VOD - Vodafone: Potential Merger Of Italian Business Is Another Step In The Right Direction

2023-12-18 17:11:57 ET

Summary

- Vodafone has been taking steps to improve its business profile and unlock value, including potential business combinations in Italy.

- The company has improved its operating performance and reduced debt through measures such as selling its stake in Vantage Towers and reaching agreements to combine operations in the UK and sell its Spanish business.

- A potential merger with Iliad in Italy could help Vodafone gain size and become more competitive, while also reducing the number of operators in the country.

Vodafone ( VOD ) has been fixing its woes in its largest markets in recent months, and recent news about a potential business combination in Italy is another step in the right direction.

As I’ve covered in previous articles , Vodafone operates in a mature industry with relatively weak growth prospects, making its investment case highly geared to income. Nevertheless, since its strategy presentation at the beginning of the year, the company had taken some measures to streamline its business and unlock value, of which recent news about a potential business combination with Iliad in Italy were well received by the market.

In this article, I review Vodafone’s strategy and discuss how its potential deal in Italy can impact its business, to see if Vodafone’s current low valuation makes it an interesting value play or not.

Business Profile & Strategy

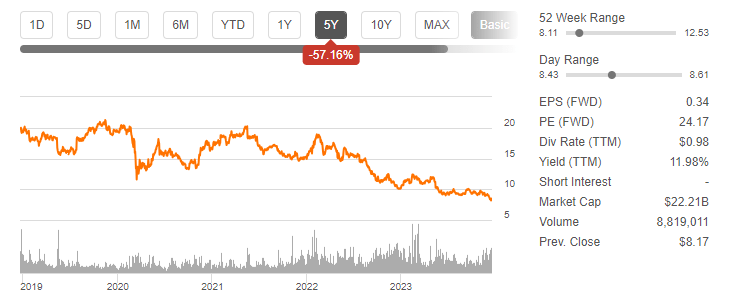

Vodafone is one of the largest telecommunications companies in the world, with operations across several European and African countries. It has more than 300 million mobile customers, 28 million broadband customers, and some 22 million TV customers across its markets. Its current market value is only about $22 billion and its shares are trading at a forward price-to-earnings ratio of only 7.2x, after several years of a clear downtrend in its share price.

{kind=link}

Share price (Seeking Alpha)

Vodafone has changed its CEO at the beginning of this year, and presented a new business strategy, which was not particularly well received by the market because it was not transformative enough to convince investors that Vodafone’s financial performance would change much in the future.

Despite that, Vodafone’s operating performance has improved more rapidly than I was expecting, as I’ve recently analyzed , and the company has taken some important steps to improve its business profile and deliver higher returns in the future.

Indeed, some months ago, Vodafone announced that it would sell its stake in the towers segment Vantage Towers ( OTCPK:VTAGY ), which enabled it to reduce its financial leverage and achieve an acceptable level within the telecoms industry, and also announced an agreement with CK Hutchison Holdings Limited ( OTCPK:CKHUY ) to combine the company’s operations in the U.K., with its competitor Three.

More recently, Vodafone also reached an agreement to sell its Spanish business to Zegona Communications, in a deal that can achieve a total amount of €5 billion (€4.1 billion in cash plus €900 million in Preference Shares no later than six years after the deal is closed).

This means that over the past six months, Vodafone has been able to monetize its towers business and reduce debt, which was one of the main market concerns, plus also reached a potential deal to become more competitive in the U.K. and to dispose a struggling unit within the group (Spain).

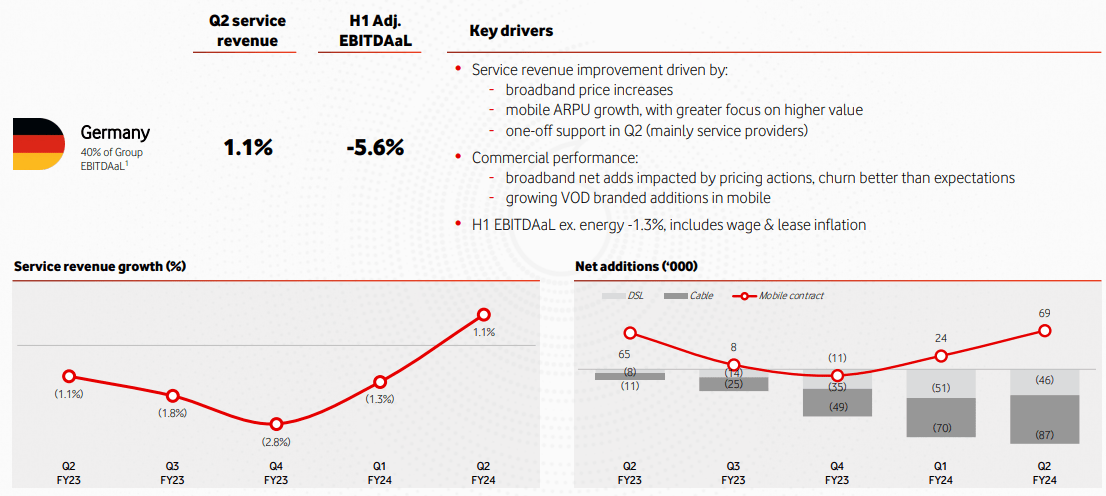

These measures are quite important because Vodafone’s largest markets are Germany, the U.K., Spain and Italy. In Germany, Vodafone has taken some measures in recent months to improve pricing and reduce customer churn, which are bearing fruit as the company has been able to improve its operating performance in the country over the past couple of quarters, as shown in the next graph.

{kind=link}

German KPIs (Vodafone)

As the company is expected to improve its market position in the U.K through the combination of its operations with its competitor Three and should dispose its Spanish unit over the coming months, Italy is the only large market where the company still needs to take further measures to address its struggling operations.

Like in Spain, Vodafone’s operations in Italy have reported very weak operating trends in recent years and a turnaround seems hard to achieve in the short term, as the market competition is quite fierce and Vodafone does not hold a leading position in the country. Indeed, Vodafone has reported a decline of 2.8% YoY in service revenue during Fiscal Year (FY) 2023, among the weakest performances within the group over the last year. In the first half of FY 2024, this unit reported lower service revenue again and a significant drop in EBITDA, being the clear laggard among Vodafone’s largest markets in Europe.

European markets (Vodafone )

In Italy, Vodafone operates both in the fixed and mobile markets, being the second-largest player after Telecom Italia ( OTCPK:TIIAY ), the Italian incumbent player. Telecom Italia holds a market share above 41% in the fixed wireline segment, while in the mobile segment is also the market leader with a market share of some 29.5%.

Iliad, a French telecom company, entered the Italian mobile market in 2018 with a low-cost strategy . Like it has done in France, the company undercut competitors’ pricing to gain new customers, being a major market disruptor and putting pressure on the largest players. In Italy, this has naturally led to lower revenues and higher customer churn at larger players, namely Telecom Italia and Vodafone, explaining to a large extent why Vodafone has reported weak operating trends in the country over the past few years.

Iliad is nowadays the fourth largest mobile operator in Italy, holding a market share of about 7.5%, the same market position it holds in its domestic market. In France, Iliad has a market share of close to 16%, thus Iliad’s strategy in Italy is not likely to change much in the near future, until it reaches a larger size, like it has achieved in its home market.

Vodafone’s previous CEO complained in the past about competition in Italy, and Iliad’s role in the market, saying that there were too many operators in Italy and that pricing was reaching unsustainable levels. Since then, market conditions have not improved much and costs related to fiber and 5G rollout are putting further pressure on the operator’s profitability and capital expenditures, explaining why Iliad has reportedly proposed a merger in Italy.

While Iliad is growing quite rapidly in Italy, this market is highly competitive and a business combination would allow the combined company to gain size and become more competitive with Telecom Italia. Vodafone was open to several options regarding its Italian unit, which could potentially also include a sale, thus this potential deal was well received by the market given that Vodafone’s shares are up considerably after this news.

Furthermore, Vodafone is reportedly also considering a potential deal with its competitor Swisscom ( OTCPK:SCMWY ), which holds Fastweb in Italy, thus this move by Iliad seems to be a way to offer a better deal to Vodafone and maintain a competitive position in the market, something that would be threatened by a potential combination of Vodafone with Fastweb.

According to Reuters, Vodafone had the following to say about this offer from Iliad:

Vodafone is supportive of in-market consolidation in countries where it is not achieving appropriate returns on invested capital and confirms it is exploring options with several parties to achieve this in Italy, including through a merger or a disposal.

This means that Vodafone is taking the right steps to improve its operating performance in its most important markets, and if it can’t reach a positive outcome by performing a turnaround on its own, it will seek the best way to create value for shareholders through a disposal. Investors should note that Vodafone has refused to sell its Italian operations last year to Iliad, in a €11.25 billion offer, as the valuation was seen as being too low.

Under this new deal, Vodafone would receive €6.5 billion in cash and a 50% stake in the combined business, plus a €2 billion shareholder loan to ensure long-term alignment. Iliad would receive €500 million and the same shareholder loan, plus an option to buy further 10% of shares at the same price as when the deal eventually closes.

Annual synergies of a potential merger could reach €600 million according to some analysts, thus this deal seems to be quite positive for Vodafone as it would monetize its stake in its Italian operations, reduce the number of operators in the country, and share the burden of future investments with Iliad.

If Vodafone eventually decides to sell the whole business, I think it would also be well received by the market, given that it would streamline its operations in markets with better profiles of return on invested capital, plus other markets where its growth prospects are stronger, namely in Africa. This would be a positive factor for a higher valuation in the future, given that Vodafone has struggled for years to improve its performance in challenging markets, Spain and Italy being two main concerns for investors.

Conclusion

While Vodafone is a mature company and has relatively weak growth prospects, it has taken decisive steps to improve its business profile in recent months, plus a potential deal in Italy is also very good news for the company. Beyond a very high-dividend yield, Vodafone is reporting improving operating trends and is fixing its most important markets, which should lead to higher investor confidence about its business prospects ahead.

However, this doesn’t seem to be currently reflected in its share price, which is trading at the lowest valuation over the past five years at only 7.2x forward earnings, thus Vodafone seems to be an interesting value play for investors that are willing to bet on positive turnaround prospects over the next few years.

For further details see:

Vodafone: Potential Merger Of Italian Business Is Another Step In The Right Direction