VOD - Vodafone: A Dividend Paying Stock On The Decline

2023-03-08 10:43:53 ET

Summary

- Vodafone is a telecom giant, operating internationally. The company's stock has declined unwaveringly in the last eight years.

- Economic conditions are weakening, but history suggests Vodafone should be able to navigate this without a material fall in demand.

- Vodafone has agreed to the sale of its towers business at a valuation of $16BN. This is part of a several-year strategy of selling assets.

- Vodafone's financials are a mess. The business is heavily indebted and funding its dividends through this.

- The company is appropriately valued and paying 9% dividends, but we do not like the company's profile long-term.

Company description:

Vodafone Group Public Limited ([[VODPF]], [[VOD]]) is a telecommunication company , operating across Europe and internationally. The company is listed in the UK, as a constituent of the FTSE 100. The company offers mobile services, broadband, television, voice; and other telecommunications/financial services.

Vodafone has had an atrocious 8 years. The stock has gradually and consistently fallen with very little in the way of a reversal. Management has attempted a turnaround, expansion into new markets, and realization of poor-performing segments. Unfortunately, none of these strategies have worked.

Although we have kicked this paper off on a downer, mass selling can always be an opportunity. Every stock has a fair value and if its share price falls enough, it could reach and exceed this. We will consider the company's financials and its relative valuation against competitors, with the backdrop of the current economic environment and the telecommunications industry.

Recent news:

Towers

In late 2022, Vodafone began the process of selling a large stake in its mast and tower business , Vantage Towers ( VTWRF ). GIP and KKR are the buy-side, valuing the company at EUR16BN. They will purchase around half of the business, allowing Vodafone to retain co-control over the infrastructure to roll out 5G while realizing cash to pay down debt.

Across Europe, we are seeing key infrastructure sold to funds, as they seek reliable consistent income. KKR has led this wave, having failed in a bid for Deutsche Telekom ( DTEGY ) but succeeded in purchasing partial ownership of Northumbrian Water Group.

Liberty Global

Liberty Global ( LBTYA ), a telecoms multinational has taken a 5% stake in Vodafone. LG has described this as an opportunistic investment, believing the company to be undervalued. This has the potential to cause price action should LG increase its stake from this point.

African business

Vodafone is said to be exploring the sale of its African business, one of the jewels within Vodafone, which could raise $14BN . Etisalat, Vodafone's largest shareholder could purchase the business themselves and merge this with their current African operations, potentially maximizing the value for Vodafone.

It is far too early to comment on this currently and will not refer to it unless and until further details are provided.

Economic considerations:

Market conditions have weakened as a result of changing economic conditions globally. Inflation grew quickly in 2022 driven by multiple factors, including the Russian invasion of Ukraine. To combat this, Central Banks began to increase rates to cool demand, which is working but slowly. This said, we will likely need further rate hikes and continued heightened levels to bring inflation to a sustainable level.

With this in mind, we believe a recession is likely in many weaker economies. We are seeing a cost-of-living crisis which is depressing demand, especially in discretionary markets. if rates are to remain heightened, this will only worsen in our opinion.

The impact on the telecoms industry, and Vodafone in particular, is likely to be mild. Historically, telecoms businesses have navigated weak demand well. The reason for this is their relative demand inelasticity. People generally do not give up mobile phone contracts because it is a necessity (although they are more likely to shop around). The same goes for most other telecommunication services, they are vital to our way of living in the modern day. As long as Vodafone can remain price competitive, which is reasonable to assume given the high level of competition in the industry, it should maintain healthy demand. Looking at Vodafone's performance in 2007-2009, we saw growth of 6%, 14%, and 16% (although large impairment against goodwill on the bottom line). AT&T ( T ) showed low single-digit growth during this period.

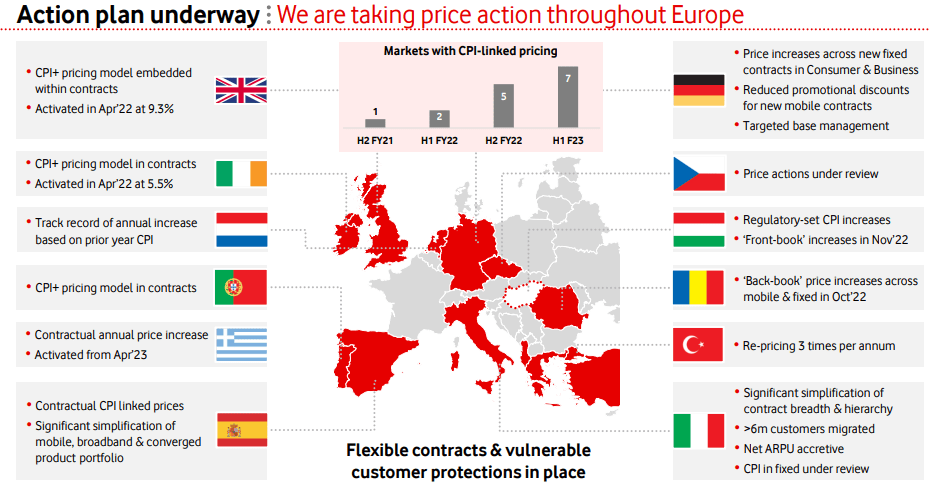

Further, when we consider the inflation aspect of things, the risk is also mitigated. Vodafone has positioned its contracts to include inflationary price increases, as well as general price hikes. Therefore, margins will not be compromised.

Vodaphone price action in Europe (H1 investor pack)

{kind=link}

For this reason, we believe Vodafone will face pricing pressure but will not see a material decline in demand.

Telecommunications industry:

The telecoms industry is a largely mature market but has faced much upheaval and change in recent years. The industry is somewhat cyclical, with new technologies and demand for faster speeds resulting in periodic large developments. We are in the process of one now, with the rollout of 5G technology and many countries pushing for greater internet speeds across rural locations.

In 2023, Deloitte has identified the following key themes in the market:

- More competitive broadband markets - Deloitte believes the broadband market will be shaken up by the ability to bundle broadband with other services. The reason for this is greater optionality with services, as wireless connections become a viable alternative to traditional wired home internet. This is an area Vodafone can exploit, as they have an offering across the spectrum. In the UK for example, Vodafone sim cards can be bundled with TalkTalk internet and TV. The provides consumers with one all-encompassing service while receiving a little discount. For Vodafone, this means significant upselling.

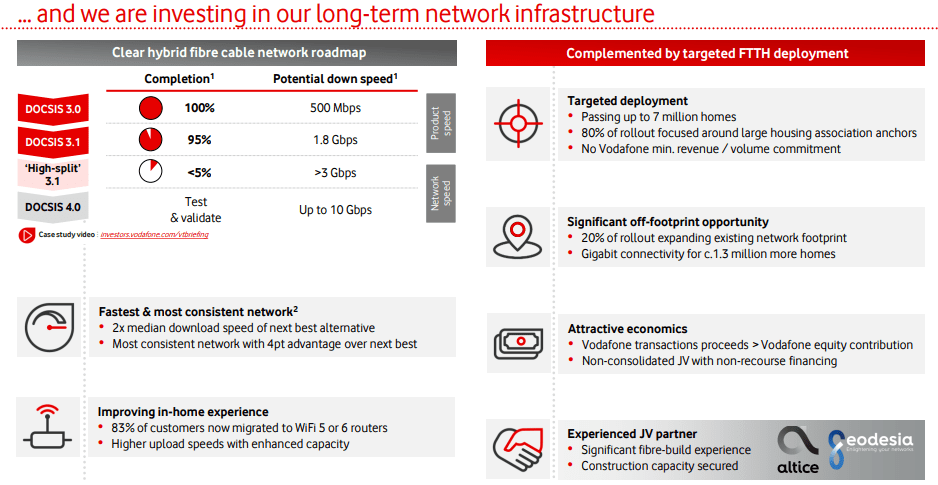

- Decentralized government broadband infrastructure funding - An opportunity is present with governments taking a step back from infrastructure, choosing to support businesses instead. Again, Vodafone has done well here, committing a considerable amount of Capex to expand its infrastructure. This is both through partnerships, funding-supported and direct.

Vodaphone infrastructure spend (H1 investor pack)

{kind=link}

- Interest in multi-access edge computing and private cellular networks - The market is nascent but is proving as an area of need for enterprises. This is a continuation of computing power innovation, with greater-sized data needing to be transferred at greater speeds. This is another area Vodafone has its hands in, with a partnership with AWS ( AMZN ) to cement its offering.

- Reassess cybersecurity and risk management in the 5G era - A new generation of internet infrastructure serves as new opportunities for cybercrime. Vodafone Portugal was hacked in early 2022 and so is certainly an area of focus. The amount of customer data held, and key infrastructure managed, is significant and so the pressure is extremely high to ensure no breaches.

The key themes in the industry revolve around the current innovation we are seeing. Vodafone as a large player in the market is at the forefront of this development.

Financials:

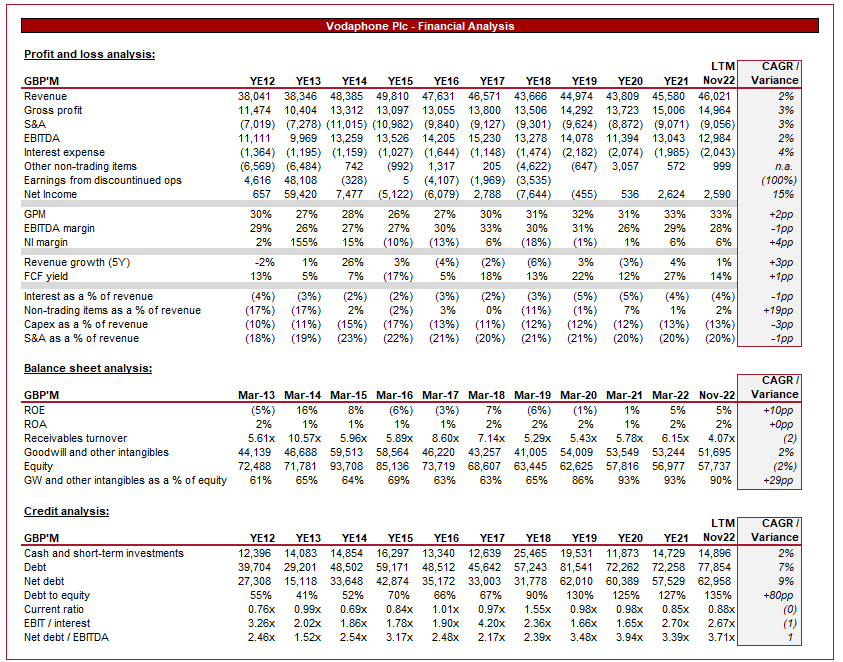

Vodaphone Financial (Tikr Terminal)

{kind=link}

Vodafone's financials are a story of two halves, one quite good and one deal-breaking.

From a P&L perspective, the business looks relatively good. Revenue growth has marginally lagged behind inflation, but the business has been attempting to cut loose low-margin segments. Given the number of incumbents in the market, competition will mean it is incredibly difficult to outperform on the top line for any extended period.

The business has a lot of noise throughout the historical period. In FY13 we see what looks like a typo, one of the largest corporate profits in its history. Vodafone disposed of its 45% holding in Verizon . Further, we see other large, discontinued operations and non-trading items in various periods, much of which is just noise.

This has led to large variability in net income. CAGR is 15% but we observe 4 periods of negative growth and no real evidence to suggest a normalization.

Capex is increasing as a % of revenue, showing Vodafone's commitment to improving its infrastructure, in line with management claims.

This all translates to a FCF margin of 14%, which is extremely healthy. At these levels, the business can fund dividends and buybacks sustainably.

For an investor looking for a low-risk dividend play as part of a well-balanced portfolio, Vodafone's P&L looks like an ideal choice. The problems quickly arise when the eye falls on the balance sheet.

Vodafone's balance sheet has gone through a decade of value destruction. GW and other intangibles have increased from 61% of equity to 90%, with much of their tangible assets sold or expended.

Further, net debt has grown extensively and now exceeds equity. The business has been FCF generative so it's strange to see such growth in debt. We believe the reason for this is the company's desire to maintain dividends and share buybacks.

The reality is much of the quality assets in the business have been sold. Much of the company's cash is being paid to investors and this is all being financed by debt. Having a large GW/intangible balance is not necessarily a bad thing, but at 90% of equity, the risk of impairments is very high. The company's ROE is 5%, suggesting the GW/intangibles are not of great quality.

Debt is not a bad thing but to essentially fund dividends through it is a form of long-term liquidation. Famed investor Terry Smith has spoken much on this topic, believing it to be a trap that many investors overlook.

Peer comparison and valuations:

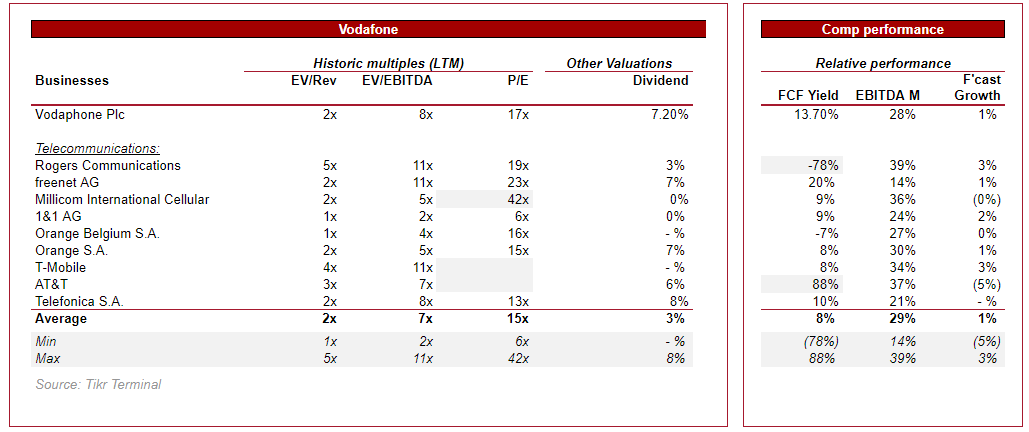

Peer group valuation and relative performance (Tikr Terminal)

{kind=link}

When comparing Vodafone to its peers, the business looks slightly undervalued. It is trading in line with comps but boasts 8% dividends (with management committing to a 9% yield as of H1's share price of £0.98) and superior FCF yield.

We have not looked into these businesses in detail, but as shown in the case of Vodafone, the headline numbers hide much of the problems within.

If we were to suggest Vodafone deserves a 1x premium on EBITDA, this would suggest no upside currently. Further, there are no catalysts in sight. It is very unlikely that the stock will move positively when growth is forecast at 1%.

Conclusion:

When I consider what Vodafone offers, it feels like the opposite of a GARP, a decline at a reasonable price. The company is doing the right things, investing in capex and expanding its offering. Unfortunately, the company is bloated with debt and selling whatever it can to ensure dividends and buybacks are maintained. There does not seem to be a long-term strategy for transforming the business, it all seems to be around maintaining the status quo and selling what can be sold when possible.

Our view is that dividends are maintainable and that Management will continue to support this. Investors looking purely for dividends and do not care about a sustained decline in share price should consider Vodafone. For everyone else, this is a stock to avoid in our view. That said, the telecoms industry looks interesting, for a more bullish view, see our Nokia ( NOK ) write-up.

We rate this stock a sell.

For further details see:

Vodafone: A Dividend Paying Stock On The Decline