VOD - Vodafone Needs To Change

2023-05-22 01:49:19 ET

Summary

- New CEO unveils a new restructuring plan.

- There was a further slowdown in Germany. Portfolio optimization needs to step in.

- A robust balance sheet and a positive dividend confirmation. We decided to lower price target, but maintain our buy rating.

Vodafone (VOD) performances are slowing down and unfortunately, we are not surprised. Last time, we anticipated Vodafone's negative trend with a publication titled ‘ Value Pick Or Value Trap? ’. Despite that, after having analyzed the recent quarterly update, we decided to confirm our buy rating ' Too Low To Ignore ’. Our analysis was supported by 1) higher interest from strategic buyers such as Iliad owner, 2) the company’s cost-saving initiatives, 3) portfolio optimization with Hungarian and Vantage Tower disposals, 4) and a tasty dividend yield with a compelling valuation within its closest peers on an FCF basis.

Q1 results

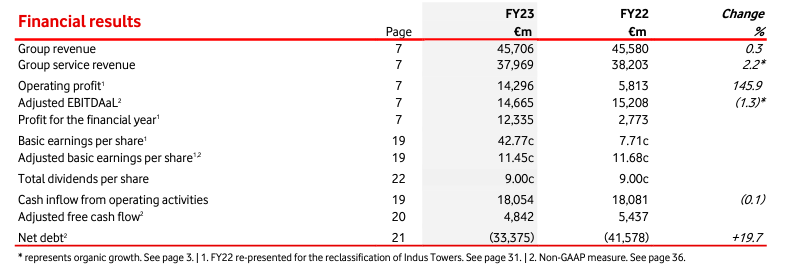

This week, the British red giant reported its figures and lost more than 6% of its market cap. In fiscal 2023, the British telecom reported revenues up by just 0.3% to €45.7 billion from €45.6 billion recorded last year. This result absorbs African growth, unfavorable currency rate developments, and lower revenues from European services. Over the year, the group's adjusted EBITDA decreased by 1.3% to €14.7 billion, and this was mainly due to higher costs and commercial underperformance in Germany (we already reported this negative trend in our latest analysis). Operating profit increased to €14.3 billion and net profit amounted to €12.3 billion (EBIT was €2.8 billion in 2022, but this increase is largely due to Vantage Towers' capital gain. The company's total DPS was confirmed at 9 cents, including a final DPS of 4.5 cents.

{kind=link}

Vodafone Financials in a Snap

Source: Vodafone press release

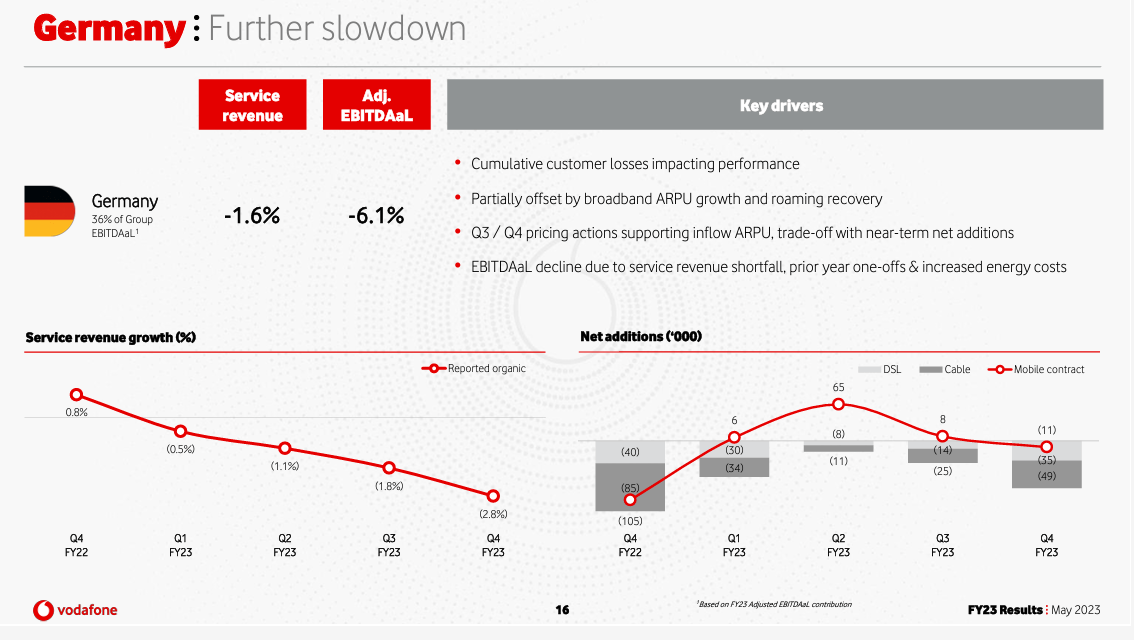

This EBITDA drop was already anticipated in our estimates but now with this announcement becomes clear that a bigger change is needed. Vodafone key challenges endure across the EU area and particularly in Germany. This was already visible in Q4. Even inorganic actions such as M&As could have the potential to reverse the negative trend; however, the impact of these attempts might take some time to show in the real numbers.

{kind=link}

Vodafone Germany development

Source: Vodafone results presentation

New CEO changes

The group has recently been in the hands of the new CEO, Margherita Della Valle, who highlighted that the revenues of this year will be largely flat and announced a plan to " recover competitiveness ". Here at the Lab, we positively view this new change. She started the conference call by stating that Vodafone's performance was " not good enough and to obtain constant results, Vodafone must change" . In the restructuring plans, there are 11,000 job cuts in three years, a project for the German recovery, and the launch of a strategic review in Spain. The new CEO declared that the moves have the aim to simplify the corporation. Already last March, in Italy, the company announced to the unions a restructuring plan that would have involved a 20% layoff of the total workforce.

{kind=link}

Telecom Sector aggregate stock price performance

As a reminder, his predecessor Nick Read left in early December after a four-year mandate and a sharp decline in the company's share price. Read resigned from office as the company was in talks to merge its United Kingdom operations with HK-based rival Three UK, owned by CK Hutchison group. According to local media , the deal is worth more than £15 billion. The new CEO Della Valle is a longtime Vodafone veteran who previously served as CFO and interim chief executive officer before being appointed to a permanent top role. It is going through a challenging period for the company. Lately, there have been two major developments to report.

Vodafone Business and RingCentral launched an integrated cloud-based communication solution on the Italian market that combines the messaging and video features of RingCentral with the fixed and mobile voice communication features of Vodafone Business. This will support Vodafone’s service revenues.

On the other hand, in February, Vodafone rejected an offer of €11.25 billion for the Italian assets by a consortium led by the Iliad. It was over before it even started. While Wall Street analysts were calculating synergies from the merger, the English giant essentially said "no thanks" with a concise statement in perfect British style. Vodafone confirmed that it had received an offer from Iliad, without indicating the assessment made by the French group that it would be supported by Apax Partners in the operation, but then explained that it judged the proposal not aligned. According to Iliad, the cash proposal was in the interest of the shareholders and would have satisfied the desire for Italian consolidation. At this point, the Iliad note still explains, in Italy Xavier Niel's group will continue to navigate alone and gain market share.

Do the M&A technical trials end here? Hard to tell. Iliad's offer, as Vodafone also underlined, was preliminary and certainly not binding. The market certainly didn't like the answer, which in a few hours brought the Vodafone share from positive to negative. According to Bloomberg , Vodafone's Spanish assets have also reportedly attracted the interest of potential buyers, including Apollo Global Management, The value? Over $4 billion. From what we understand, there is an air of consolidation among the European TLCs.

Conclusion and Valuation

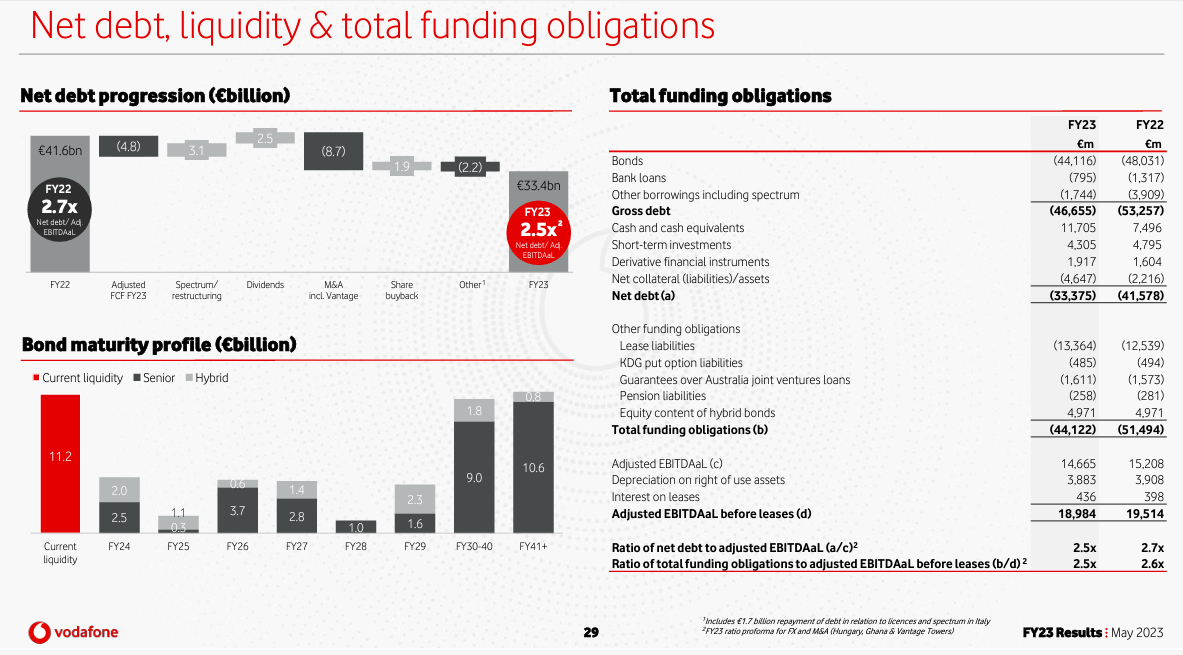

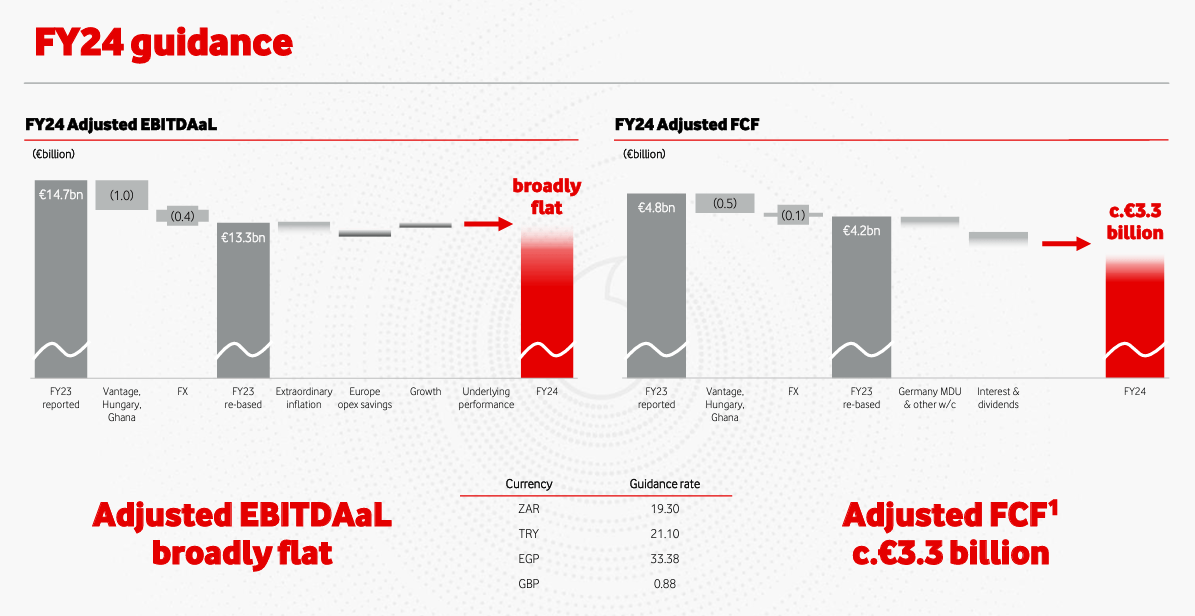

On a positive note, there was a significant reduction in net debt. Vodafone reached €33.4 billion on a proforma financial obligation with an adjusted EBITDAaL at now 2.5x. However, the EU TLC sector has the lowest ROCE, alongside the highest CAPEX. This resulted in WACC being lower than ROCE for over a decade. As a result, this impact Vodafone shareholder returns. This is why Vodafone was a hard call to make . With the new CEO, guidance has been resettled to the bottom with adj. FCF at approximately €3.3 billion, including dividend and working capital requirements, and an adjusted EBITDAaL remained at around €13.3 billion (broadly flat vs 2022). The company managed to beat adj. FCF internal estimates; however, the market was more focused on the recovery plan and the lower 2024 outlook projection. It is not uncommon that when a new CEO steps in, earnings are reviewed at the bottom (to surprise the market later). Despite that, on a free cash flow basis with a twelve-month visible period, and still valuing the company with its historical multiple on an EV/EBITDA, we decided to lower the Vodafone price target from £135 to £130; however, we still maintain a buy. Risks are included in our initiation of coverage .

{kind=link}

Vodafone net debt evolution

{kind=link}

Vodafone 2024 outlook

For further details see:

Vodafone Needs To Change