VOD - Vodafone: Improving Operating Trends Support 10.8% Dividend Yield

2023-12-14 17:31:34 ET

Summary

- Vodafone offers a high-dividend yield and attractive valuation, making it appealing for long-term investors.

- The company has made progress in streamlining its business and selling off non-performing assets.

- While the telecom sector is mature, Vodafone's improved operating performance and low valuation make it an attractive investment opportunity.

Vodafone ( VODPF ) offers a high-dividend yield and an attractive valuation, making it interesting for long-term investors.

As I’ve covered in previous articles , Vodafone has several fundamental issues that are pressuring its share price, and a quick turnaround is not likely. However, the company continues to progress well on its strategy to streamline its business, and its high-dividend yield makes it an interesting income play for long-term investors.

In this article, I analyze its most recent financial performance and update its investment case, to see if it remains a good yield play or not within the European telecom sector.

Earnings Analysis

The telecom sector is mature, and growth prospects are, generally speaking, quite muted. As a company that is exposed to several markets across Europe, Vodafone is clearly not immune to this backdrop, explaining why its financial performance has not been impressive in recent years .

To unlock value, make the group less complex, and reduce debt, the company decided to sell part of its towers business, called Vantage Towers ( VTAGY ). In recent months, it announced a merger of its U.K. business with its competitor Three, which is owned by CK Hutchison Holdings Limited ( CKHUY ). The merger is still pending due to regulatory approvals. In addition, VOD has recently reached a deal to sell its Spanish business.

In Spain, Vodafone was not one of the largest operators, facing fierce competition from Telefonica ( TEF ) and Orange ( ORAN ), and this country was one of the main laggards within the group. The prospects of a turnaround were not great, leading Vodafone to decide to sell it instead of trying to perform another restructuring of its operations.

Vodafone was able to reach an agreement to dispose its Spanish unit for a total amount of €5 billion to Zegona Communications, which is distributed by €4.1 in cash and €900 million in Preference Shares no later than six years after closing. This deal was valued at 5.3x EV/EBITDA, which is an acceptable multiple for a unit that was reporting some weak financial figures, thus this can be seen as a positive factor for Vodafone.

Indeed, while this deal took some time to be executed, the valuation was higher than previously expected. When the news was first reported, the valuation was expected to be about €4 billion. Thus, Vodafone was able to extract more value from this sale, which is a positive outcome for the company.

Showing that Vodafone made the right decision to sell its Spanish unit, while Vodafone was able to report improved operating trends in Q2 FY 2024, Spain remained a laggard, reporting declining revenues compared to the same quarter of the last fiscal year.

As shown in the next graph, Spain accounts for some 6% of the group’s EBITDA and, together with Italy, is a unit that is reporting poor operating trends, both regarding revenues and profits.

Key regions (Vodafone)

On the other hand, the U.K. and other Continental Europe operations reported much improved operating trends, supported by higher pricing and good commercial momentum, which are positive signs about its business turnaround prospects.

However, investors should note that in the U.K. pricing is linked to CPI, thus recent increases were quite high and the country’s regulator wants to change the way price hikes are calculated. It was disclosed some days ago , that the U.K. telecom industry regulator wants to end price hikes linked to inflation for consumer contracts, which would be a negative factor for operators in the future. While this may only apply to new contracts going forward, and a final decision is only expected in Q2 2024, this could make it more difficult for operators to charge more due to rising inflation, which is not good for pricing power across the industry in the U.K.

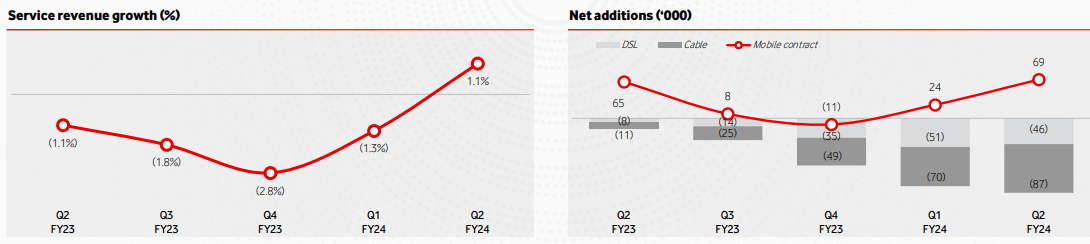

Regarding Germany, which is Vodafone’s largest market, it also reported improved operating trends over the past couple of quarters, showing that Vodafone’s actions on pricing and efforts to reduce customer churn are bearing fruit. In the last quarter, Vodafone was able to report higher revenue after several quarters of declining revenues, and also reported net additions, boding well for operating trends ahead. Given that Germany represents some 40% of its EBITDA, and is expected to increase its weight following the sale of the Spanish unit, this country is key to an overall turnaround of its business.

{kind=link}

Germany KPIs (Vodafone)

In growth markets, which include mainly Africa and Turkey, Vodafone maintained good growth momentum, while the business segment has also reported positive trends with Spain being the only exception.

Taking into account this backdrop, Vodafone’s service revenues increased by 4.7% YoY in Q2 FY 2024 , being the highest growth rate of the past six quarters. Despite good top-line growth, the inflationary environment continues to be a headwind for the company’s profitability, especially rising energy costs. Due to this background, its adjusted EBITDA on an organic basis increased by only 0.3% YoY to £6.4 billion in the first semester of the fiscal year 2024, leading to a drop in its EBITDA margin of about 60 basis points.

Regarding its cash flow generation, Vodafone continues to invest considerably in its 5G network and other infrastructure, leading to capital expenditures of €3.4 billion in the first half of the fiscal year, a slight decline from the same period of the previous fiscal year. It also had a significant cash outflow related to working capital, as the company increased headset inventory ahead of the holiday season, reflecting usual seasonality at the end of the calendar year. This led to negative free cash flow of about €2 billion in H1 FY 2024, while in the second half of the year this metric should be positive and, according to analyst’s estimates, its free cash flow should be around €2.5 billion in FY 2024.

Due to this seasonality in cash flow, its net debt increased to some €36 billion at the end of last September, leading to a net debt-to-EBITDA ratio of 2.7x (vs. 2.5x in FY 2023). Nevertheless, Vodafone’s guidance is to report stable EBITDA in FY 2024, thus its leverage ratio is expected to also be stable in the second half of the fiscal year. Going forward, this ratio should decline a little bit following the sale of its Spanish business, assuming that Vodafone will use these proceeds mainly to reduce debt, leading to a leverage ratio of 2.4x when the deal is completed.

Regarding its dividend, Vodafone has kept its interim dividend unchanged over the past four years. The next dividend is set to be paid next February, even though its ex-dividend date was last November. For the full year, its dividend is also expected to remain stable, which means that Vodafone is expected to remain a high-dividend yielder in the short term.

Indeed, due to a declining share price in recent months, Vodafone’s dividend yield is currently about 10.8%, which is quite attractive to income investors, and is more a reflection of undervaluation rather than poor dividend sustainability or prospects of a dividend cut ahead.

While the telecom industry is quite mature and a quick turnaround of its business is not likely, Vodafone is taking decisive actions to improve its operating performance and streamline its operations, which should have a positive impact on its long-term growth prospects. This is also supportive for its dividend, thus investors should see its high-dividend yield as an opportunity rather than being a warning sign about fundamental issues with the company.

Conclusion

Vodafone has reported an improved operating performance in the past couple of quarters, following several quarters of poor operating trends. This shows that Vodafone’s new strategy is bearing fruit more rapidly than I was expecting some months ago. While a turnaround will take time and Vodafone operates in a mature industry, its current valuation seems to be too harsh taking into account its actions performed in recent months to improve its business.

Indeed, Vodafone is currently trading at only 8.3x forward earnings, at a significant discount to its own historical average over the past five years at more than 14x. This is also cheap compared to its European peers, which trade on average at closer to 12x earnings, thus Vodafone seems to be an attractive income and value play right now.

For further details see:

Vodafone: Improving Operating Trends Support 10.8% Dividend Yield