic context and the fact that clients do not need to spend Capex upfront. Here, coming back to the complexity reduction rhetoric, through solutions emphasizing automation, orchestration, and visibility as shown below, VMware enables CIOs to achieve more while spending less in terms of manual monitoring and troubleshooting, thereby delivering productivity gains.

{kind=link}

sase.vmware.com

Now, in the worst-case scenario that expected growth does not materialize, there is always the profitability factor that comes with transitioning from a revenue model whereby customers are charged upfront to a more flexible one where additional sales per customer are possible thanks to a-la-carte consumption.

To illustrate my point about profitability, the table below shows the cost of sales over total sales expressed as a percentage where it is found that, on relative terms, expenses for subscriptions have decreased from 21.36% in Q1-2023 to 17.09% in the last reported quarter. This is due to the larger client base on which to split fixed costs.

{kind=link}

Table Built using data from SEC filings for the quarter ending on May 5 (www.seekingalpha.com)

Looking ahead, these lower costs of sales should contribute to better gross profit margins which have been kept in the 81%-83% range since 2019. On trickling down the income statement, these higher margins could offset some of the additional operating expenses seen in the last four years and reduce the need for Broadcom, the potential acquirer, to increase product prices as feared by certain customers.

Concluding With The Broadcom Acquisition

Now, a potential price hike would be against VMware's relatively flexible purchasing and consumption program which encourages businesses to adopt a multi-cloud path. Looking further, concerns have also been voiced by IT managers about the possibility of a reduction in the level of customer support, as well as a reduction of investments in certain VMware products given that Broadcom is also a large vendor of software products for enterprise monitoring and security. Such concerns could prove beneficial to competitor Nutanix ( NTNX ).

However, in order to obtain regulatory approval, the key criterion is antitrust legislation whereby a merger does not impact competitors to such an extent that it limits their market power.

For this matter, according to a Seeking Alpha news update, Broadcom has obtained conditional approval for its proposed $61 billion acquisition of VMware from the EU as it has satisfied some regulatory concerns, related to interoperability with rivals. In this case, as I mentioned earlier, being vendor agnostic, VMware has designed its software to work with most hardware products with one example being Fiber Channel host bus adapters (FC HBAs) that connect servers to outside storage and are produced by Broadcom's competitor Marvell Technology ( MRVL ). To resolve the contention, Broadcom has provided assurance to regulators that the merged entity would continue to support the competitor's technology as well as those of new entrants.

This is certainly a positive in the regulatory approval journey, but, adopting a cautionary posture, it is better to wait for clear signs of regulatory progress in China , given the two companies' global footprints.

In conclusion, by making its product available in SaaS mode, VMware is successfully transitioning its revenue model from license to subscription. As such, it should improve revenue growth and be more profitable. However, since valuation remains on the high side, economic uncertainty prevails in many parts of the world, and tensions with China seemed to have flared up recently, I have a Hold position, all in the name of prudence.

For further details see:

VMware: Subscription Revenue Status And Regulatory Update